AU - AngloGold Ashanti: Turnaround Thesis Intact

Summary

- AngloGold Ashanti is one of the top-performing stocks since the October lows, up more than 80% in less than 100 trading days.

- This strong recovery from multi-year lows can be attributed to the stock's dirt-cheap valuation three months ago, combined with rising gold prices that have improved sentiment sector-wide.

- However, while the turnaround story is intact at AngloGold, evidenced by improving safety trends, reduced leverage ratios, and declining operating costs, much of this looks priced into the stock.

Just over three months ago, I wrote on AngloGold Ashanti ( AU ), noting that while the company had seen a dent in its development pipeline with the outlook for Quebradona/Gramalote being less clear, significant negativity was priced into the stock as it hovered near support at US$12.70. Since then, the stock has enjoyed an 80% plus rally in less than 90 trading days, making it one of the best performers in the sector. However, while this has undoubtedly improved the stock's momentum, it's left it in a vulnerable position where it's susceptible to a sharp correction. Hence, I see this rally above US$22.40 as an opportunity to book some profits.

Tropicana Operations (Company Website)

{kind=link}

Q3 Results

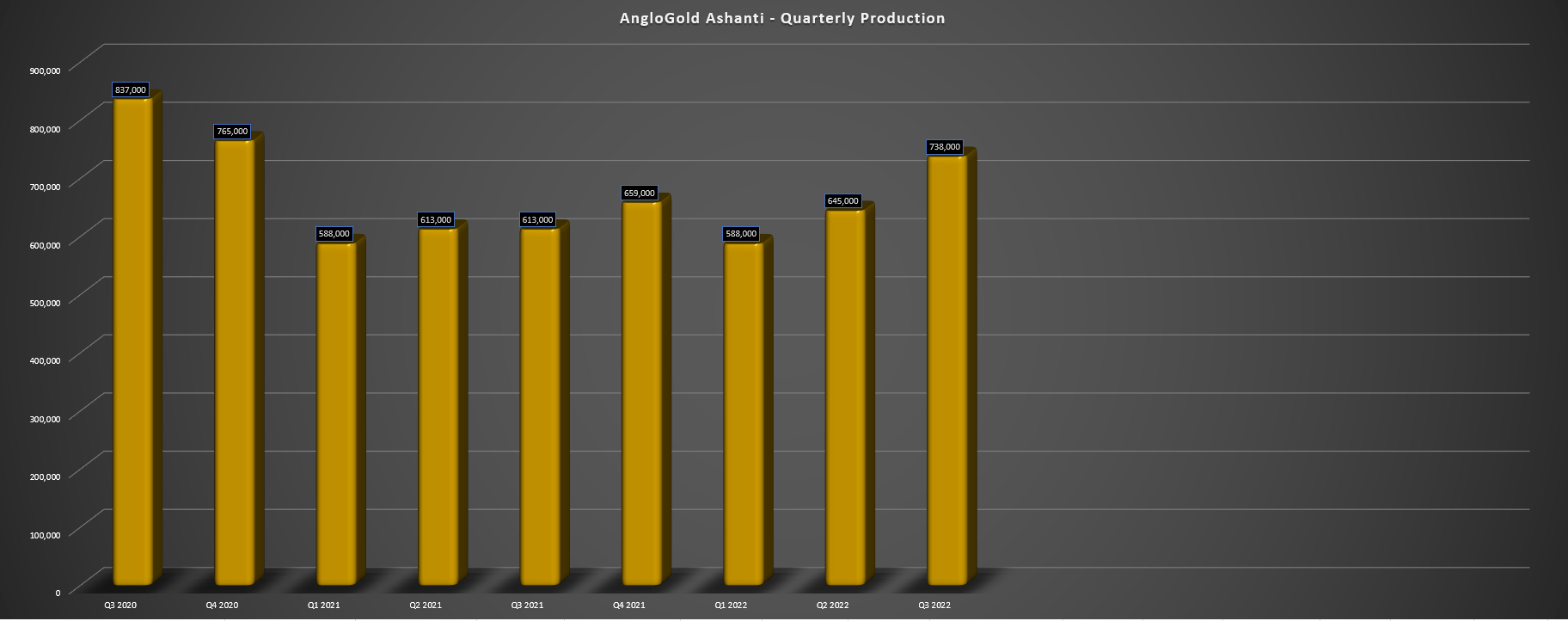

AngloGold Ashanti ("AngloGold") released its Q3 results in November, reporting quarterly production of ~738,000 ounces of gold, a significant increase from the year-ago period. The increase in production was driven by higher grades and throughput at most of its operations, with the most significant increases coming from Obuasi (~72,000 ounces), Geita (~156,000 ounces), Iduapriem (~66,000 ounces), Tropicana (~86,000 ounces), and Serra Grande. Notably, after a tough year in 2021 related to a fall of ground incident, Obuasi is on track to meet FY2022 guidance of 240,000 to 260,000 ounces and should see production ramp up to 400,000+ ounces at sub $1,000/oz costs in 2024 once Phase 3 work is completed this year.

AngloGold - Quarterly Gold Production by Mine (Company Filings, Author's Chart)

{kind=link}

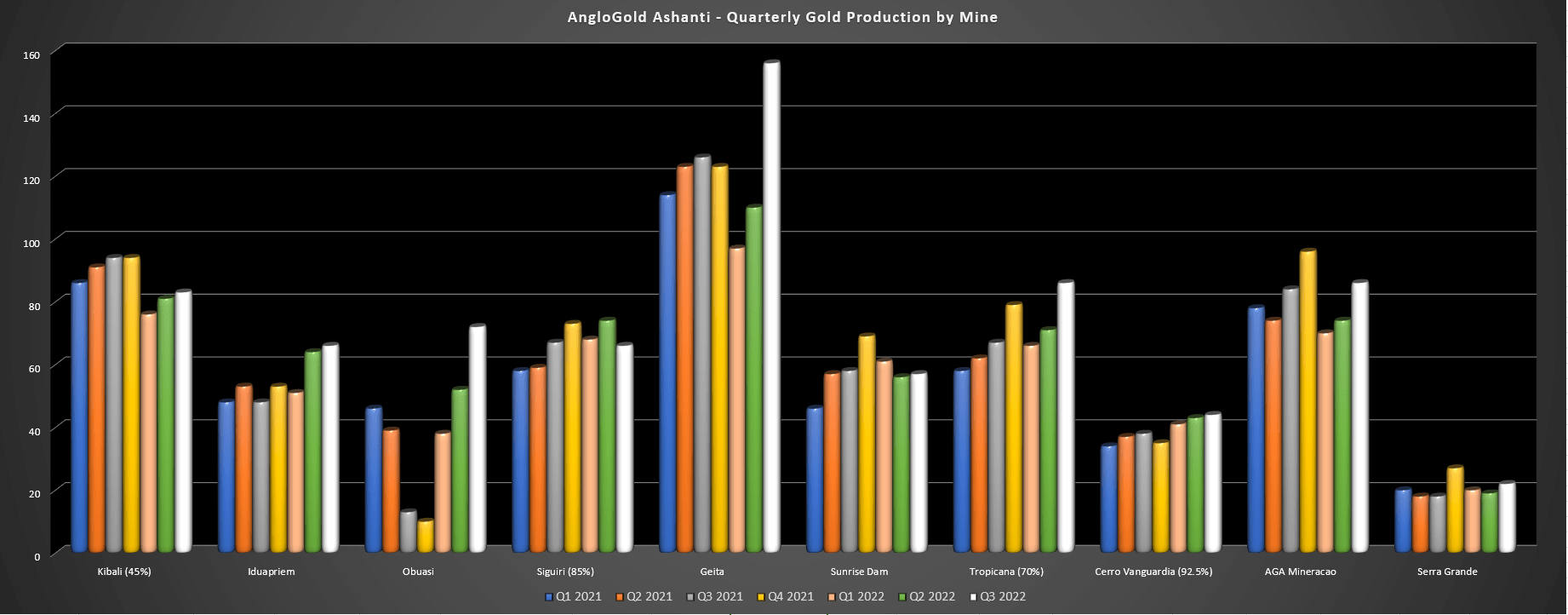

If we look at quarterly production by mine, we can see that nearly every operation saw higher production in Q3, except Kibali (45%), Siguiri (85%), and Sunrise Dam. The lower output at Kibali was related to lower grades mined. Meanwhile, Siguiri saw a dip in output due to mining disruptions related to protests related to employment demands, leading to fewer tonnes processed. Finally, Sunrise Dam saw a marginal decline in production due to lower recovered grades. Fortunately, this was more than offset by the increased production at other assets, especially with Geita and Obuasi having monster quarters from its African segment.

AngloGold Ashanti - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

Moving over to cost performance, AngloGold was not immune from inflationary pressures, calling out higher fuel, labor, and consumables costs. Fortunately, this was offset by increased output. The result was that all-in-sustaining costs (AISC) dipped to $1,284/oz in the period, a significant improvement from $1,362/oz in Q3 2021. However, while this was an improvement, AngloGold was up against easy year-over-year comps with elevated costs in the year-ago period. That said, the company still saw a $26/oz negative impact in the period from its Brazil TSF compliance program, where it is converting to dry-stack tailings facilities at all its mine sites. Plus, despite the weaker gold price, AISC margins were up slightly year-over-year ($433/oz vs. $423/oz), though still below the industry average.

AngloGold - Gold Price, All-in Sustaining Costs & AISC Margins (Company Filings, Author's Chart)

{kind=link}

Finally, AngloGold generated $169 million in free cash flow in the period (Q3 2021: $17 million), benefiting from higher sales volume and lower capital expenditures. This helped the company to end the quarter with an improved cash position of ~$1.2 billion and net debt of roughly $750 million. As the chart below shows, the company's net debt has continued to improve, as have its leverage ratios, and I would expect this to continue with higher free cash flow as the TSF compliance program winds down, and the company benefits from a higher gold price, with an added benefit from optimization work at individual assets under its Full Asset Potential program.

Recent Developments

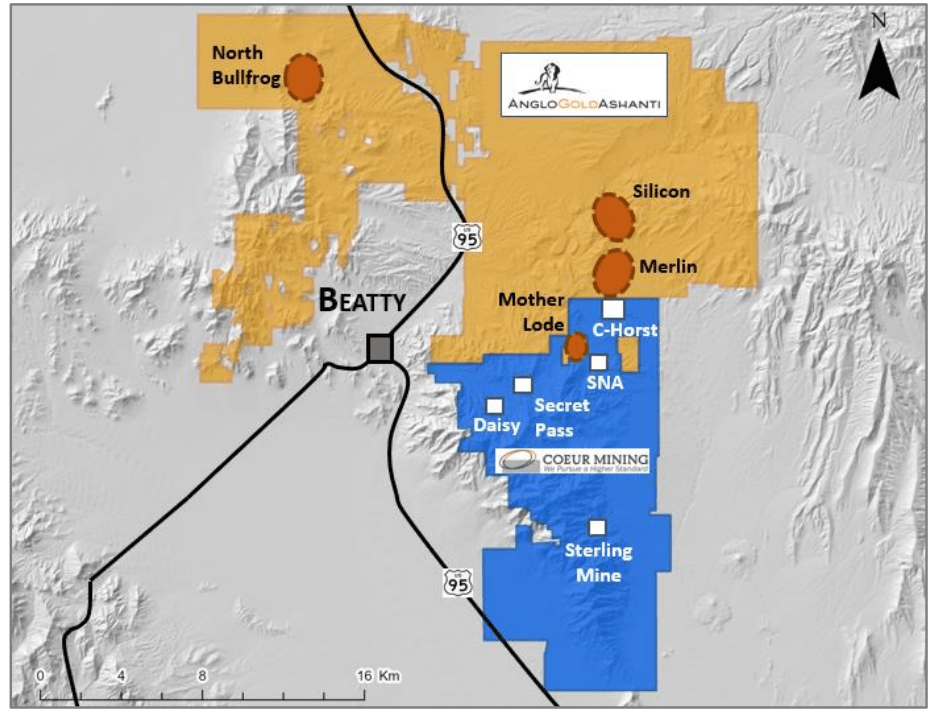

Moving over to recent developments, the major news in the quarter was that Obuasi reached Phase 2 commercial production at the end of Q3 and is on track for a solid year with further growth expected post-2023 (increasing mining rates to 5,000 tonnes per day). This will be driven by upgrading the KMS/KMV shafts, developing a new vent shaft, and progressing development to access Block 11. Meanwhile, from a development standpoint, AngloGold announced that it would be acquiring Coeur Sterling, Inc. for $150 million from Coeur Mining ( CDE ) to secure key land in the Beatty District of Nevada next to its already large tenements. The acquisition is subject to a contingent payment of $50 million if 3.50 million ounces are defined vs. a current resource of ~1.0 million ounces.

AngloGold - Beatty District Land Position (Company Website)

{kind=link}

As the image above shows, this is a very strategic acquisition given that it adds considerable land just south of the company's Merlin and Silicon deposits and surrounding its Mother Lode deposit which was acquired from Corvus Gold (in addition to North Bullfrog and surrounding land) last year. While I think the price was arguably a little high, it's hard to put a price on strategic ground that takes the border off what could be a future mining complex in Nevada for AngloGold Ashanti and help improve its jurisdictional profile. As it stands, AngloGold expects the first production from Nevada by 2026, with a goal to produce ~300,000 ounces at sub $1,000/oz costs by the end of the decade. If achieved, this would provide an 11% boost to production vs. FY2022 guidance.

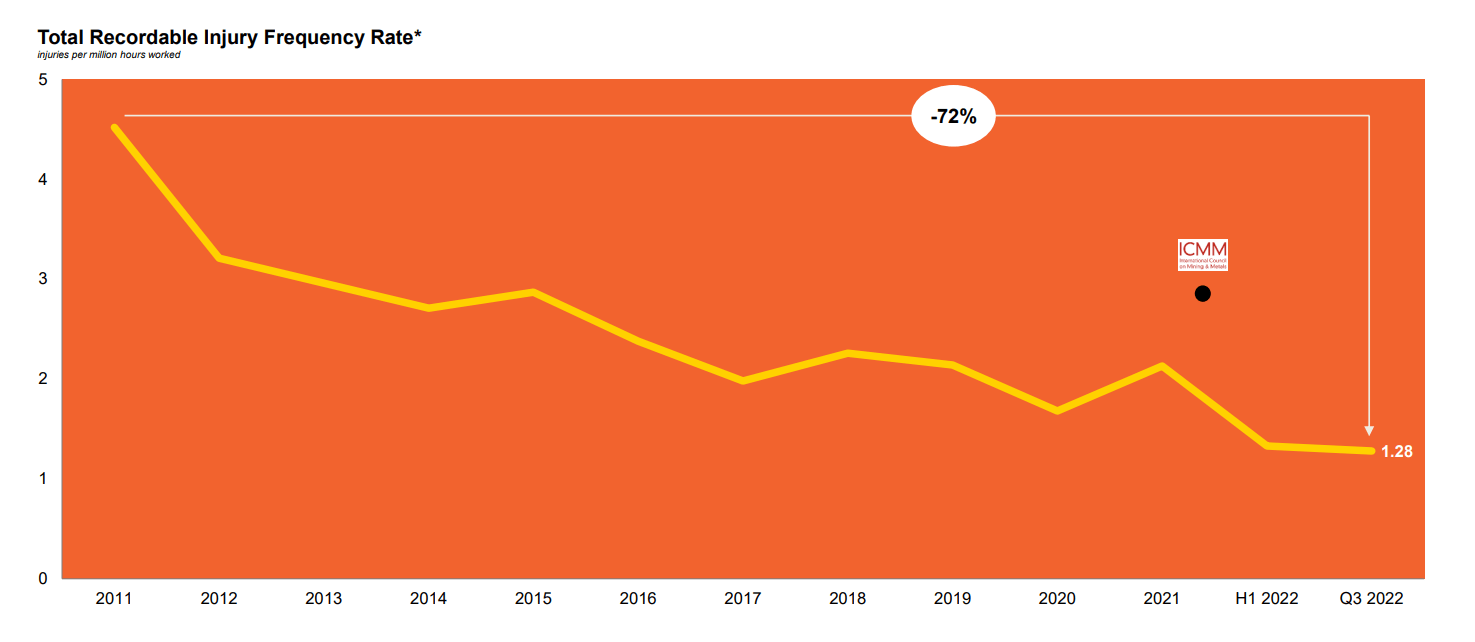

Finally, if we look at AngloGold's safety trends, there's a lot to be encouraged about here since Alberto Calderon took over in 2021. In fact, AngloGold has made major strides over the past 18 months, with its Total Recordable Injury Frequency Rate ((TRIFR)) declining sharply to multi-year lows at 1.28. Some investors may brush off worker safety as a secondary or tertiary metric, choosing to focus most on operating performance and costs. However, this is a mistake, and the importance of safety cannot be understated. One example is Alcoa ( AA ) in 1987, which placed safety above everything else when former CEO Paul O'Neill came on board, with the below excerpt from his tenure (1987-1999) there as follows:

" I knew I had to transform Alcoa. But you can't order people to change. So I decided I was going to start by focusing on one thing. If I could start disrupting the habits around one thing, it would spread throughout the entire company."

- Alcoa CEO, Paul O'Neill

AngloGold - TRIFR Performance (Per Million Hours Worked) (Company Presentation)

{kind=link}

O'Neill's decision to focus on safety worked masterfully because one keystone habit can generate a massive ripple through an organization. In Alcoa's case, an increased focus on safety led to better workplace practices, better worker morale, and ultimately a more efficient workplace - from manufacturing to everyday tasks. It worked so well for Alcoa that net income tripled from when O'Neill began his tenure as CEO, proving that being laser-focused on one keystone habit can be a recipe for success. So, after two years of inflationary pressures taking a bite out of margins sector-wide, it is encouraging to see AngloGold making substantial progress in this critical operating metric, which could be a leading indicator for improved operational performance.

Let's dig into valuation to AngloGold's valuation to see whether this turnaround story is priced attractively:

Valuation & Technical Picture

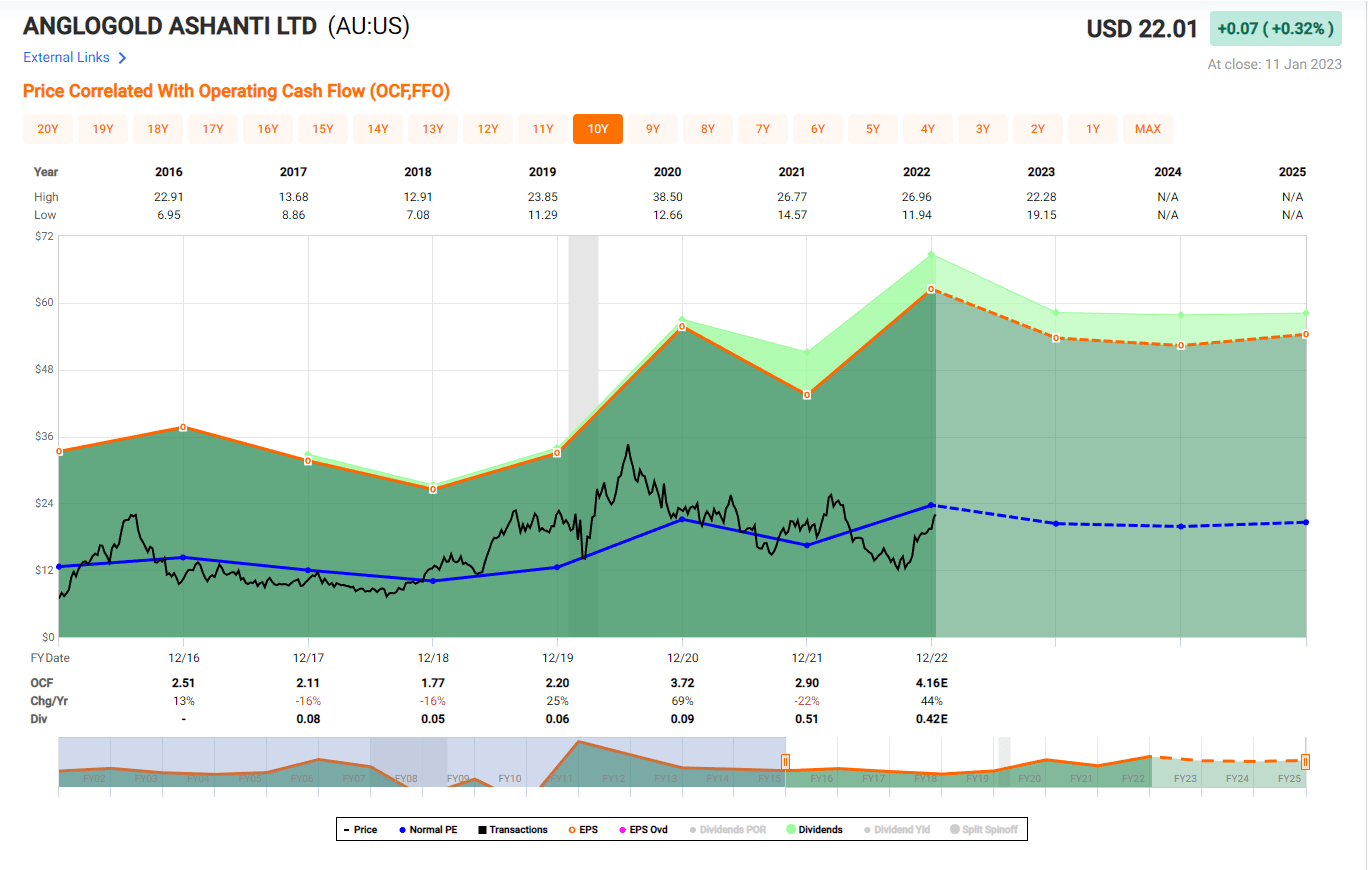

Based on ~420 million shares and a share price of $22.50, AngloGold trades at a market cap of ~$9.45 billion or an enterprise value of ~$10.3 billion. I would argue that this is becoming an expensive valuation for this future ~3.0 million-ounce producer, especially given that its costs continue to lag the industry average, and it also operates out of some less attractive jurisdictions (Tanzania, DRC, Argentina, Brazil). In fact, AngloGold has now found itself trading at a premium to its historical cash flow multiple (10-year average: 5.5x) based on FY2023 cash flow per share estimates of $3.65, currently sitting at 6.2x forward cash flow.

Based on what I believe to be a more conservative multiple of 5.5x cash flow and more conservative FY2023 cash flow estimates of $3.55, I see a fair value for AngloGold of US$19.50, leaving the stock more than 15% above fair value currently. Obviously, a rising gold price will lift all boats, and the stock could certainly beat FY2023 estimates if the gold price continues cooperating. Still, given that the gold price can be quite volatile, I prefer to use more conservative estimates, and under these assumptions, I don't see any value in AngloGold Ashanti here. I generally prefer a minimum 30% discount to fair value to justify buying new positions, which would require a dip below US$14.00 for me to become interested in the stock.

AngloGold - Historical Cash Flow Multiple (FASTGraphs.com)

{kind=link}

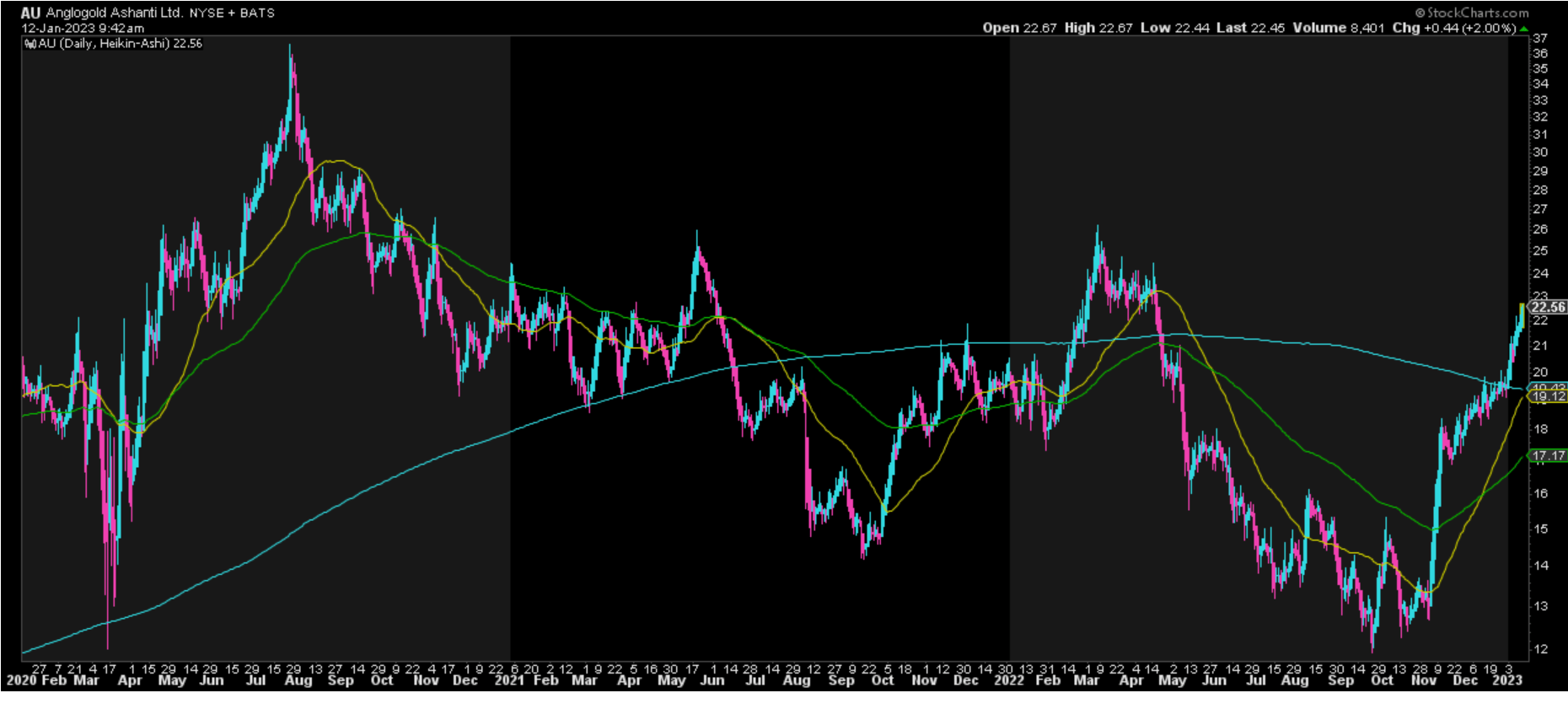

Moving to the technical picture, we can see that AngloGold has hopped back above its moving averages, which is positive from a momentum standpoint. Still, it's now sitting within 10% of strong resistance at US$24.60 - $24.90. Meanwhile, the next strong support level doesn't come in until US$13.30 - US$13.50. This translates to a reward/risk ratio of 0.30 to 1.0 when measuring the potential upside to resistance vs. potential downside to support, with this being an unfavorable reward/risk ratio. I generally prefer a minimum of a 5 to 1 reward/risk ratio to justify starting new positions, and the stock isn't remotely close to this setup currently. Hence, with the valuation no longer attractive and the stock being short-term extended, I see this as an opportune time to book some profits.

AU 2-Year Chart (StockCharts.com)

{kind=link}

Summary

With AngloGold Ashanti being in the penalty box after a tough year in 2021 and a slow start to FY2022, the stock became very attractively valued below US$13.00, setting up a low-risk buying opportunity in September. Since then, the company has continued to make progress and has beefed up its development pipeline in Nevada, potentially placing it on track to create a new Tier-1 jurisdiction mining complex by 2030. However, with the stock adding $4.2 billion in value in just three months, I see a lot of this already priced into the stock, and AU is not cheap, with it trading at ~6.0x forward cash flow and above 1.25x P/NAV. Hence, while the investment thesis has improved, the valuation has become stretched, suggesting the best course of action is to book some profits above US$22.40.

For further details see:

AngloGold Ashanti: Turnaround Thesis Intact