BUD - Anheuser-Busch Could Be In The Late Stages Of The Business Life Cycle

2023-10-25 15:46:16 ET

Summary

- Anheuser-Busch InBev's profitability metrics have declined over the long term, indicating weak pricing power and increased competition.

- Declining financial performance suggests a lack of innovation and overreliance on the company's rich legacy portfolio of brands.

- I believe the stock is slightly overvalued and there is no upside potential from current levels.

Investment thesis

My fundamental analysis suggests that Anheuser-Busch InBev SA/NV ( BUD ) was unable to efficiently manage years of high profitability to extend its growth stage of the lifecycle. The company demonstrates a secular decline in profitability metrics across the board, and it is a huge red flag to me. Revenue growth over the decade was somewhat in line with general inflation, but trend analysis suggests that costs outpaced revenue growth. This means the company's pricing power is weak as competition intensifies in my view. Lastly, my valuation analysis suggests that the stock is slightly overvalued. All in all, I assign the stock a "Hold' rating.

Company information

Anheuser-Busch InBev SA/NV is the world's largest brewer by volume and one of the leading global consumer product companies by revenue. BUD produces, markets, and distributes a portfolio of over 500 beer and other malt beverage brands.

The company's fiscal year ends on December 31. BUD disaggregates its segments by geographic areas. According to the latest annual SEC filing , more than 70% of sales were generated outside North America in FY 2022.

Financials

The company's financial performance cannot be called strong over the past decade. Despite a decent 3.3% revenue CAGR, profitability metrics deteriorated substantially across the board. The operating margin shrank notably from 32.4% ten years ago to 24.9% in FY 2022. As a result, the free cash flow [FCF] margin ex-stock-based compensation [ex-SBC] shrank significantly as well. It is also worth mentioning that the FCF margin has been very volatile over the past decade.

{kind=link}

Despite having a strong average 14.5% FCF margin over the past decade, the company's balance sheet does not look like a fortress. The outstanding debt was above $80 billion as of the last reporting date and it is by far higher than the outstanding cash balance. The leverage ratio is lower than 1, but still, it looks too high to me. Short-term liquidity metrics also do not look so strong. The business is highly capital-intensive and the management was not very efficient in capital allocation. The company had a relatively high FCF margin for most of the years over the past decade. At the same time, BUD neither built a strong balance sheet nor kept shareholders very happy in my opinion because stock buybacks were rare and dividend growth also did not look impressive.

Seeking Alpha

The latest quarterly earnings were released on August 3, when the company missed consensus estimates. Despite the fact that revenue grew by 2.2% on a YoY basis, the adjusted EPS narrowed from $0.75 to $0.72. The profitability narrowed due to the cost of revenue and SG&A both growing faster than the top line.

Seeking Alpha

The upcoming quarter's earnings are scheduled for release on October 31. Consensus estimates forecast quarterly revenue at $15.82 billion, indicating a 4.8% YoY growth. The adjusted EPS is expected to be flat YoY despite a projected solid revenue growth.

Seeking Alpha

To conclude, I do not like the company's financial performance trend. There is little evidence that the company makes strong strategic moves to either drive revenue growth or improve BUD's profitability. The lack of profitability metrics expansion also indicates weak pricing power despite having a solid and massive portfolio of well-known beer brands as the company struggles to pass on inflationary effects to customers. The inability to adjust pricing in line with cost inflation indicates that the competition intensifies because the company does not only compete with other brewers but with all soft drink manufacturers. The company's below-average balance sheet also suggests there are not many resources to fuel significant revenue growth in the foreseeable future. Overall, I believe that the business is in the late stages of the business lifecycle.

Valuation

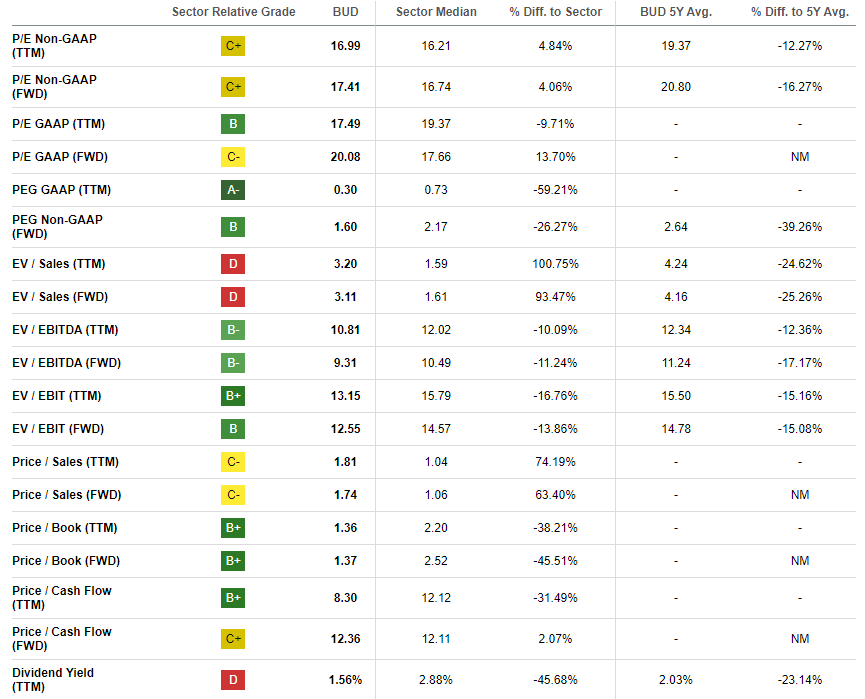

The stock price declined by about 10% year-to-date, significantly underperforming the broader U.S. market. Seeking Alpha Quant assigns the stock a low "D+" valuation grade, which means the stock is likely to be overvalued based on ratios analysis. On the other hand, current multiples are notably lower than historical averages across the board. For a company of a scale like BUD, I think it is more appropriate to look at how current multiples compare to historical averages.

{kind=link}

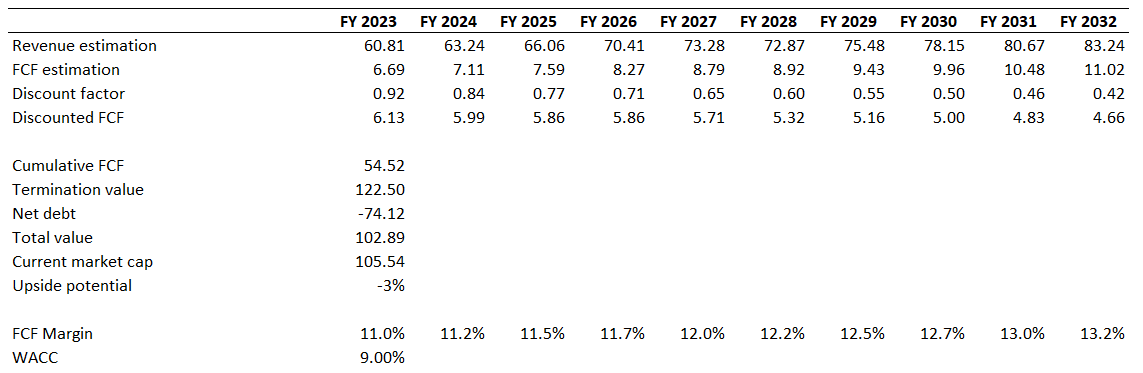

Despite being a dividend stock, BUD does not demonstrate solid consistency in payouts. Therefore, the discounted cash flow [DCF] simulation would be a better option to proceed with. I use a 9% WACC for discounting. The TTM FCF ex-SBC margin is 11%, and I incorporate it for my base year with a further 25 basis points yearly expansion. Revenue consensus estimates project a 4% CAGR for the next decade, which I consider fair to use in my DCF.

{kind=link}

According to my DCF simulation, the stock is approximately fairly valued after the outstanding net debt is incorporated into calculations. That said, the current stock price is close to the fair price, and there is no upside potential from the current levels that I see.

Risks to consider

The major secular risk to the company's operations is the increasing portion of people becoming more health-conscious . It is also well-known that drinking alcohol is not good for health , generally speaking. That said, it is highly likely that beer consumption trends are poised to deteriorate over the long term. The lack of revenue growth and narrowing profitability suggests that the company is relying too much on its legacy beer brands and lacks innovation in non-alcoholic drinks.

Another set of significant risks is related to the company's worldwide presence. Selling its goods across the globe means that BUD faces substantial international trade risks, which include potential changes in regulations and tariffs. Failure to comply with the complex web of international rules and laws might lead to substantial financial and reputational damage. Generating more than 70% of sales outside North America also means the company faces substantial foreign exchange risks.

Bottom line

To conclude, BUD is a "Hold". The company's financial performance is in secular decline due to the management's overreliance on its legacy brands and lack of initiatives to drive growth or improve business efficiency. The company did not demonstrate solid efficiency to absorb years of high FCF margins. It did not manage to build a strong balance sheet to make the company well-positioned to extend its growth stage of the lifecycle. Moreover, the valuation does not look attractive as well.

For further details see:

Anheuser-Busch Could Be In The Late Stages Of The Business Life Cycle