PEP - Anheuser-Busch: Risky And A Failed Marketing Campaign

2023-04-13 18:40:41 ET

Summary

- Anheuser-Busch is a large beer company but has not had a strong track record.

- The company is highly indebted in a rising rates environment, and shares are rather pricey compared to the broad market and to BUD's peers.

- A recent ad campaign has likely not generated any positive ROI and added risks to a BUD investment.

Article Thesis

Anheuser-Busch InBev SA/NV ( BUD ) got a lot of attention in recent days due to a marketing campaign that involved trans activist Dylan Mulvaney. Here's a report by Seeking Alpha's news team on that matter. Right now, it looks like this ad campaign was a failed one, as it does not look like it generates additional sales and profits for the company. That being said, it is also far from guaranteed that there will be a long-lasting negative impact from boycotts. Still, the ad campaign and the reaction by some customers add risks to an investment in BUD stock, and since BUD doesn't look like a good investment even without this new development, I doubt that BUD is a good buy today.

Why BUD Does Not Look Especially Attractive Even Without This Ad Campaign

Anheuser-Busch InBev is one of the largest beer companies in the world. But it does not look like a very appealing investment, I believe, due to several reasons.

First, BUD has not been able to deliver compelling growth in the past:

Over the last five years, revenue is up 5%, or 1% per year. Considering that cumulative inflation has totaled 21% over the same time frame, according to this inflation calculator by the US Bureau of Labor Statistics, Anheuser-Busch InBev has delivered a substantial revenue decline in real terms. Even before the drastic inflation rates we have seen over the last year that has been the case, as 1% annual revenue growth is not enough to balance out inflation even while it is running at the 2% target rate -- and in the current environment, inflation is way higher.

Of course, not all companies are able to push inflation onto customers, but producers of discretionary consumer goods should ideally be able to do so. The fact that BUD has not been able to generate any positive revenue growth in real terms for years, and that its sales are declining when we account for inflation, suggests that the company doesn't have a lot of pricing power. Contrast this with PepsiCo's ( PEP ) 34% revenue increase over the last five years, which easily beat inflation and which made for a substantial revenue gain in real terms, to see what other consumer staples producers are capable of.

Even worse, BUD is not only negatively impacted by a combination of weak pricing power and high inflation rates when it comes to its revenue performance, but also when it comes to its margin performance:

BUD's gross profit has declined by 8% over the last five years in nominal terms, or by around 30% in real terms. During the most recent quarter, BUD has seen its gross margin compress by a hefty 300 basis points on a year-over-year basis. Peer Heineken ( HEINY ) has seen its gross profit rise by 7% over the last five years, which is significantly better than BUD's performance, but which still represents a decline in real terms, suggesting that the beer industry, overall, is not doing too well in this environment.

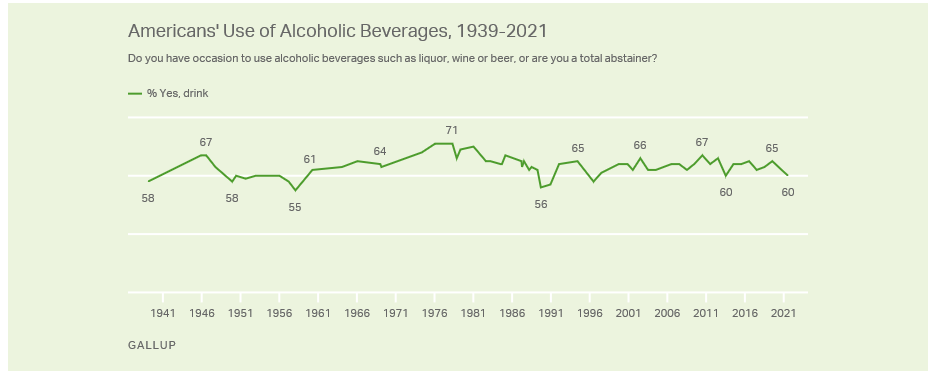

Consumer staples company PepsiCo, for reference, has seen its gross profit expand by more than 30% in the same time frame. This can likely be explained by PepsiCo's better pricing power due to stronger brands and less competition, but also by the fact that the soda market and the snacks markets are more favorable than the beer market overall. The following graph from a Gallup poll suggests that alcohol consumption, which includes beer, might be trending downward in the US:

{kind=link}

While the overall market is not enjoying growth and might actually be shrinking, BUD (and, to some extent, other large brewers) is facing increasing competition from smaller breweries that sell craft beers. This is a headwind that other consumer staples companies such as Coca-Cola ( KO ) or PepsiCo are not experiencing, as there is no "buy from your local soda producer" mindset or trend.

This makes me believe that the beer space, overall, is not overly attractive. At the right valuation, beer companies could still be solid investments, of course, but other consumer goods sectors seem more favorable.

Anheuser-Busch InBev is also facing headwinds from its massive debt load. According to its annual report for 2022, the company ended the year with a net debt position of $69.7 billion. That's equal to more than 3.5x its EBITDA, which seems like a rather high leverage ratio for a consumer goods company. Management agrees with that belief, as the company plans to lower its net leverage ratio to around 2x EBITDA over time. In other words, the company currently has close to twice the net debt that management sees as optimal. This means that the company will be focused on reducing debt for some time, which limits BUD's shareholder return potential, and it also means that its bigger-than-optimal debt position makes for some risks. The company would be less flexible in a crisis, and it is exposed to rising interest rates. While having $70 billion in net debt is not an issue in a low rates environment, the interest rate increases we have seen in the US and around the world over the last year will impact BUD significantly. Of course, interest rate increases do not immediately impact BUD, as fixed-rate debt has the same interest rate until it matures. But in case maturing debt is not paid back fully, it has to be refinanced at higher rates. In a smart move, BUD has pushed out maturities on a large portion of its debt, with some of that maturing in the 2040s and later. Still, there are considerable (multi-billion dollar) maturities in 2024 and each of 2026-2032, thus higher interest rates could impact BUD negatively in the coming years. Other companies with lower leverage, such as Heineken and PepsiCo, which both have a ~2x leverage ratio, are better protected and less exposed to high and rising interest rates.

If BUD was trading at 10x earnings, one could argue that it would still be a strong investment despite the inflation headwinds, the low business growth, and the high debt load. But BUD is not trading at 10x net earnings -- instead, the stock is valued at 19.5x forward net profits at the time of writing. Shares are up more than 40% from the lows seen last fall, which has made the company quite expensive. The broad market's forward earnings multiple is 18.2, according to current estimates, meaning BUD is now trading at a premium relative to the average company -- despite the issues and headwinds shown above. Relative to its peers, BUD also looks somewhat pricey -- Heineken trades at a similar valuation despite having a much stronger balance sheet and a better growth and cost control track record, while Ambev S.A. ( ABEV ) and Molson Coors ( TAP ) trade at lower valuations, as their earnings multiples for the current year are 17.8 and 13.3. Carlsberg A/S ( CABGY ) also looks cheaper based on a trailing earnings multiple of 17.

In short, BUD is trading at a premium compared to the broad market and its peers, despite a rather weak balance sheet, weak growth, weak cost controls, and above-average risks due to its high debt load. I'm not an investor in any of its beer peers today, but a company such as TAP, at a massive discount compared to BUD, seems more attractive. The fact that BUD only offers a dividend yield of 0.8% is not helping, either.

A (Failed?) Ad Campaign And Its Impact

As noted above, BUD has been in the news and has gotten a lot of attention on social media due to an ad campaign involving trans activist Dylan Mulvaney. I believe that this ad campaign has failed, as it does not seem to generate a lot of positive attention, and since it seems highly doubtful that the ROI on this ad campaign is positive.

Reading through hundreds of comments on recent BUD articles and news items here on Seeking Alpha, which is an investment site and not a politics site and which should thus have a diverse base of users (geographically and from a politics perspective), there are generally two groups of commenters: Those that believe that this ad will not have a meaningful impact in the long run, and those that believe that this ad will have a meaningful negative impact in the long run. So it looks like the best-case scenario is that this ad has not had any impact whatsoever, while the worst-case scenario is that it has had a lasting negative impact. Of course, that's a pretty bad outcome for an ad campaign. Ad campaigns cost money, and they should bring in substantial additional revenue to justify the investment. If the best-case scenario is that the investment has not hurt sales (while not generating any additional sales on a net basis), then the ROI of that ad campaign will likely be negative.

The uproar and boycott are mostly centered on the US. Anheuser-Busch InBev generates a little less than 30% of its revenue in North America, or $17 billion in 2022. A little more than 30% of its EBITDA is generated in this market, meaning North America is a more profitable market compared to other markets BUD is active in. There is no way of knowing how large the impact of the boycott will be both in the short-term and long-term, but the Seeking Alpha news item linked at the beginning of this article notes a "notable" volume decline. If, as an example, 5% of BUD's sales in North America were to disappear this year, with no notable impact from 2024, that would mean $850 million of lost revenue, or a ~$500 million hit to BUD's gross profits. On a net basis, the impact would be a little smaller, but could still be in the several hundred million dollars range. Deciding on an ad campaign that costs the company hundreds of millions of dollars would be a pretty bad business move. Of course, it's possible that there will not be any impact, as consumers might forget about this news item quickly. But it's also possible that the impact is larger than 5%, at least in the near term. No matter what, it looks like this ad campaign has not worked well for BUD, as it seems highly unlikely that additional profits and customer activity will be created, and the ad campaign has added risks to an investment in BUD. Since BUD wouldn't seem like a compelling investment even without this ad campaign, it is not a buy with the ad campaign controversy, either.

For further details see:

Anheuser-Busch: Risky And A Failed Marketing Campaign