BUD - Anheuser-Busch InBev: Limited Upside Potential

Summary

- Anheuser-Busch InBev is the market leader in the beer market, with a market share of above 30% and higher profitability than its peers.

- BUD's balance sheet is inflated with long-term debt and goodwill, as it must acquire new companies to maintain its market share in a rapidly shifting consumer market.

- BUD is quite expensive, with a P/E ratio of around 24. DCF analysis underlines this as its intrinsic value is just 10% above its market price.

- I assign BUD a hold rating, as it is still very profitable and has a deep moat, but has limited upside potential in the coming years.

Anheuser-Busch InBev SA/NV ( BUD ) ( OTCPK:BUDFF ) is the largest beer company in the world, with a global market share of around 30% of the beer market in 2020. Its main competitors do not even come close, as Heineken (HEINY) is around 12% and both Carlsberg (CABGY) and Snow are around 6% market share. As the figure below shows, BUD has been remarkably stable YTD and outperformed the S&P 500 slightly, only being down 6.6% while the S&P 500 is down 7.5%. I do however believe that it will significantly underperform the S&P 500 in the coming years, as it is quite expensive (P/E around 24 (LTM)) and the intrinsic value is just above its current price. On top of that I believe that there will be more and more of a headwind in the North American and European markets, as consumers want a healthier lifestyle and demand more specialized products, such as local craft beers and low calorie drinks.

{kind=link}

Stable results, but leveraged balance sheet

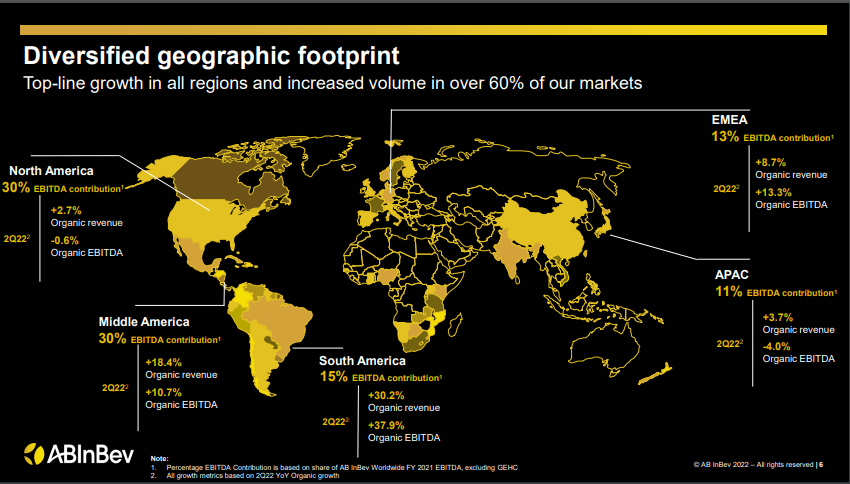

BUD's results have been very stable over recent years, with current EBITDA around $18 billion dollars. This gives us earnings of $2.53 per share, resulting in a P/E ratio of just below 24. It is also very diversified, as the figure below shows. 30% of its sales come from Northern America, 30% from Middle America and around 15% from both South America and Europe. 11% of its revenue comes from Asia.

However, I'm not impressed with BUD's balance sheet, as it has both a lot of goodwill ($115 billion) and long-term debt ($80 billion) on its books. This is due to an aggressive strategy of taking over other brands to maintain its market dominance. Such high debt levels can quickly deteriorate in an macroeconomic environment with rising interest rates, such as we are currently facing. Moreover, the large amount of goodwill might be written off when demand falters and can quickly lead to a rapidly deteriorating P/B ratio, which is currently still favorable around 1.7.

BUD: global presence (Anheuser-Busch InBev)

{kind=link}

More health-aware consumers demand different drinks

Another significant risk, in my opinion, stems from the healthier lifestyle that consumers pursue. Global trends are changing quickly and younger generations strive towards both a healthier lifestyle and more specialized and local beers (the craft beer movement). As shown on Statista , beer consumption in the U.S. is stable, while the population is growing, thus beer consumption per capita is declining. Moreover, craft brewers are gaining market share . In 2021, U.S. beer volume sales were up 1%, while craft brewer volume sales were up 8%. This creates a need for more takeovers from BUD, in order to retain its market dominance. I think this is a real threat to BUD's market dominance, as BUD already has an inflated balance sheet and competition is growing.

Peer comparison shows higher profitability, but also price

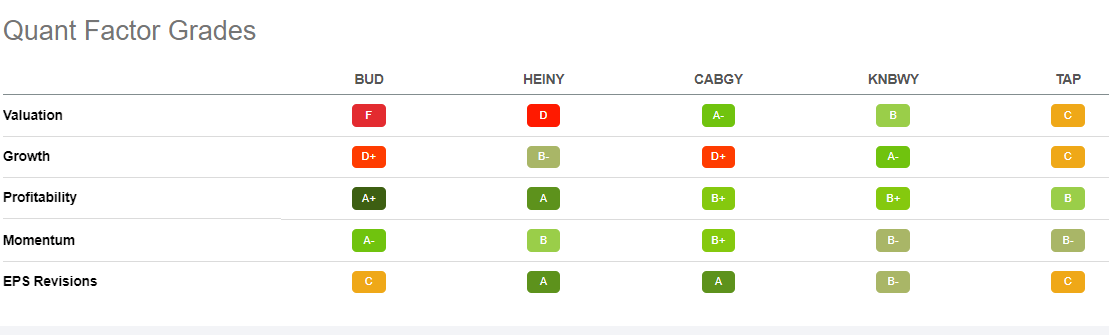

A more positive note is BUD's high profitability, more so than its closest competitors Heineken and Carlsberg. BUD's EBITDA margin for 2021 was just under 33%, significantly higher than Heineken (21%) and Carlsberg (22%). This is also shown by the figure below, which highlights Seeking Alpha's Quant ratings on BUD and its closest competitors. It also shows that BUD is lagging behind on growth, compared to its closest competitors, and that it is more expensive, as the P/E ratio has already shown. This higher P/E ratio, compared to its competitors, is however justified by its higher profitability. However, a P/E ratio of around 24 is relatively high for a company with limited growth opportunities, such as BUD, as it is already the market leader with a huge market share.

Peer comparison (Seeking Alpha)

{kind=link}

DCF analysis shows no undervaluation

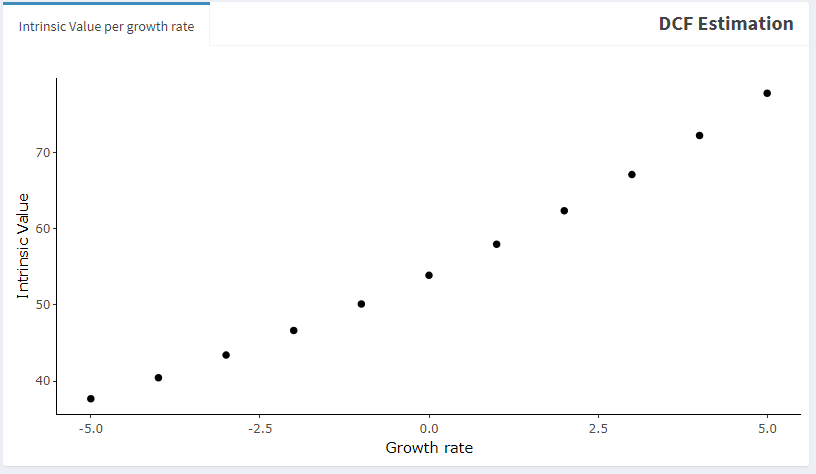

Going a little more in-depth and quantifying my investment thesis, I've performed a DCF analysis. For my calculation I will use BUD's 2021 free cash flow per share of $4.56. Guidance for the next year is however lower at $3.77 per share. Furthermore, I will use a terminal growth rate of 3%, a discount rate of 10%, a growth rate of 1% and a time horizon of 10 years. I also show a DCF analysis for varying growth rates of -5% to 5% for completion's sake. A growth rate of 1% yields us an intrinsic value of around $67. This is around 10% higher than the current market price.

However, taking into account a margin of safety as well, in my opinion this is not satisfactory to expect an above market performance. Growth rates of 5% or above should be achieved to maintain a margin of safety of around 30%, as the figure below shows. Especially with guidance for the next year already begin down from 2021, this seems highly unlikely. This underlines the limited upside potential for BUD.

DCF analysis: 1% growth rate (Author) DCF analysis: growth rates of -5% to 5% (Author)

{kind=link}

{kind=link}

Conclusion

BUD has had a remarkably stable year, outperforming the S&P 500. However, I do not expect it to continue outperforming the S&P 500, as its price is quite high with a P/E ratio of around 24 and its growth potential is limited by its already large market share. Moreover, its stock price has limited upside potential as my DCF analysis has shown. Next to this, the balance sheet is quite leveraged and unstable, as BUD has a high level of goodwill and long-term debt on its balance sheet.

Its P/B ratio of 1.7 should thus be treated with caution and will probably rise in a macroeconomic setting of higher interest rates. Moreover, global trends are shifting quickly in the beverage market, with younger generations demanding healthier drinks. In addition to this, the craft beer movement persists and is still growing, creating additional headwinds for BUD.

BUD has taken over other brands in order to retain market dominance, but this does come at a cost, resulting in the high debt and goodwill levels as discussed before. BUD is still the market leader and has strong fundamentals, compared to its peers. However, the stock is quite expensive, the company faces strong headwinds and there is no clear undervaluation. Therefore, I assign BUD a hold rating.

For further details see:

Anheuser-Busch InBev: Limited Upside Potential