AU - AngloGold Ashanti: Tracking In Line With FY2023 Guidance

2023-05-19 13:21:26 ET

Summary

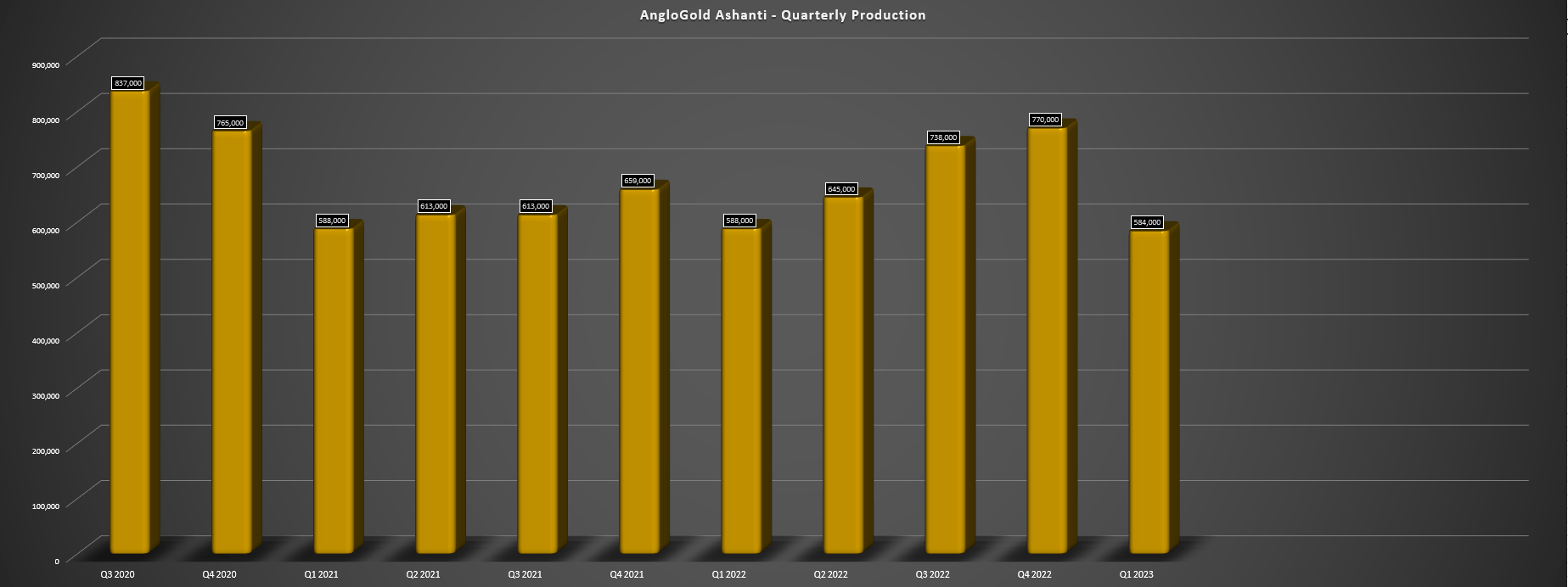

- AngloGold Ashanti released its Q1 results earlier this month, reporting quarterly production of ~584,000 ounces of gold, a 1% decrease from the year-ago period.

- Unfortunately, while output was down only marginally, costs rose to some of the highest levels sector-wide at $1,619/oz, and the company reported another free cash outflow despite higher gold prices.

- The good news is that it's making progress to reduce costs and between the Obuasi ramp-up, a low-cost Nevada mining hub, and Ghana JV, we should see lower costs post-2025.

- That said, I don't see enough margin of safety here at US$24.70, with the stock trading just shy of estimated fair value with one of the highest-cost profiles sector-wide for 2023/2024.

We're over three-quarters of the way through the Q1 Earnings Season for the Gold Miners Index ( GDX ) and one of the first companies to report its results was AngloGold Ashanti ( AU ). AngloGold Ashanti's ("AngloGold") results were slightly below my expectations with ~584,000 ounces produced at all-in sustaining costs of $1,619/oz, lending to inflationary pressures and slightly higher sustaining capital. And while the company remains on track to meet its guidance, this is another turnaround year for the company as it works to improve its balance sheet while investing to meet TSF-related regulatory requirements in Brazil and optimize its operations through its new Full Asset Potential program. Let's dig into the Q1 results below.

{kind=link}

Q1 Production & Sales

AngloGold Ashanti released its Q1 results earlier this month and reported a 1% decrease in gold production year-over-year, from ~588,000 ounces to ~584,000 ounces. While its African portfolio had a strong quarter with output up ~6% year-over-year to ~348,000 ounces on the back of higher output from Obuasi and Iduapriem, its Australian and Latin American assets had weaker quarters with production down 1% and 15%, respectively. The sharp drop-off in production in Latin America was due to significantly lower production at AGA Mineracao and Serra Grande, with lower grades and throughput at both assets. The lower sales volumes, combined with inflationary pressures, put a further dent in margins, and all-in sustaining costs soared to $2,446/oz (Q1 2022: $1,635/oz) at its Latin American region operations.

AngloGold - Quarterly Production (Company Filings, Author's Chart)

{kind=link}

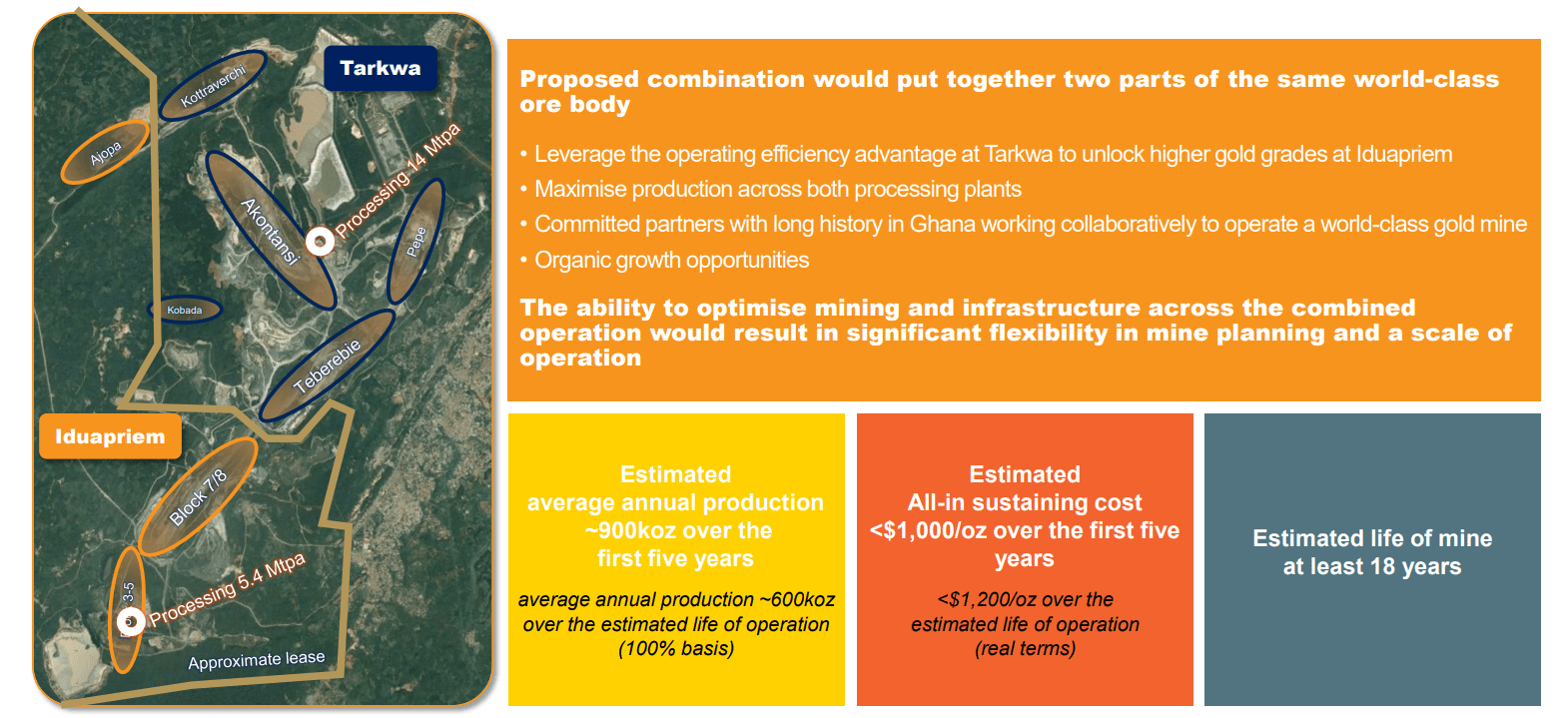

Digging into its African operations a little closer, Obuasi had a monster quarter with ~60,000 ounces produced vs. ~38,000 ounces in the year-ago period, benefiting from higher throughput and significantly higher grades of 7.74 grams per tonne of gold. And this asset will continue to improve over the next two years, with AngloGold targeting 400,000 ounces of production by the end of 2024. Elsewhere, Geita's production was flat at ~98,000 ounces. Meanwhile, at Iduapriem, Q1 output was ~63,000 ounces (Q1 2022: ~51,000 ounces), with higher throughput and grades. The notable development here is the planned joint venture to combine Tarkwa and Iduapriem into one Tier-1 scale asset, with an ownership of 60% Gold Fields ( GFI ), and 30% AngloGold.

Assuming the plans to amalgamate the two mines succeed, total processing capacity would increase to ~19.5 million tonnes and the combined operation would have an 18-year mine life, with 900,000+ ounces over the first five years at sub $1,000/oz all-in sustaining costs. Over the life of mine, both companies envisioned costs remaining below $1,200/oz, a significant improvement from FY2022 costs of $1,299/oz at Iduapriem and $1,248/oz at Tarkwa. This is certainly a positive development and I think this is a smart move by both companies and similar to what Barrick ( GOLD ) and Newmont ( NEM ) did in Nevada with Nevada Gold Mines to streamline operations and take the borders off to create lower-cost and more sustainable operations (albeit on a much smaller scale).

{kind=link}

Finally, looking at its Australian operations, Q1 production was down slightly to ~125,000 ounces on the back of lower production at Tropicana and flat production at Sunrise Dam. At Tropicana, waste stripping at the Havana Pit resulted in lower open-pit grades, offset the higher underground grades from Tropicana Underground. And similar to its Latin American operations, costs increased materially year-over-year to $1,309/oz and $1,564/oz for cash costs and all-in sustaining costs vs. $1,160/oz and $1,324/oz, respectively, in Q1 2022. On the positive side, the Full Asset Potential program is delivering as hoped at Sunrise, with monthly development rates up over 20% to ~1,200 meters per month with improved drilling performance.

{kind=link}

Costs & Margins

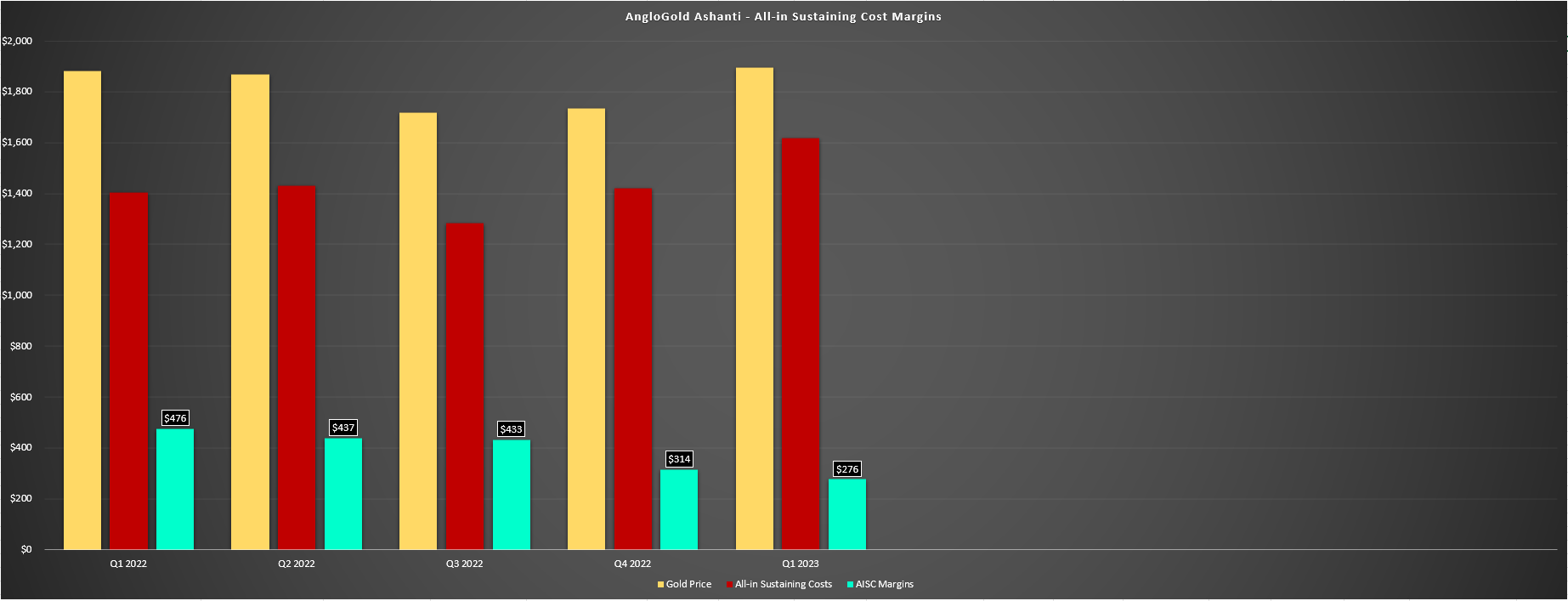

Moving over to costs and margins, AngloGold's all-in sustaining costs rose substantially in Q1, up 15% from $1,405/oz to $1,619/oz. These costs are over 23% above the estimated Q1 industry average of ~$1,300/oz, impacted by inflationary pressures that are up year-over-year even if they appear to have peaked in Q3/Q4 2022, and slightly higher sustaining capital expenditures. And while AngloGold's average realized gold price was slightly higher in the period at $1,895/oz, all-in sustaining cost margins dipped to $276/oz from $476/oz in the year-ago period.

AngloGold Ashanti - Costs & AISC Margins (Company Filings, Author's Chart)

{kind=link}

The good news is that commentary from Q1 Conference Calls sector-wide suggests that miners have seen the worst of the inflationary pressures after a tough two years, and with a stronger average realized gold price in Q2, AngloGold should see an improvement in margins sequentially (Q2 vs. Q1). Plus, from a bigger standpoint, Obuasi will be a much higher-margin operation if it can sustainably operate at 360,000+ ounces per annum (50% higher than its current production profile), its Iduapriem asset will see improved costs with synergies if the joint-venture plans are successful, and its Nevada mining-hub with above average open-pit grades will provide a lift to AngloGold's total output at much lower costs. So, while the current cost and margin profile leaves a lot to be desired, there is a path back to sub $1,350/oz AISC.

Finally, from a financial standpoint, AngloGold reported a cash outflow of $161 million in Q1 on the back of higher capital expenditures and lower margins. This resulted in an increase in net debt to ~$1.13 billion. That said, while 2023 was expected to be a disappointing year from a free cash flow standpoint using a conservative $1,800/oz gold price assumption, the gold price is certainly providing a tailwind, and this high-cost producer should have a decent year if the gold price can remain above $1,900/oz, translating to AISC margins closer to ~$500/oz vs. expectations of ~$350/oz previously. Let's take a look at AU's valuation and technical picture.

Valuation & Technical Picture

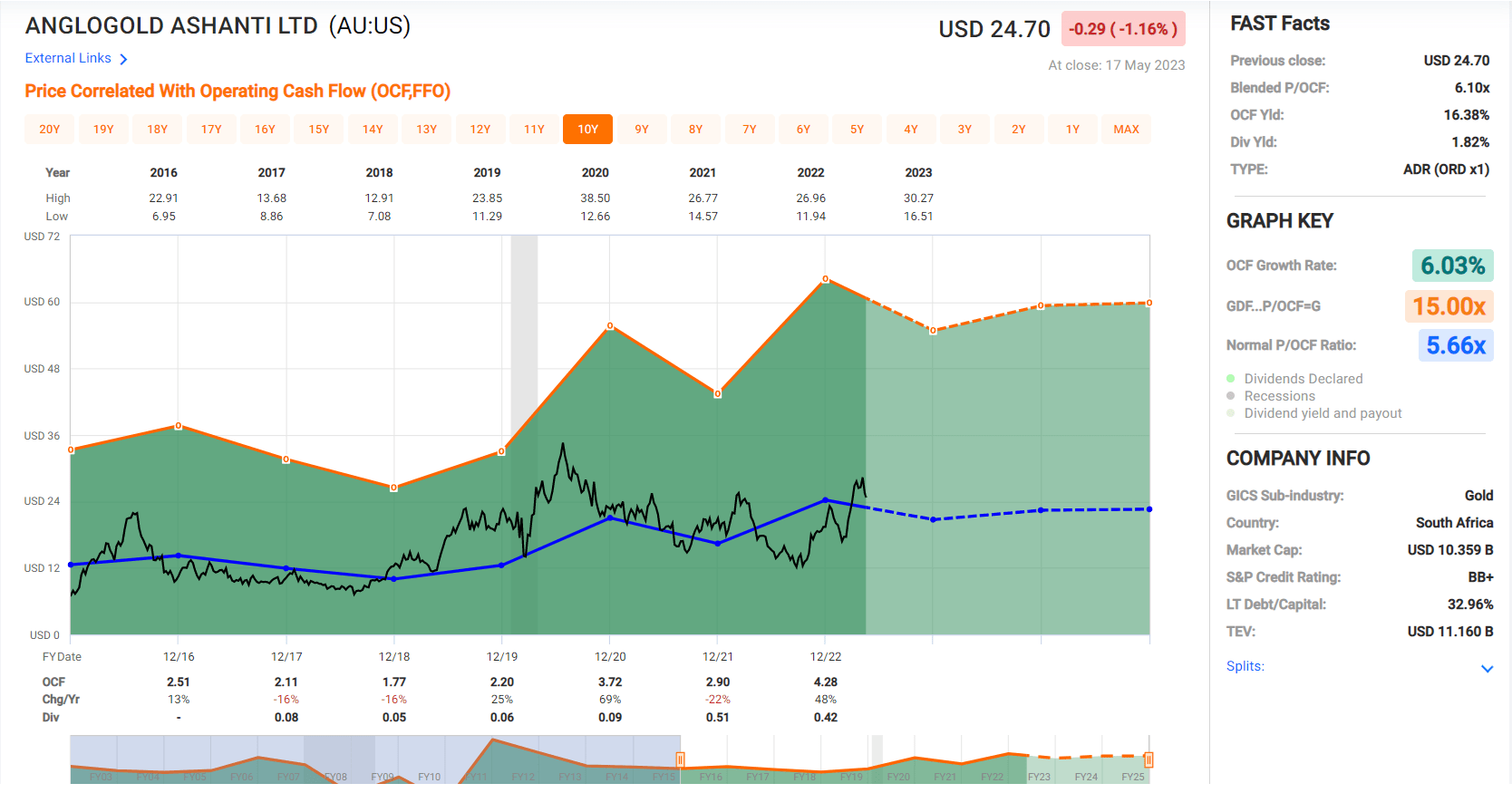

Based on ~421 million shares and a share price of US$24.70, AngloGold trades at a market cap of $10.4 billion and an enterprise value of ~$11.5 billion. This leaves it trading at a significant discount to Newcrest Mining ( NCMGF ) despite a similar production profile, but it's important to note that the two companies could not be less similar from a margin standpoint, with Newcrest guiding for all-in sustaining costs of ~$1,000/oz with a $3.45/lb copper price assumption in FY2023, while AngloGold is guiding for all-in sustaining costs of $1,425/oz in 2023. This places AngloGold well ahead of its peer group from a cost standpoint, and it also has less than 20% of production coming from Tier-1 jurisdictions (Newcrest: ~60%).

{kind=link}

This inferior margin profile and jurisdictional profile help explain AngloGold's discount from a valuation standpoint relative to peers, not to mention that Newmont has paid what I would argue is a rich price for Newcrest in its recent transaction even if there are some clear synergies. In fact, AngloGold has historically traded at just ~5.7x cash flow, one of the lowest cash flow multiples among the million-ounce producer peer group. Based on what I believe to be a fair multiple of 6.3x cash flow (15% premium to 10-year average) to account for its increasing exposure to Tier-1 jurisdictions later this decade, an improving cost profile and its proposed joint venture to create a larger and lower-cost asset (Iduapriem/Tarkwa) and FY2023 cash flow per share estimates, I see a fair value for the stock of US$22.70.

{kind=link}

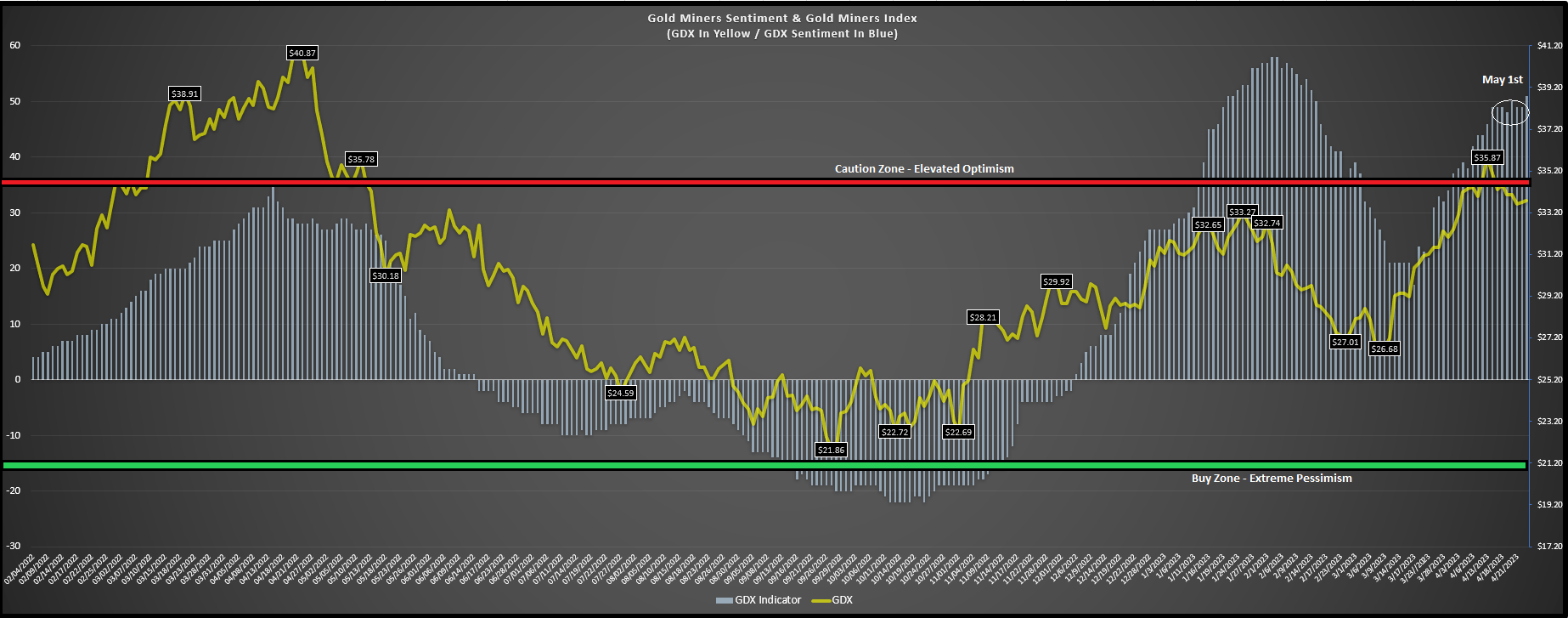

Even if we assign an additional $1.2 billion in value to assets that could be divested (Gramalote) and its Nevada portfolio or $2.85 per share, this still translates to a fair value of just US$25.55 per share, only marginally above where the stock is trading currently. Hence, despite AngloGold's recent pullback from its highs, the stock still looks close to fully valued relative to its historical multiples. And while a rising tide will lift all boats as it did AngloGold last month, the gold price's upside momentum has dissipated and sentiment on miners was in nosebleed territory (semi-exuberant) as of early May (shown above), suggesting it's hard to rule out further downside for the stock.

{kind=link}

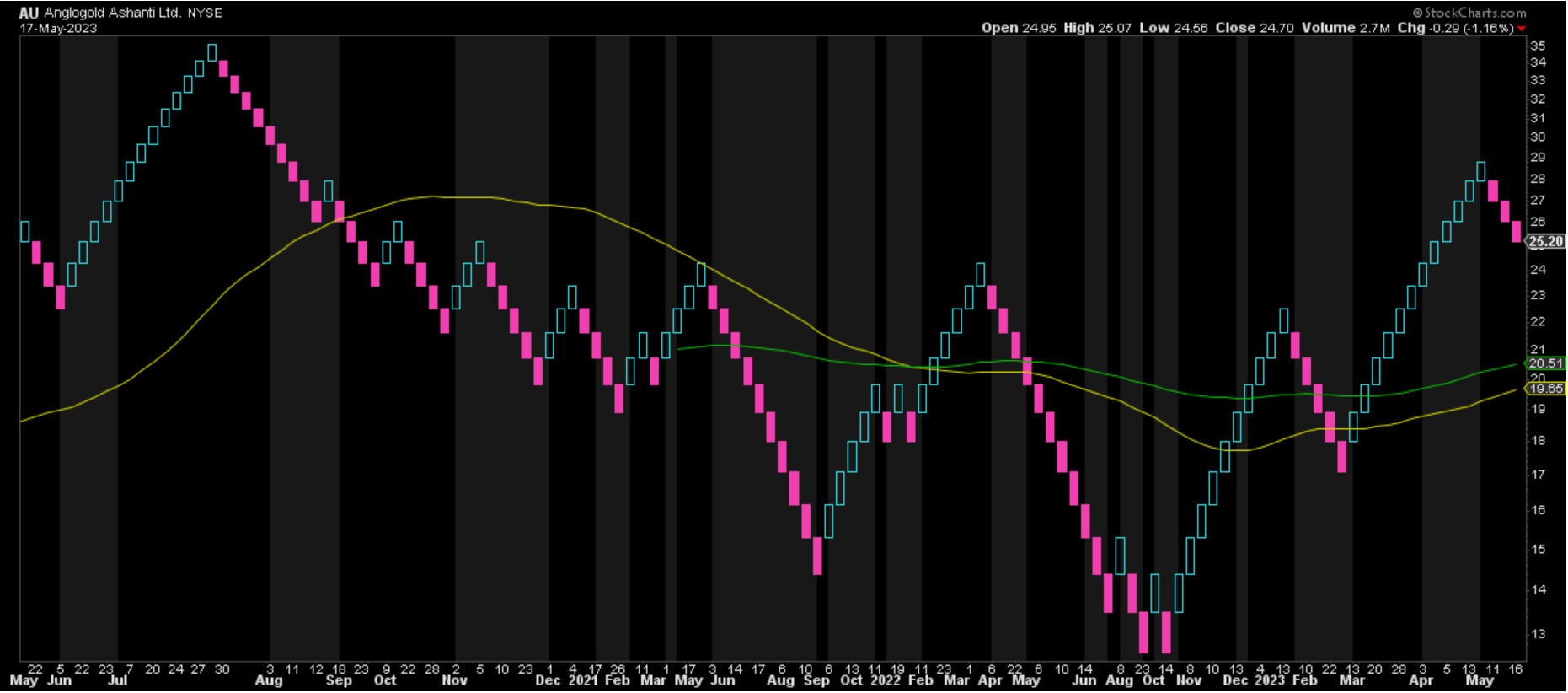

Finally, if we look at the technical picture, AngloGold is trading in the upper portion of its support/resistance range, with a new resistance level at US$26.75, and no strong support until US$16.55. This doesn't mean that the stock has to drop back below US$17.00 and revisit support, but from a reward/risk standpoint, AngloGold's setup remains unattractive with a reward/risk ratio of 0.25 to 1.0. Hence, if we were to see a rebound in the stock back above US$26.20 before July, I would view this as an opportunity to book some profits.

Summary

AngloGold's Q1 results were mediocre with one of the highest-cost profiles sector-wide and relatively flat output, plus continued free cash outflows. The good news is that progress continues to be made across the portfolio, with a low-cost production hub set to start up by 2026 in Nevada, ongoing work on its Full Asset Potential program to reduce costs, and Obuasi's costs set to improve as it ramps up towards ~350,000 ounces by year-end 2024. This should help AngloGold maintain its large production profile at more respectable costs and help it return to a consistent free cash flow generator even at conservative gold prices.

That said, the stock isn't cheap here at US$24.70 and there are multiple open gaps below the current price, so I continue to see far more attractive bets elsewhere in the sector.

For further details see:

AngloGold Ashanti: Tracking In Line With FY2023 Guidance