TPX.B:CC - Anheuser-Busch InBev: The Boycott Is No Longer Important

2023-11-19 10:00:00 ET

Summary

- Anheuser-Busch InBev's sales in the US remain impacted, with losses accelerating in FQ3'23, implying that the backlash may not be over yet.

- However, the management's aggressive efforts in other regions have also paid off, with the Middle Americas now the company's top and bottom line driver.

- While Bud Light has clearly been dethroned in the US, we believe that BUD's well-diversified global footprint and intensified domestic marketing efforts may be able to balance the temporal headwinds.

- However, investors must also note that the lost target audience may be gone for good, with TAP already recording massive wins in consumer market share and retailer shelf space.

- As a result, BUD investors may want to temper their near-to-intermediate-term expectations since Bud Light's reversal in the US market may take longer than expected.

We covered Anheuser-Busch InBev SA/NV (BUD) in August 2023, discussing its mixed prospects then, as the backlash impacted the performance of the North American region. Since the region was previously the company's top and bottom line driver, there had been valid concerns about its ability to regain the lost market share.

In this article, we will be discussing BUD's (still) impacted sales volume in the North American region, with losses intensifying as the management has had to provide financial assistance to its wholesalers.

Then again, we maintain our Buy rating, with the management's successful marketing efforts in other regions contributing to its excellent FY2023 guidance and the consensus optimistic forward estimates through FY2025.

We shall discuss further.

The Boycott Is No Longer Important

For now, BUD has reported an excellent FQ3'23 earnings call , with revenues of $15.57B ( +2.9% QoQ / +3.1% YoY) and adj EPS of $0.86 (+19.4% QoQ/ +6.1% YoY).

This further builds upon the great results reported in FQ2'23, with revenues of $15.12B (+6.4% QoQ/ +2.2% YoY) and adj EPS of $0.69 (+11.2% QoQ/ -13.8% YoY), implying that the management's strategic pricing actions have more than balanced the moderate decline in its sold volumes.

BUD already reports a notable improvement on a QoQ basis in AB InBev own beer volumes sold to 132.32M hls (+2.7% QoQ/ -3.9% YoY) and non-beer volumes to 18.58M hls (+5.3% QoQ/ +1.3% YoY) globally.

However, it is apparent that the backlash has yet to pass over , attributed to the accelerating decline in its volume sold in North America to 23M hls (-2.2% QoQ/ -17.7% YoY), compared to those reported in FQ2'23 at 23.54M hls (-1.2% QoQ/ -13.9% YoY) and in FQ1'23 at 23.85M hls ( +1.7% QoQ / -1% YoY).

As a result, it is unsurprising that BUD continues to report impacted revenues of $3.86B (-2.2% QoQ/ -13% YoY) and adj EBITDA of $1.23B (+4.2% QoQ/ -26.7% YoY) in the North American region, directly attributed to the reduced Bud Light sales to wholesalers by -17.6% and retailers by -16.6%.

Then again, we maintain our confidence in the company's global prospects, attributed to its well-diversified footprint with the management's focus in the Middle Americas and South Americas already bearing fruit.

Both regions have reported growing sales volumes with higher ASPs, resulting in BUD's expanded top and bottom line contributions over the past few quarters.

Particularly, Middle Americas has now taken over the North American region as the company's top and bottom line driver, with accelerating revenues of $4.33B (+6.1% QoQ/ +21.2% YoY) and adj EBITDA of $2.05B (+7.3% QoQ/ +25.7% YoY) by the latest quarter.

The South America region has also done relatively well, with expanding revenues of $3.1B (+13.2% QoQ/ +7.5% YoY) and adj EBITDA of $1.01B (+37.4% QoQ/ +27.4% YoY), implying that the impact of the boycott in the North America region is no longer as important as it was in the past.

Therefore, while Bud Light has clearly been dethroned in the US, we believe that BUD's well-diversified global footprint may be able to balance the temporal headwinds, especially since the management has doubled down on its traditional marketing efforts.

The list includes un-controversial partnerships with the NFL/ Super Bowl , college footballs , several country/ rock music festivals , and Ultimate Fighting Championship , while also putting several top marketing executives on leave.

However, investors must also note that the lost target audience may be gone for good, with BUD's direct competitor, Molson Coors Beverage Company ( TAP ), already recording massive wins in consumer market share, retailer shelf space, and top/ bottom line performance in the latest quarter:

We've already gained thousands of tap handles across the U.S. since the beginning of the second quarter... Over 50 retailers have made space changes in late summer or fall due to the massive shift in consumer purchase behavior we have seen since April 1 (i.e: the backlash against Bud Light).

Among the chains that moved their resets up to the fall, Molson Coors was the biggest beneficiary with Miller Lite and Coors Light gaining +6% to +7% more shelf space (on a QoQ basis)... it's tens of thousands of cubit-feet of space.

The conversations for spring resets are well underway. And while we can't exactly predict the future, it's safe to say that we expect to gain more shelf space for our big brands in those resets as well.

This development is unsurprising indeed, with TAP experiencing a drastically different US growth volume of +4.5% YoY, particularly attributed to Coors Banquet at +30% YoY, Coors Light at double digits, and Miller Lite at high single digits, as more beer consumers increasingly transition away from Bud Light.

As a result, BUD investors may want to temper their near-to-intermediate-term expectations, since the Bud Light's reversal in the US market may take longer than expected.

Most Of The Pain May Already Be Over

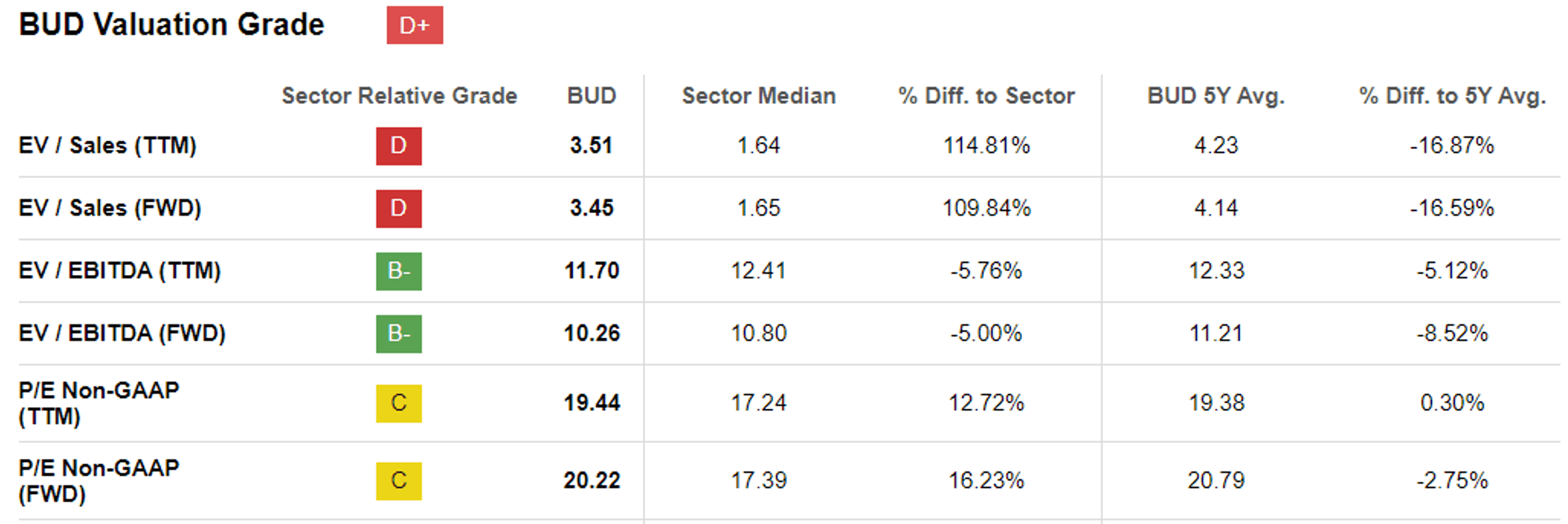

BUD Valuations

{kind=link}

For now, BUD's FWD P/E valuation of 20.22x and EV/ EBITDA of 10.26x remain somewhat lower when compared to its 3Y pre-pandemic mean of 21.40x and 13.26x, respectively.

However, we believe that these levels are already much improved compared to post-backlash impacted valuations of 16.16x and 8.73x, respectively, implying that most of the pain may already be over.

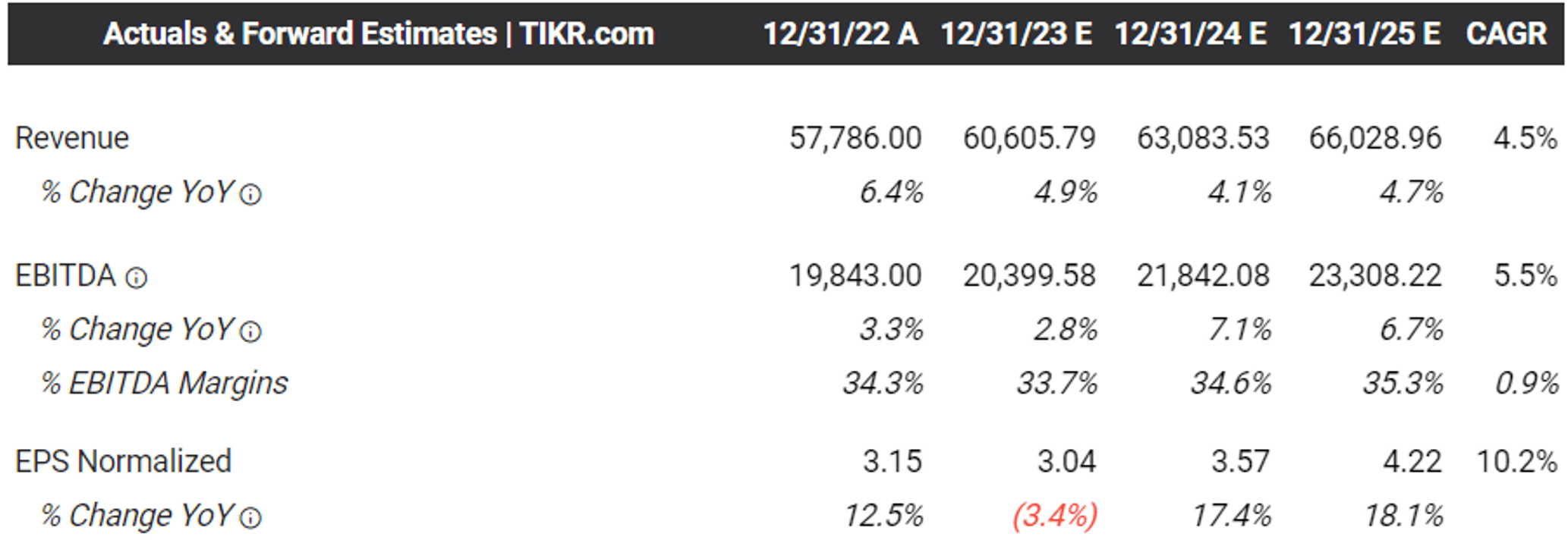

The Consensus Forward Estimates

{kind=link}

In addition, based on the management's FY2023 adj EBITDA growth guidance of between +4% and +8% YoY, we may see BUD generate a robust adj EBITDA of $21.03B at the midpoint.

Based on its 2.01B of shares outstanding in FQ3'23, we may see the company generate a robust adj EBITDA per share of $10.46B (+5.9% YoY) as well.

However, with an elevated annualized interest expense of $3.15B (-30.9% QoQ/ -4.4% YoY) and other annualized pension/ accretion expenses of $920M, it may be more prudent to refer to the consensus FY2023 adj EPS estimates of $3.04 (-3.4% YoY), since it portrays a more accurate picture of the company's profitability.

Combined with its FWD P/E valuation of 20.22x, we believe that the BUD stock is still trading near its fair value of $61.46.

Based on the consensus FY2025 adj EPS estimates of $4.22, there appears to be a decent upside potential of +39.4% to our long-term price target of $85.32 as well.

So, Is BUD Stock A Buy , Sell, or Hold?

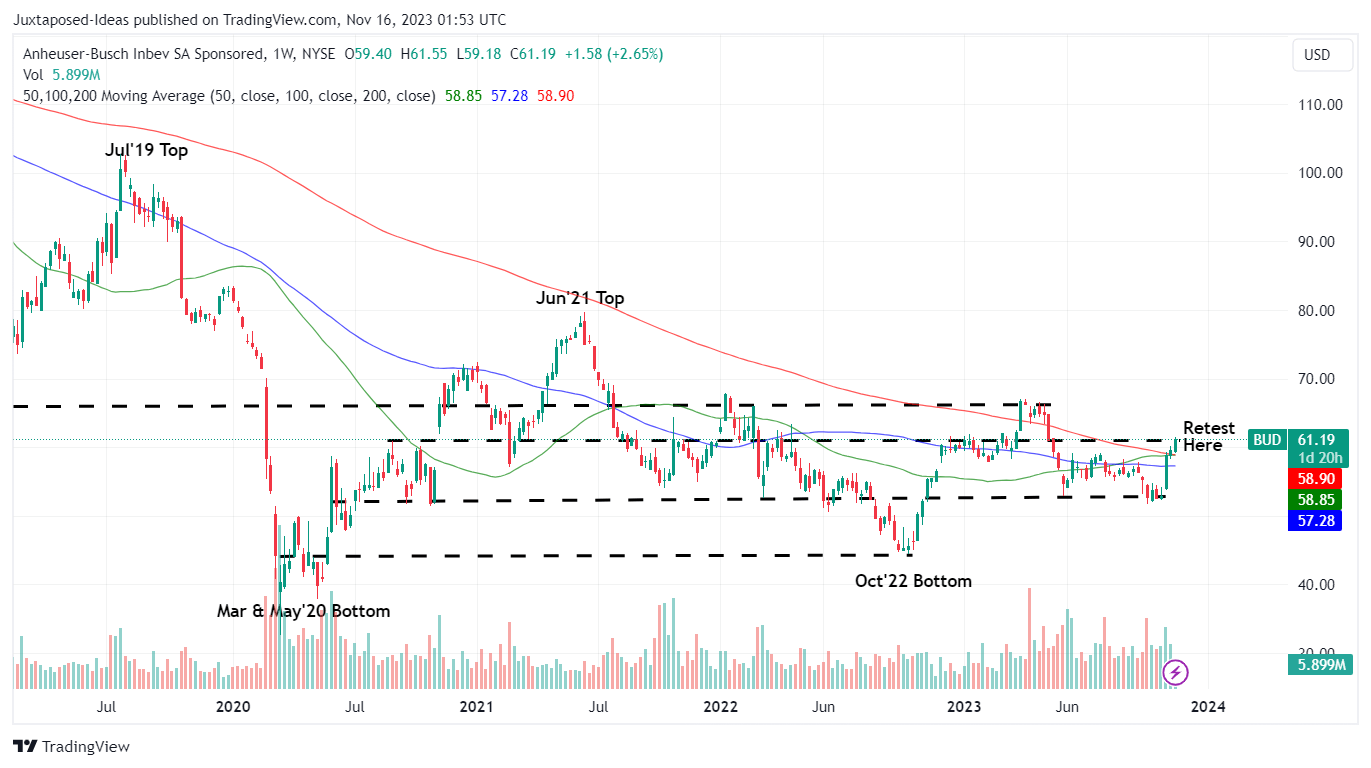

BUD 5Y Stock Price

{kind=link}

For now, thanks to the encouraging FY2023 guidance, it is unsurprising that BUD has rallied tremendously by +15.8%, with the stock now retesting its resistance levels of $61s.

However, we are uncertain if the stock is able to sustain this recovery, attributed to the dramatic correction after the boycott since April 2023 and its sideways movement since then.

As a result, we are of the opinion that the BUD stock may return some of its recent gains in the near term, as some traders opt to take their profits at current levels.

Therefore, while we may rate the stock as a Buy, investors may want to wait for a moderate pullback to its previous support levels of $52 and $57 for an improved margin of safety.

For further details see:

Anheuser-Busch InBev: The Boycott Is No Longer Important