ANFGF - Antofagasta: Still One Of The Best Copper Stories Out There

2023-06-23 10:30:00 ET

Summary

- Antofagasta is a London-listed copper mining company with a specific focus on Chile.

- This year, the company will produce in excess of 1.5 billion pounds of copper at a cash cost of $1.65 per pound.

- The year started weak, but the production will increase throughout this year.

- Increasing volatility in the copper sector may create interesting entry points.

Introduction

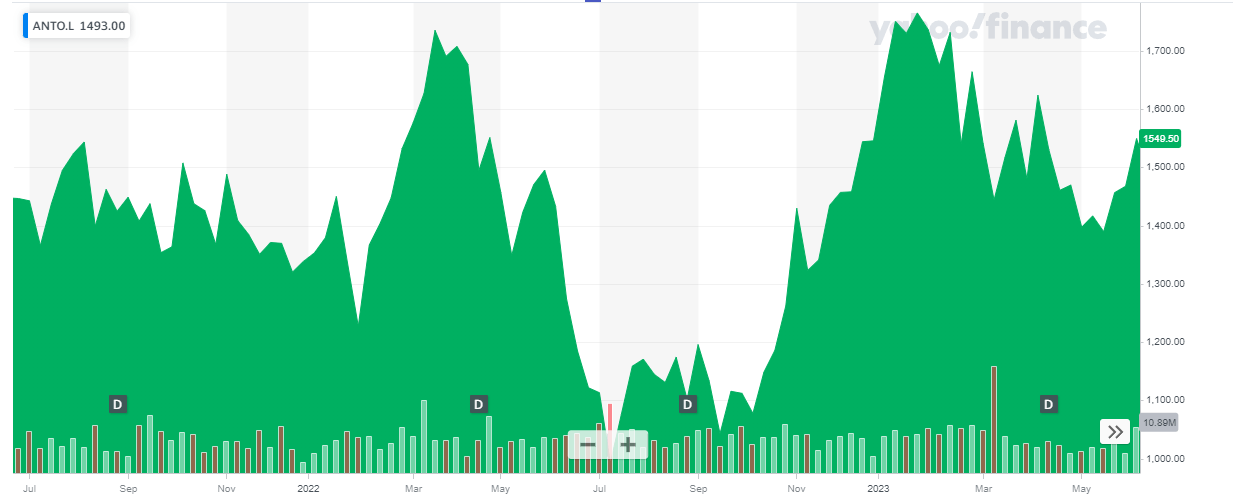

The share price of Antofagasta ( OTC:ANFGF ) has increased by approximately 40% since my previous article on the company was published. After a very weak production result in H1 2022, I argued the copper output would increase sharply in the second half of the year . That effectively happened but the total copper production in 2022 fell by a double-digit percentage as the stronger second semester couldn’t make up for the ‘lost pounds’ in the first half.

{kind=link}

Antofagasta’s primary listing is in London where the company is part of the FTSE 100. The ticker symbol on the LSE is ANTO, and the average daily volume exceeds 1.7 million shares . There are just over 985M shares outstanding resulting in a market cap of just under 15B GBP (around 19B USD at the current exchange rate). Although the company’s primary listing is in London, I will not convert the financial results in GBP as Antofagasta reports its results in US Dollars.

The strong copper price boosted Antofagasta’s cash flows in 2022 - but the output was disappointing

As explained in my previous article, the copper production at Antofagasta would be weighted towards the second half of the year as the company had to deal with drought and reduced concentrate pipeline availability at Los Pelambres while the average grades at the Centinela concentrator were lower as well.

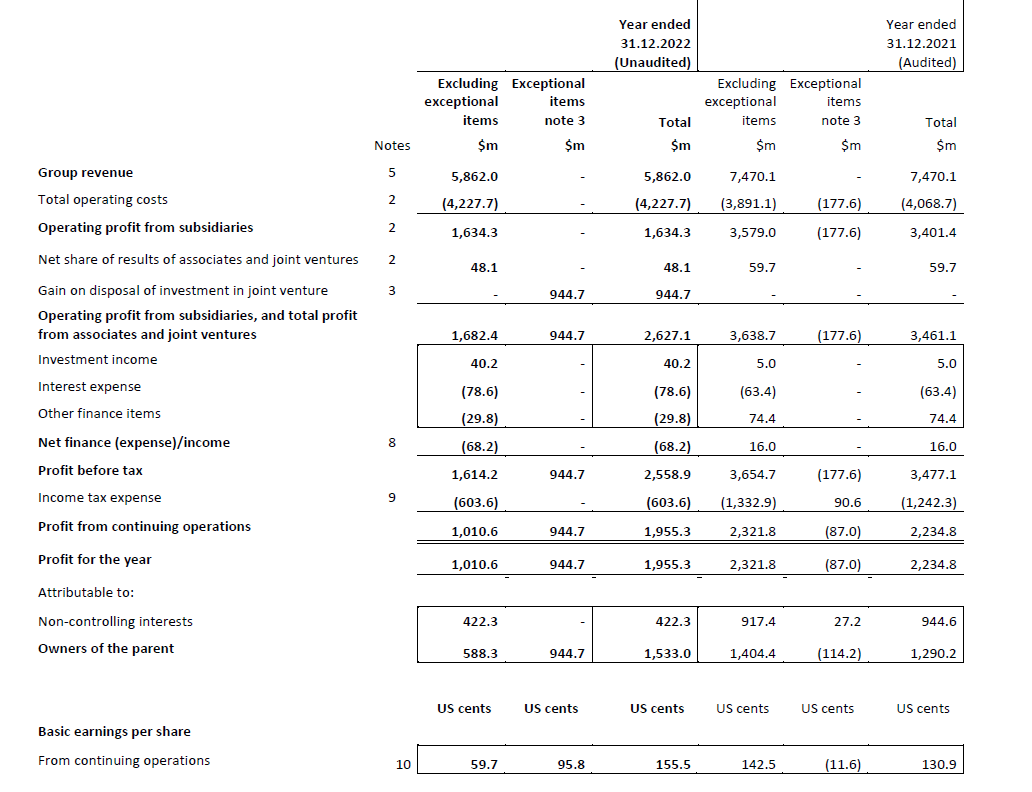

The total revenue for the year was approximately $5.86B . That’s substantially lower than in 2021 when Antofagasta was able to record a $7.47B revenue thanks to a higher production rate and higher average copper price. Unfortunately the operating expenses also increased in 2022 (hardly a surprise) and this resulted in a contraction of the operating profit which dropped by more than 50% compared to 2021.

{kind=link}

As you can see in the image above, Antofagasta reported a total operating income (including a $48M contribution from associates and joint ventures) of $1.68B. And after deducting the $68M net finance expense, the pre-tax income fell to $1.61B resulting in a net profit of $1.01B of which $588M was attributable to the shareholders of Antofagasta. The earnings per share from continuing operations fell to 59.7 dollarcents (the EPS including the non-recurring gain on an asset sale was 1.55 USD). While this means the stock is trading at approximately 25 times earnings, let’s not forget 2022 was a disappointing year in general and the company expects the copper, gold and moly output to increase this year (I will discuss the outlook for this year later in this article).

As Antofagasta’s operations have a long mine life with a high up-front construction cost and relatively moderate sustaining and maintenance capex, I’m also always interested in the free cash flow result of a mining company in general, and definitely in Antofagasta’s cash flow results.

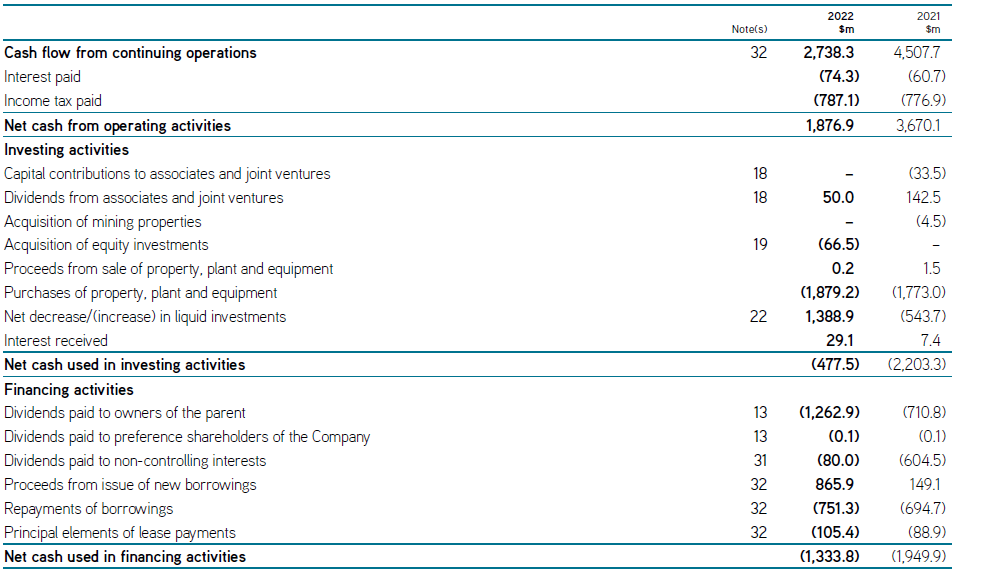

As you can see below, the starting point of the cash flow statement is the $2.74B cash flows from continuing operations.

{kind=link}

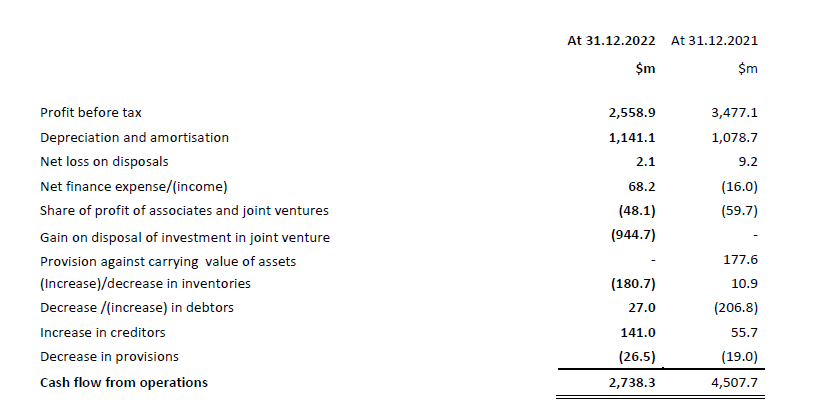

Fortunately the footnote provides more details. The cash flow from operations obviously does not take the non-recurring gain on the sale of an asset into consideration, and looking at the details, there was a total net investment of approximately $38M in the working capital position and the provisions.

{kind=link}

So adjusted for the working capital changes, the underlying operating cash flow is approximately $1.92B. We should add back the 29M USD In interest received and 50M USD in received dividends while we should also deduct the 105M USD in lease payments, resulting in an adjusted operating cash flow of just under $1.9B.

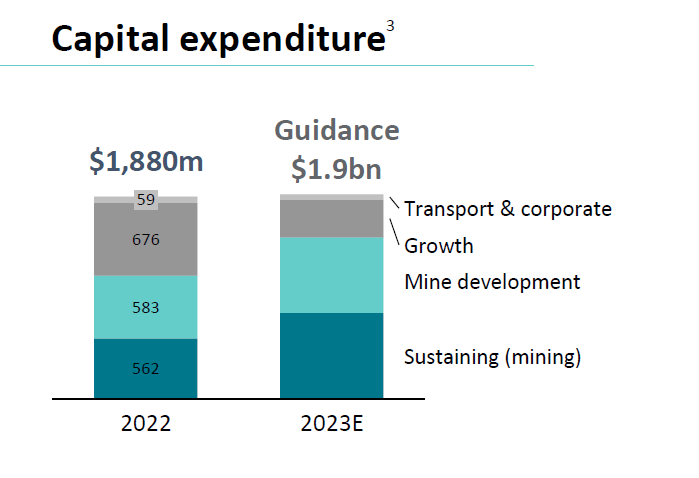

While the total capex of $1.88B means the company was barely breaking even, keep in mind that A) there was a substantial cash inflow of almost $1.4B from the sale of an asset so the balance sheet remains robust. And keep in mind only about $560M of the total capex is classified as sustaining capex. The rest of the capex is related to mine development expenditures and growth investments. This means the total net sustaining free cash flow was approximately $1.3B (and this obviously still excludes the cash inflow from the asset sale).

Not the entire amount is attributable to Antofagasta’s shareholders. As we saw in the income statement, about 422M USD of the total net income was attributable to non-controlling interests. However, only 80M USD of the attributable profit was registered as a dividend that was paid to the non-controlling interests.

The problem is that you don’t exactly know what percentage of the sustaining capex (and growth capex) is attributable to the non-controlling interests and the ‘fair’ impact of the attributable net income is likely somewhere in between the 80M and 422M USD. But even if you would deduct the entire 422M USD as some sort of ‘theoretical’ portion of the profit and cash flow attributable to third parties, the net sustaining free cash flow would still be around $900M and in excess of $0.90 per share for Antofagasta shareholders.

And considering it wasn’t a great year, that’s not a bad result at a copper price of $4/pound.

Expect a high single digit production increase this year

While the total production in FY 2022 was a little bit disappointing, it was caused by a temporary throughput reduction at Los Pelambres and a lower production at Centinela. That’s unfortunate but Antofagasta seems to be pretty confident this will be a non-recurring impact (of course, drought it not something you can really predict and it is a risk we will have to take into consideration going forward). For the current financial year, Antofagasta’s official production guidance is 670,000-710,000 tonnes of copper , 220-240,000 ounces of gold and 10-11,500 tonnes of molybdenum. A portion of the higher copper output is related to the completion of the expansion of the Los Pelambres desalination and concentrator and Antofagasta is guiding for a copper production that will increase every single quarter of this year.

The mid-point of the copper production guidance would indicate a YoY production increase of almost 7%. That’s great, but the most noticeable impact will come from the higher gold production. The mid-point of this year’s output guidance would represent a YoY production increase of approximately 30%. While that sounds impressive we also shouldn’t get overly excited as a 50,000 ounce increase in the gold production will add just about $100M to the revenue and cash flow. Definitely nothing to sneeze at but it’s not a company changing even.

The production cost this year will come in at $1.65 per pound of copper on a cash cost basis and after deducting the impact from by-product credits. That’s slightly higher than last year, mainly because of the anticipated lower molybdenum price. In its outlook, Antofagasta is also referring to anticipated lower gold prices but that still remains to be seen; the price impact of molybdenum is definitely more important.

The total capex for this year will be $1.9B of which $1.5B is earmarked for sustaining capex and mine development capex . This mine development capex does include the investments related to the expansion of the desalination plan and engineering work on the ‘second concentrator’ project at Centinela. This means the ‘real’ sustaining capex is substantially lower and as explained in the first portion of this article, the sustaining capex excluding mine development was just $562M in FY 2022. While this will increase, it will likely remain limited to $750-800M this year.

{kind=link}

Investment thesis

Antofagasta expects the copper production to continue to increase on a quarter-on-quarter basis this year which means the Q1 production of 146,000 tonnes should be the lowest point of the year. The increasing production numbers are coinciding nicely with the increase of the copper price and just like last year, this does mean the second half of the year should be better for the company (of course this is subject to the copper price in the second semester).

The 2022 results could be seen as a benchmark for the financial results using a robust copper price but a conservative copper production. The increased production should boost the cash flow results this year (the moly price is an unknown factor here though) and this validates Antofagasta as an interesting pick in the copper space. The stock isn’t cheap right now (as its share price has jumped by about 40% since my previous article was published) but given the current volatility in the commodity markets it’s perhaps a good idea to add (or keep) Antofagasta on your shortlist of ideas.

For further details see:

Antofagasta: Still One Of The Best Copper Stories Out There