HBRIY - APA Corp.'s Egypt Operations Offset By Domestic And U.K. Headwinds (Downgrade)

2023-06-05 10:59:43 ET

Summary

- APA Corporation is a $10.4 billion market cap U.S. & international oil and gas producer with a 3.0% dividend yield. Operations are in the U.S., Egypt, Suriname, & the UK.

- The company has been particularly impacted by lower natural gas prices, particularly in the Permian Basin. Its UK production is subject to new, extraordinarily high tax rates.

- APA merits additional review if average Permian natural gas prices increase (beyond normal winter upswing) or APA can announce a Suriname development schedule.

APA Corporation ( APA ) produces gas and oil from the U.S., Egypt, and the UK’s North Sea. It also has a discovery currently under appraisal in offshore Suriname (near Venezuela).

Dividends yield is 3.0%, smaller than the less risky 2-year US Treasury rate. APA meets its pledge to return a minimum of 60% of free cash flow to shareholders with dividends and share repurchases.

Because of the challenges of selling Alpine High (Delaware sub-basin in the Permian) natural gas, APA has struggled more than many companies in the sector. The temporary spike in global natural gas prices gave the company a lift last year; however, gas prices have fallen by 75% or more and are expected to remain depressed until more LNG capacity comes on in 2024. APA faces additional challenges because its Alpine High gas competes with zero-marginal-price oil-associated Permian gas and gas pipeline takeaway capacity from the region is insufficient.

Europe was in dire need of natural gas (and oil) during 2022; however, the UK government’s approach of nearly doubling the tax on North Sea production ensures companies will choose other projects away from the North Sea. The tax hike also limits the value of APA’s North Sea reserves, although these only represent about 10% of the company’s total reserve value.

I recommend APA Corporation as a “hold.”

Oil and Natural Gas Prices

From the weekend’s OPEC meeting: the Saudis are electing another million BPD cut, which takes total cuts to 4.66 million BPD, or about 4.5% of world production.

In the U.S., companies are tied to maintenance capital spending for oil and very little spending for gas drilling.

June 2, 2023, closing oil price for West Texas Intermediate ((WTI)) crude oil at Cushing, Oklahoma for July 2023 delivery was $71.74/barrel. Natural gas price for July 2023 delivery at Henry Hub, Louisiana was $2.17/million British Thermal Units ((MMBTU)).

EIA

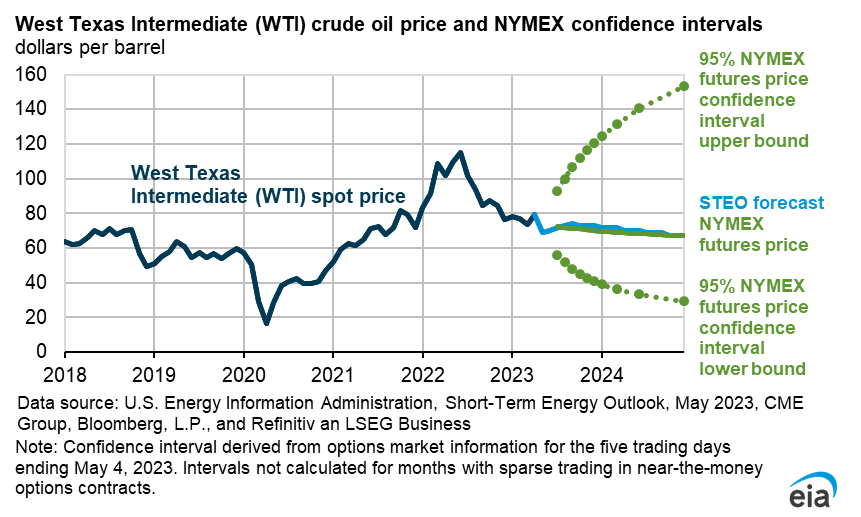

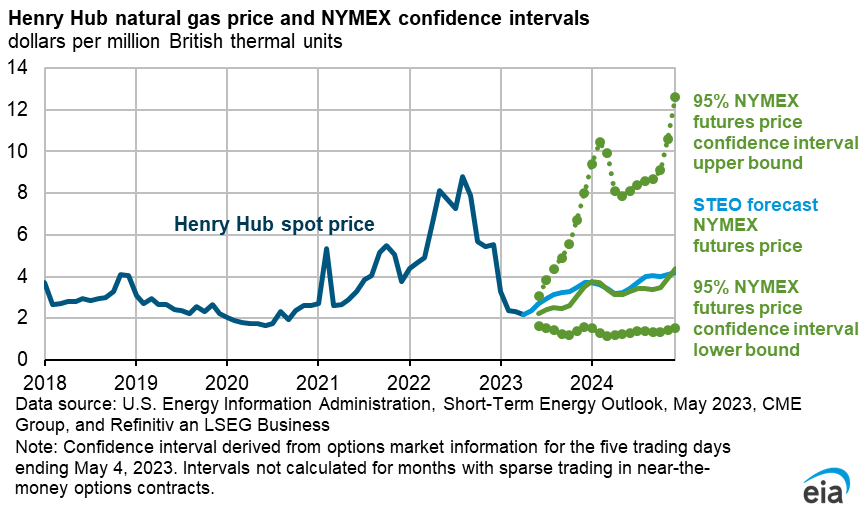

Supply and demand factors point to stable oil prices and seasonally higher natural gas prices in the second half of 2023.

The EIA’s 5-95 confidence interval charts for both oil and gas prices through the end of 2024 are shown below. The oil price range by year-end 2024 is $30-$155/barrel. The gas price range fluctuates seasonally.

{kind=link}

{kind=link}

The UK NBP (National Balancing Point) reference natural gas price—important for APA’s small volume of UK gas production—has shrunk to $6.87/MMBTU for July 2023 delivery. However, it rises to $14.54/MMBTU for January 2024 delivery.

APA’s Permian Natural Gas Problem

A major issue for APA is its Alpine High natural gas (in the Delaware sub-basin of the Permian) is far from markets and competes with the associated gas that surfaces with oil. So gas production from the Permian is responsive to the oil price, not the gas price. The West Texas gas price (Waha reference price) is particularly important for APA given its large Alpine High gas reserve. This price is often under pressure and has actually gone negative several times.

According to the most recent issue of Natural Gas Weekly from the Energy Information Administration ((EIA)), natural gas production from the Permian was at an all-time high of 21 BCF/D in 2022. This was 14% above the 2021 average. The Permian is the second-largest producing area in the country after Appalachia, which produced 34.8 BCF/D in 2022.

At present, Permian Basin gas prices have gapped lower than the reference Henry Hub prices. They are expected to remain lower until additional Permian gas pipeline takeaway capacity comes on in late 2024.

EIA

First Quarter 2023 Results

In the first quarter of 2023 , APA reported net income of $242 million or $0.78/share. This is compared to net income of $1.9 billion or $5.43/share for 1Q22.

Net cash provided by operations was $335 million and adjusted EBITDAX was $1.3 billion. Free cash flow was $272 million for the quarter.

The company produced 394,000 BOE/D; adjusted production excluding Egyptian noncontrolling interest and tax barrels was 318,000 BOE/D. About half of production was from the U.S., an eighth was from the North Sea, and about three-eighths was from Egypt.

On a global basis, production was

*50% oil,

*14% natural gas liquids

*36% natural gas.

Due to lower Permian Basin gas prices, APA announced a $100 million reduction in its 2023 capital budget of $1.9 billion-$2.0 billion. 1Q23 upstream investment was $495 million. The company repurchased $142 million of stock.

For the 2Q23, the company expects similar capital expenditures and slightly larger production of about 324,000 BPD.

Worth noting also is APA’s 140 MMCF/D gas supply contract to Cheniere Energy, Inc. ( LNG ) starting August 1, 2023, and expected to have a $175 million positive cash flow impact in 2H23.

APA is a joint venture partner with TotalEnergies SE ( TTE ) and is appraising finds in offshore Suriname (Krabdagu), near oil-producing countries Venezuela and Guyana. They have not yet announced a development schedule.

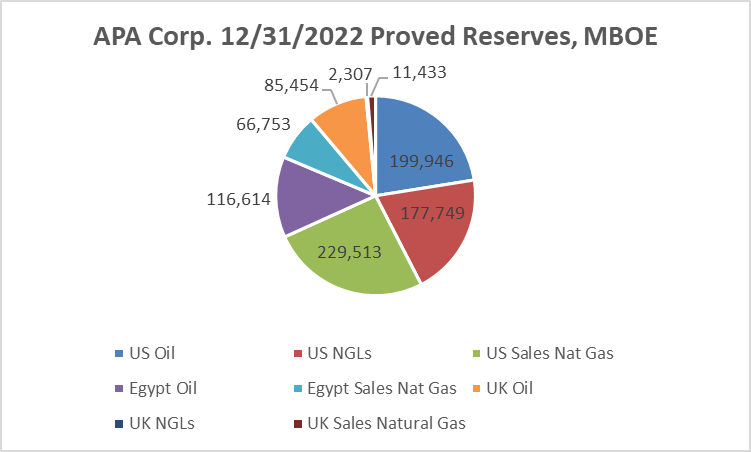

Reserves

At December 31, 2022, APA's total estimated proved reserves were 890 million BOEs. Most are proved developed. Note that prospective reserves from Suriname have not yet been proven up, so are neither booked nor included here.

Of the 890 million BOE total, 402 million barrels (45%) were oil, 180 million barrels (20%) were natural gas liquids, and 1.8 trillion cubic feet (or 308 million BOE or 35%) were natural gas.

Proved reserve categories are shown below. The graph makes clear that nearly half of APA’s proved reserves are U.S. natural gas liquids and U.S. natural gas, both of which are lower valued than oil on an $/BOE basis.

{kind=link}

The present value of future net cash flows at a 10% discount rate (PV-10), a standard measure of comparison for reserves, is $17.6 billion for year-end 2022. This compares to $12.4 billion for year-end 2021 for a similar reserve volume, so the difference is almost completely the higher prices used in the calculation.

The $17.6 billion reserve PV divides as:

$10.7 billion U.S.;

$5.1 billion Egypt;

$1.8 billion UK.

Competitors

APA is headquartered in Houston, Texas.

With U.S. operations in the Permian Basin, Eagle Ford shale, Austin Chalk, the U.S. Gulf Coast, and the Gulf of Mexico, APA competes directly with virtually every company exploring and producing in the US except Utica/Marcellus-only or Powder River-only companies.

International competitors include BP p.l.c. ( BP ), Harbour Energy plc ( HBRIY ), Chevron Corporation ( CVX ), ConocoPhillips ( COP ), Equinor ASA ( EQNR ), Exxon Mobil Corporation ( XOM ), Qatar Petroleum, Shell plc ( SHEL ), and Total.

In Suriname, companies work with Suriname state company Staatsolie.

Governance

At June 1, 2023, Institutional Shareholder Services ranked Apache’s overall governance higher than in the past —a 4, up from an 8, with much improved sub-score of audit (2, up from 8), board (1), shareholder rights (7), and compensation (9). In this ranking a 1 indicates lower governance risk and a 10 indicates higher governance risk.

At May 15, 2023, shorts were 4.1% of floated stock. Insiders own only 0.43% of shares.

The company’s beta is 3.53, far above the overall market, but in line with oil and gas price volatility in the US and abroad.

At March 30, 2023, the largest institutional stockholders, some of which represent index fund investments that match the overall market, were Vanguard (13.5%), BlackRock (8.9%), State Street (7.0%), Hotchkis & Wiley (5.5%), Invesco (4.0%), and Harris Associates (3.5%).

BlackRock, State Street, and Invesco are signatories to the Net Zero Asset Managers initiative, a group that, as of December 31, 2022, managed $59 trillion in assets worldwide and which (despite less energy supply due to reduced Russian exports to Europe) limits hydrocarbon investment via its commitment to achieve net zero alignment by 2050 or sooner.

Financial and Stock Highlights

APA’s market capitalization is $10.4 billion at the June 2, 2023, stock closing price of $33.68 per share. The company’s 52-week price range is $30.15-$51.95 per share, so the closing price is 65% of the one-year high. The price is 71% of the one-year target of $47.56.

Trailing twelve-month ((TTM)) EPS is $6.70, giving a current price-earnings ratio of a bargain 5.0.

The average of analysts’ expectations for 2023 and 2024 EPS is $4.81 and $6.29, respectively, for forward price-earnings ratio range of 5.4-7.0.

TTM returns on assets and equity are an excellent 23% and 215%, respectively.

TTM operating cash flow was $4.4 billion and levered free cash flow was $2.7 billion.

At March 31, 2023, APA had $11.8 billion of liabilities including $5.8 billion in long-term debt, $2.45 billion in current liabilities, and $2.0 billion in asset retirement obligations. Assets are $13.2 billion for a very steep liability-to-asset ratio of 89%.

Be aware that balance sheet ( an accounting number, not market capitalization) shareholder equity on March 31, 2023, was only $444 million. It is outweighed on the balance sheet by the Egyptian noncontrolling interest of $990 million.

Recall that APA has pledged to return a minimum of 60% of free cash flow to shareholders via dividends and share repurchases.

The dividend of $1.00/share yields 3.0%. However, at present, the less-risky two-year US Treasury rate is 4.33%.

Overall, the APA Corporation’s average analyst rating is 3.0, or “hold” from the 29 analysts who follow it. However, at least one analyst considers the company significantly undervalued.

Notes on Valuation

APA Corporation book value is quite low at $1.44/share. That it is a fraction of the market price indicates positive investor sentiment.

As noted, PV-10 reserve value is $17.6 billion. Enterprise value is $16.0 billion. Market capitalization is $10.4 billion.

The ratio of enterprise value to EBITDA is an astonishingly low (bargain) 2.6, far below the maximum of 10.0.

The $10.4 billion market capitalization gives APA average-level $32,700 per flowing BOE and $61,900 per flowing barrel of oil. Both numbers exclude Egypt noncontrolling interest and tax barrels.

Positive and Negative Risks

It is not unusual for countries to unilaterally attempt to change the terms of their agreements with multinational producers. This could be a risk in Suriname. Indeed, this occurred in the UK with an increase in the tax rate on offshore North Sea production from 40% to 75%.

APA is long-established in Egypt, so it appears less likely there.

It is possible that the Suriname find could be less economical than hoped.

Increasing Permian basin oil production and increasing gas-oil ratios as the field ages has and will increase the production of associated gas, risking even more over-supply. Gas pipeline takeaway capacity is considered insufficient until buildout in 2024.

Risks include U.S. political and regulatory risk — particularly with banks and several states still taking a race-to-zero-hydrocarbons posture. All are led by the U.S. Biden administration, which remains bizarrely keen to eliminate U.S. oil and gas production entirely.

Inflation, while it can raise the price of oil since oil is denominated in dollars, also increases operating and financing costs.

Investors should consider their oil and natural gas price expectations as the factors most likely to affect APA.

Recommendations for APA Corporation

APA Corporation’s results are hurt by the fall in natural gas prices in the U.S. and abroad, and additional taxation in the UK. There is standard, but enormous, uncertainty around the timing and volume of new production from offshore Suriname. Production from Egypt continues apace but results there are not enough to backstop the far-lower Permian gas prices.

In a time of higher US Treasury rates, APA’s 3.0% dividend is appealing but modest.

Due to the continuing gas price challenges for gas from its large Alpine High development, I am downranking APA Corporation from buy to hold.

apacorp.com

For further details see:

APA Corp.'s Egypt Operations Offset By Domestic And U.K. Headwinds (Downgrade)