CPE - APA Corporation: The Callon Petroleum Acquisition Creates An Overall Win

2024-01-06 02:25:15 ET

Summary

- APA announced it will acquire Callon Petroleum in a $4.5 billion all-stock deal, boosting its total free cash flow and size of its Permian acreage.

- The newly acquired acreage has a higher oil content than its existing Permian assets.

- The deal has the potential to dilute APA's Egyptian assets and achieve a multiple more in line with Permian peers.

- APA expects $150 million in annual synergies and a 1.5% increase in EBITDAX, but the operational pairing lacks geological synergies.

Thesis

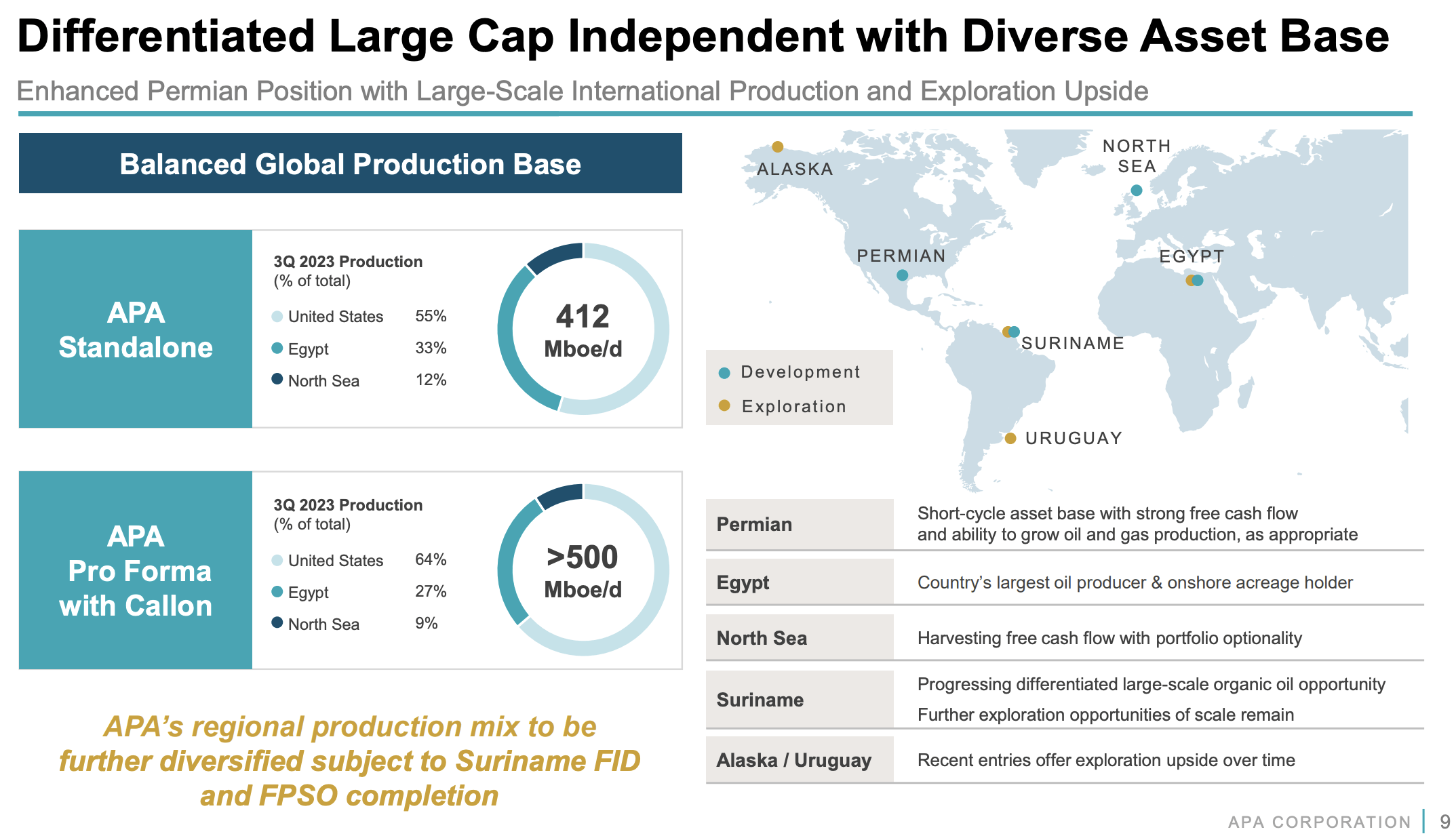

APA (APA) announced that it has reached an agreement to acquire Callon Petroleum (CPE) for approximately $4.5 billion in an all stock deal. APA traded down 7.35% following the announcement and closed at $34.05/share. The deal helps APA boost its total operations to over 500 MBOE/d with 64% of that production coming from the US.

While this deal certainly makes APA a bigger company, bigger isn't always better. In this article, I will examine how the deal will affect APA's realized pricing as well as operating costs on a per BOE basis. I will also determine if the sell-off following this announcement presents a buying opportunity.

Company Snapshot

APA is an independent oil producer with a little bit of everything. It owns land-based oil, NGLs, and natural gas production facilities in the Permian Basin of the United States, as well as Egypt. In addition, it also produces offshore in the northern sea off the coast of the United Kingdom.

The large shiny object the company is currently developing is in Suriname. Suriname is a small country in the North East portion of South America. APA has a 50% working interest in block 58 and a 45% working interest in block 53 off the Suriname coast.

{kind=link}

APA has partnered with the French company Total Energy (TOTZF) to explore and develop potential oil reserves located in these blocks. The two companies hope to mimic the success seen in neighboring Guyana (developed by Exxon (XOM) and Hess Corporation) which is several years ahead on the production curve.

Highlights of the Transaction

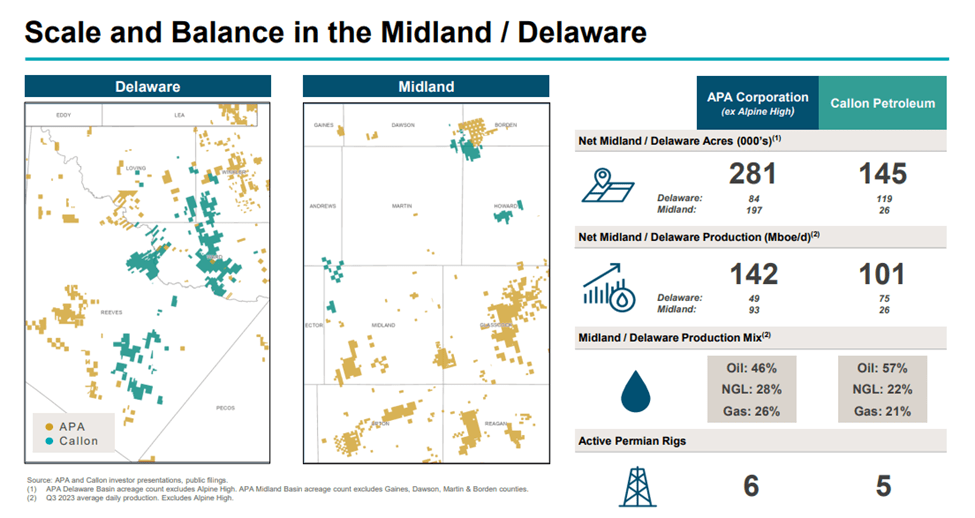

By bringing Callon into the fold, APA boosts its Permian acreage by roughly 50%. The bulk of this acreage (82%) is in the Delaware basin in the Reeves and Ward counties. This has the benefit of pushing the production profile of APA to become predominantly US oriented.

In my previous article on APA in May, I discussed how APA was generally undervalued on a per BOE basis compared to other producers. I believe its Egyptian assets are viewed by investors as a liability despite their high oil content. Part of this deal may be oriented around attempting to dilute its Egyptian assets in order to achieve a multiple more in line with Permian peers. If this works out, it will be a very cost-effective method of multiple expansion.

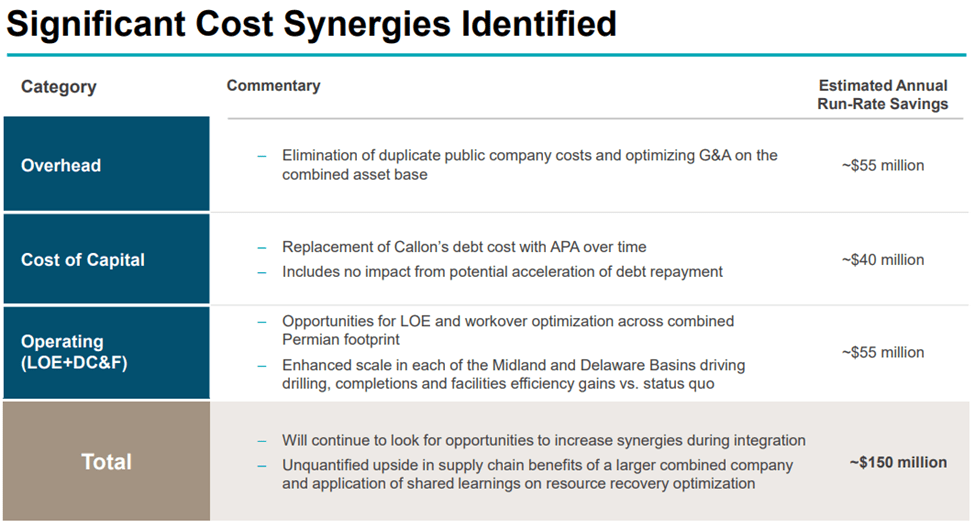

There are also operational aspects to this deal as well. When two companies merge, there is also the expectation of improved efficiencies and capabilities. The main operational benefit being advertised by APA is more efficient rig usage and continued benefits in economies of scale. As a result of this deal, APA projects to realize $110 million in annual operating synergies. Thus far, in 2023, APA has recorded $3.9 billion in EBITDAX . Therefore, these synergies will yield approximately a 1.5% increase in EBITDAX.

APA also projects to save on costs of capital. The projections target $40 million in savings associated with achieving better terms on the Callon debt. The savings in debt related costs will translate into an increase in earnings of $0.10/share.

{kind=link}

One complaint I can muster is that this pairing does not have a lot of geological synergies. The two companies only have a few select locations where they shared property lines. To make a good operational pairing, acquiring your neighbor allows for increased drilling laterals and operating efficiency. APA has a high operating cost per BOE compared to its peers, and I would like to see it focusing on unlocking more 3-mile laterals to get that number down. These long laterals are key to maximizing the production for dollars spent.

{kind=link}

Better in the Permian, Slightly Better Economics as a Whole

As a whole, APA doesn't have great operational statistics compared to other large cap peers. With an oil spread of only 37% of total production, its realized price in the Permian is $41.19/BOE. It also has a relatively high cost of operations, coming in at $14.40/BOE. The table below summarize the Q3 operating performance of several large cap Permian producers. All information is derived from the companies' 10-Q reports.

| Q3 Realized Price |

| Q3 Operating Expense |

| DVN |

| $46.92/BOE |

| $12.19/BOE |

| FANG |

| $54.37/BOE |

| $10.51/BOE |

| PXD |

| $52.13/BOE |

| $11.58/BOE |

| APA (Permian only) |

| $41.19/BOE |

| $14.40/BOE |

| CPE |

| $54.50/BOE |

| $14.30/BOE |

APA is slightly different from this group by having foreign assets. The high oil content of its Egyptian and North Sea assets drastically improve its margins. The benefit of acquiring CPE is these assets have essentially the same realized price per BOE as APA as a whole, due to its higher oil cut. CPE accomplishes this while having a lower operating expense per BOE and will be dilutive to the combined company. The overall impact will be higher margins for APA going forward.

The table below compares the full APA portfolio with CPE.

| Q3 Realized Price |

| Q3 Operating Expense |

| APA (All) |

| $54.82/BOE |

| $15.64/BOE |

| CPE |

| $54.50/BOE |

| $14.30/BOE |

Debt Maturities Have Become More Complicated

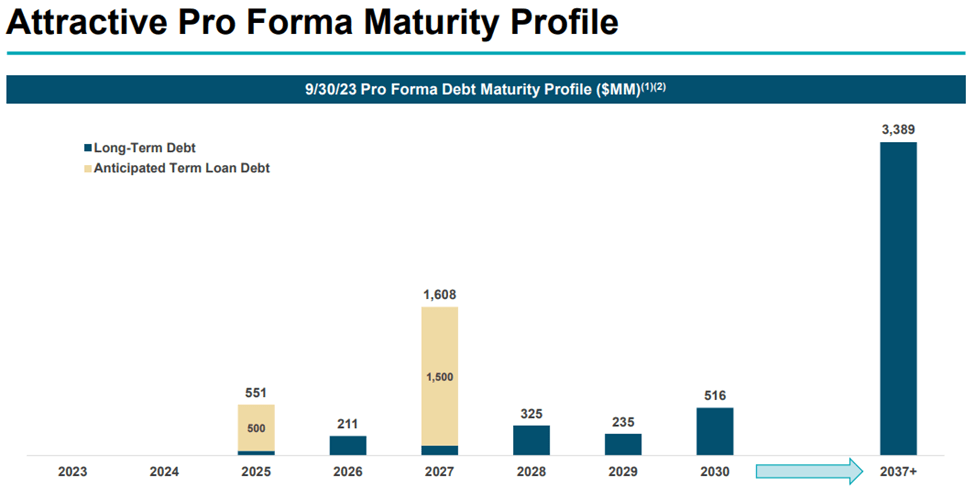

One of my favorite aspects of APA prior to this transaction was the spacing and very manageable amount of annual maturities in the 2025-2030 time frame. I viewed this as important because this is the theoretical ramp up period for operations in Suriname.

Suriname is a 200 MBOE/d project that will be a monumental addition to APA. Having debt maturities get in the way of that is a mistake. 2027 now has $1.6 billion in debt due, up from a measly $100 million. This is not the kind of problem I would like to be solving when the company should be all hands on deck with Suriname. This is probably a minor detractor in the grand scheme of it all as it can be refinanced, but I'm just not a fan of the idea.

{kind=link}

Risks

Energy prices limped to the finish line of 2023 and are continuing to show weakness in the first week of 2024. If these do not improve, FCF will suffer in Q1 and potentially beyond. However, given the 7.5% price drop that was seen on Thursday, a significant amount of price risk has been taken out of the stock.

APA also has a significant portion of its production tied to natural gas. I do not see much help in that area until the end of 2024 or early 2025 when LNG exports begin to ramp. I expect this portion of the portfolio to continue to underperform for the near term.

Finally, any prolonged time period of depressed oil prices will also create pressure on the FID of Suriname, as the project is less economical at lower energy prices. I view long term WTI prices to be in the range of $75-$80/barrel so I do not see this as an immediate risk but could manifest itself as a result of global economic distress.

The Bottom Line

The acquisition of CPE has its pluses and minuses, so let's review.

1. An increased percentage of US based production presents the opportunity for multiple expansion as its foreign assets become diluted by the larger company.

2. A fair amount of cost savings will be realized by increasing Permian production by 50%. Economies of scale will be realized to the amount of approximately $110 million of annual operating expense savings.

3. $40 million in annual savings related to the cost of capital using APA debt financing.

4. There is low geological synergies due to general lack of neighboring acreage. This will not improve its reserves of three mile laterals to aid in cost reductions.

5. The debt maturity cadence is not as attractive as it once was. $1.5 billion in additional maturities due in 2027 is inopportune during the potential ramp in Suriname.

Overall, the pluses outweigh the minuses, so I feel this acquisition is a win. With prices returning to just $0.13/share above my previous buy rating, I maintain my BUY rating for a long term growth position.

For further details see:

APA Corporation: The Callon Petroleum Acquisition Creates An Overall Win