JELD - Apogee Enterprises: A Revision To Expectations

Summary

- Shares of Apogee Enterprises have declined at a time when fundamentals remain robust.

- This trend is expected to continue through at least the end of its 2023 fiscal year, creating some clarity for investors moving forward.

- Given how shares are priced, the firm's stock now seems to offer some nice potential moving forward.

Architecture is incredibly important for a variety of reasons. It's vital in determining the use of a particular property. The way in which it's structured can convey certain feelings or messages to those visiting or working in said property. In short, architecture helps to define who we are, what we do, and how well we do it. One company that operates in this market is Apogee Enterprises ( NASDAQ: APOG ). Specifically, the company focuses on products such as windows, curtain walls, the coating and fabricating of high-performance glass, and more. From a purely fundamental perspective, this enterprise has been doing exceptionally well as of late. Management also expects that trend to continue for the foreseeable future. Even so, shares have taken a step back, driven by concerns about the broader economy. While I was once more neutral on the business, the changes I have seen have led me to revise my thinking and increase my rating on the enterprise from a ‘hold’ to a soft ‘buy’.

The picture has improved

Back in early April of this year, I wrote an article talking about the upcoming earnings release for the fourth quarter of Apogee Enterprises’ 2022 fiscal year. Since then, the company is not only reported data for that quarter, it has also reported data for the first quarter of its 2023 fiscal year. What has been made available so far, which includes guidance for the rest of the 2023 fiscal year, looks to be rather appealing. This marks a change compared to my prior sentiment on the company, when I said that the business was still in the recovery phase and that its historically rocky fundamental performance made the company more or less fairly valued. At that time, I had the company as a ‘hold’, reflecting my belief that it would likely generate returns that more or less match what the broader market would achieve. Since then, the company has lived up to this expectation, with shares generating a loss of about 11.3% compared to the 10.1% experienced by the S&P 500 over the same window of time.

{kind=link}

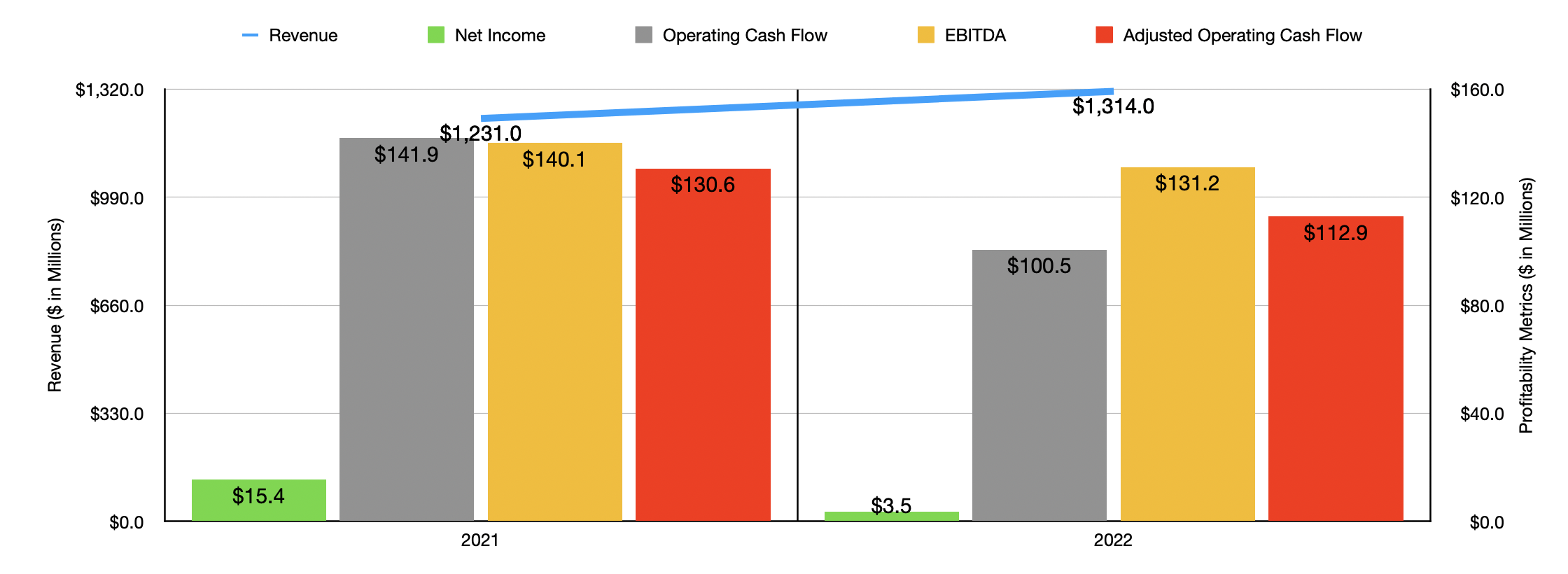

When it comes to digging into the numbers, we should first start with the 2022 fiscal year . During that year, sales for the company came in at $1.31 billion. That represents a decent improvement over the $1.23 billion in sales generated during the company's latest fiscal year. This 6.8% rise was driven by record revenue from the company’s LSO (Large-Scale Optical Technologies) and Architectural Services segment of the enterprise, as well as increased sales associated with its Architectural Framing Systems segment. Unfortunately, the company did see some of this sales increase offset by the Architectural Glass segment, which suffered from a decrease in volume year over year. Under the LSO segment, sales skyrocketed by 45.1% from $70.1 million to $101.7 million. This, management said, was driven by demand recovery following the COVID-19 pandemic, as well as by a favorable sales mix. The Architectural Services segment, meanwhile, experienced an 18.1% rise in revenue because of higher volume from executing projects that were already in its backlog.

When it comes to profitability, the picture was less than ideal. Net income of $3.5 million came in far lower than the $15.4 million in profitability the company generated in the 2021 fiscal year. Operating cash flow managed to drop from $141.9 million to $100.5 million. But if we were to adjust for changes in working capital, the decline would have been from $130.6 million to $112.9 million. Meanwhile, EBITDA for the company also suffered, dropping from $140.1 million to $131.2 million.

{kind=link}

Although the picture for the 2022 fiscal year proved to be rather mixed, the same cannot be said of the current fiscal year . For the first quarter of the year, the company generated revenue of $356.6 million. That's 9.4% higher than the $326 million in sales reported for the first quarter of 2022. A 19.4% increase in the Architectural Framing Systems segment, driven largely by inflation-related pricing actions, and a 13.9% rise in revenue associated with the Architectural Services segment associated with increased volume from executing projects currently in the company's backlog, were instrumental in this improvement.

L ike in the case of the 2022 fiscal year, however, the 2023 fiscal year is also proving to be beneficial from a profitability perspective. Net income for the first quarter of the year came in at $22.7 million. That's more than double the $10.8 million generated just one year earlier. This Was driven in large part by the company's gross profit rising from 20.8% of sales last year to 24% this year thanks to management's ability to push more than all of its inflation-related costs onto its customers. Other profitability metrics have followed suit. Although operating cash flow declined from $6.9 million to negative $30.5 million, the adjusted figure for this rose from $29.6 million to $40.5 million. Another metric that fared very well was EBITDA. This ultimately rose from $28.7 million in the first quarter of 2022 to $42.8 million the same time this year.

For the 2023 fiscal year as a whole, management has pretty high hopes for the company. Adjusted earnings per share are expected to come in between $3.50 and $3.90. At the midpoint, that would translate to adjusted net profits of $83.8 million. This compares to the $62.6 million in adjusted profits generated in the 2022 fiscal year. No guidance was given when it came to other profitability metrics. But if we assume that they will increase at the same rate that adjusted net profits should, we should anticipate adjusted operating cash flow of $151.1 million and EBITDA of $175.6 million. It's likely that management will make full use of this rise in profitability. I say this because, in late June of this year, the company announced that it was increasing its share buyback program by 1 million shares to 1.25 million shares. So far, management has not bought back any stock. But that could change at any moment.

{kind=link}

Using these numbers, pricing the company becomes pretty easy. On a forward basis, the firm is trading at a price-to-earnings multiple of 10.5. This compares to the 14.1 reading that we get using data from 2022. The price to adjusted operating cash flow multiple should be 5.8. That's down from the 7.8 reading we get using data from 2022. Meanwhile, the EV to EBITDA multiples should decline from 8.5 to 6.4. As part of this analysis, I also compared the company to five similar businesses. On a price-to-earnings basis, these companies ranged from a low of 4.6 to a high of 38.6. In this case, three of the five companies were cheaper than Apogee Enterprises. Using the price to operating cash flow approach, the range is between 8.7 and 29.4, with our prospect being the cheapest of the group. And when it comes to the EV to EBITDA approach, the range is between 2.9 and 15.2. In this scenario, two of the five companies are cheaper than our prospect.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Apogee Enterprises |

| 10.3 |

| 5.8 |

| 6.4 |

| American Woodmark Corporation ( AMWD ) |

| 38.6 |

| 15.9 |

| 15.2 |

| JELD-WEN Holding ( JELD ) |

| 8.0 |

| 25.7 |

| 7.2 |

| Quanex Building Products ( NX ) |

| 8.4 |

| 8.7 |

| 4.7 |

| Tecnoglass ( TGLS ) |

| 11.8 |

| 9.3 |

| 7.3 |

| Insteel Industries ( IIIN ) |

| 4.6 |

| 29.4 |

| 2.9 |

Takeaway

All the data that I'm looking at right now suggests to me that Apogee Enterprises is sitting in a pretty good position at the moment. I do still think the company will face volatility in the long run. But shares are priced at very low levels on an absolute basis and don't look to be any worse than fairly valued compared to similar businesses. All in all, this gives me the confidence to increase my rating on the company from a ‘hold’ to a ‘buy’.

For further details see:

Apogee Enterprises: A Revision To Expectations