BUD - Anheuser-Busch InBev: The Clear Market Leader Still For Grabs At A Huge Discount

2023-09-29 12:42:51 ET

Summary

- AB InBev is the world's largest brewery with over 500 brands and holds multiple tangible competitive advantages.

- The company's economic moat is supported by cost efficiency, economies of scale, and a diverse product portfolio.

- Despite recent controversies and macroeconomic conditions, AB InBev is undervalued by 40% and offers long-term investment potential.

- Strong Buy rating reiterated.

Investment Thesis

Anheuser-Busch InBev ( BUD ) is the world's largest brewery selling over 500 different brands of beers. The firm's massive portfolio of brands is complemented by tangible cost advantages that help the firm outperform their market peers from an operational perspective.

Recent controversies and unrelenting macroeconomic conditions have done little to elevate share prices, with a potential 40% undervaluation still being present in the stock.

Considering the undervaluation, continuing fiscal strength, and their massive economic moat I still rate AB InBev as a Strong Buy and believe the firm will earn value-oriented investors outsized returns in the long term.

Company Background

{kind=link}

Anheuser-Busch InBev (AB InBev) is a multinational brewery based in Leuven, Belgium. The firm operates across over 150 countries and sells over 500 different brands of iconic beers such as Stella Artois, Budweiser, and Corona Extra.

AB InBev as an entity today has been formed through years of transformative acquisitions and mergers with the most notable being the acquisition by Belgian InBev of the American brewer Anheuser-Busch.

Their most recent high-profile acquisition in 2016 of South African brewer SAB Miller has allowed the firm to control around 30% of the total market share in the beer industry. This makes AB InBev significantly larger than even their nearest competitor Heineken N.V. ( HEINY ) which enjoys around 11% of the market share.

The firm's strategy of acquiring smaller brewers from across the globe and incorporating them into their operational processes has allowed AB InBev to grow rapidly throughout the years. However, the firm has also generated significant amounts of debt, especially since the acquisition of Anheuser-Busch.

Since 2016 AB InBev has battled to deleverage their business by reducing their debt burden rapidly. The firm has also focused acutely on expanding margins through streamlining their business operations and simplifying their operational structure.

AB InBev CEO Michel Doukeris took over the helm of the company back in 2021 and has since overseen the company's transformation into a more operationally efficient entity. I believe Doukeris' extensive knowledge of the beer industry and past experiences within both InBev and Anheuser-Busch means he is the right man to lead AB InBev forward as a company.

Economic Moat - In-Depth Analysis

AB InBev has a truly massive economic moat that is both wide and robust in nature. The firm benefits from a raft of intangible assets and an operational cost advantage compared to its competitors which together generate significant moatiness for the firm.

To ensure cost efficiency and operational excellence, AB InBev takes advantage of the scalable nature of the production processes present within the beer brewing industry to minimize inefficiencies within their supply network.

The firm's huge scale allows the firm to benefit from massive economies of scale. By negotiating for high-volume and low-cost per-unit supply deals with their suppliers, AB InBev is able to reduce the COGS associated within their operations holistically starting from the procurement of raw materials and extending all the way to the distribution and packaging of their products.

The TTM 310 days payables on which AB InBev currently operates illustrate how hard the firm pushes its suppliers in the name of reducing overall COGS and increasing operating margins within their business.

In 2022 AB InBev brewed 595 million hectoliters ((HL)) of beer which, when divided by their FY22 PP&E costs of $27.18B, provides a production cost per HL value of $45.68/HL. This illustrates the massively efficient operational model AB InBev has developed especially when compared to the $60.69/HL production costs upon which Heineken N.V. operates their business.

This fundamental cost advantage allows AB InBev to operate significantly more efficiently that their competitors which ultimately should allow the firm to generate outsized returns from their business.

While the firm's tangible and clear cost advantage already generates huge moatiness for the firm, the brewer's intangible assets are just as important to driving sales within the highly competitive markets in which they operate.

{kind=link}

With over 500 brands of beer and other alcoholic beverages on sale, AB InBev undoubtedly has the largest portfolio of drinks products in the world. Out of the top 10 most valuable beer brands in 2023, AB InBev owns six of them.

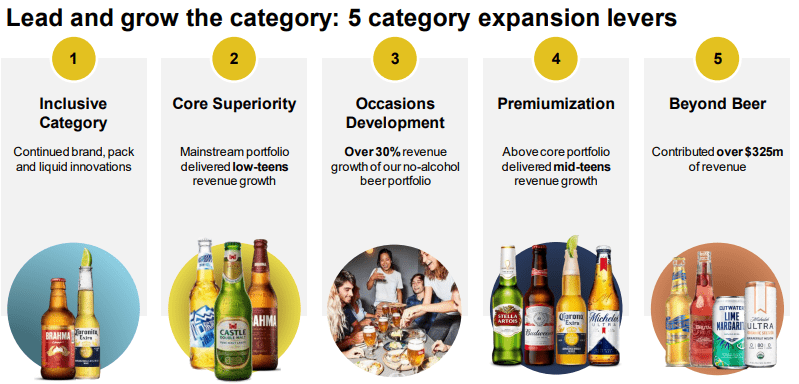

The firm is currently executing a strategic plan to increase sales of their premium brands and beers to complement their fundamental "core" line-up of drinks. This should allow the firm to extract greater margins from these higher-priced products as the brewing processes are not particularly more costly thus further expanding their $/HL advantage.

{kind=link}

AB InBev's iconic Budweiser brand of beer saw a boycott by the far-right political movement in the U.S. due to a supposedly controversial advertisement souring relations with this group of citizens. The small drop in sales led to the Mexican Modelo beer overtaking Budweiser as the most-sold beer in the U.S.

modelousa.com

While this initially seems regrettable, it must be remembered that AB InBev owns Constellation Brands which is the company responsible for brewing Modelo beer. While the firm doesn't own the distribution rights in the United States for Modelo due to an antitrust settlement in 2013, the boycott in 2023 essentially did nothing to AB InBev's overall portfolio strength.

I believe this situation perfectly illustrates how robust and extensive AB InBev's product portfolio really is. The massive diversity both in terms of geography and style of beers creates huge flexibility in AB InBev's sales strategy and allows the firm to accurately satisfy the constantly changing tastes and preferences of its customers.

{kind=link}

Furthermore, the firm's rapid expansion into the "beyond beer" category which includes more trendy alcoholic beverages such as hard seltzers and premixed cocktails allows AB InBev to develop an even stronger grasp on the alcoholic beverage market.

I believe this diversification is also key in ensuring AB InBev stays relevant within the industry and avoids a situation whereby their key brands and revenue streams face stagnating public appeal.

Considering the huge raft of brands and products sold by AB InBev along with their tangible cost advantage in production processes, I believe that the firm has a truly huge economic moat.

While many firms become bloated or inefficient as a result of mergers and acquisitions, AB InBev has maintained a highly efficient supply network throughout their expansionary business strategies.

This has allowed the firm to become a truly market-leading firm within the beer industry with multiple competitive tailwinds supporting the company's growth and profitability over the coming years. I believe the firm's economic moat will help generate a tangible competitive advantage for at least the next 25 years.

Financial Situation

AB InBev has consistently generated solid profits and gradually expanded margins over the last five years. The firm's 5Y average ROA, ROE, and ROIC are 2.92%, 8.22%, and 5.97%, respectively. While these returns are not particularly outstanding (especially the relatively slim 5.97% ROIC) I believe the upward trend illustrated in these metrics is still positive.

For the same period, AB InBev operated their business on gross, operating and net margins of 58.62%, 27.47%, and 9.39%, respectively. The very healthy gross margin in particular suggests that the fundamental business model at AB InBev is incredibly lucrative and remains unaffected by short-term headwinds or the uncompromising macroeconomic conditions currently impacting the global economy.

While the net margin is not huge and has undoubtedly decreased from pre-Anheuser Busch merger highs of around 19% in 2025, I believe the upward trend in these metrics once again illustrates that AB InBev is moving in the right direction and is effectively managing the streamlining of their operations structures.

{kind=link}

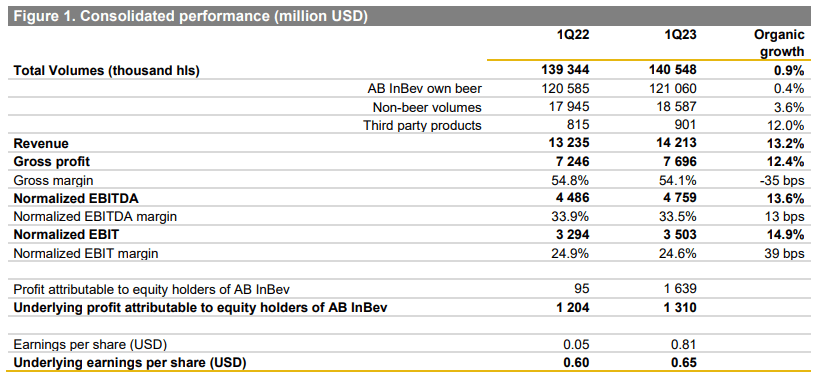

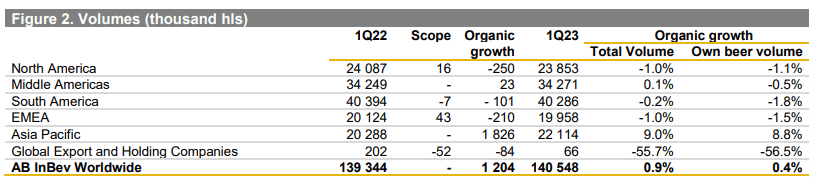

AB InBev's FY23 has been progressing well for the company from profitability, growth, and operational perspectives. Q1 saw the firm generate 13.2% organic YoY revenue growth which was driven primarily by premiumization of their sales along with organic total volume growth.

This first quarter strength saw normalized EBITDA increase 13.6% YoY with gross profits growing 13.2% to over $7.7B.

{kind=link}

Q1 was also characterized by very strong volume growth in the Asia Pacific geographic demographic where own beer volumes grew 8.8% organically. This was the only geographic region in AB InBev's portfolio that saw volume growth.

Considering the essentially flatline volume growth achieved by AB InBev worldwide, it is clear that the firm's "premiumization" business strategy is working well even in the almost recessionary macro environment currently impacting the firm. By focusing on more premium brands, AB InBev should be able to continue to extract solid profits and revenues even as consumers purchase less products overall.

Unfortunately, the firm's COGS for Q1 increased 14% YoY to just over $6.52B which resulted in the firm's gross profit margin contracting by 35bps to 33.5% from 33.9% in Q1 FY22. This increase in costs was mainly attributed to an overall increase in the price of raw materials, labor, and transportation due to the increasing levels of inflation witnessed across the globe.

{kind=link}

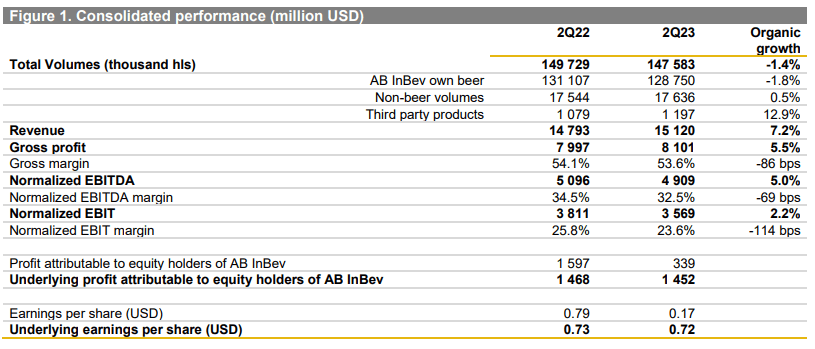

Q2 saw AB InBev achieve similar levels of revenue and gross profit growth as they did in the first quarter of 2023. The firm's revenue saw 7.2% organic growth driven primarily by the increased sale of premium beers and despite the overall -1.4% YoY drop in total volumes.

Normalized EBITDA fell 5% while gross margins declined another 86bps to just 53.6%.

{kind=link}

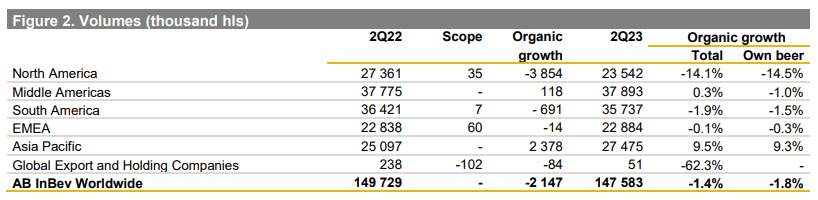

The firm's Asia Pacific geographic segment once again illustrated significant robustness with regards to total beer volume growth with the segment seeing an overall 9.3% increase. This is in contrast to continuing contractions in total volumes sold witnessed in other geographic segments.

The significant 14.5% drop in North American total volumes may initially seem concerning, but when compared to the overall 14.1% contraction witnessed across the beer industry as a whole, AB InBev has largely performed according to expectations.

The firm's market share within the North American Market has remained constant which illustrates that no fundamental damage has been done to the business in this region.

The -0.4% underperformance relative to the rest of the North American market can be attributed to the very slight decline in sales (particularly to retailers) of Budweiser beers as a result of the controversy surrounding their ad campaign for the drink.

AB InBev polled over 170,000 Budweiser customers across the U.S. and found that 80% had a neutral to positive opinion of the drink. This illustrates that essentially no tangible damage has been done to the brand despite the noise created by media and far-right politicians.

{kind=link}

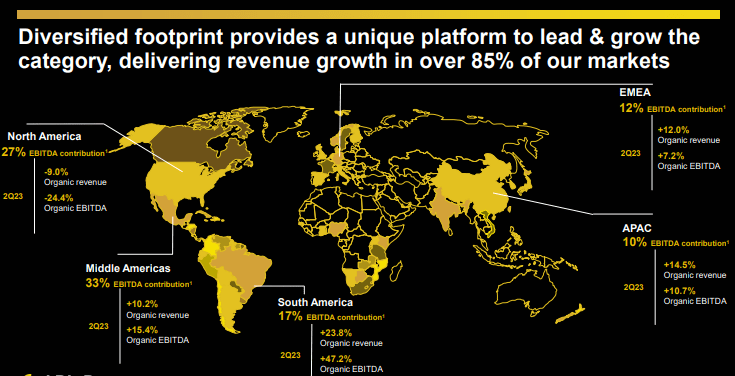

Furthermore, the huge diversity AB InBev holds from geographic perspective with regard to their revenue streams means that some North American weakness has less of an impact on overall profitability and growth than for some of their competitors such as Boston Brewing Company.

While Q1 and Q2 seem to have presented investors with a mixed bag of results, I believe the underlying business at AB InBev has only strengthened. The firm reported a 9.0% increase in revenue per HL in Q2 FY23 with HY23 results showing a 10.6% increase.

{kind=link}

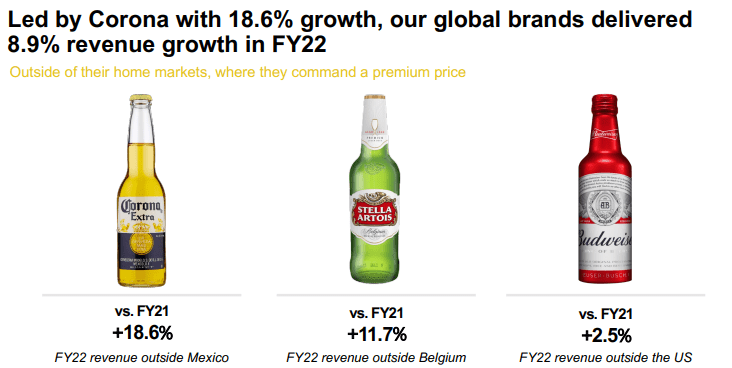

Such significant improvements in revenue per HL are impressive given the decreasing volumes and increasingly income-stressed nature of consumers. Furthermore, AB InBev managed an 18.4% increase in combined revenues of their global brands (Budweiser, Stella Artois, and Corona) outside of their respective home markets.

This illustrates the firm's premiumization strategy at work and suggests that once again, the shift towards selling less product but at a higher margin is working well for the firm.

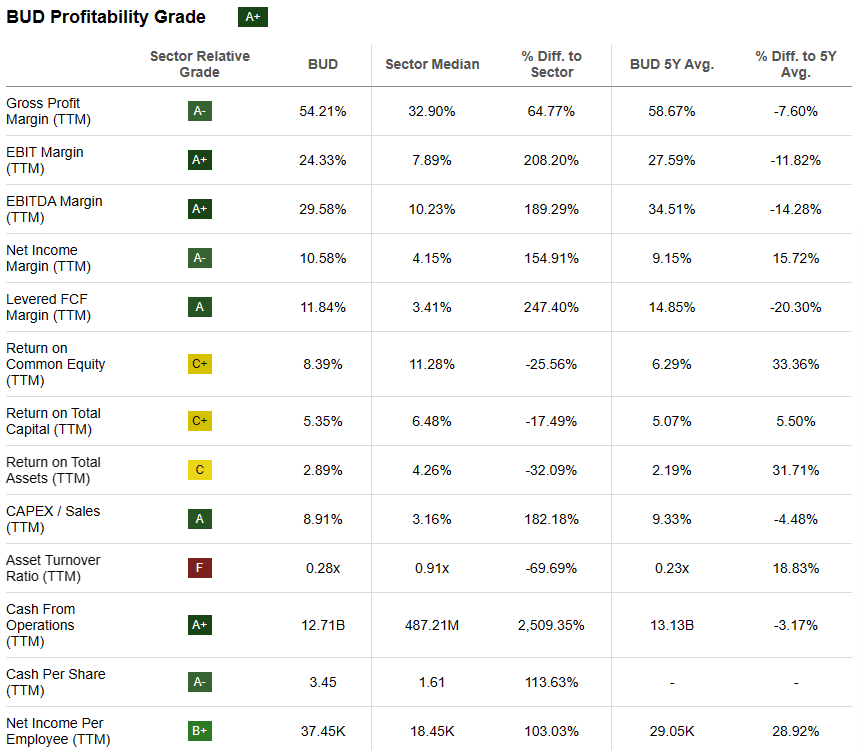

Seeking Alpha | BUD | Profitability

{kind=link}

Seeking Alpha's Quant calculates an " A+ " profitability rating for AB InBev. I believe this to be an accurate overview of the firm's overall profitability and income statement strength. Such fiscal resilience despite an increasingly bearish macro environment is refreshing and incredibly positive to see from an investor standpoint.

From a balance sheet perspective, AB InBev appears to be incredibly well managed despite their continuous debt burden.

While the SAB Miller acquisition did increase the debt burden of AB InBev significantly, the incredibly budget-oriented management style and culture present at the firm has meant that these debentures are being consistently paid down.

I also believe that the absolute desire for operational excellence communicated by Doukeris at the Q2 webcast illustrates that AB InBev is not going to rest until they become the incredibly profitable and lean business, they were pre-2016.

The firm currently has $21.48B in total current assets while total current liabilities amount to $33.77B. This imbalance in short-term liquidity leaves the firm with a current ratio of 0.64 and a quick ratio of 0.41.

I do not view this imbalance negatively as the firm's huge cash flows and consistent profitability place little doubt that AB InBev will be able to meet all current obligations without the need to raise additional debt.

Total assets for the firm amount to $216.4B with total liabilities just $127.6B. This leaves the firm with an excellent debt/equity ratio of 0.59.

The real issue that investors currently perceive with AB InBev as a company stems from the significant lump of long-term debt that the company possesses.

As of Q2 FY23, AB InBev still holds $73.8B in long-term debentures. This is significant and leaves the firm with a leverage ratio of 3.70x. However, this leverage ratio is already down from 4.86x in June 2020 with continuous deleveraging planned for the foreseeable future.

BUD FY23 Q2 Report

Furthermore, the firm's debt profile is incredibly well staggered with the majority of their notes only maturing post 2036. The $3B due to mature through to 2025 should place little strain on near-term cash flows and I believe that the sums due in 2026 may still be refinanced in the coming years.

I do not foresee AB InBev facing any real liquidity concerns and believe that the firm's strong cash flows and profitability should allow the company to easily meet their debt obligations.

AB InBev has received an upgraded A3 credit rating from Moody's for their senior unsecured notes and an affirmed Prime-2 commercial paper rating. The outlook remains stable. A3 is classified as credit obligations which are of upper-medium grade and are subject to low credit risk.

From a financial perspective, I believe AB InBev is a fundamentally profitable, well-run, and fiscally sound firm that still has the capability to achieve outsized returns on their invested capital. While the debt burden carried by the firm continues to worry some investors, I believe their massive moat and huge profitability overrule any fears of lacking liquidity present at the firm.

The continued efforts to deleverage the firm while expanding margins illustrate that AB InBev has sound management that understands the importance of returning the company to the significant levels of profitability for which they were known pre-2016.

Valuation

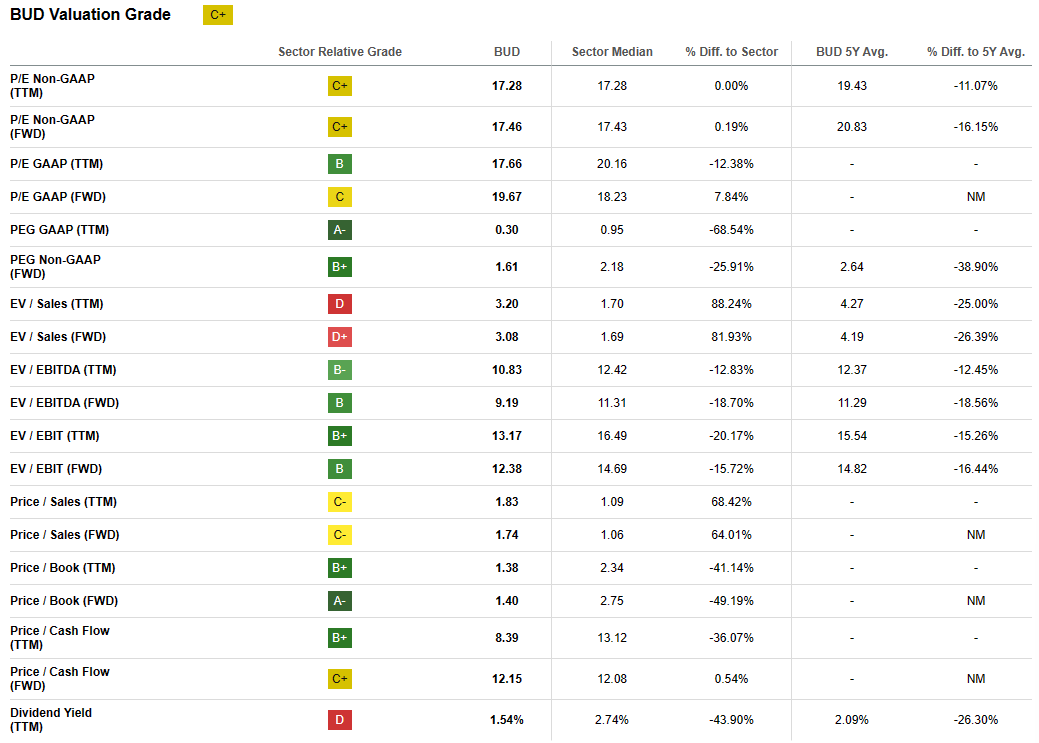

Seeking Alpha | BUD | Valuation

{kind=link}

Seeking Alpha's Quant assigns AB InBev with a " C+ " Valuation grade. I believe this is an excessively pessimistic representation of the intrinsic and future value present within AB InBev's shares.

The firm currently trades at a P/E GAAP FWD ratio of 19.67x along with a P/CF FWD of just 12.15x. Their FWD EV/EBITDA of just 9.19 is quite surprising. AB InBev's EV/Sales TTM and FWD are 3.20 and 3.08 respectively which is a little elevated but not overly concerning.

Considering only these basic valuation metrics I believe AB InBev is difficult to price accurately. While the P/E and EV/EBITDA metrics suggest an undervaluation, in my opinion, the elevated EV/Sales suggests a potential overvaluation.

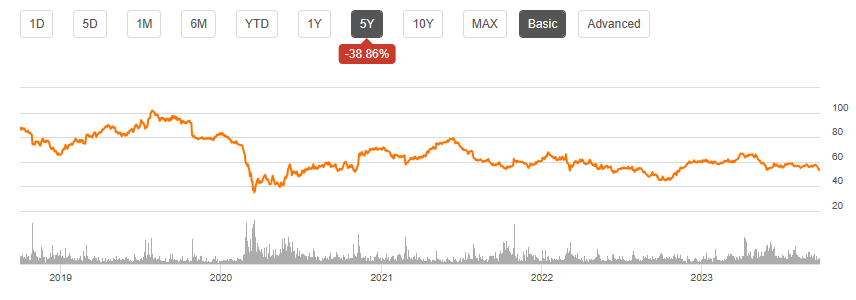

Seeking Alpha | BUD | Summary Chart

{kind=link}

From an absolute perspective, AB InBev shares are trading at a significant discount relative to previous valuations, especially pre-2016. The huge debt burden acquired during the acquisition of SAB Miller resulted in investors becoming bearish on shares with a sell-off lasting for essentially four years.

While the relative valuation provided by simple metrics and ratios along with the absolute comparison begin to create a baseline of understanding regarding the value present in AB InBev shares, an intrinsic value calculation is absolutely necessary.

The Value Corner

By utilizing The Value Corner's Intrinsic Valuation Calculation, we can better understand what value exists in the company from a more objective perspective.

Using AB InBev's current share price of $53.56, an estimated 2024 EPS of $3.69 , a realistic "r" value of 0.10 (10%), and the current Moody's Seasoned AAA Corporate Bond Yield ratio of 4.95 x, I derive a base-case IV of $93.50. This represents a massive 43% undervaluation in the firm.

Even when using a more pessimistic CAGR value for r of 0.07 (7%) to reflect a scenario where AB InBev sees slowed growth in gross revenues due to stagnation of sales in a recessionary environment, shares are still valued at around $73.80 representing a 28% undervaluation.

Considering the valuation metrics, absolute valuation, and intrinsic value calculation, I believe AB InBev is still clearly trading in what can only be considered deep-value territory.

In the short term (3-12 months), I find it difficult to say exactly what may happen to valuations. While the growing revenues and profits are positive, the contracting total volumes and gross margins suggest that weakening consumer demand is beginning to impact even AB InBev.

I believe the firm's short-term performance is ultimately tied to the general sentiment surrounding the U.S. market as a whole. While I do believe that AB InBev has a robust economic moat and is set to expand margins significantly, the timescale of these improvements may not fall within the next 12 months.

In the long term (2-10 years), I see AB InBev strengthening their position at the helm of the beer industry and believe their competitive advantages will become even stronger. While fierce competition from the likes of Heineken and more artisanal craft brewers may challenge the firm, their robust portfolio of products combined with a difficult-to-replicate cost advantage should help the firm prevail in the long run.

Risks Facing AB InBev

AB InBev is relatively well protected from risks but sees some tangible threats arising from increasing inflation and increasing competition potentially placing downward pressure on profitability and sales respectively.

The continuously rising pricing levels currently being witnessed in economies across the globe present AB InBev with the challenge of managing raw materials and transportation costs within their business operations.

Any increases in barley and oil pricing levels could leave AB InBev in a difficult situation whereby their COGS increase substantially while an equal raising of product prices is unviable. This would place direct pressure on gross and operating margins which would almost undoubtedly contract.

While the firm's premiumization strategy and shift towards selling more high-end beers should help protect the firm from such a scenario, the risk still exists that their core product categories (which drive volume output for the firm) could see contracting margins.

Increasing levels of competition could also see total volumes continue to fall for AB InBev as more artisanal craft beers and alternative product categories eat away at the firm's market share. While the firm has a great portfolio of market-leading brands, diversification away from beer alone will be critical for AB InBev to ensure their portfolio is relevant in years to come.

AB InBev has historically been effective at meeting trendy consumer demands and adjusting volume outputs of different beers to meet changing tastes accurately, but failed execution in this category is always present.

I do not see any material risk arising towards AB InBev from the Budweiser controversy earlier in the year. Ultimately, this short-term politically motivated "boycott" has little to do with the firm's beer or products and more realistically reflects the increasingly turbulent political environment present within the U.S.

{kind=link}

From an ESG perspective, AB InBev faces little tangible risks. While beer production and barley farming can be quite water-intensive, the firm is dedicated to reducing the environmental impact their operations have on the globe.

In 2022 alone AB InBev garnered over 10 different ESG-related distinctions ranging from the Gold Medal for International Corporate Achievement in Sustainable Development from the WEC to the AA rating by MSCI ESG Research for performance on ESG-related issues.

Considering these factors, I would happily recommend AB InBev to a more ESG-conscious investor as the material lack of ESG risks facing the brand would make the firm a great pick. Of course, opinions may vary and I implore you to conduct your own ESG suitability research should this be of concern to you.

Summary

AB InBev is still an outstanding leader in the beer industry. Their unrivalled product portfolio of iconic brands, tangible cost advantage in production, and dedication to fiscal control sets a benchmark not only within the beer industry but for any mega-cap corporation as a whole.

While the firm's performance since the 2016 acquisition of SAB Miller has been less stellar than their previous track record, the consistent gains made by management toward achieving their previous levels of profitability seem to be going unnoticed by investors.

This combined with a difficult FY23 both from a PR and macroeconomic standpoint has left shares trading at a potential 40% undervaluation. From a pure value perspective, AB InBev remains a great deep-value pick in my opinion.

While the timeframe in which a return to pre-2016 levels of profitability and investor returns is difficult to forecast, I believe the firm's unassailable position within their industry means that long-term profitability is almost assured.

Therefore, I maintain my Strong Buy rating for AB InBev and remain invested in the company personally. While I am not growing my position at the present time (due to the already sizeable exposure I have to the company), any further drop in valuations may prompt me to reassess this possibility.

For further details see:

Anheuser-Busch InBev: The Clear Market Leader Still For Grabs At A Huge Discount