AIF - Apollo Tactical Income: Top Of The Capital Stack Paying 11%

2023-08-29 04:40:36 ET

Summary

- Apollo Tactical Income Fund is the top-ranked senior loan closed-end fund over the past 10 years, paying a well-covered 11% distribution.

- Plus, "double discounts" with both the fund itself discounted 10% off its NAV, and a further discount on the market price of the fund's underlying loan portfolio.

- Bottom line: An overall discount of about 15+% on a well-managed portfolio of senior, secured corporate loans.

- No wonder professional institutional investors own 47% of it.

Apollo Tactical Income Fund ( AIF ) is a closed-end fund that focuses primarily on credit investing, its assets comprising:

- Senior secured corporate loans (72%)

- High yield bonds (21%)

- Collateralized loan obligations (CLOs) (7%)

I own it personally, and we also hold it in our Inside the Income Factory core model portfolio, as well as in our simplified "KISS & DRIP" model.

Let's look at why we like AIF. What criteria do we apply?

I started to do credit and financial analysis in the early 1970s, when we had slide rules, pencils and paper instead of calculators, computers and spreadsheets ( link here ). So I tend to be somewhat spartan and frugal in my analytical approach, focusing on a few essential factors and features in assessing closed-end funds and similar instruments:

- What does the fund say it expects to do?

- What is its total return history?

- How does the fund earn that total return?

- What is the fund's earnings coverage (aka "distribution coverage"); in other words, how much of its distribution is covered by Net Investment Income ("NII")?

- How dependent is the fund on "heroic" income, over and above its NII, for its historical total return and to fund its distribution?

- How can we tell if funds that are highly dependent on capital gains as their primary source of total return, especially equity funds, will continue to generate capital gains in the future?

- How is the fund priced? What does it pay as a distribution yield? Is there a discount that provides a margin of error?

- Who is investing along with me? Are there professional/institutional investors putting their money into the fund?

How does AIF describe its strategy?

This is from its website :

The Fund's primary investment objective is to seek current income with a secondary objective of preservation of capital by investing in a portfolio of senior loans, corporate bonds and other credit instruments of varying maturities.

As mentioned above, most of its portfolio is senior corporate loans. Senior loans are at the top of the corporate capital structure, which means they get paid first in the event of the issuer's default or bankruptcy. Virtually all of them have specific collateral security, which lenders get to sell and collect 100% of the sales proceeds, before any creditors below them get paid; with the equity (i.e. the stockholders) collecting whatever is left, if anything, after the senior, secured creditors and then all the other unsecured creditors below them, get paid.

This makes senior secured loans a very durable asset class, with the average defaulted loan recovering about 65-75% of its principal, according to historical default and recovery studies going back many decades. This means if the default rate (i.e. the percentage of healthy loans expected to default) is projected to be, say, 5% in an upcoming recession (if in fact we get one), then the losses to loan investors would be only about 1.7%. That's because if defaulted loans repay their investors 65% (we'll be conservative), then the loss on each defaulted loan is 100% minus 65% recovered, or a loss of 35% of the loan principal. If 5% of your loans default, and you lose 35% on each one, then your overall portfolio loss is 5% times 35%, or about 1.7%.

That would be a pretty modest loss to take on a portfolio with a recession level (i.e. 5%) of defaults. (And it would likely be VERY modest compared to what equity investors would be losing in the same recession scenario.)

In normal periods, defaults would be much less, perhaps 1 or 2%, so your losses on a secured loan portfolio might be 0.35% to 0.7%. In either case the losses are modest compared to the yields of 8-10% (or even higher, 11% currently) that a fund like AIF offers us.

Total Return History

AIF has been a stellar performer in the senior secured loan space for the past decade. Its sponsor and manager, Apollo Global Management, has about $600 billion under management, and has been doing "alternative asset" management, especially credit, for over 30 years.

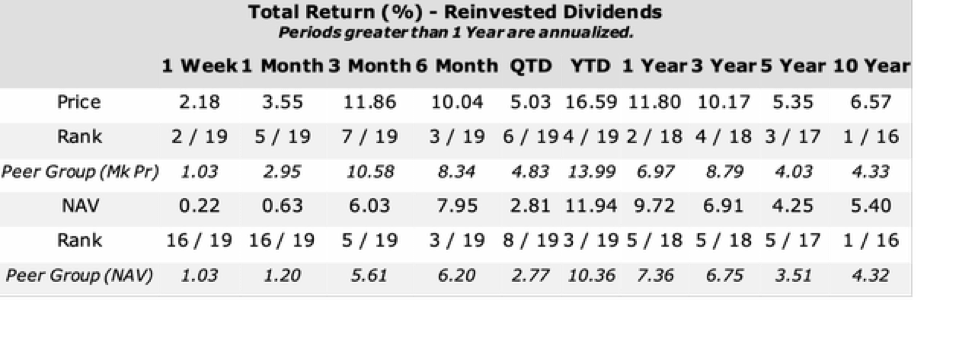

Here is AIF's total return record for the past decade:

{kind=link}

This chart from CEFData shows how AIF was #1 out of 16 closed end funds in total return, measured on market price and on Net Asset Value ("NAV") over the past 10 years, and #4 out of 19 and #3 out of 19, for Year-To-Date total return, by market price and NAV respectively. The 10 year average returns in the 5-6% range were very good for a period that had base interest rates close to zero for much of the period.

Now, with the Secured Overnight Funding Rate ("SOFR"), the base rate for senior corporate loans, up over 5% and likely to stay there for awhile, the yield on loans is much higher once you add a credit spread. That has brought senior loan yields to the 10% range, which is why this asset class is so attractive to Income Factory® and other institutional investors seeking to earn equity-level returns via cash distributions, so capital gains become a "nice to have," rather than a "must have." This article from Pinebridge Investments points out that senior loan yields have not been this high since the 2009 crash.

How Does AIF Earn Its Total Return?

Total Return from an investment is the cash earned from it, via dividends, interest or other cash distributions, plus the gain or loss in its value during the reporting period. So a fund that pays a 10% distribution and has a capital gain of 0%; or one that pays out a 0% distribution and has a capital gain of 10%; or one that pays out a 5% dividend and grows in value by 5%; they all have a total return of 10%.

But how the fund actually earns that 10% total return can vary quite a bit. Most credit or fixed income funds own assets (loans, bonds, preferred stocks, etc.) that collect interest or dividends that they use to pay their own distributions to shareholders. That allows those funds to pay all (or at least most) of their distributions with their own incoming cash flow, and therefore without having to sell off any (or much) of their own capital base to raise the cash to pay the distributions. I often refer to this as being able to pay their distributions with "business as usual" income , since the interest and dividends on their portfolio tend to keep on flowing in, regardless of whether the market is causing the day-to-day value of the assets generating that "business as usual" income to go up or down.

Equity funds, on the other hand, generally hold stocks that only pay dividends of about 1-2%. The S&P 500 ( SPY ), for example, pays a yield of 1.5%. That means the many closed-end funds that hold stocks and pay distributions of 6 or 7% or more, as many do, have to earn capital gains each year exceeding that amount, if they want to both cover their distributions and still have some ability to grow their stock price and achieve a total return of 9-10%. I call that being dependent on "heroic" income , as opposed to the "business as usual" income that credit and fixed income funds need to support their distributions.

Distribution Coverage: Little Reliance on "Heroic" Income

Fortunately, AIF can rely on its "business as usual" income - the cash flow from its credit portfolio - to pay its distributions. In its most recent annual report it reported Net Investment Income ("NII"), which is the interest income on its portfolio minus all the fund expenses, of $17.2 million, which covers the distributions it paid out to shareholders of $17.0 million by 101%.

The story is even better since then, as the chart up above shows, with the fund having achieved a year-to-date total return of 16.5% and 12% on its market price and on its NAV, respectively. On an annualized basis, those year-to-date returns would, of course, be even higher; but the main point is that the fund is easily covering its current annualized distribution yield of 11.1%.

But that's not all, as we consider the discounts we as investors can benefit from when we buy AIF and other senior loan closed-end funds at this point in the market cycle.

Discounts on Discounts

To start with, we know at the moment we can buy AIF at a 10% discount to its Net Asset Value ("NAV"). That means the fund's market price is only 90% of the current market value of the loans in AIF's portfolio, so when we buy the fund, we have 10% more assets working for us than we had to pay for.

But that 10% discount on the market price only tells part of the story. The market price of healthy senior corporate loans is itself discounted from the loans' par value (.e. the amount the borrower has to pay back to the holder at maturity). Currently the 100 largest corporate senior loans (per the Morningstar/LSTA Index) are trading at prices averaging 96 cents on the dollar, but many other loans are trading at prices closer to 90. Even if we assume AIF's portfolio is priced as high as 95 cents on the dollar, it means as investors we are paying 90% of the market price, for a portfolio whose prices are already only 95% (or less) of the 100 cents on the dollar AIF will receive back from the borrowers when the loans reach maturity.

So our overall discounted price is 95% times 90%, or about 85% of what the loans will ultimately repay. That's a 15% discount, and it means that besides AIF's fully covered 11% yield that we are currently receiving, there should be room for some serious capital gains and/or special distributions in the future.

Investing In Good Company With Professionals

We are not the only ones to have noticed AIF, with its great long-term record and the current opportunities offered by the discounts in BOTH the closed-end fund market and the corporate loan market. Major institutional investors and other mutual funds, including activist firms Boaz Weinstein's SABA group and Philip Goldstein's Bulldog group, together own about 47% of the fund. Obviously that alone is not a reason to buy a fund, but I like the additional positive signal it sends. And I like knowing that I'm in good company when I make the investment, that professionals doing this for a living with millions of dollars are endorsing my selection.

Bottom line

- Experienced manager

- Great record over the past decade

- Attractive, well-secured asset class, especially at this point in the cycle

- High yielding, well covered distribution

- "Double discounts on discounts"

- Lots of institutional investor interest

Those are the reasons I hold it personally as well as in our Inside the Income Factory core model portfolio. As always, I look forward to your comments.

For further details see:

Apollo Tactical Income: Top Of The Capital Stack, Paying 11%