LULU - ANTA Sports: Great Domestic Sportswear Company With Uncertain International Prospect

2024-01-16 20:01:28 ET

Summary

- ANTA has outperformed its peers only in the Chinese market by emulating successful strategies and avoiding their pitfalls.

- Despite short-term inventory challenges due to the pandemic and DTC transformation, recovery signs are evident from ANTA’s latest interim report.

- ANTA is the most likely Chinese sportswear company to capture a significant market share internationally but it does not have precedence of similar successful strategies to emulate from.

- The stock is undervalued, but investing in a Chinese company like ANTA presents significant regulatory uncertainties.

Investment Thesis

ANTA Sports ( ANPDY ) and Li Ning ( LNNGY ) are both major beneficiaries of the Chinese consumers’ nationalistic sentiments, but Li Ning’s over-reliance on this has impeded its business strategy. ANTA, with its relatively diversified brand portfolio and larger market capitalization, has outperformed Li Ning in almost all financial measures suggesting it is more likely to capture a significant share of the international market than Li Ning.

ANTA’s success over Li Ning is attributed to its direct-to-consumer ("DTC"/"D2C") selling model, a key differentiator against Li Ning. Learning from Nike’s ( NKE ) successful DTC strategy, ANTA launched its own DTC transition in 2020, showing good financial results. By learning from its peers and avoiding their pitfalls, ANTA is poised to maintain its growth momentum.

ANTA has a short-term challenge in inventory management. This was attributed to the pandemic and the recently embarked DTC transformation. Signs of recovery in inventory turnover are already observed in its latest interim report . Investors should observe if the “average turnover days” continue to decrease as the company strives to increase its store numbers indicating effective inventory-to-sales conversion in the new stores.

ANTA is smaller than most leading international sportswear brands but not far behind. However, based on Li Ning’s unsuccessful international expansion and lack of a successful strategy to emulate, the odds of ANTA’s achieving international success are not in its favour.

The stock price is deeply undervalued presenting a good value play opportunity only for investors who do not mind the regulatory uncertainties associated with investing in Chinese companies.

Company Overview

ANTA Sports is a well-established and growing company with a strong brand portfolio and a large market share in China. As the second-largest sportswear company by revenue in the Chinese market, second only to Nike, the company is well-positioned to capitalize on the growing demand for sportswear in China and around the world.

The company operates a variety of brands in its portfolio, including ANTA, FILA, DESCENTE, KOLON SPORT and AMER:

{kind=link}

Its product offerings span a wide range of sportswear and footwear for various sports, including basketball, running, training, outdoor, fitness, and lifestyle.

Comparison with Li Ning

In my opinion, ANTA's closest comparable company is Li Ning.

While both Li Ning and ANTA have been massive beneficiaries of the Chinese consumers' nationalistic (or "Guochao ") sentiments over the last decade, this tailwind is not a panacea to permanent business longevity.

As this article described comprehensively, Li Ning's business strategy was severely impeded by its over-reliance on the rise of Guochao sentiments:

the brand’s position in the market is ambiguous and it relies too much on its nationalistic designs, being vulnerable to potential scandals

Can ANTA learn from Li Ning's pitfalls and rise above its current competitors in both the local and international athleisure market? We look at a few perspectives to find out.

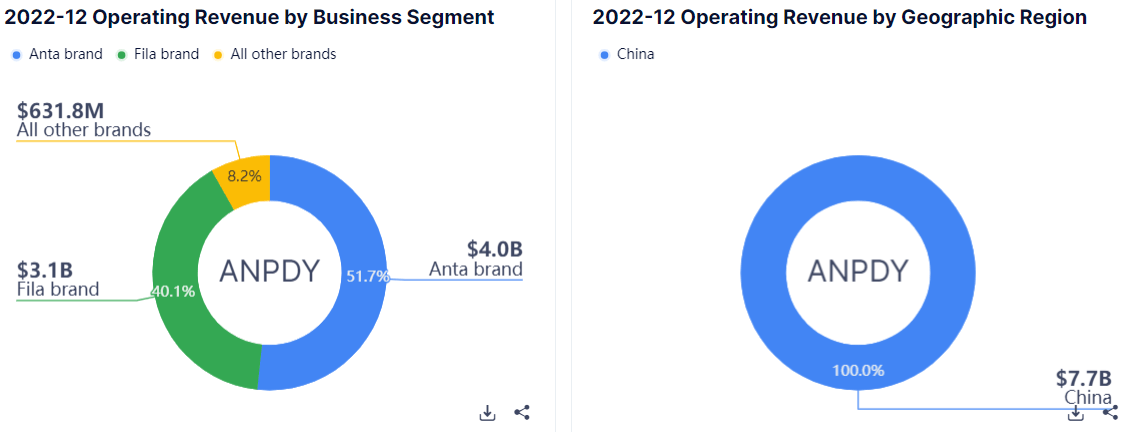

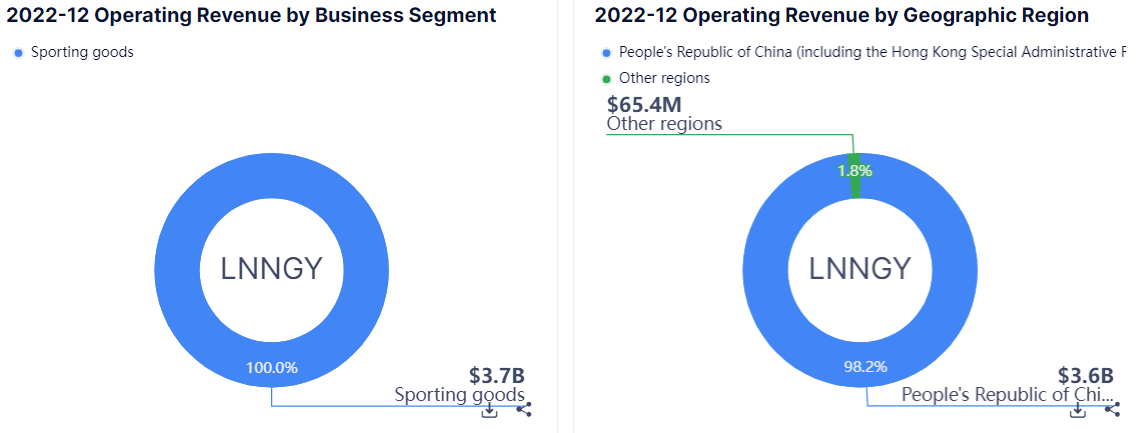

We look at the revenue profiles of both ANTA and Li Ning to gain more insights:

ANTA (Guru Focus) Li Ning (Guru Focus)

{kind=link}

{kind=link}

Looking at the charts:

- In terms of geographical spread in revenue, both Li Ning and ANTA's revenue are highly concentrated in the Chinese market which is one of the most volatile in the world. This is a significant concentration risk that both companies are trying to mitigate by attempting to penetrate the international market, with limited success. According to this article , the top 10 sports brands in the international market are still dominated by non-Chinese brands.

- In terms of brand diversification, Li Ning appears to be highly dependent on its homegrown brand, while ANTA has at least one other major brand of Fila to rely on.

In terms of size, we can observe that ANTA is much larger than Li Ning in market capitalization and enterprise value:

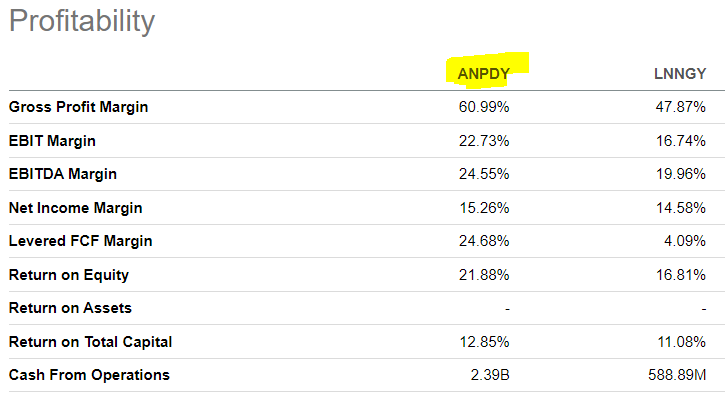

Financial Comparison (Seeking Alpha)

If we look at some profitability ratios and figures from Seeking Alpha , ANTA is faring much better than Li Ning by almost all measures:

{kind=link}

In my opinion, ANTA has achieved the financial strength to overtake Li Ning as the leading Chinese sportswear/athleisure brand. It has so far avoided the pitfall of over-leveraging on the Chinese consumers' nationalistic sentiments. Looking at the significant diversification of its revenue away from the Chinese market with the acquisition of the rights of the international Fila brand in the Chinese market, it appears likely that ANTA is proactively avoiding this pitfall and preparing for an eventual penetration in the international market.

According to this article by Janus Henderson, as of 2022, ANTA already leads Li Ning in the Chinese sportswear market share at 20.4%. ANTA's market share is second only to Nike at 22.6% while Li Ning's market share is only 10.4% at 4th place. Based on this data, ANTA has already overtaken Li Ning as the top Chinese sportswear brand. If ANTA keeps up with its current momentum of growth, it is en route to overtaking Nike as well in the local Chinese market.

Armed with its financial prowess and existing presence in the international market (via the Fila brand), ANTA appears to be the most likely Chinese sportswear/athleisure brand that can surpass its predecessors to capture a significant share of the international market.

ANTA's Strengths In Direct-To-Consumer

ANTA's success over Li Ning is by no means an accident. This article from KrASIA describes the direct-to-consumer selling model as the key competitive advantage of the company:

At the beginning of its establishment, the company was mainly a shoe OEM factory, coming from CEO Ding’s family roots as a shoe factory. Overtime, however, the company has built up its capabilities across the entire supply chain, from R&D to design, manufacturing, distributorship and even its own dedicated logistics team. This was a key differentiator against domestic competitor Li-Ning .

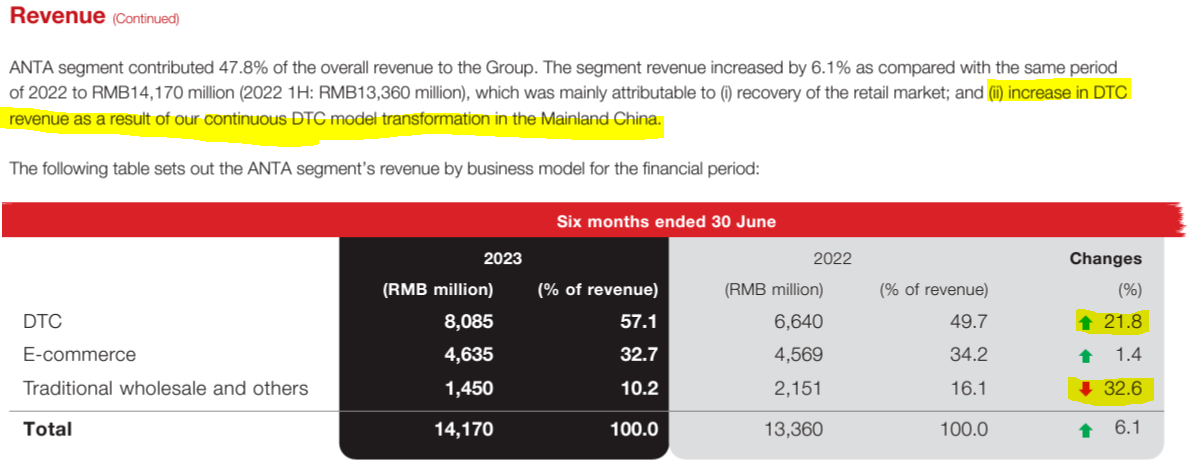

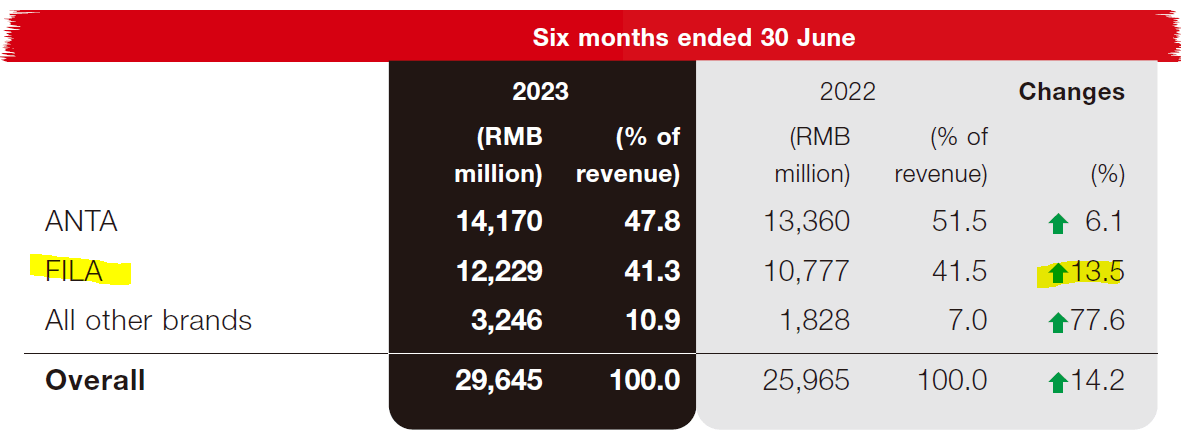

From the company's interim report, we can see DTC now accounts for the majority of ANTA's revenue and increased by 21.8% while revenues from traditional sales channels are the smallest in proportion and diminishing by 32.6%:

{kind=link}

ANTA launched the DTC (direct-to-consumer) transition in 2020, to mirror the successful DTC strategy of Nike , which started in 2017.

So far, ANTA appears to have done a good job of learning from its competitors:

- It learnt the best practice of using DTC from Nike and has shown good execution results financially.

- It avoided the pitfall of Li Ning where it increased its product prices astoundingly to blatantly take advantage of consumers' nationalistic sentiments.

If the company continues its due diligence of actively learning from its more successful peers and avoiding their pitfalls, ANTA should be able to maintain its current growth momentum.

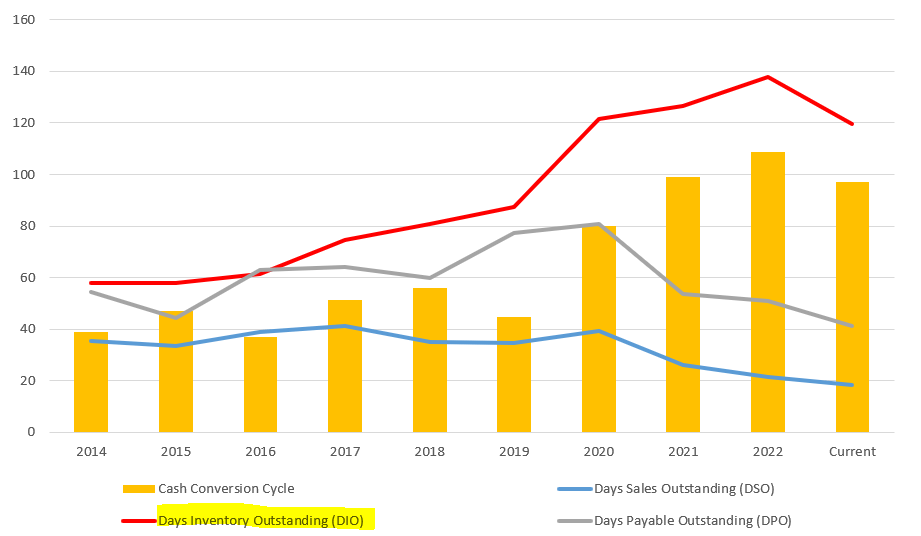

ANTA's Short-Term Inventory Challenge

ANTA has some short-term challenges with its inventory management. To illustrate this, we observe the company's Cash Conversion Cycle ("CCC") trend from a multiyear perspective and found it to be visibly increasing since 2020.

CCC is made up of 3 variables:

CCC = Days Inventory Outstanding ("DIO") + Days Sales Outstanding ("DSO") ? Days Payable Outstanding ("DPO")

Using data from Morningstar under "Operating and Efficiency", we plot the changes of these 3 variables of ANTA in the graph:

Cash Conversion Cycle (Morning Star)

{kind=link}

We can observe that of the 3 variables, DIO increased the most, suggesting that ANTA is holding onto its inventory for a significantly longer period.

From the company's 2022 annual report , ANTA's management attributed this to the pandemic and recently embarked DTC transformation.

Inventory Turnover (2022 annual report)

From the latest interim report, we observe this heightened inventory turnover is already experiencing a significant recovery:

Inventory Turnover (interim report)

The rise in inventory turnover is expected to be short-lived as China's supply chain activity continues to recover . While the DTC transformation was causing some short-term delay in inventory turnover, this transformation is expected to achieve greater sales efficiency to provide long-term growth for the company in the long run.

Investors should observe whether ANTA's inventory turnover continues to improve to eventually bring down the rising CCC trend.

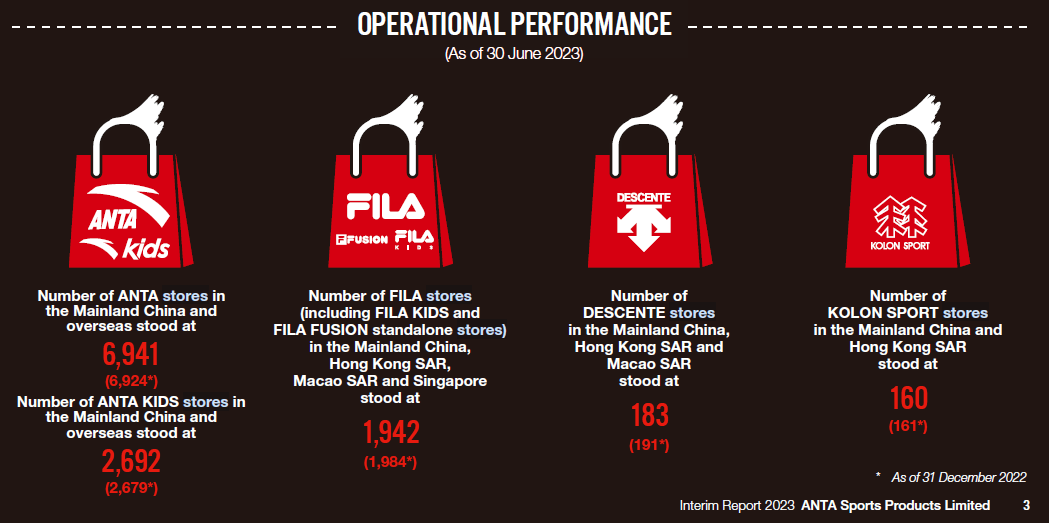

Increasing Store Numbers

From the interim report, the management provided the latest and targeted number of stores for each brand:

Current Store Numbers (interim report) Target Store numbers (interim report)

{kind=link}

{kind=link}

In my opinion, the company is not far from meeting its target. With a store number of 1942, the Fila brand has already met its target of 1900 - 2000 store number. The store numbers from other brands are also very close to their respective targets.

Not only has the Fila brand met its store targets, but these new stores have also increased its revenue significantly.

{kind=link}

For its homegrown " ANTA" and "all other" brands, investors should observe if the company can meet both its store number targets and continue its momentum of revenue growth at the same time.

This will indicate the new stores can effectively convert their inventory into sales, which will help to reduce their inventory turnover and will bring down the rising CCC trend eventually.

Capturing International Market Share

So far, we discussed how ANTA has risen above its predecessor Li Ning to become the top Chinese sportswear company. Now we explore the chances of it capturing a significant share in the international market.

Using a top-of-mind recall, I list down some famous sportswear brands that come up immediately in my mind. Using Seeking Alpha's summary page for each company, I estimated their market capitalizations and compared them with ANTA:

In my opinion, right now, although ANTA is visibly smaller than most of the leading international brands, it is not lagging too far behind. ANTA's size is still in the "ten of billions" range, similar to Lululemon and Adidas. I do not think ANTA will materially challenge Nike's dominance, but it might have a fair chance against other brands on the list.

Now, let's look at the overall strategy of ANTA to penetrate the international market. As observed earlier, ANTA's most successful brands based on revenue share are homegrown ANTA and the acquired international brand of Fila.

Before ANTA, Li Ning also tried to expand internationally using its homegrown brand when it opened its U.S. headquarters and flagship store in the US in January 2010. More than 10 years have passed and its revenue share from the international market is still less than 2%, as observed from the Guru Focus website earlier. Hence, based on Li Ning's experience, the odds of ANTA's homegrown brand achieving success internationally are not in its favour.

How about ANTA's Fila brand? Was there a precedence of success by a Chinese company in using an acquired international brand to dominate the market? I cannot think of an example from the sportswear market. However, in my opinion, looking at the e-commerce industry, we can infer from Alibaba's acquisition of the Lazada brand to capture the market share of e-commerce in the SEA region back in 2016.

According to this LinkedIn article, after the acquisition, what followed for Lazada was a series of disorganized changes in management that the author described as "a game of musical chairs". In terms of performance, Lazada is now lagging behind Shopee in terms of GMV ($21B against $73.5B). Also, this strategy failed despite Alibaba's repeated injection of cash into Lazada:

Alibaba has repeatedly injected cash into the company since 2022, with this most recent investment -- its third in 2023 -- bringing this year's total to over $1.8 billion.

Earlier in my article, I remarked that:

ANTA appears to be the most likely Chinese sportswear/athleisure brand that can surpass its predecessors to capture a significant share of the international market.

Compared to its predecessor Li Ning, I still think so, based on its financial prowess against Li Ning and its track record in emulating well-proven strategic execution.

However, in my opinion, concerning penetrating the international market, investors should take into consideration that ANTA does not have a successful strategy to emulate, which implies a significant amount of uncertainty in its international expansion plans.

ANTA announced a 5-year plan in 2019 to promote their brands to greater heights, both locally and internationally. Aside from ongoing incremental investments in R&D, the company also used the two Olympics events Tokyo 2020 and Beijing 2022 to boost its brand's awareness on the global scene.

ANTA also targets younger Generation Z by working closely with influential young idols and athletes such as Wang Yibo and Gu Ailing. This collaboration with international athletes in high-profile events appears to have been executed by its predecessor Li Ning as well with limited success. However, past failures might not imply future failures.

Investors should observe whether ANTA's executions in these plans will be successful in the long run.

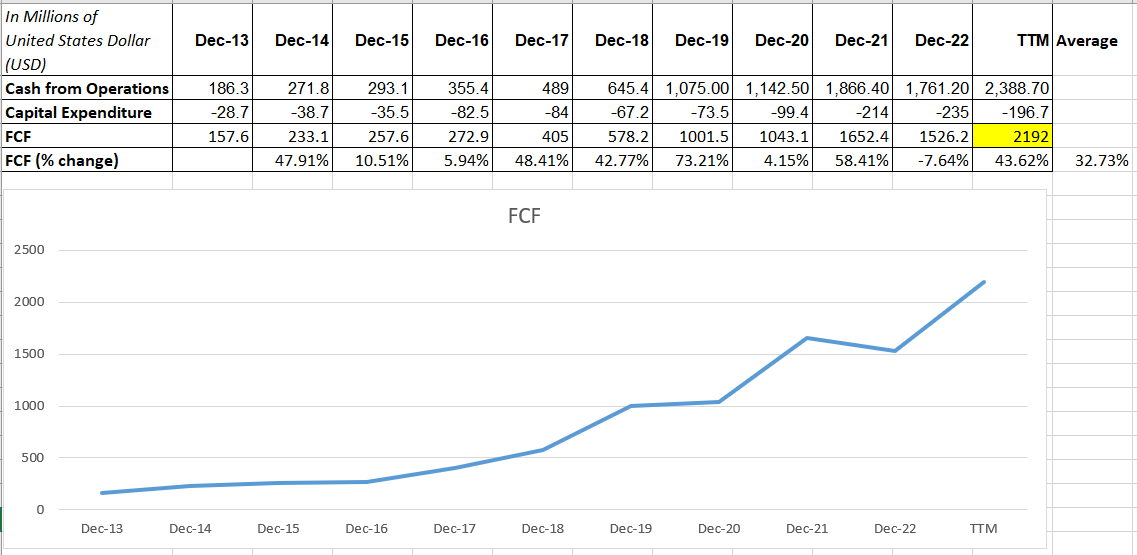

Valuation

ANTA has a very favourable top and bottom line that largely trickles down to its free cash flow ("FCF"):

{kind=link}

From the FCF graph tabulated from Seeking Alpha's data, on average, the growth in FCF is more than 30% per year.

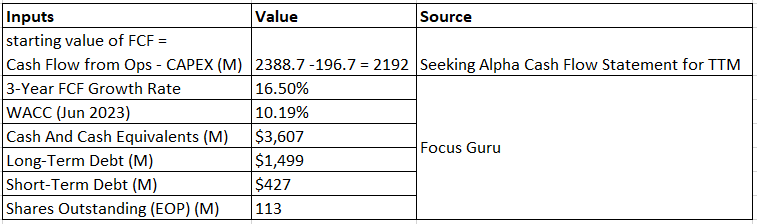

Here are the inputs and assumptions for my calculations of ANTA's intrinsic value using the DCF model:

Intrinsic Value Input (Calculated by Author)

{kind=link}

- The starting value of FCF is derived using cash flow figures from Seeking Alpha . The rest of the inputs are taken from different links from Focus Guru.

- For growth rate, Focus Guru's projection of 16.5% is reasonable and conservative since ANTA has historically grown its FCF by more than 30% on average, as discussed in an earlier section.

The Chinese government is well-known for taking sweeping measures to regulate targeted industries, as demonstrated in the crackdown on its major tech companies more than two years ago. This is also observed in the education business. We have not witnessed such drastic measures in the sports industry yet, which ANTA is in. Still, in my opinion, this presents a material uncertainty unique to investing in Chinese companies.

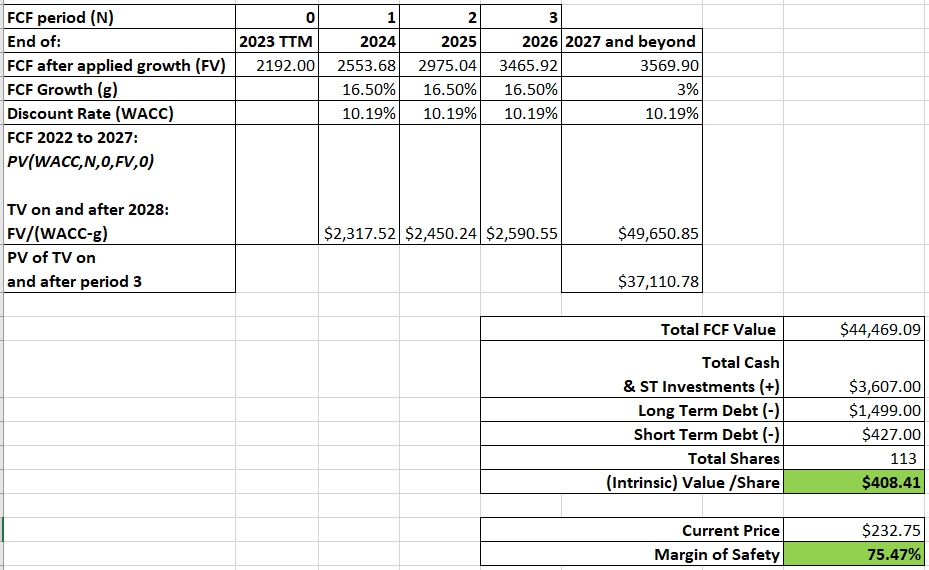

With such uncertainty in mind, I will model my DCF calculation with a more conservative growth timeline by assuming that ANTA will continue to grow by 16.5% for only the next 3 years (as opposed to my usual preference of 5 years), with growth tapering to a terminal value of 3%:

Intrinsic Value (Calculated by Author)

{kind=link}

Taking into account the company's short-term liquid assets and debt, the intrinsic value is $408.41, implying the stock is deeply undervalued , presenting an upside of more than 75%.

Risks

ANTA inherits the same regulatory risks as other Chinese stocks due to the government's willingness to impose sweeping measures on targeted companies, forcing them to comply even if it means greatly hurting their bottom line for the benefit of the public's welfare. This started more than 2 years ago and is still happening recently .

Investors should only invest in ANTA if they are comfortable with this risk.

Conclusion

ANTA has outperformed its peers only in the Chinese market mainly by emulating successful strategies and avoiding pitfalls committed by its peers.

Despite short-term inventory challenges due to the pandemic and DTC transformation, recovery signs are evident from its latest interim report.

In the international market, ANTA is the most likely Chinese sportswear company to capture a significant market share. However, there has not been a precedence of such a success among the Chinese sportswear companies. I discussed earlier that ANTA's strengths lie in emulating successful strategies from its peers. Hence, without such precedence of success, its prospect of expanding internationally is uncertain.

The stock is undervalued, but investing in a Chinese company like ANTA presents regulatory uncertainties which investors should be aware of.

Overall, this stock is a ' buy ' only for investors who understand and accept the regulatory risks associated with investing in the Chinese stock market.

For further details see:

ANTA Sports: Great Domestic Sportswear Company With Uncertain International Prospect