AU - AngloGold Ashanti: Tracking Above FY2023 Cost Guidance

2023-11-28 13:41:00 ET

Summary

- AngloGold Ashanti reported a decline in Q3 production and higher costs, with year-to-date costs tracking well above its guidance mid-point.

- On a positive note, its corporate restructuring is completed, its future in Nevada looks better than ever, and Obuasi's recent setback can be remedied with a change in mining methods.

- In this update, we'll look at the Q3 results, recent developments, and whether the stock has drifted into a low-risk buy zone following its recent underperformance.

Just over five months ago I wrote on AngloGold Ashanti ( AU ), noting that while it was successfully growing reserves in 2022, the stock was trading at a multiple well above its historical average at ~7.0x cash flow, suggesting there was no reason to chase the stock above US$24.50. Since then, AngloGold reported a softer than planned Q2 after a CIL tank failure at Siguiri, and while Q3 was an improvement, its Obuasi Mine ran into unfavorable ground conditions, affecting consolidated output. The stock has since seen a ~40% drawdown, which isn't surprising given the two consecutive misses combined with the stock being extended heading into its Q2 report.

On a positive note, AngloGold remains confident it will deliver into annual guidance despite the setbacks (Siguiri/Obuasi), it has a better Q4 on deck at Obuasi, and its corporate restructuring is completed (headquarters moved to Denver, primary listing on NYSE, and corporate domicile changed to UK), suggesting the potential for some multiple expansion down the road vs. previous multiples if it can execute successfully in Nevada and add another major Tier-1 mining jurisdiction at lower costs to its portfolio. In this update, we'll look at the Q3 results, recent developments, and whether the stock has drifted into a low-risk buy zone following its recent underperformance.

{kind=link}

Iduapriem Gold Pour - Company Report

Q3 Production & Sales

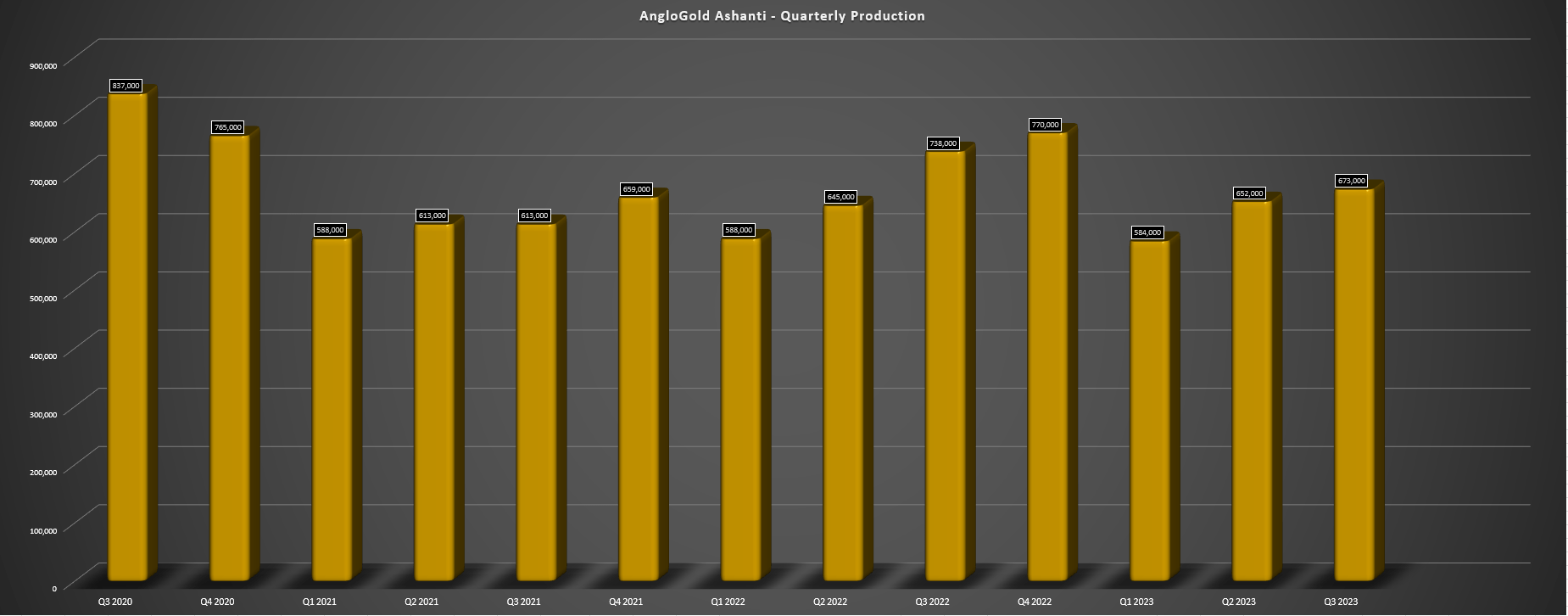

AngloGold Ashanti ("AngloGold") released its Q3 results earlier this month, reporting quarterly production of ~673,000 ounces of gold, a ~9% decline from the year-ago period (19% on a three-year basis with slower than planned growth at Obuasi unable to offset the divestment of its South African operations). This sharp decline in production year-over-year was partially related to placing its CDS Mine in care & maintenance at AGA Mineracao in August, in addition to another tough quarter at Obuasi in what's been a difficult stretch over the past few years (operator hit by underground LHD in 2020, sill pillar failure in May 2021). Fortunately, the most recent issue did not result in a fatality despite losing underground equipment in a fall-of-ground incident, and the company is confident it can overcome these challenges with a different mining method in these areas of the mine. Hence, while Q3 was the worst quarter since Q1 2022, we should see a much better Q4 with production of 80,000+ ounces (in line with year-end 2022 goal of 320,000 to 340,000 ounces).

{kind=link}

AngloGold Ashanti Quarterly Production - Company Filings, Author's Chart

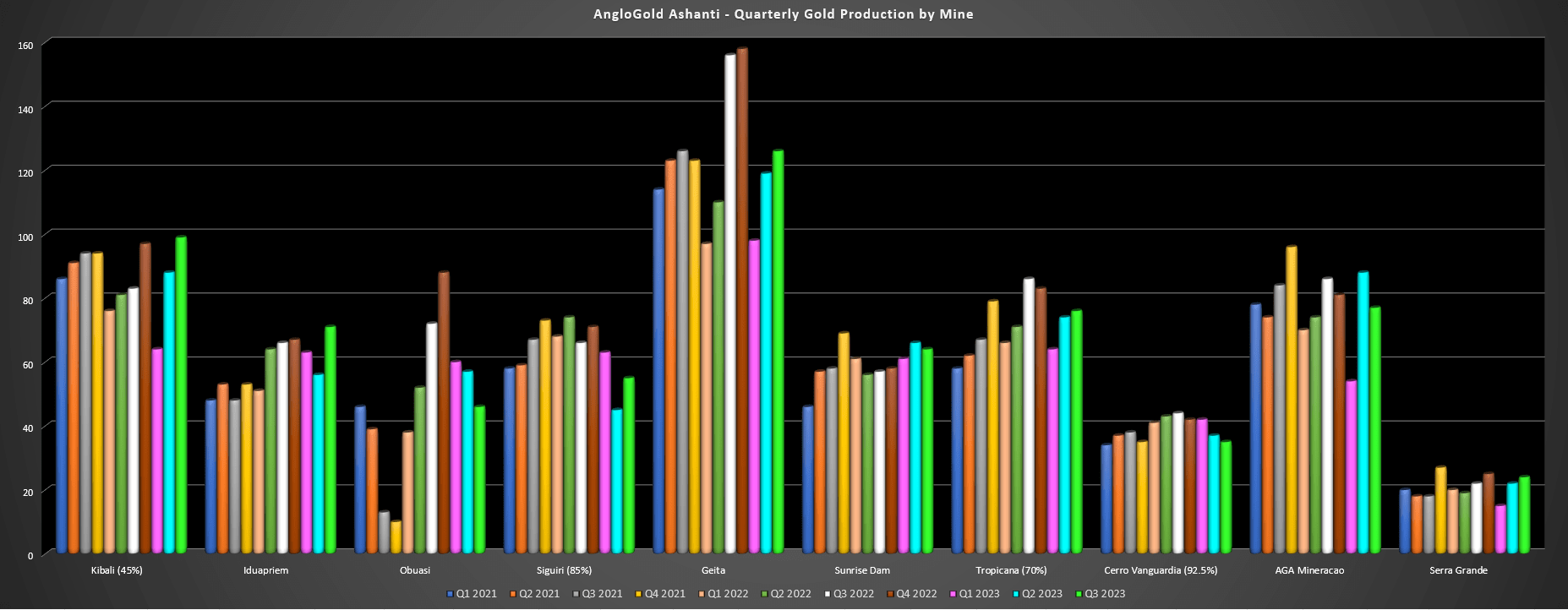

Digging into the operations a little closer, the company saw lower production year-over-year from its African segment, with lower production at Siguiri (~55,000 ounces), Geita (~126,000 ounces), and Obuasi (~46,000 ounces). At Geita, lower production at higher all-in sustaining costs [AISC] of $1,320/oz was related to sticky inflationary pressures, fewer ounces sold, and higher sustaining capital, with output down due to lower grades. On a positive note, the asset is still expected to produce ~500,000 ounces this year, maintaining its Tier-1 scale despite a 5% decline vs. last year's levels on a year-to-date basis. Meanwhile, the company's Siguiri Mine rebounded from the CIL tank failure in Q2, but higher throughput could not offset lower grades and costs were up meaningfully to $1,664/oz and $2,020/oz for cash costs and AISC, respectively. Finally, Obuasi's grades were lower because of difficult ground conditions (forced to reduce mining rates), with the much lower head grade of 4.43 grams per tonne of gold leading to a sharp drop in production.

{kind=link}

AngloGold Ashanti Quarterly Production by Mine - Company Filings, Author's Chart

Fortunately, the company's larger Kibali Mine saw meaningful growth year-over-year with ~99,000 attributable ounces produced on the back of higher throughput and grades of 3.22 grams per tonne of gold vs. 2.87 grams per tonne of gold in the year-ago period. This helped to improve costs when combined with taking the CDS Mine offline given the lower costs at this asset and much higher costs at CDS. It's also encouraging to hear that the company expects to replace reserves once again at this asset net of depletion. As for the company's other large Iduapriem Mine which is still awaiting approval for a combination with Tarkwa to create a larger and more profitable asset, production was up to ~71,000 ounces (Q3 2022: ~66,000 ounces), benefiting from higher throughput with the new TSF commissioned and better grades with mining in Block 7 and Block 8 Cut 2 A and B.

{kind=link}

Kibali Mine Operations - Barrick Gold

Moving over to Australia, production was down year-over-year to ~140,000 ounces (Q3 2022: ~143,000 ounces), at higher all-in sustaining costs of $1,453/oz. The lower production was related to Tropicana which offset increased production at Sunrise Dam given the lower throughput and lower grades. That said, it is encouraging to see Tropicana continuing to maintain its improvements from its Full Potential Program, with a 12% increase in production year-over-year driven by higher underground tonnes mined and processed. In fact, Q3 underground tonnes of ~659,000 tonnes is tracking towards the company's goal of increasing underground throughput from 2.6 to 3.0 million tonnes per annum, and we saw better costs at the asset year-over-year ($1,352/oz AISC vs. $1,430/oz) despite slightly higher sustaining capital given the higher volume sold.

Finally, the company's operations in the Americas also saw lower production year-over-year and continued to be a drag on the portfolio from a margin standpoint. This was evidenced by ~136,000 ounces produced at all-in sustaining costs of $1,629/oz vs. $152,000 ounces produced in the year-ago period at $1,644/oz. On a positive note, the company did see higher output adjusting for placing Cerro do Siti in care & maintenance in August, and it's also continued to work towards increasing its proportion of output from Tier-1 jurisdictions with an intense focus on adding ounces in Nevada and the decision to walk away from its 50% share in Gramalote which it sold to B2Gold ( BTG ). On this note, AngloGold continues to work towards first production in Nevada by 2026 with a Final Investment Decision for North Bullfrog expected next year assuming permits are granted in a timely manner.

Costs & Margins

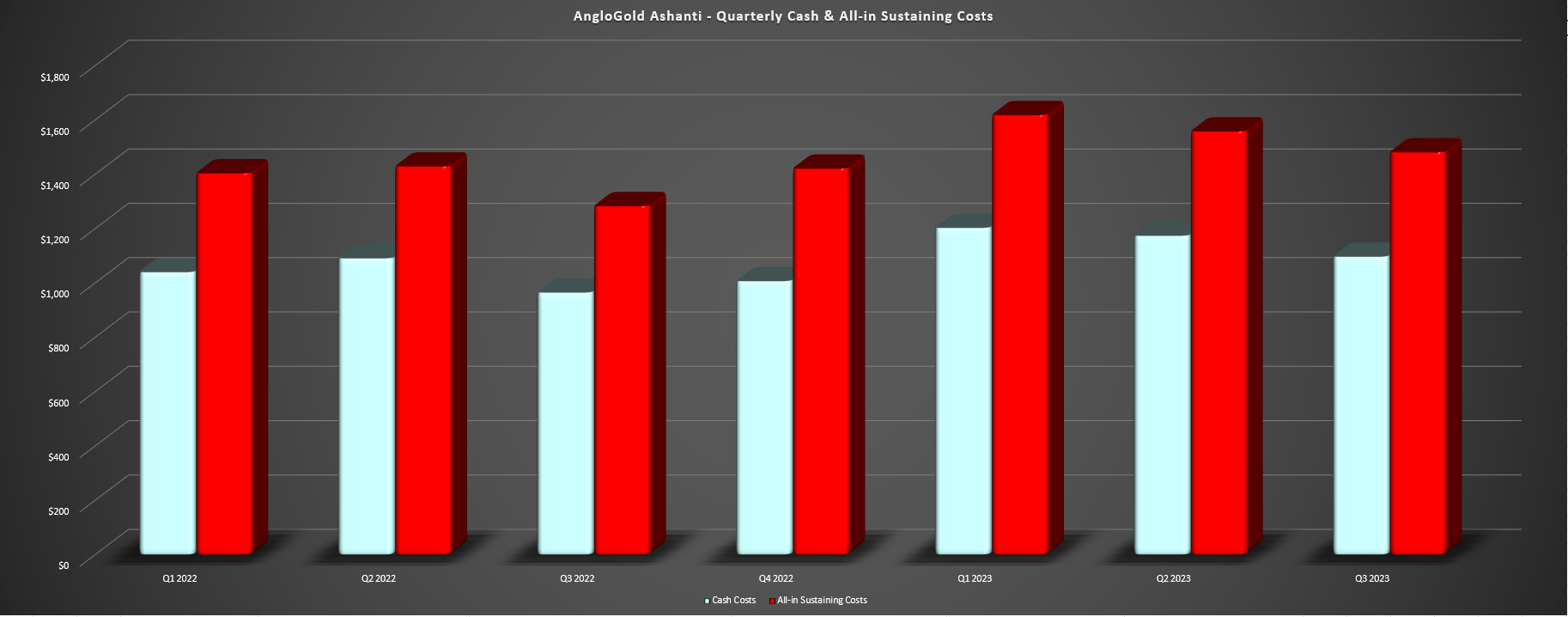

Looking at AngloGold's costs and margins, we saw a significant increase in all-in sustaining costs year-over-year to $1,559/oz (+20%) and cash costs were also up sharply year-over-year to $1,098/oz (Q3 2022: $966/oz). The increase in all-in sustaining costs was partially related to higher sustaining capital spend year-over-year which was a headwind, but cash costs continue to be well above the industry average and wiped out most of the benefit on a cash margin standpoint from the higher realized gold price vs. Q3 2022 levels ($1,717/oz). When discussing costs, AngloGold noted that inflation remains around 5% which is consistent with that communicated by Gold Fields ( GFI ) which operates in similar jurisdictions (Africa/Australia/South America). Hence, while there are gains to be had from the combination of Tarkwa and Iduapriem (if approved) and its Full Potential Program, I wouldn't expect a dramatic improvement in overall costs until it's able to bring low-cost Nevada operations into production.

{kind=link}

AngloGold Quarterly Cash Costs & AISC - Company Filings, Author's Chart

Looking at costs from a year-to-date basis, there wasn't much to write home about either given consolidated AISC of $1,550/oz, though year-to-date costs have been dragged up by underperformance at Siguiri ($1,832/oz year-to-date) and Obuasi ($1,647/oz year-to-date). On a positive note, even if Obuasi is well behind its stated goal of 400,000 to 450,000 ounces at $925/oz AISC by year-end 2023 as highlighted in its 2021 Annual Report, the recent setback is not a huge deal, and the company is continuing to make progress on Phase 3 which is now 82% complete (albeit pushed out to H2 2024). The other positive is that the estimated capital to complete redevelopment has not changed despite delays related to heavy rainfall and unanticipated levels of residual mud following dewatering. Plus, while Q3 was certainly disappointing, we should see a material improvement in costs with production set to increase another 60% in FY2025 (~400,000 ounces) if all goes to plan.

"When Phase 3 construction is completed at the end of 2023, Obuasi will be positioned to produce 400,000oz to 450,000oz a year at an all-in sustaining cost (AISC) of $900/oz to $950/oz."

- AngloGold Ashanti Annual Report 2021

As for addressing the poor ground conditions, AngloGold noted that it was back on track to more normal mining rates in October and its plan is to employ underhand cut and fill in more challenging areas of the mine vs. sub level open stoping previously. And although this is a higher cost mining method, it will allow for less dilution by mining more selectively and most importantly, safer extraction of ore. AngloGold noted that it is currently testing this new mining method and its COO has experience with the method, de-risking its implementation. To summarize, while costs were much higher than I anticipated in Q3 and year-to-date ($1,550/oz vs. guidance of $1,405/oz to $1,450/oz), we should see a better year for costs overall in H2 2024 vs. H2 2023, assuming Obuasi can make meaningful progress on its delayed ramp-up to full production levels, and there seems to be a path to much lower costs in 2029 if it can bring 300,000 ounces of low-cost Nevada production online.

Summary

AngloGold Ashanti had a disappointing Q3 and year-to-date costs are tracking well above its initial guidance mid-point of $1,428/oz with just one quarter to go. However, it's been a difficult year for the company at two key operations, and while this year has been below my expectations, there is a path to a re-rating later this decade if Obuasi can ramp up to 450,000 ounces and as the company de-risks its path to growth in Nevada (permits, FS level studies and start of construction on larger Nevada footprint). Although this points to a much higher share price in the long-run, the transformation won't happen overnight, and I still don't see enough margin of safety in AU at US$19.20 at ~6.7x FY2024 cash flow estimates. Hence, while I think this is an interesting turnaround story if it gets cheap enough and dips below US$15.30, I continue to focus on what I see as more attractive bets elsewhere in the sector.

For further details see:

AngloGold Ashanti: Tracking Above FY2023 Cost Guidance