KBWY - Apartment REITs: Tracking For Soft Landing

Summary

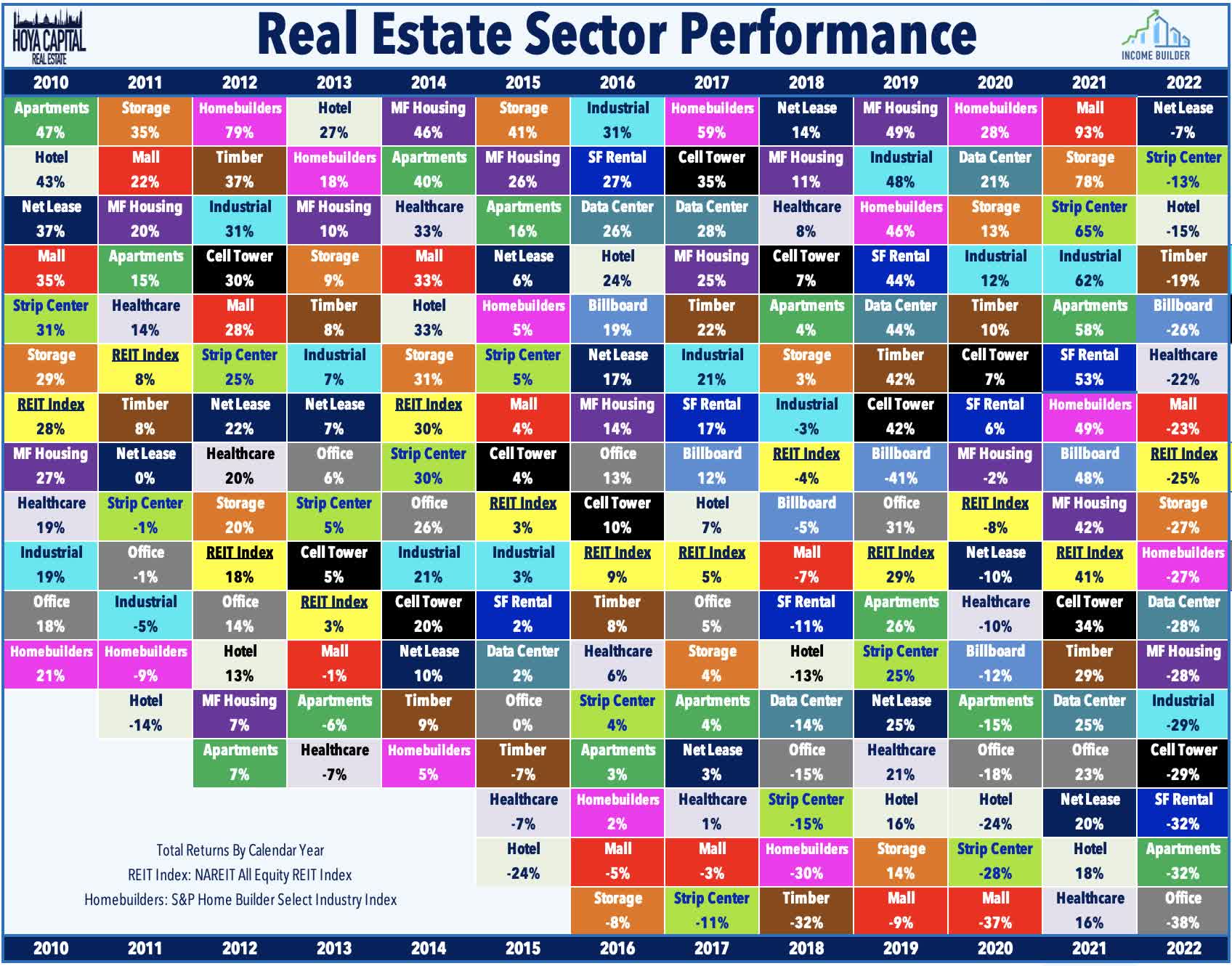

- Apartment REITs were the second-worst-performing property sector in 2022 - barely outperforming the troubled office sector - despite delivering a record year of operating performance highlighted by 20% FFO growth.

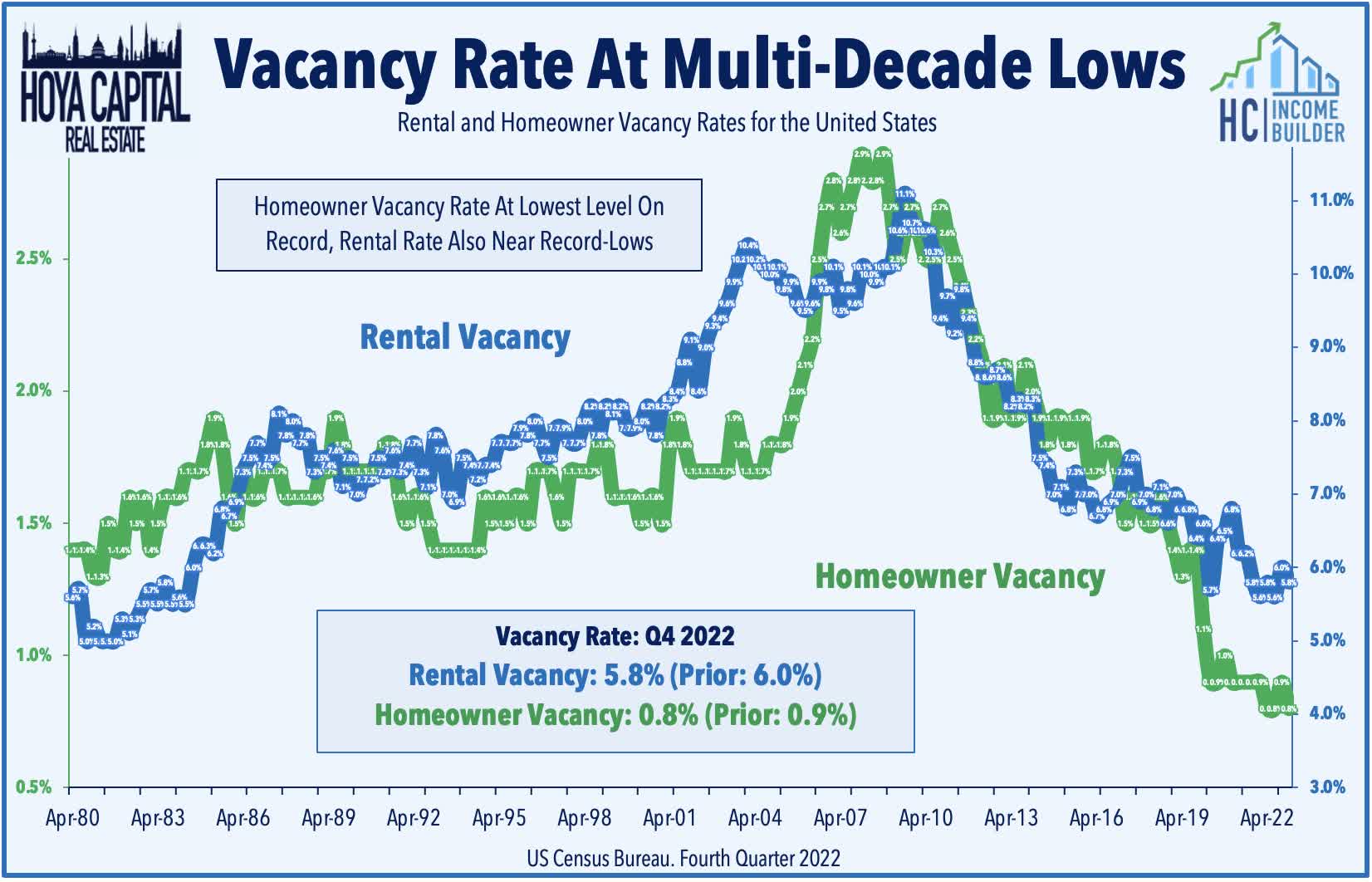

- Following two years of historic rent growth, there is little doubt that growth will moderate over the coming quarters. Market consensus sees a "hard landing" with rising vacancies and declining rents.

- Apartment REIT earnings results and guidance have pushed back on the dire narrative. REITs forecast NOI growth of 7% and FFO growth of 4% in 2023 - among the highest in the REIT industry.

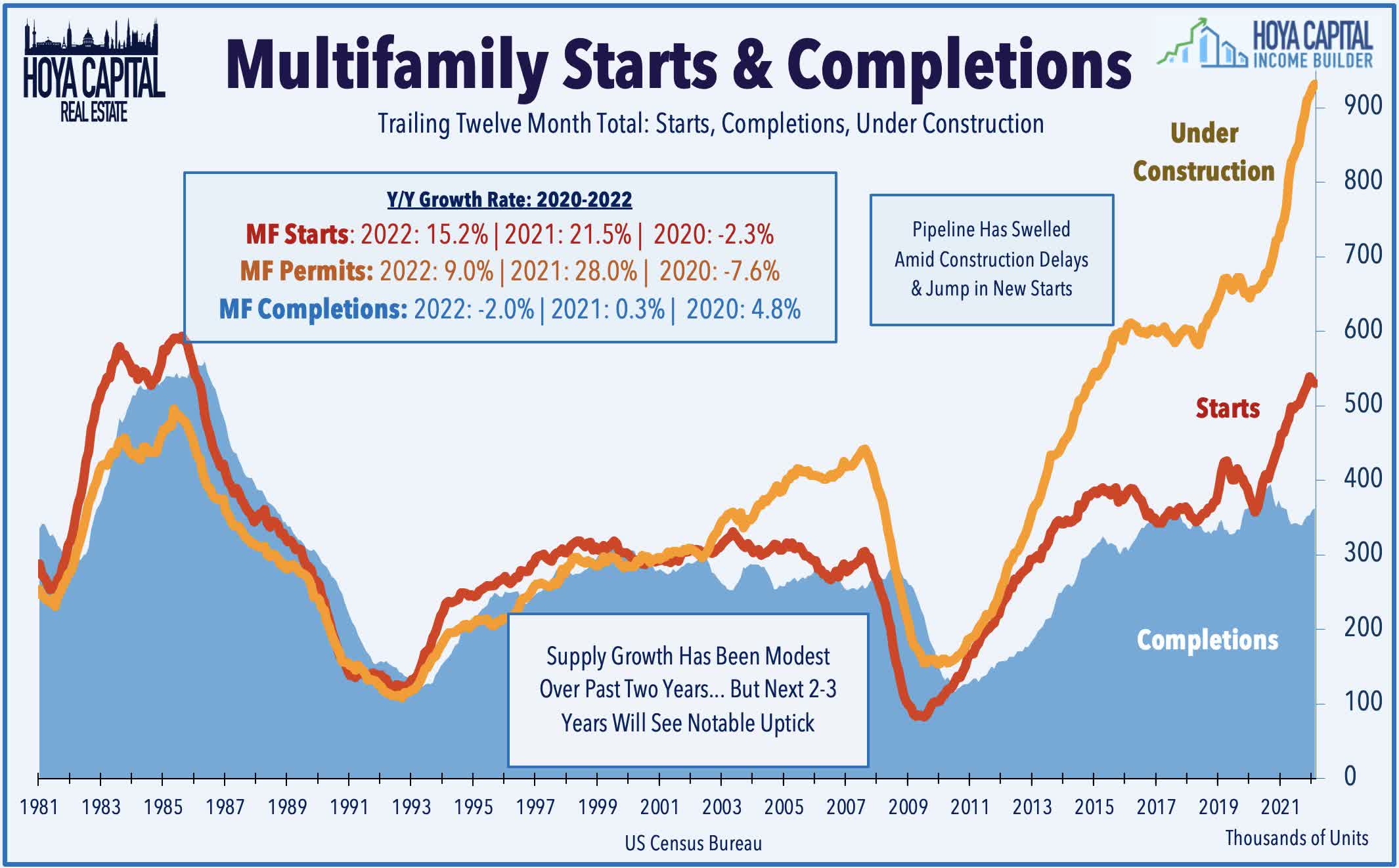

- Supply concerns are the root of the market pessimism as soaring rents sparked a wave of new development that will come to market over the next 18 months. Elongated development timelines make some often-cited pipeline metrics look scarier than reality.

- Our Sunbelt skew worked exceptionally well throughout the pandemic as Sunbelt REITs delivered cumulative FFO that more than doubled their Coastal peers. Supply headwinds require an even more discerning approach, and we prefer secondary and suburban markets and REITs focused on value-add over ground-up development.

REIT Rankings: Apartments

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on February 21st.

{kind=link}

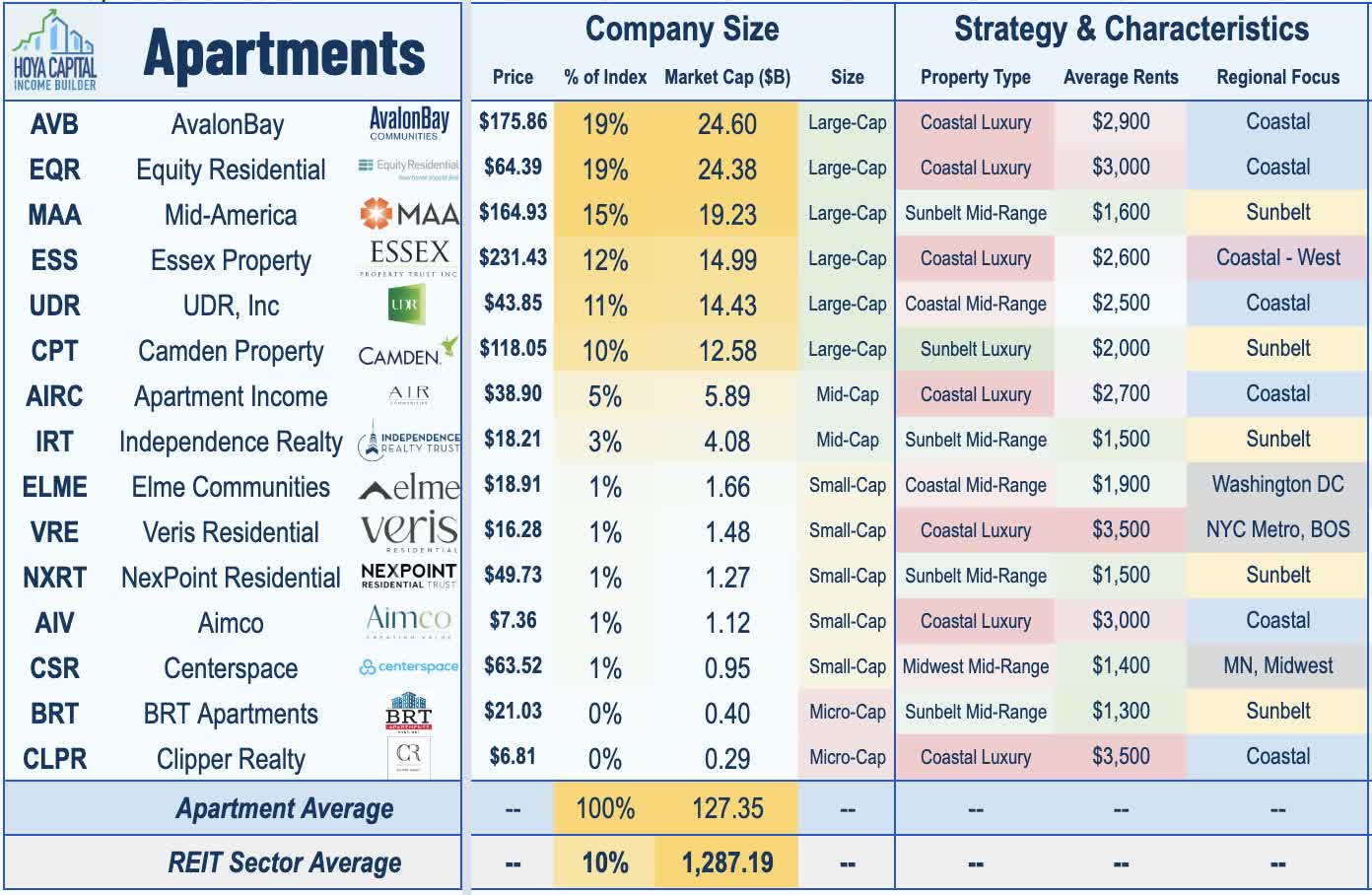

Within the Hoya Capital Apartment REIT Index , we track the fifteen largest apartment REITs, which collectively account for roughly $130B in market value and own over a million rental units across the United States. Apartment REITs were the second-worst-performing property sector in 2022 - barely outperforming the troubled office sector - despite delivering a record year of operating performance underscored by 20% growth in Funds From Operations ("FFO") driven by rent growth of a similar record-setting magnitude. Supply concerns driven by a wave of new development - along with lingering recession worries - are at the root of the market pessimism, with valuations reflecting expectations of a "hard landing" across rental markets with rising vacancy rates and a sustained period of negative rent growth.

{kind=link}

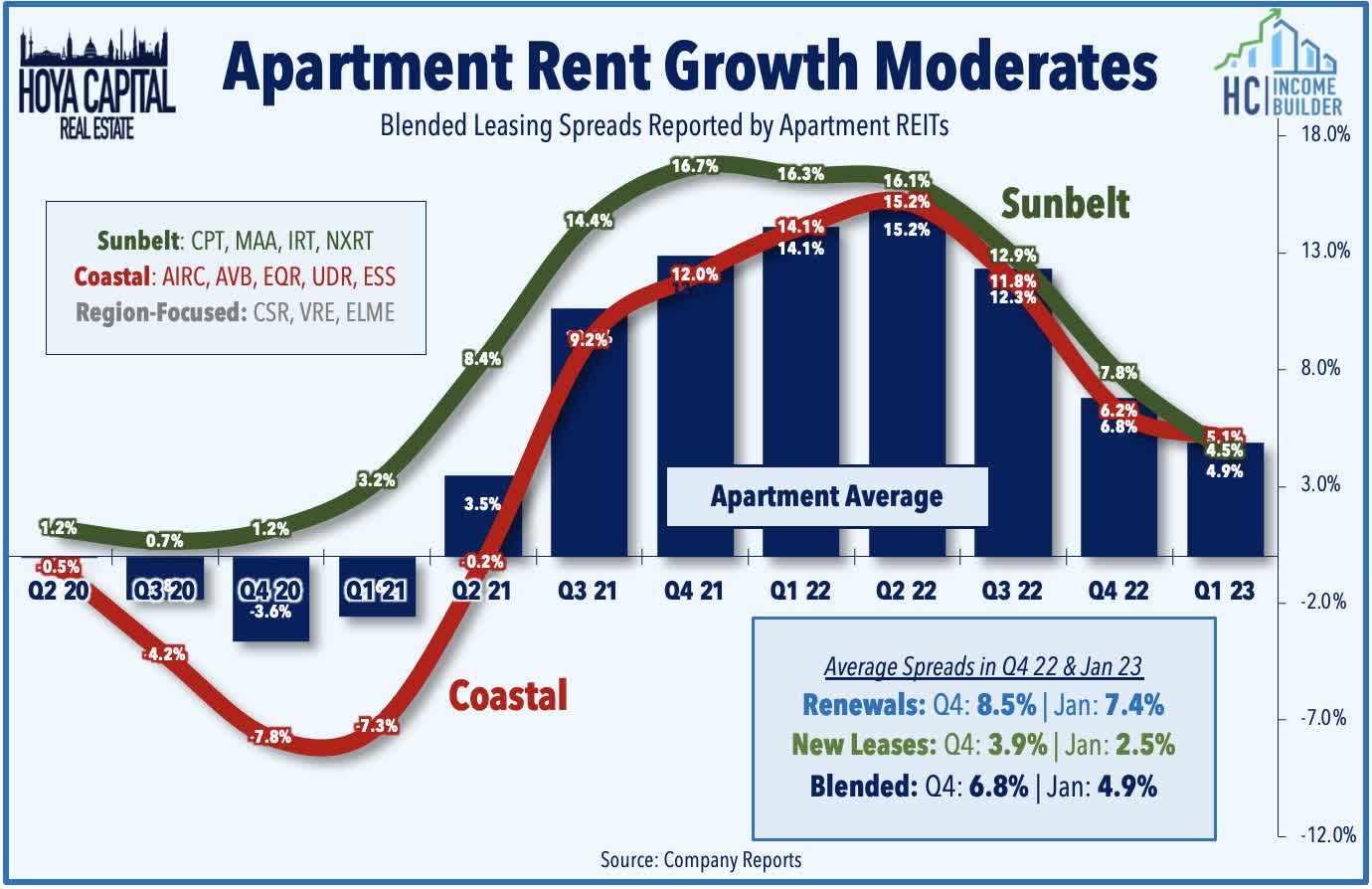

Relief may be in sight for renters across the nation that, for several years, were receiving an unwelcome surprise at the end of their lease term with double-digit percentage increases on their renewal offer and even higher effective rent increases on new lease offers. Consistent with a broader cooling of inflationary pressures, the historic pace of rent growth has moderated significantly since peaking at around 20% nationally in late 2021, but recent apartment REIT earnings results and forward guidance have pushed back on the dire narrative depicting a " crash " in rental markets. While rent growth on new leases cooled to below 5% in January, renewal spreads remained firm at above 7% in Q4 and into January. Buoyed by these firm renewal spreads, Apartment REITs expect average same-store NOI growth of nearly 7% and FFO growth of roughly 4% in 2023 - among the highest in the REIT industry.

{kind=link}

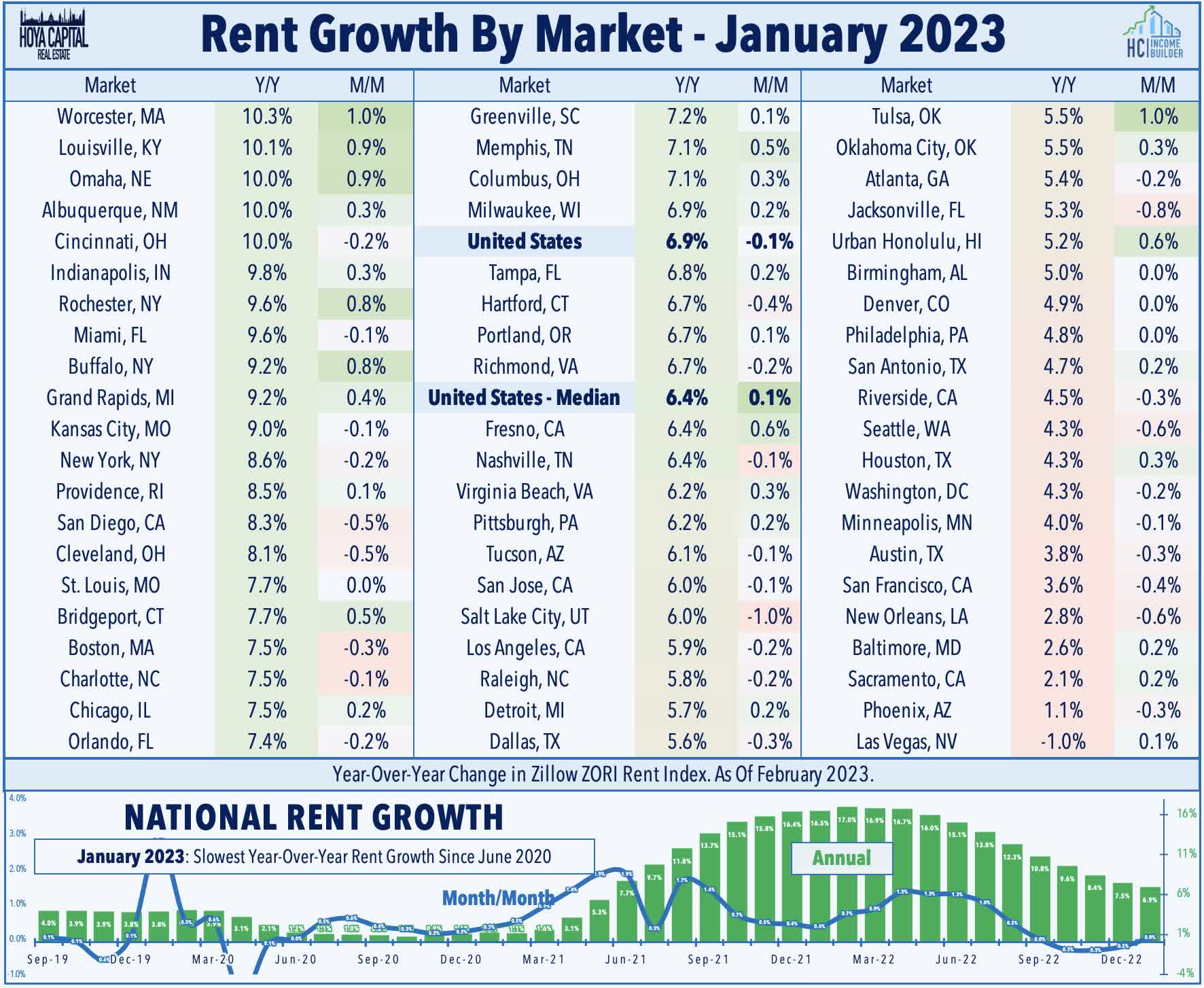

While valuations suggest that public market investors have bought into the "hard landing" narrative, recent data and forecasts from the leading multifamily data providers point towards the "soft landing" scenario of a steady normalization in rent growth and an uptick in vacancy rates back towards historical averages, but not the outright steep declines in rental rates that are currently being seen in prices of other pandemic-affected commodities and goods. Notably, the latest data from Zillow ( Z ) shows that annual rent growth for the median U.S. market cooled to 6.4% in January - down from the 15% increases in early 2022 - but recorded a sequential month-over-month increase for the first time since August. Consistent with apartment REIT reports, recent market-level performance has departed from the Sunbelt-outperformance themes that were on display early in the pandemic. Northeast markets have shown notable resilience in recent months, while several Sunbelt markets, including Las Vegas, Phoenix, and Austin have lagged.

{kind=link}

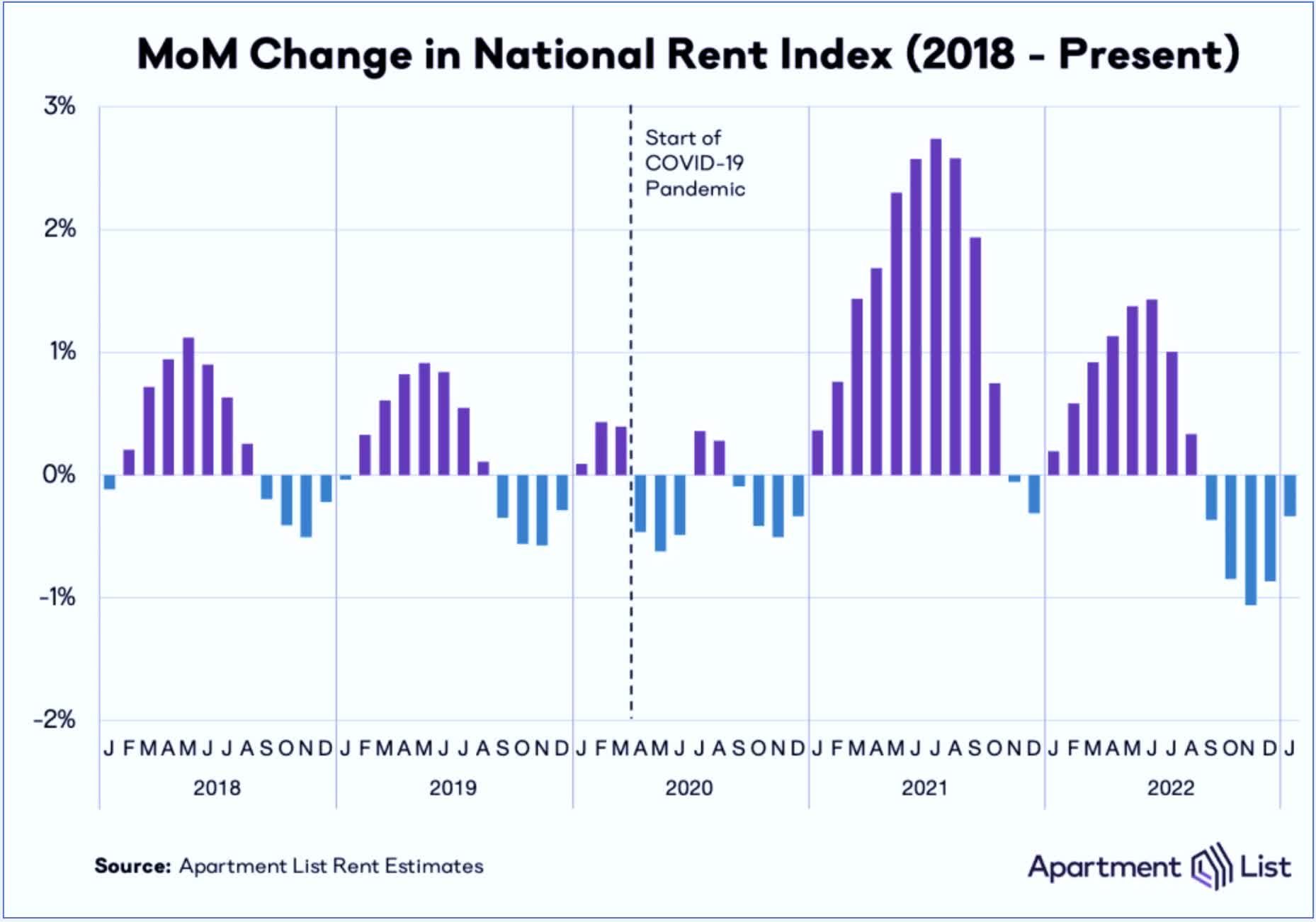

Apartment List data shows similar trends in its National Rent Report, noting that while the year-over-year rent growth cooled to 3.3% in February, the pace of cooldown has stabilized since late 2022 and the firm sees a "return to a level of rent growth that was the norm before the pandemic." Its report also highlighted recent strength in Midwestern markets, commenting that "markets in the Midwest may now represent some of the last bastions of affordability." The report noted that California remains a persistent soft spot, however, highlighting that San Francisco and San Jose are the only two large metros where the median rent is currently cheaper than it was at the pandemic's onset. Elsewhere, Yardi's 2023 forecast calls for 3.1% rent growth this year while Real Page Analytics sees rent growth at 2.9% for 2023 - "effectively matching the pre-pandemic norm."

{kind=link}

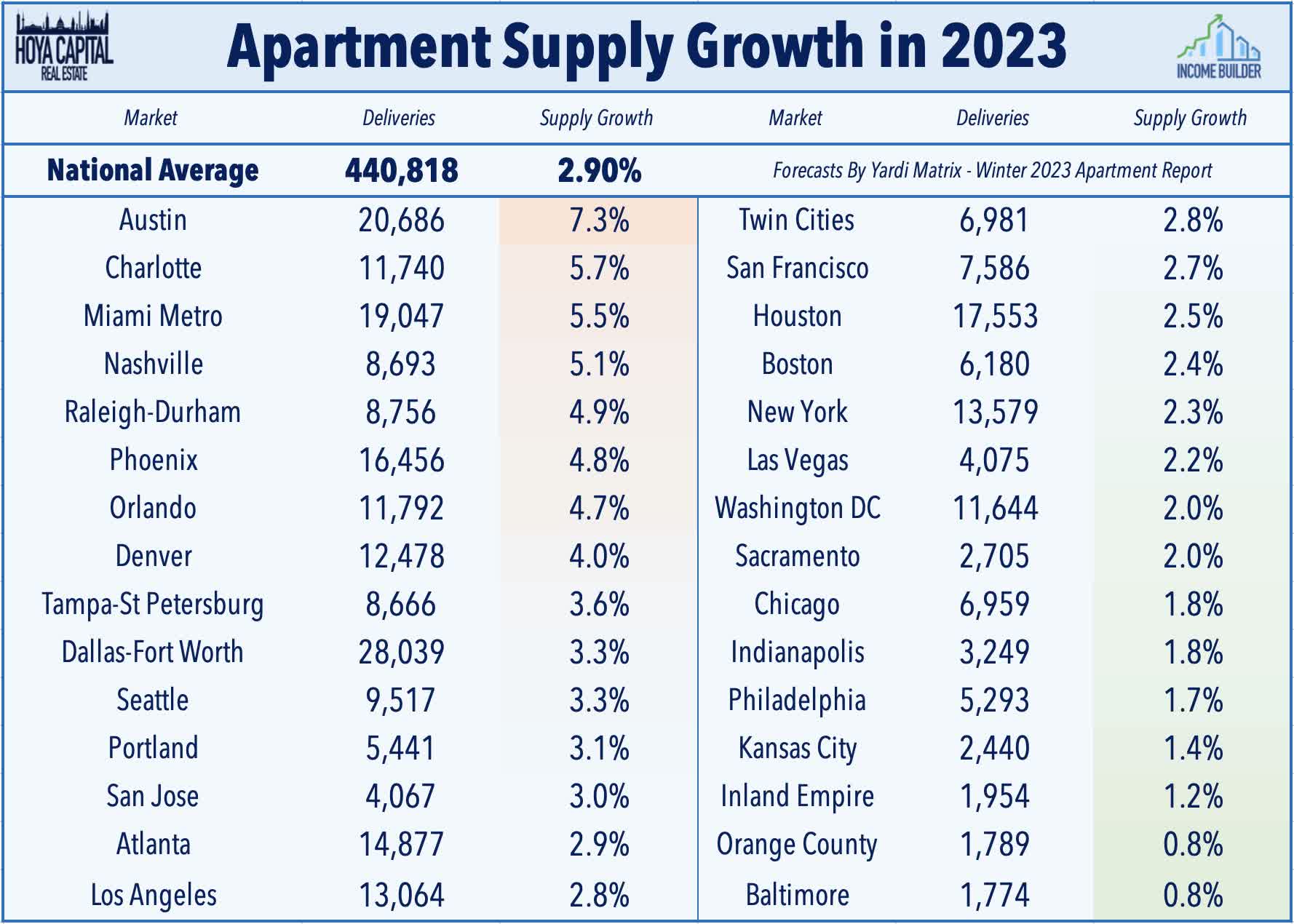

Supply concerns are the root of the market pessimism as soaring rents sparked a wave of new development that will come to market over the next 18 months, but we believe the often-cited metrics look more menacing than reality. After several years of muted supply growth, multifamily starts jumped 20% in 2021 and another 15% in 2022. Driven largely by the effects of the elongated development timelines resulting from supply chain disruptions and labor constraints, the pipeline of under-construction units has swelled to nearly 1 million units in early 2023, up considerably from the roughly 450k highs during the prior two development peaks in 1985 and 2007. Yardi expects 440k units to be delivered in 2023 - up from the 325k in 2022 - representing a 2.9% increase in stock which roughly matches levels seen in 2018 and 2019.

{kind=link}

While the overall level of supply growth appears manageable, Yardi predicts supply growth will top 5% across a handful of markets - primarily in the Sunbelt region - including Austin, Charlotte, Phoenix, Miami, and Nashville - markets that have generally seen the strongest population growth and cumulative rent growth over the past three years. Yardi projects that deliveries will begin to wane by mid-2024, however, due to lingering or worsening impediments to new development, including the difficulty of getting construction financing, ongoing delays in labor, and challenges in getting entitlements from local planning and zoning boards.

{kind=link}

These pockets of oversupply will result in an increased level of market-by-market bifurcations that will require an even more discerning approach compared to the simple "Sunbelt skew" that worked so effectively throughout the pandemic. We see the best opportunities in REITs focused on secondary and suburban markets which are seeing more limited supply growth. We also prefer REITs that focus their external growth on value-add improvements over ground-up development - a strategy that comes with less risk and lower overhead.

{kind=link}

Macro Fundamentals: Housing Shortage Evident

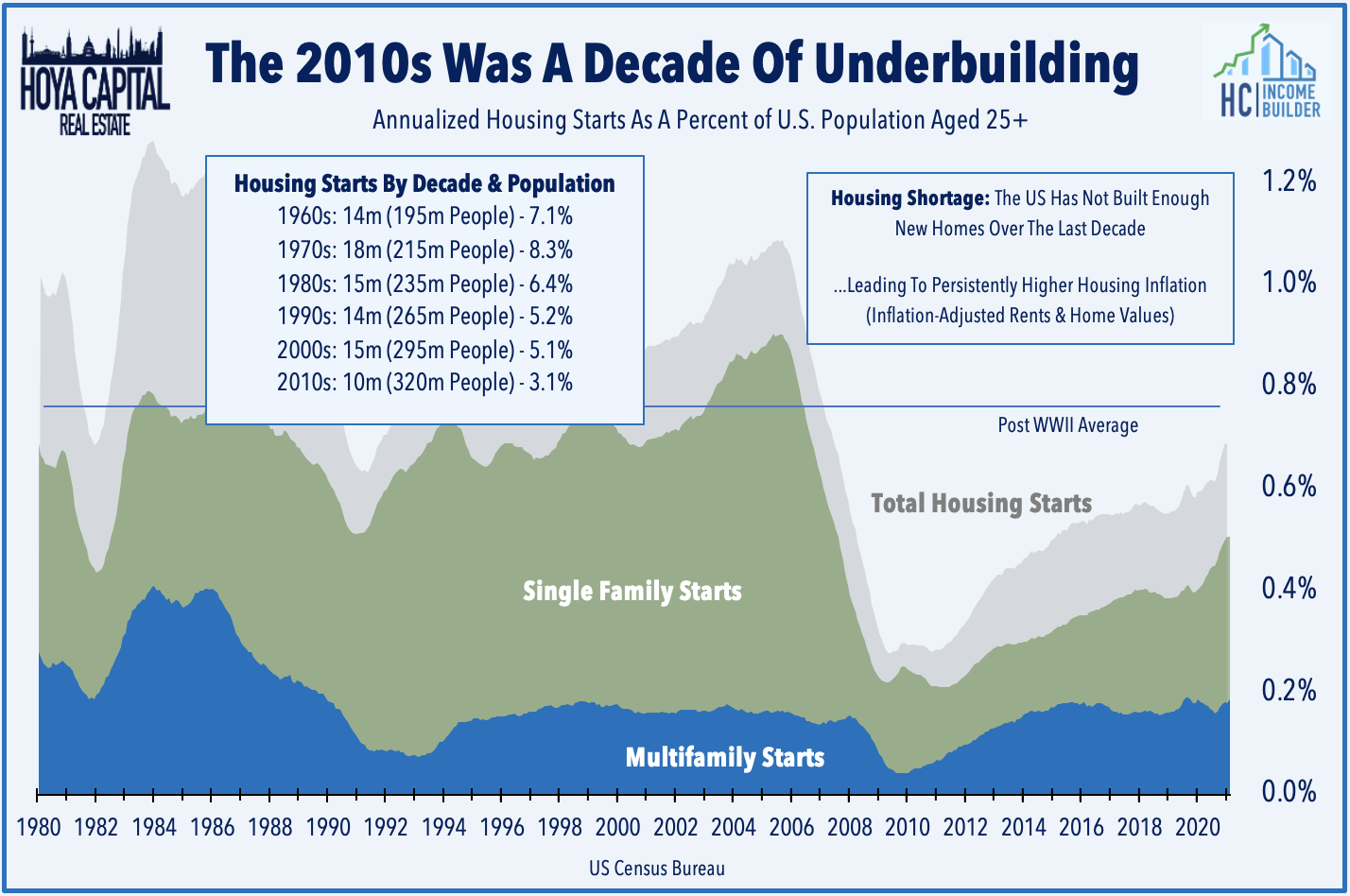

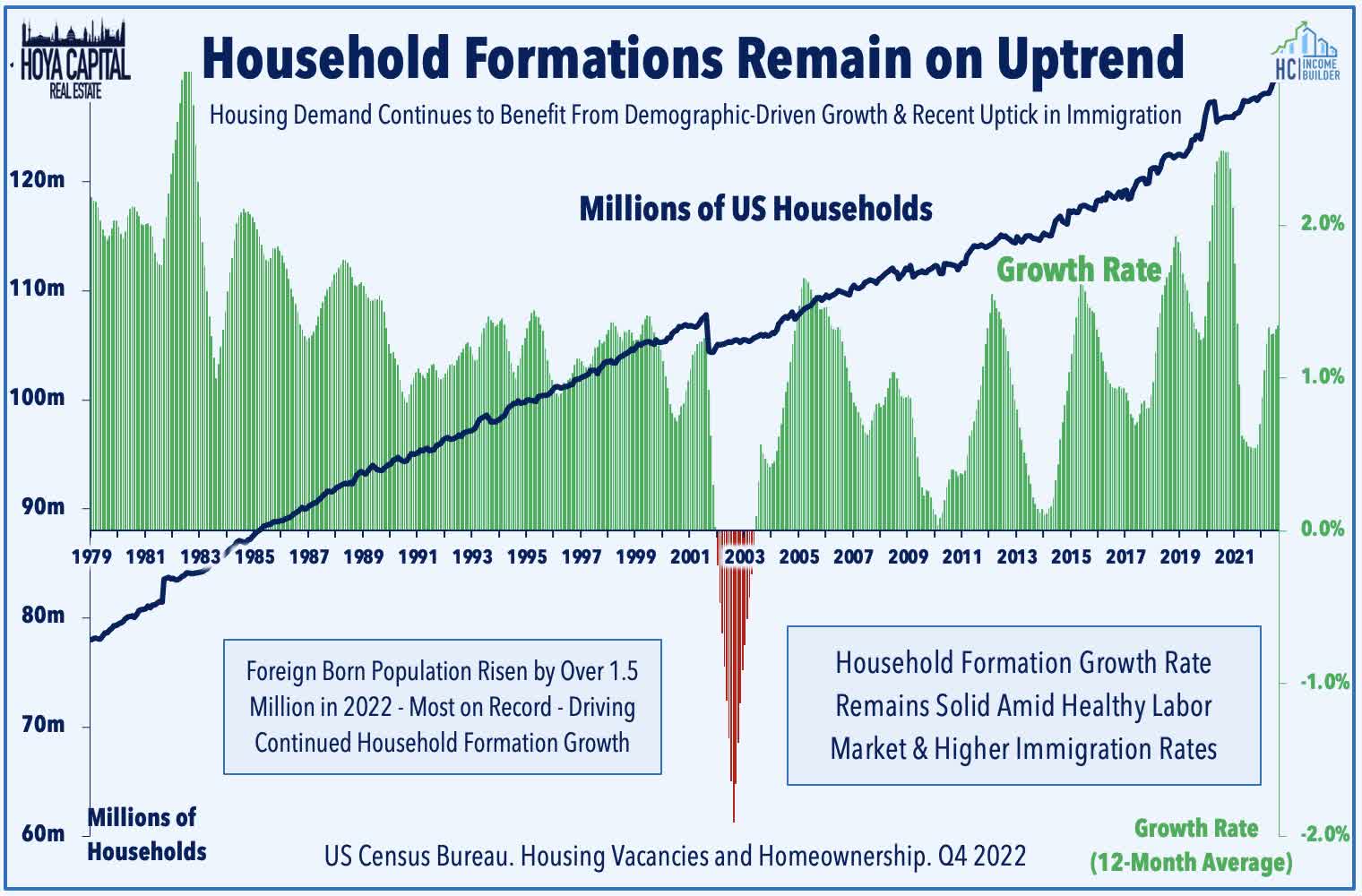

It's also important to recognize that the uptick in multifamily supply growth comes alongside a corresponding decline in single-family development amid a rate-driven housing slump that has driven the rate of Existing Home Sales to the lowest levels since 2010 and the rate of single-family housing starts to the lowest levels in nearly a decade. Elevated rent growth and stretched affordability metrics are perhaps the most obvious indication of a lingering undersupply of housing units, and Freddie Mac estimates that the U.S. housing market is still more than 3 million housing units short of what's needed to meet the country's demand.

{kind=link}

As we've discussed at length over the past decade, demographics suggested the 2020s were already poised to see historic levels of housing demand as the millennial generation - the largest cohort in American history - came full-steam into a severely undersupplied U.S. housing market. What we could not foresee, however, was the added acceleration provided by the pandemic-driven "Work From Home era" which has begun to unleash millions of extra "deferred" formations among adult children, in particular. Meanwhile, net international migration added more than a million people to the U.S. population between July 1, 2021 and July 1, 2022 - a 168.8% increase from the prior year - marking the largest single-year increase since 2010.

{kind=link}

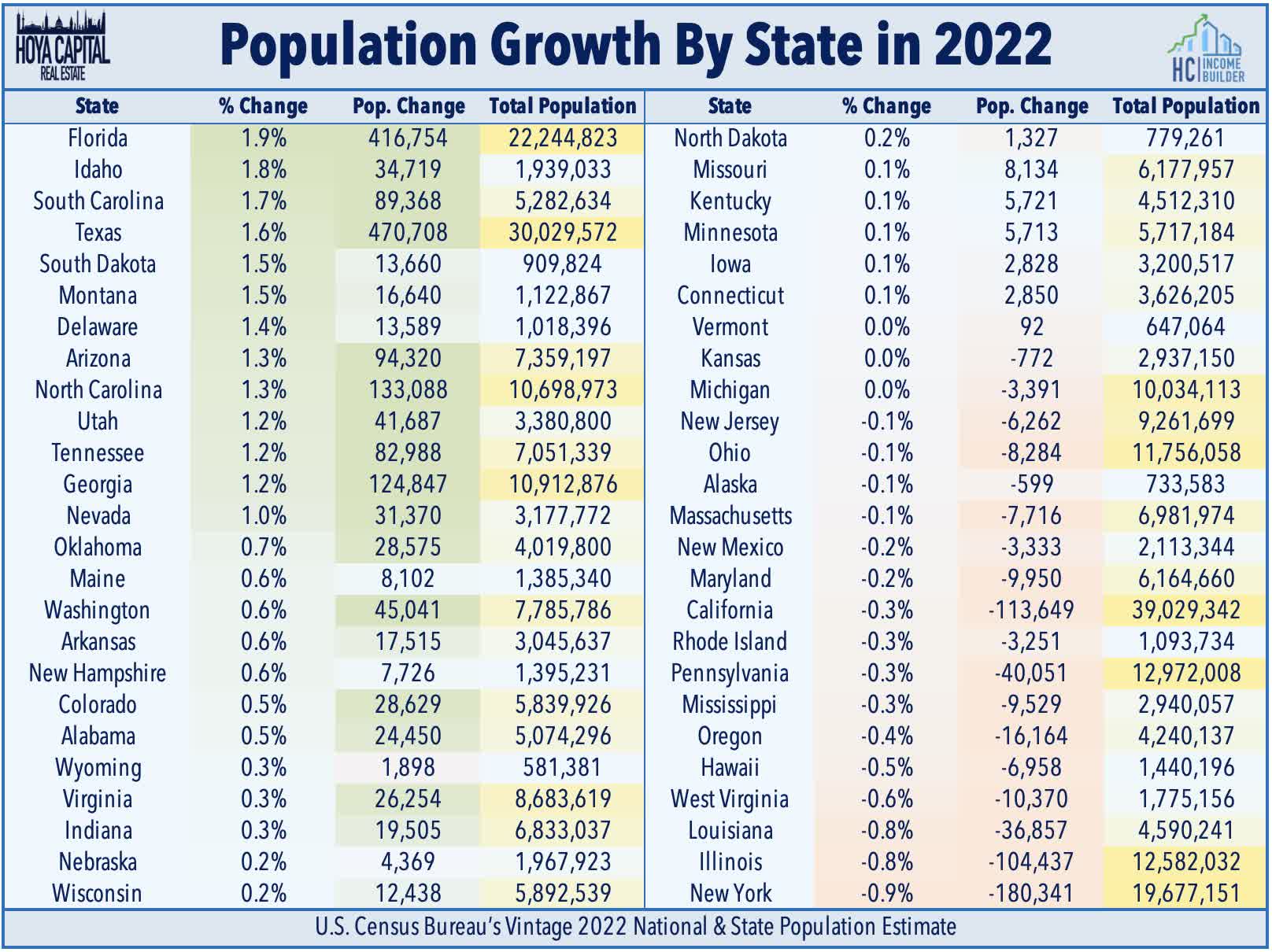

Diving deeper into the newly-released Census data, we observe that Florida was the fastest-growing state in 2022 on a percentage basis with an annual population increase of 1.9% while Texas earned the top spot on an absolute basis with the addition of nearly a half-million new residents. New York saw the highest outflows on both a percentage basis and an absolute basis, losing nearly 1% of its total population this past year. California and Illinois also recorded six-figure decreases in the resident population. At the regional level, the South was the fastest-growing and the largest-gaining region last year, increasing by 1.1% while the West region recorded an annual increase of 0.2%. The Northeast and the Midwest regions, however, recorded population declines of -0.4% and -0.1% residents, respectively.

{kind=link}

Apartment REIT Fundamentals

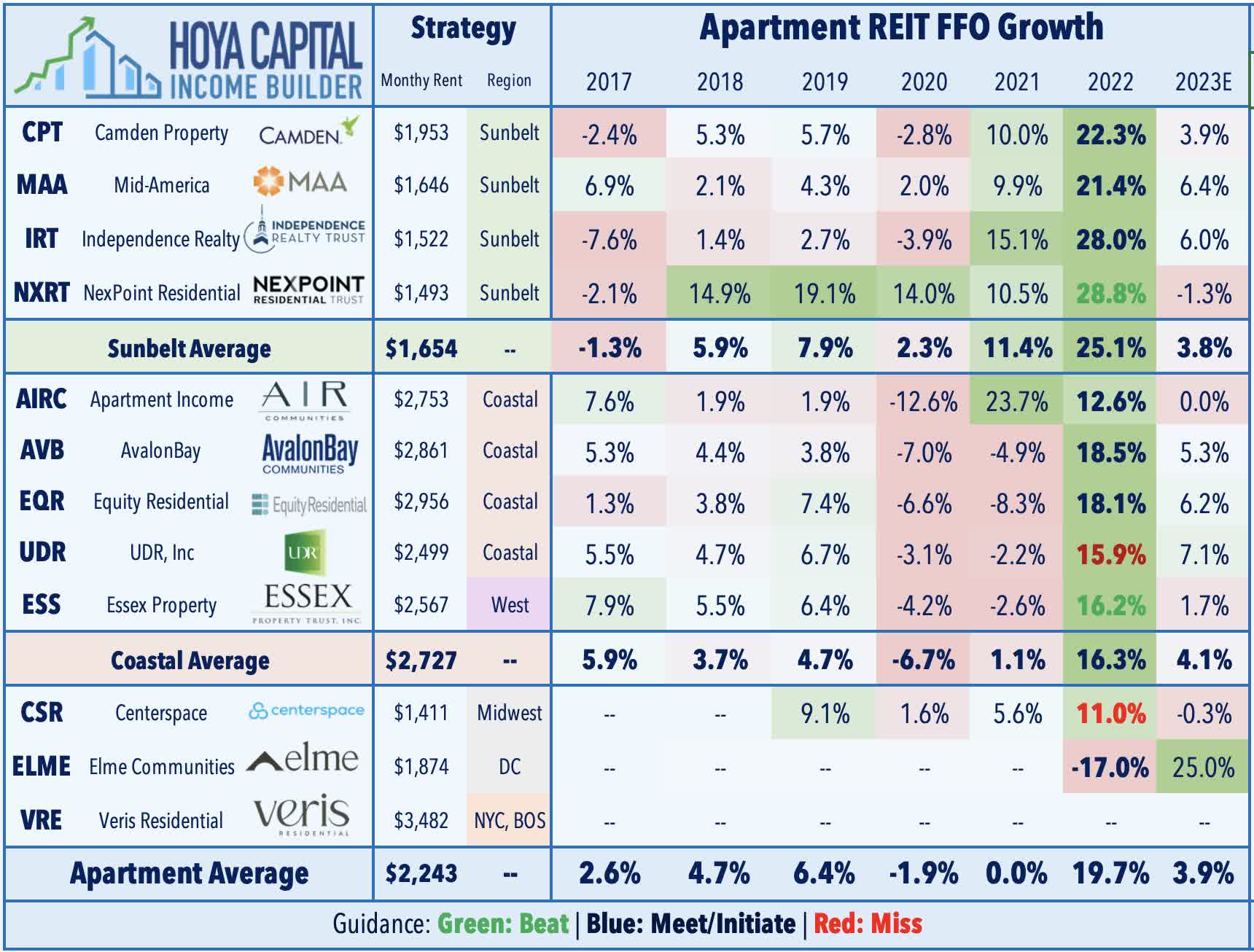

As discussed in our REIT Earnings Halftime Report , apartment REITs were an upside standout in fourth-quarter earnings season with a solid slate of reports that pushed back on the "hard landing" narrative. Apartment REITs delivered average FFO growth of 19.7% for full-year 2022 - the strongest year ever for the sector and the second-highest earnings growth rate across the real estate industry behind the roughly 23% growth from the storage REIT sector. As expected, the outlook for 2023 calls for more muted growth with average FFO growth of 3.9% which, if achieved, would likely trail only the industrial and manufactured housing sectors for the strongest in across the REIT industry. Of the eleven REITs that provide guidance, nine REITs delivered results that either matched or exceeded their prior outlook.

{kind=link}

Sunbelt-focused NexPoint Residential ( NXRT ) reported the strongest FFO growth at 28.8% in 2022 followed close behind by Independence Realty ( IRT ) at 28.0%. If these full-year outlook targets are met, apartment REITs will have delivered average cumulative FFO growth of 27.7% since the start of the pandemic. Sunbelt REITs never skipped a beat during the pandemic and now expect 2023 FFO levels to be 47.7% above their pre-pandemic rate from 2019 while Coastal REITs now expect 2023 FFO levels to be 13.5% above 2019-levels. The once-wide performance spread between Sunbelt and Coastal-focused REITs has even-out in recent quarters, however, and the edge for 2023 appears to lean slightly toward the Coastal REITs. Notably, occupancy rate declines and the uptick in turnover rates were far more muted among Coastal REITs, symptomatic of the recent uptick in supply growth in the Sunbelt markets beginning in late 2022. Lower turnover rates in Coastal markets - which remained near all-time lows at around 40% in Q4 versus 50% among Sunbelt REITs - explain much of the delta in expense growth.

{kind=link}

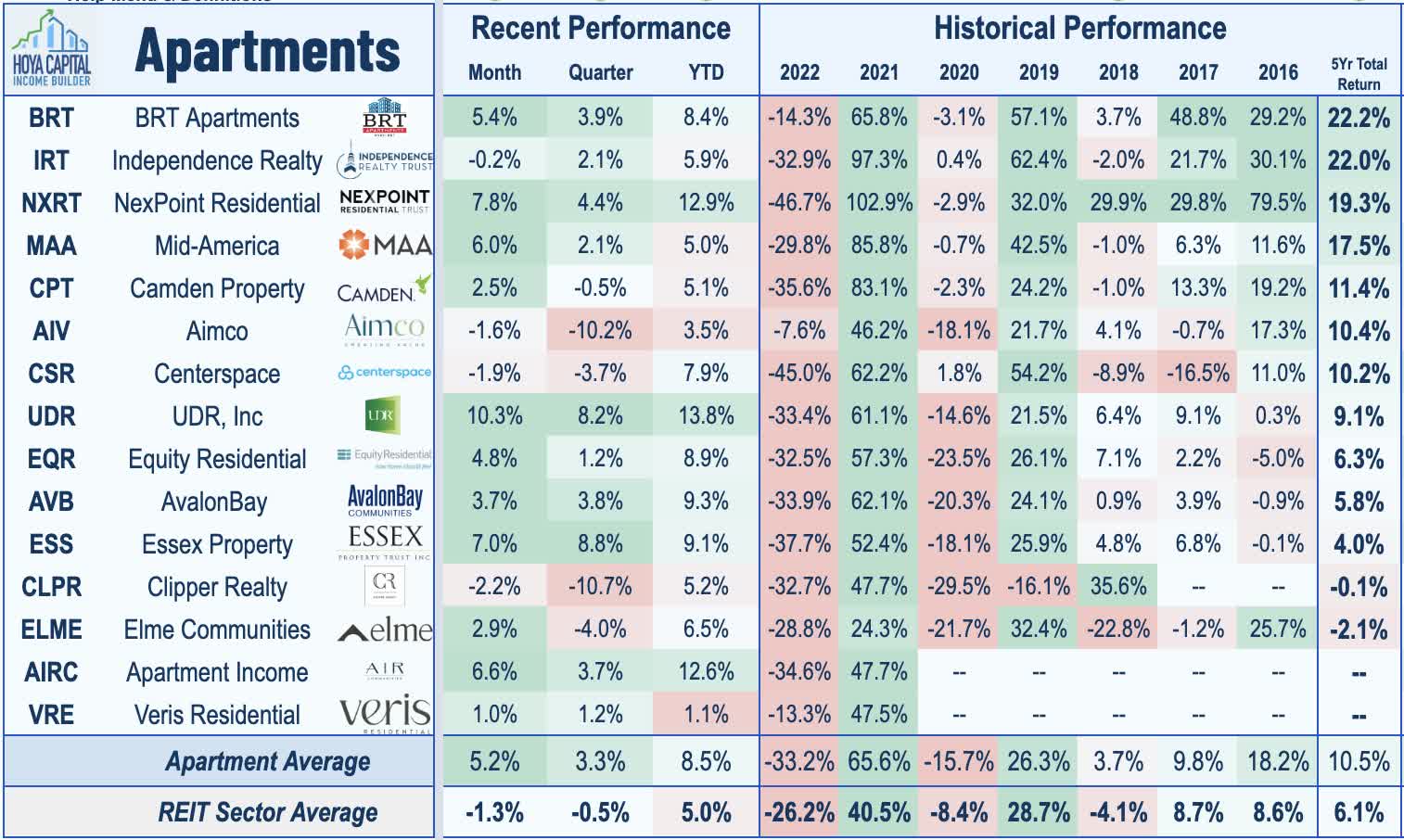

The strength of renewal rent growth was perhaps the most significant takeaway from these results. While new lease rates have seen a rather sharp sequential slowdown since peaking in Q2 at 17.5% and slowing to 3.0% by January, renewal rates held relatively steady in the high-single-digits over the past two quarters, averaging nearly 9% in Q4 and nearly 8% in January. Among the coastal-focused REITs, Apartment Income ( AIRC ) reported the strongest rent growth metrics with 11.1% blended spreads during these periods, while NYC-focused Veris Residential ( VRE ) also reported similarly impressive results with blended spreads of over 11% across both periods. Also of note, two REITs - Essex Property ( ESS ) and Mid-America ( MAA ) - did record a negative growth rate in new leases in January.

{kind=link}

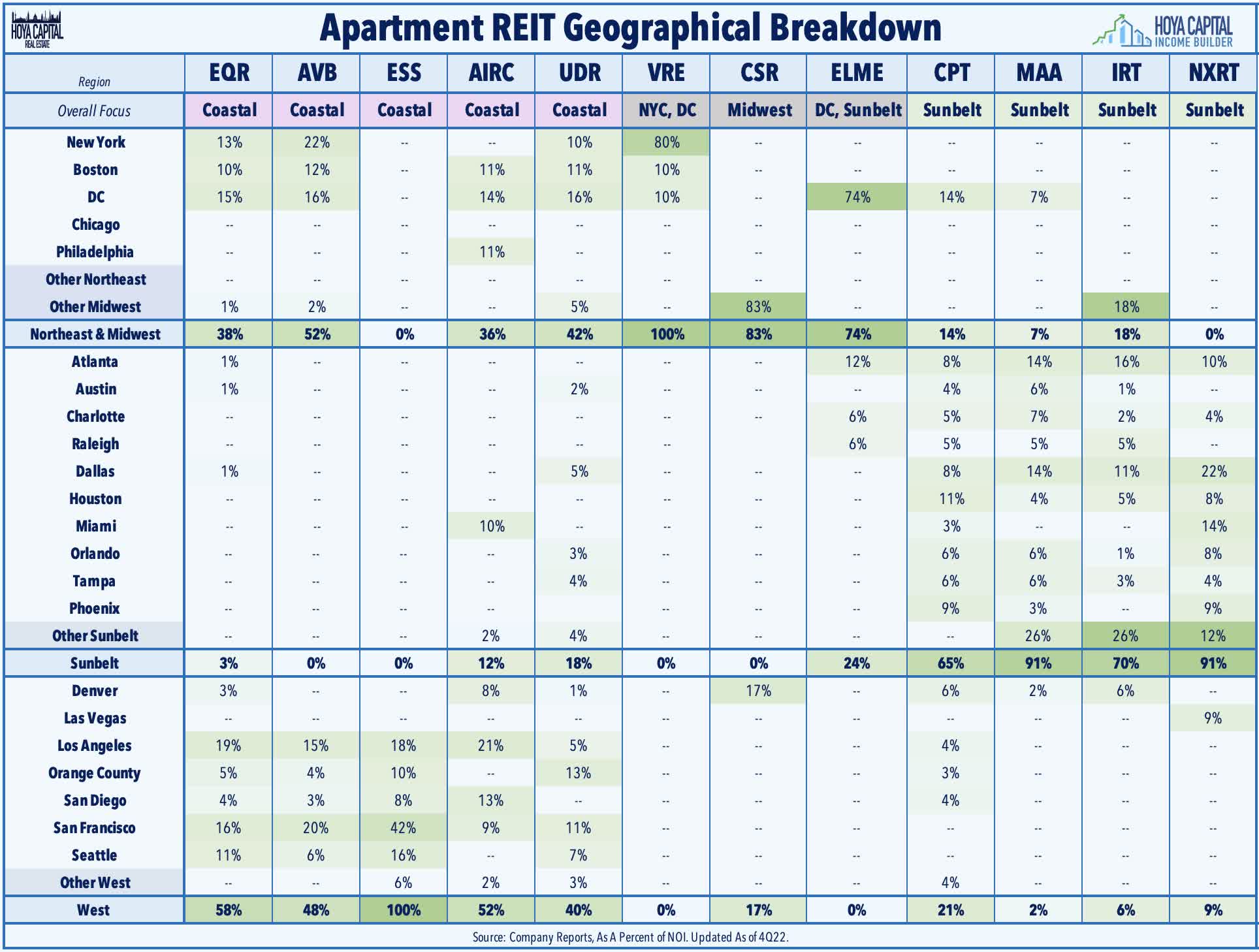

Deeper Dive: Apartment REIT Portfolios

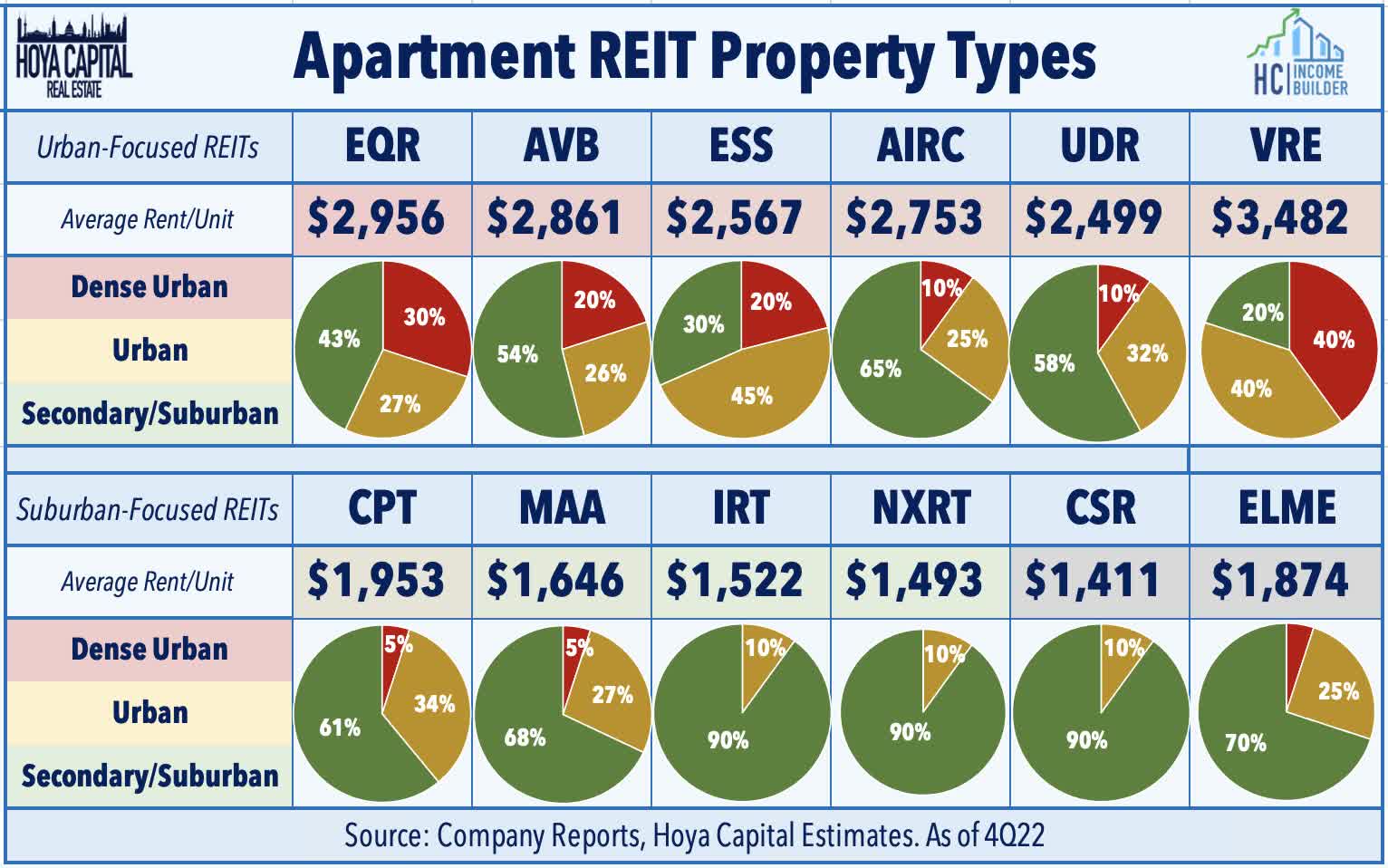

As a sector, apartment REITs collectively have fairly balanced geographical exposure across most of the major U.S. markets. Individual apartment REITs tend to focus on either coastal markets or sunbelt and secondary markets and own portfolios that typically include a blend of luxury high-rise, mid-rise, and garden-style apartment communities. Several of the newer apartment REITs are more geographically concentrated, including Veris Residential ( VRE ) - formerly known as Mack Cali - which derives around 80% of its revenues from the New York City metro region, and Elme Communities ( ELME ) - formerly known as Washington REIT - which is primarily based in Washington, DC.

{kind=link}

Speaking of Veris , the firm has been the center of some M&A drama over the past several quarters after a proposed takeover bid from Kushner Companies in October for $16.00/share, which was subsequently raised in December to $18.50/share. Veris' Board rejected the offers, commenting that the figure "grossly undervalues the company in its current form and denies shareholders the substantial value expected to be unlocked from the company's strategic transformation," and there have been few indications that the two have come any closer to a deal in recent months. The proposed deal was the first major M&A development in the space since Blackstone's ( BX ) frenzy of activity in early 2022, in which the private equity giant picked off a trio of multifamily REITs - Bluerock Growth REIT, Preferred Apartments, and American Campus - for its nontraded REIT platform known as BREIT. A wave of investor redemptions from BREIT in recent months has raised our longstanding expectation that these portfolios eventually come back to the public markets either as independent entities or through the acquisition by an existing REIT.

{kind=link}

The larger apartment REITs are generally some of the most well-capitalized companies across the REIT sector - a critical attribute during the pandemic-related turbulence - but several of the small-cap apartment REITs do operate with elevated debt levels with more exposure to variable-rate debt. Among those is NexPoint Residential , but we've been pleased with NXRT's recent progress in reducing their variable rate exposure through asset sales, refinancings, and the use of interest rate locks. The seven largest apartment REITs command investment-grade credit ratings from Standard & Poor's, led by A- ratings by AvalonBay , Equity Residential , and Camden . The larger REITs in the sector also tend to rank high on the corporate governance scale with shareholder-friendly governance structures.

{kind=link}

Apartment REIT Stock Performance

Apartment REITs were the second-worst-performing property sector in 2022 - barely outperforming the troubled office sector - despite delivering a record year of operating performance underscored by 20% FFO growth amid concern over elevated supply growth and a broader economic slowdown. The Hoya Capital Apartment REIT Index declined by 32% in 2022, lagging the 25% decline from the broad-based Vanguard Real Estate ETF ( VNQ ) and the 18% decline from the S&P 500 ETF ( SPY ). Lifted by the strong slate of earnings reports, however, apartment REITs are off to a better start in 2023 with returns of 8.5% this year compared to the 5% gain on the broader REIT index.

{kind=link}

Apartment REITs have been some of the strongest-performing REITs over most long-term measurement periods. From 2010 through 2022, Apartment REITs delivered average annual returns of 15.0%, outpacing the 10.4% annual total returns from the broad-based REIT average during that time. Among the major apartment REITs, the four Sunbelt-focused REITs - Independence , NexPoint Residential , Mid-America , and Camden Property - have delivered the strongest 5-year total returns. Three REITs are higher by double-digit percentages on the year, led by UDR , NexPoint Residential , and Apartment Income .

{kind=link}

Apartment REIT Dividend Yields

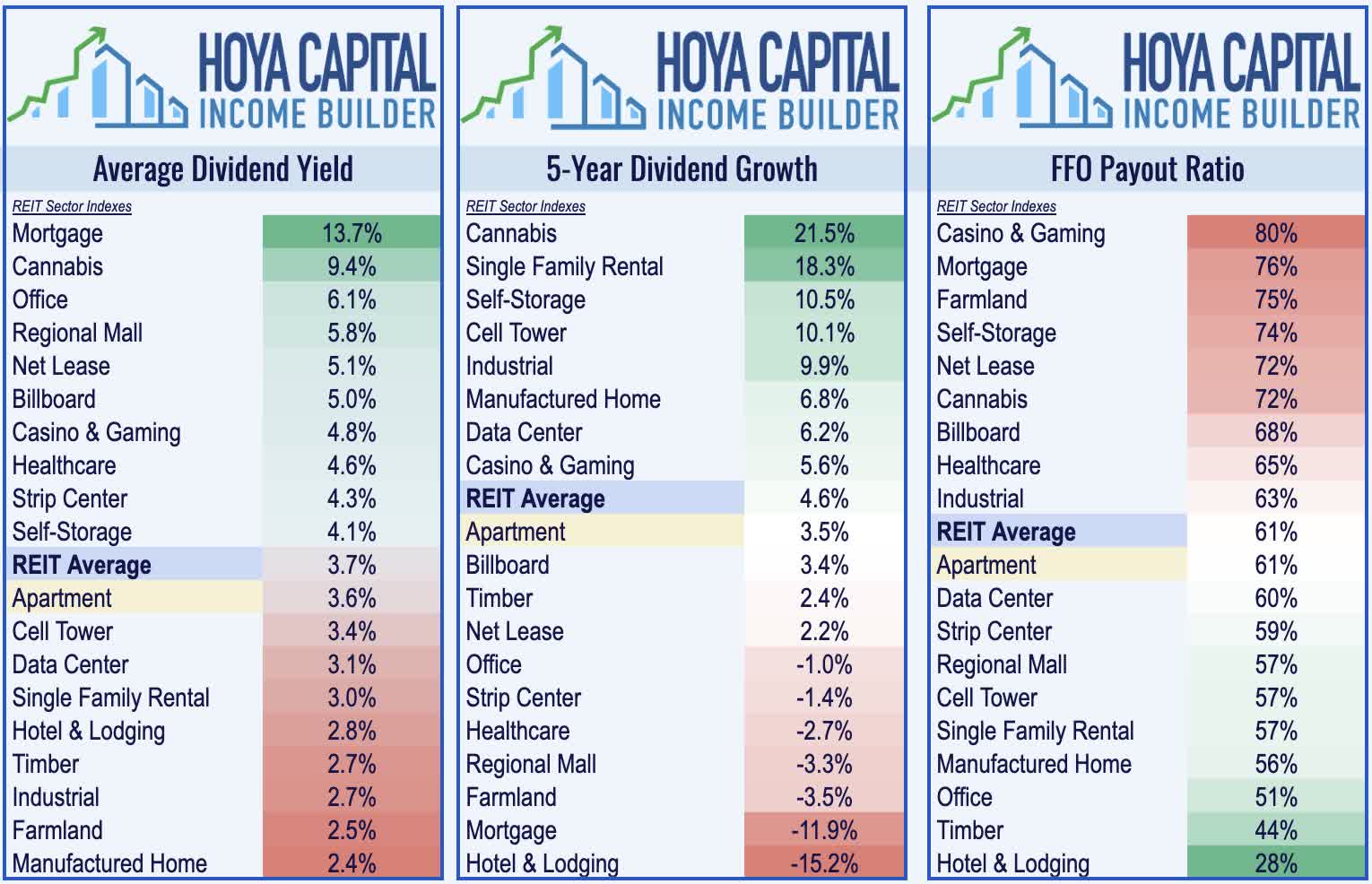

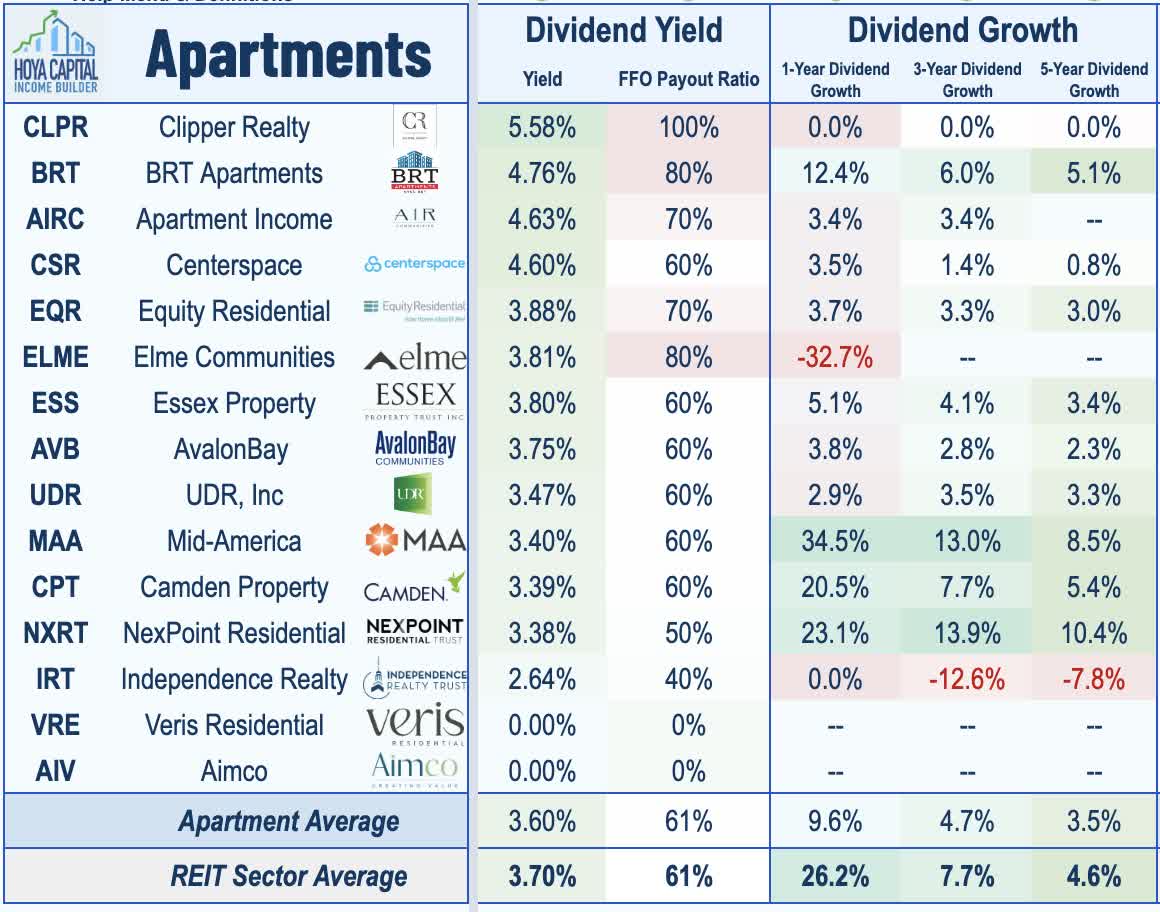

Apartment REITs pay an average dividend yield of 3.7%, which is slightly below the REIT market-cap-weighted sector average of 3.6%. Since the start of 2015, apartment REITs have delivered average annual dividend growth of roughly 4%, but pay out only around 60% of their available cash flow, giving these companies the flexibility to take advantage of external growth opportunities or to increase future distributions.

{kind=link}

Five apartment REITs raised their dividends so far in 2022 including a pair of 10% dividend hikes from NexPoint Residential ( NXRT ) and UDR ( UDR ), a pair of 6% raises from Camden ( CPT ) and Elme Communities ( ELME ), and a 4% dividend hike from AvalonBay ( AVB ). Near-perfect rent collection throughout the pandemic allowed apartment REITs to not only avoid the wave of dividend cuts that swept through the REIT sector during the early stages of the pandemic but also to be among few REITs to raise their distributions in during the depths of the pandemic in 2020 - a trend of dividend raises that continued in 2021 and 2022. Small-cap Clipper ( CLPR ) tops the charts with a dividend yield of 5.58% followed by BRT Apartments ( BRT ) at 4.76% and Apartment Income ( AIRC ) at 4.63%.

{kind=link}

Takeaway: Tracking Towards Soft Landing

Renting or owning - housing has become significantly more expensive over the past three years as pre-existing secular tailwinds related to the lingering housing shortage were given an added pandemic-related accelerant. The historic surge in mortgage rates since early last year has poured icy-cold water over the once-red-hot housing market since it fell into the cross-hairs of an aggressive Federal Reserve, however, fueling a sell-off across housing-related industry groups over the past quarter, including apartment REITs. Calls for a "hard landing" of sharply higher vacancies and declining rents appear misguided, however, and we see very good value across a handful of apartment REITs, notably those focused on secondary and suburban markets and REITs focused on value-add over ground-up development.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Apartment REITs: Tracking For Soft Landing