BUD - Anheuser-Busch InBev: It's Over

2023-08-21 07:51:13 ET

Summary

- The backlash over Bud Light continues.

- Sales of Bud Light have declined, but the pace of decline has stalled, indicating that the worst may be over.

- Despite the boycott, Anheuser-Busch InBev's earnings were better than expected, with revenue growth driven by pricing.

- There are ways to profit on a stable stock.

Folks, we closely followed the Anheuser-Busch InBev SA/NV ( BUD ) controversy this spring. We had previously opined that the damage looks permanent . To that end, there are consumers who will never buy another product from the company. But the consumer backlash over Bud Light and the advertising and promotional decisions they made seems largely to be coming to an end. Earnings were just recently reported , and we saw that indeed, there was of course a sales impact on the overall company stemming from the well-covered controversy. But here is the thing. When there is some sort of controversy around a company, it often blows over after a few weeks. In this case, the controversy lasted a few months and had an impact on the quarter.

However, the company is so global, with so many brands, the company was able to offset the pain through pricing power as well as volumes of its many other brands. Go woke, go broke, it is a popular mantra, but it is difficult to maintain long term. Yes, we know there are many of you who will never willingly put your hard-earned dollars in the pocket of this or other companies for which you do not agree with their social views. The same can be said of those who disagree on the other side of the aisle. One example is Chick-fil-A, there are very vocal groups against the company, and it grows like wildfire. On the flip side, it too has been attacked for apparently making 'woke' decisions . Yet, the stores are packed, and new stores are opening all over the country.

Now look, the company and the stock did take a hit from this. No doubt. But it looks to be over. Even we were wrong, as we predicted that the company would down guide its EBITDA outlook, but it was reiterated in the quarter. That was very surprising. And, it seems, some are slowly caving and coming back to the brand. Surely, some of the boycotters are returning, even if they are not actively buying it, they may still drink it.

Now, the thing is, we had an initial short bias on the stock in the high $60s when this all broke out. The easy short money was made. When covering it publicly, we opined it could drop to $48, despite issuing hold ratings on the stock. The stock has been pretty stable in a defined range the last two months now. But what about the actual sales data?

We were updating you on sales every few weeks, and Bud Light sales had been down 20-25% year-over-year week to week. We predicted sales of Bud Light would eventually see the down 30% year-over-year mark. The data was clear, and the situation actually did indeed worsen from the first time we told you sales were plummeting . Bud Light actually lost its top spot as the number one selling beer in America. But what does the most recent weekly sales data look like?

Well, while we were seeing sales down 20, 25, even 30% week to week compared to a year ago, the pace of sales declines has stalled. In fact, according to Newsweek and data from Bump Williams, for the 4-week period ending July 15th, the data showed a decline in sales of 13.6% . Sales are definitely still falling, but the degree of the decline has stalled. In response, along with only a dent in the overall sales and earnings for the parent company, the stock has appeared to have fully priced in the backlash. The chart tells the story:

We previously identified support at about $56, and BUD stock fell through this level, but as you can see, since June the stock has mostly traded around that level. But we did seriously question how annual guidance can be met with the brand damage that has taken place. This is not to say it had no impact, but it appears that the damage, while certainly impacting this brand, has not crushed the company. Instead, it has been dented, at best.

The data is clear. Despite Bud Light sales volume down over 30% in some weeks in June, that seems to be the peak. It is over, in our opinion, and now the company is digging out of the hole. The damage is done, noted by shares stabilizing. How were the earnings? Largely better than we expected, despite the carnage in sales of Bud Light. We thought earnings could be decimated . It simply did not materialize as such.

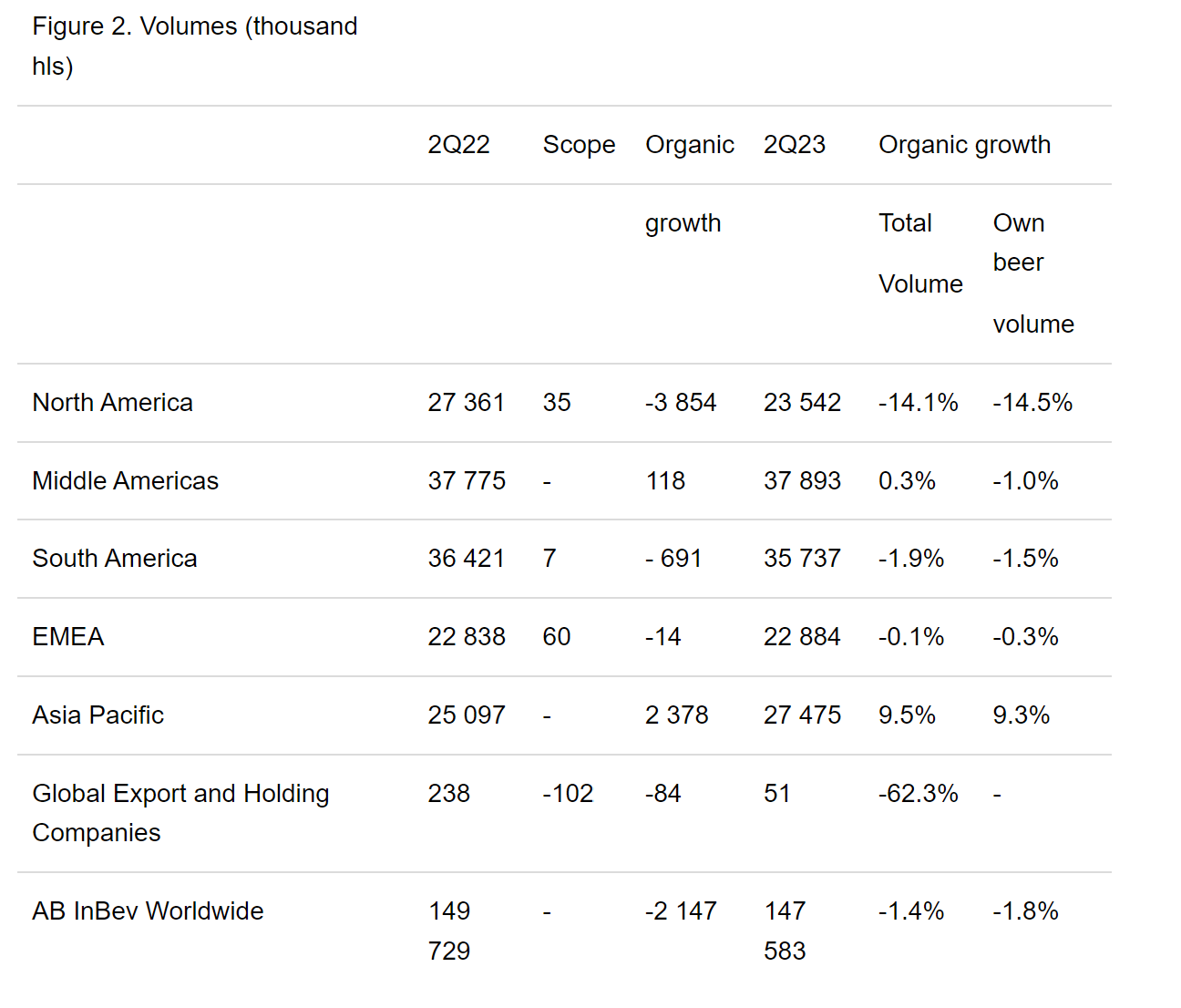

Revenue increased by 7.2% in the quarter with revenue per hectoliter growth of 9.0% and by 10.0% in the first half of 2023, with revenue per hectoliter growth of 10.6%. A lot of this was pricing driven, though, as volumes did decline. That is the impact of the boycott. A dent in the armor, not a devastating blow. In Q2, total volumes declined by 1.4%, with own beer volumes down by 1.8% and non-beer volumes up by 0.5%. In the first half of 2023, total volumes declined by 0.3% with own beer volumes down by 0.8% and non-beer volumes up by 2.1%. The volume pressure was felt in North America, that was the pressure of the boycott:

{kind=link}

So, volumes were indeed down, but the revenue still grew from last year. When combined with expenses, the company earned $0.72 per share, down a penny from a year ago, which saw $0.73 in EPS. This was also $0.03 better than consensus, and $0.04 better than our expectations. Through the first half of 2023, earnings are up, hitting $1.37, an increase from $1.33 per share in the comparable 2022 period. And in the release , the EBITDA outlook was maintained, perhaps the biggest surprise of the quarter:

We expect our EBITDA to grow in line with our medium-term outlook of between 4-8% and our revenue to grow ahead of EBITDA from a healthy combination of volume and price.

We strongly expected the range to be narrowed on the back of the U.S. pressures, but international strength offset the pressures largely.

So where do we go from here? We still see volumes falling in North America in Q3. But we see no material impact to international sales. We think that the boycott will continue to weigh this year, and while not inconsequential, the impact seems to be contained. The market is speaking with shares having stabilized. The bleeding out appears to be contained. The worst is now over.

Your voice matters

Are you trying to trade this stock? Does it look stable enough to sell premium with little risk of major moves in either direction? Are you still boycotting? Are you actively buying Bud Light or BUD products? Do you think sales declines will pick up steam? Let the community know below.

For further details see:

Anheuser-Busch InBev: It's Over