APPF - AppFolio: Attractive Growth Prospect But Priced Almost Perfectly

2023-05-10 08:30:00 ET

Summary

- AppFolio is a cloud-based property management software company with attractive fundamentals.

- The launch of AppFolio Stack, which potentially brings strategic value for the business and potential future expansion into the short-term rental market, presents catalysts for the stock.

- At ~9.5x P/S, AppFolio has a premium valuation. The target price model suggests that AppFolio is just slightly undervalued.

AppFolio (APPF) is a leading provider of cloud-based property management software solutions. Based on a quick screen, the stock's fundamentals seem attractive enough to merit further exploration. In recent fiscal years and as of its Q1 2023 earnings announcement, revenue growth has been between +20% to +30%, operating cash flow / OCF positive and steady, and the balance sheet very strong with close-to-zero debt levels.

Furthermore, despite its compelling value proposition and strong market position, AppFolio has largely flown under the radar of many investors. However, with the growing demand for digital solutions in the real estate industry, AppFolio is well-positioned to capitalize on a number of tailwinds that are expected to drive strong growth in the years ahead. As per the information by the management in Q1, I see a few catalysts benefiting the stock to establish a sufficiently attractive growth story:

- The launch of 3rd party integration marketplace services to not only enhance and streamline the customer experience but also provides a learning opportunity for AppFolio to understand better how to make strategic expansions into other value-add services - a key pillar for its growth.

- Longer term, I view short-term rental property management as a potentially interesting market for AppFolio, given the TAM and higher international exposure opportunities.

In this first coverage, I seek to discuss further those key catalysts, as well as the company's products, financials, business models, and customer segments. I will also examine the company's limitations and risks, before combining all of the information into my target price model for AppFolio, which suggests that the stock is just slightly undervalued and therefore presents a long opportunity. I initiate this coverage with an overweight rating.

Brief Background - Product/Business Models/Customers

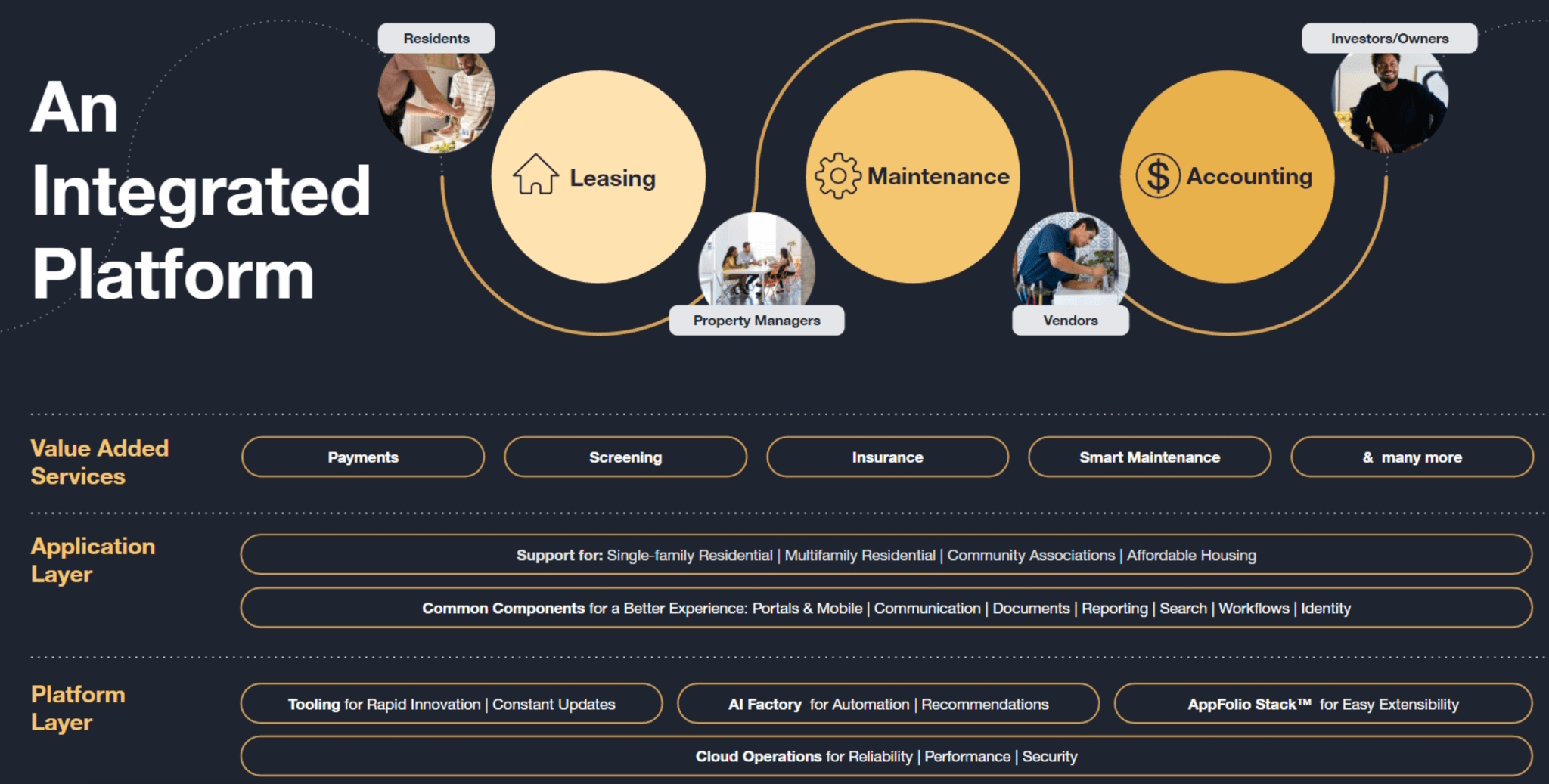

AppFolio operates exclusively in the US market, and its suite of products is designed to help property managers and landlords streamline their operations, improve tenant experiences, and ultimately, drive higher returns. AppFolio's flagship product is its AppFolio Property Manager platform / APM, which provides a comprehensive set of tools for managing everything from rent collection, tenant screening, and lease renewals to maintenance requests and accounting.

{kind=link}

As part of the company's recent upmarket move, it has also launched an enhanced offering better suited to serve customers with larger property portfolio and team members, APM Plus. As indicated from its 10-K, APM Plus provides customizable workflows, performance insights, revenue management, technology integration, and dedicated account managers to streamline property management processes, optimize asset potential, and improve customer experiences.

{kind=link}

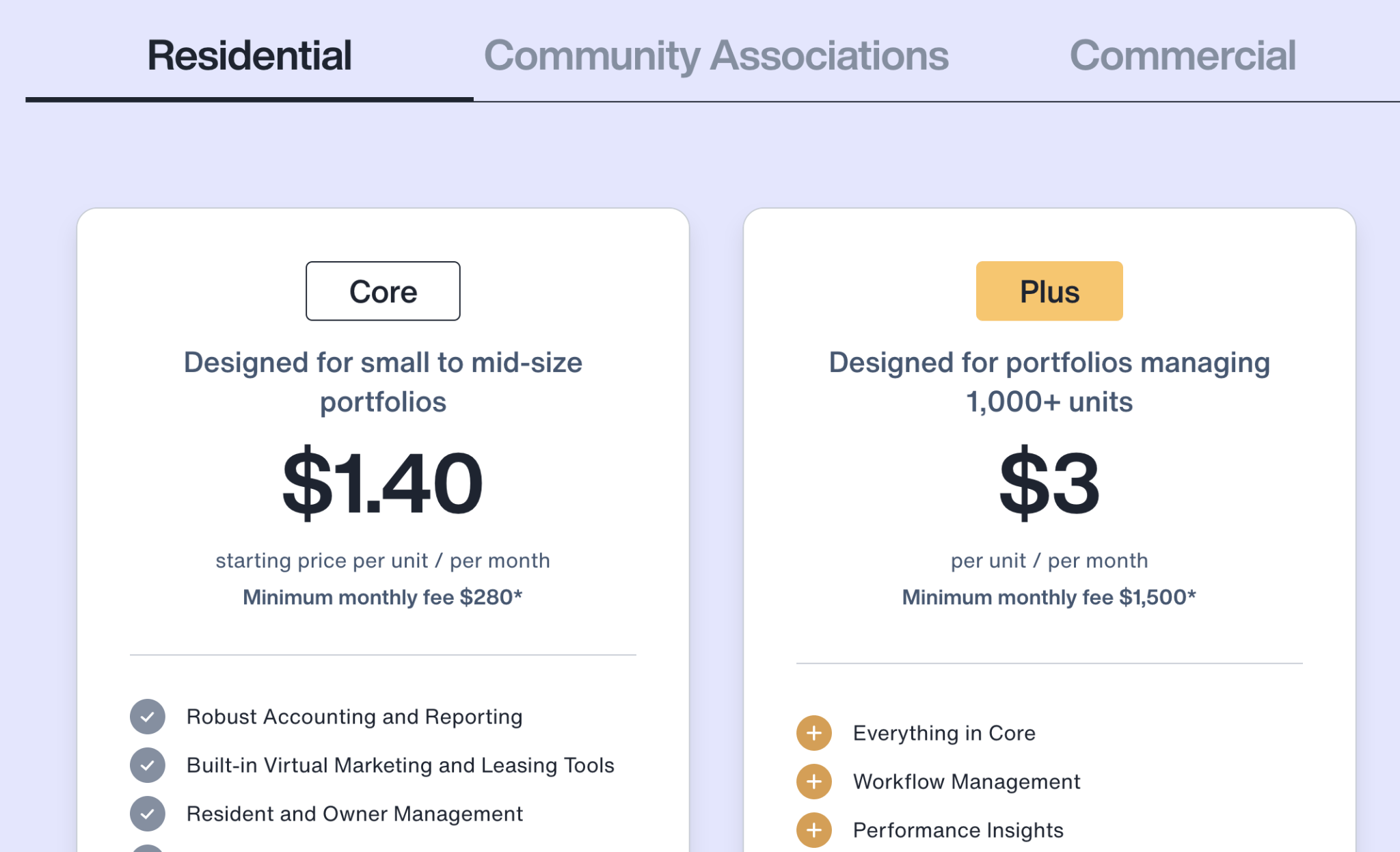

AppFolio has two main revenue streams. Firstly, AppFolio generates revenue through its subscription-based business model, whereby customers pay a subscription fee to access its cloud-based platform. Based on the company's website , the product is priced based on the number of units managed by the customer, with different pricing tiers available for different levels of functionality and support.

In addition, AppFolio also generates revenue by charging fees on certain key rental-related activities performed by its customers in its platform - termed Value-Added Services / VAS. These include fees for payment processing services, which are charged as a percentage of the transaction value, and fees for tenant screening services, which are charged on a per-screening basis. Interestingly, AppFolio has historically been generating most of its operating revenues from VAS fees instead of subscription fees to the cloud-based platform.

{kind=link}

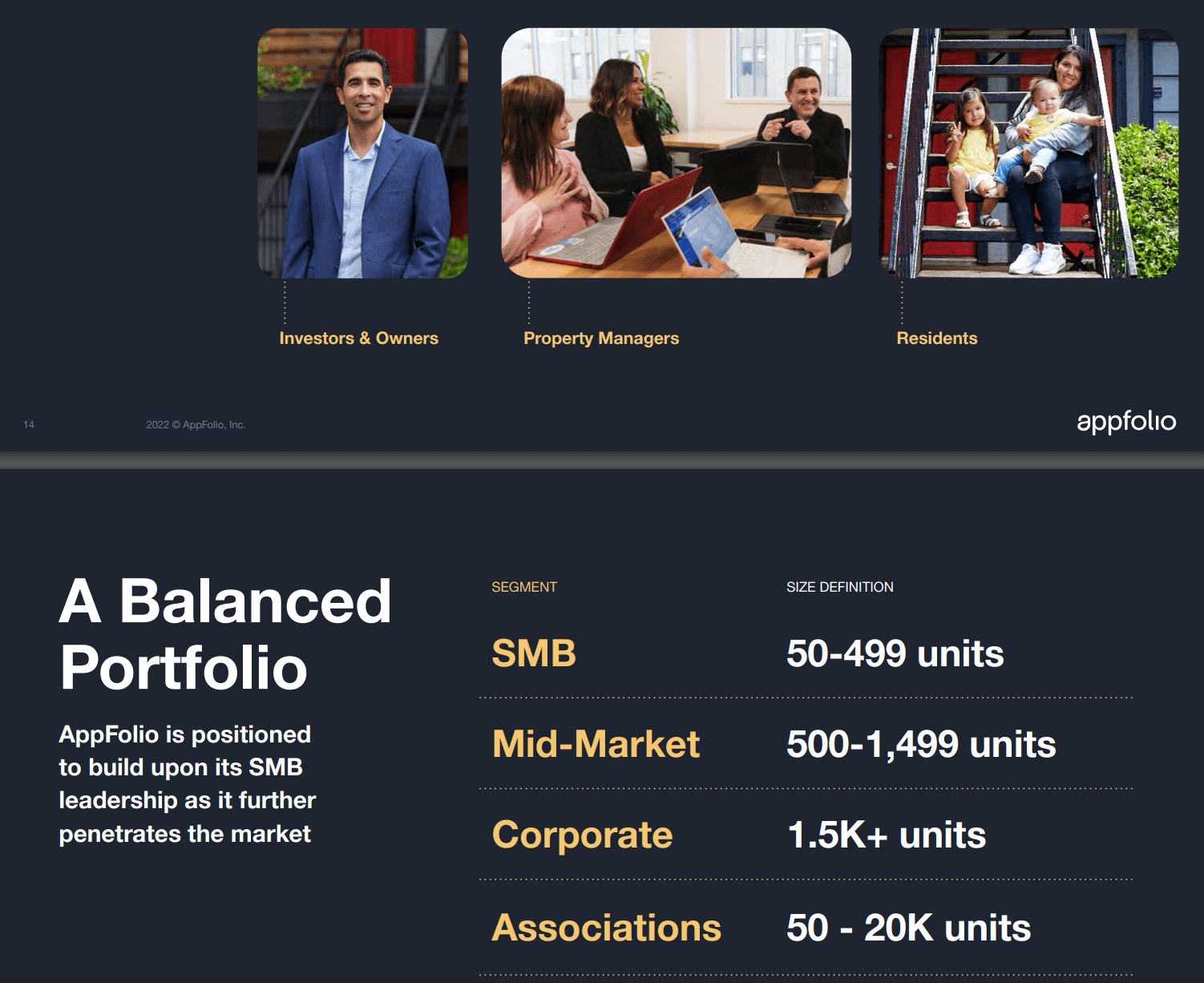

The pricing tier is also influenced by how AppFolio segments its customers, which range from individual property owners, property management companies - including residential and commercial property managers, to homeowner associations. These customers also range in size from small independent operators to large national firms.

Q1 2023 and Financial Highlights

Here is a recap of AppFolio's Q1 2023 results, along with relevant commentary:

- Q1 revenue of $136.1 million, a +29.2% YoY, beating the estimate by $5.26 million - Except for the first two quarters in FY 2021, AppFolio has historically beaten its quarterly revenue estimates.

- As of Q1 2023, total units under management increased to ~7.5 million from ~6.6 million at the end of Q1 2022 - the increase here has been quite consistent between 13% - 15% YoY. AppFolio ended FY 2021 with 6.3 million, FY 2022 with 7.3 million, and since FY 2022, we have seen a ~200k increase in the number of managed units.

- FY 2023 revenue to be in the range of $570 million to $580 million.

- FY 2023 non-GAAP operating margin is expected to be in the range of 1% to 2%.

- FY 2023 non-GAAP free cash flow / FCF margin is expected to be in the range of 2.5% to 3.5%.

- FY 2023 weighted average shares outstanding of ~36 million for the full year.

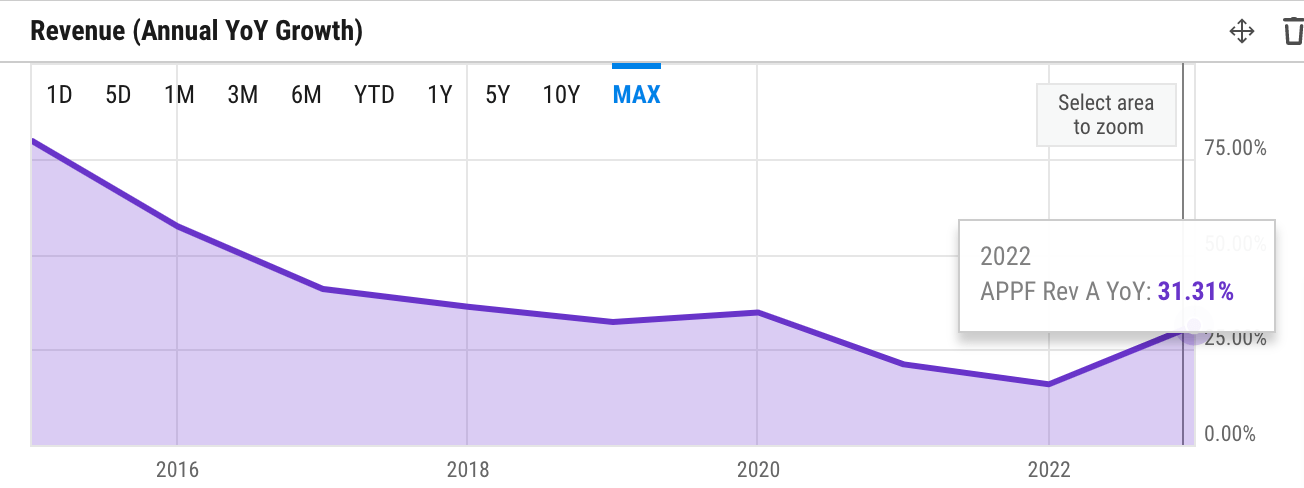

Trend-wise, AppFolio's revenue growth has been quite steady. In FY 2022, revenue also accelerated to +30% YoY, even if we had accounted for the missing revenue growth from MyCase, a business divested by AppFolio from the previous FY.

ychart - APPF's annual revenue growth

{kind=link}

Q1 revenue also grew by ~29% YoY, though in FY 2023 growth is expected to be at a +20% level. I think that the outlook remains acceptable, especially during the current economic downturn where many cloud software stocks are facing slowdowns. To that extent, it appears that AppFolio may also be a bit fortuitous to be quite isolated from the potential higher tenant displacements as a result of the growing layoff trends. Moreover, the slower growth outlook is also counterbalanced with the expectation of maintaining positive FCF.

{kind=link}

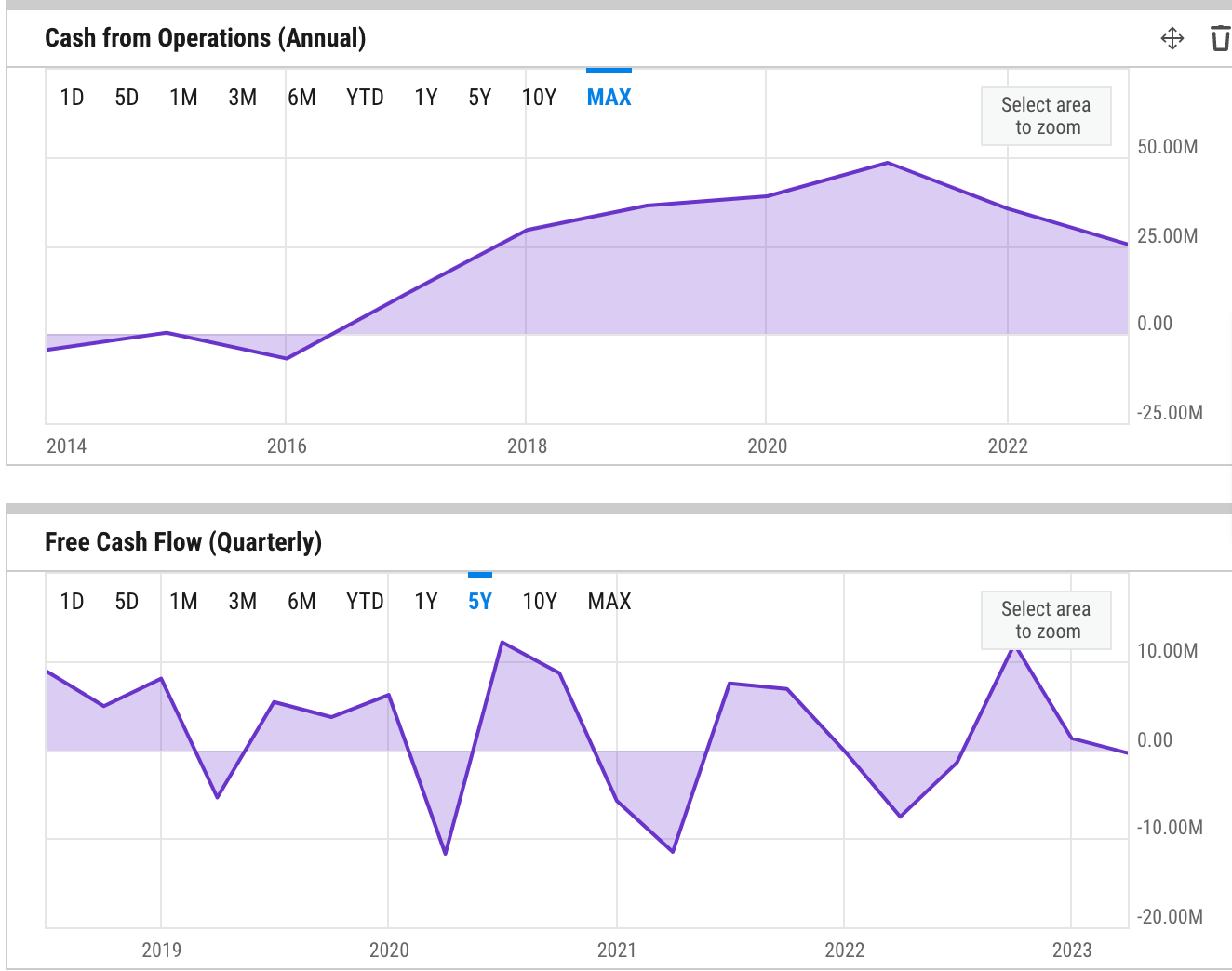

FCF and OCF generations have been steady, though I do not expect the company to guide to those particular metrics. As much as it is important to maintain a positive FCF, there is potentially a need to invest for growth at some point in the future. Furthermore, on a quarterly basis, we typically see a seasonality of FCF generation due to the property rental market behaviors. Cash flow generations tend to peak in May and September, the summer months when tenants mostly move in or out.

Market Landscape

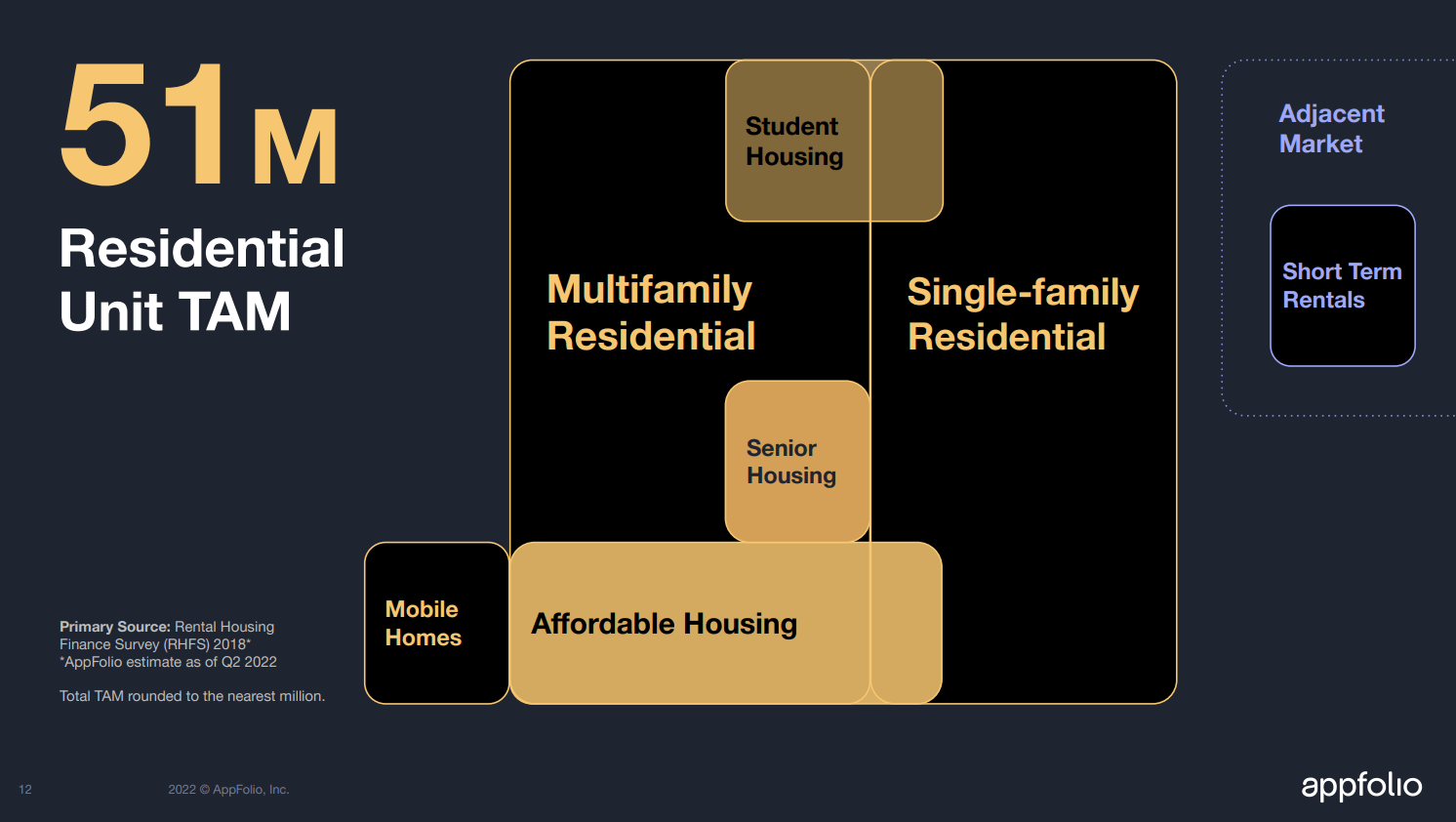

The property management software market is driven by the growth of the residential/commercial property rental market in the US. Residential is the largest segment of the property market, with AppFolio estimating the TAM to be 51 million units.

{kind=link}

Broadly, the market includes commercial, single-family/multi-family residential, and student housing properties. Factors such as demographic trends, urbanization, and lifestyle preferences, as well as economic conditions and government policies, continue to drive the market. Recent trends affecting the market include increased demand for affordable housing, rising construction costs, and the impact of the COVID-19 pandemic on rental demand and rental rates.

Additionally, the rise of technology has led to the development of innovative solutions for property management, such as AppFolio's cloud-based software solutions, which are designed to improve efficiency and streamline operations for property managers.

{kind=link}

Some competition in this space includes Yardi and RealPage, which is a portfolio company of Thoma Bravo, a software-focused PE investor. AppFolio remains the only publicly-traded company in the market landscape.

However, internationally, I see a limitation to AppFolio's solutions due to different discovery and rental behavior. While it would be ideal for AppFolio to expand to higher populated geographies, I notice how the property rental market in the US behaves a bit differently from those of other parts of the world. In the US, it is still a market that faces a high degree of fragmentation, but it is by far a more digitized market than the rest of the world.

In other large markets like China or India, the first point of contact for customers looking to rent a property for the medium or long term would often be a property rental e-commerce platform that connects them to property agents or owners who typically double as property managers. These rental platforms largely make money off premium listing or advertising, and some of them also provide cloud property management tools to enable the agents/owners/managers to manage leads. However, given the history of under-penetration of digital record-keeping and credit card payment, many of the rental fees are settled by wire transfers offline outside of the e-commerce platforms.

Platforms like AppFolio, on the other hand, are not e-commerce marketplace rental listing platforms. First customer touchpoints are generally independent rental listing sites that AppFolio often has nothing to do with, but the property managers overseeing those rental units would then adopt the AppFolio platform. Nonetheless, due to the high-touch nature of the medium to longer-term rental activities, there often appears to be a disconnect between engaging the property listing and paying for rent online in most parts of the world.

Another market segment that seems to be within AppFolio's sight is the short-term rental market, which is dominated by vacation-related activities. E-commerce rental companies like Airbnb (ABNB) have thrived in this market. Internationally, I think that a platform like AppFolio may instead spot an opportunity in the short-term property management market, where customer behaviors in online bookings and payments are relatively more uniform globally.

Catalyst

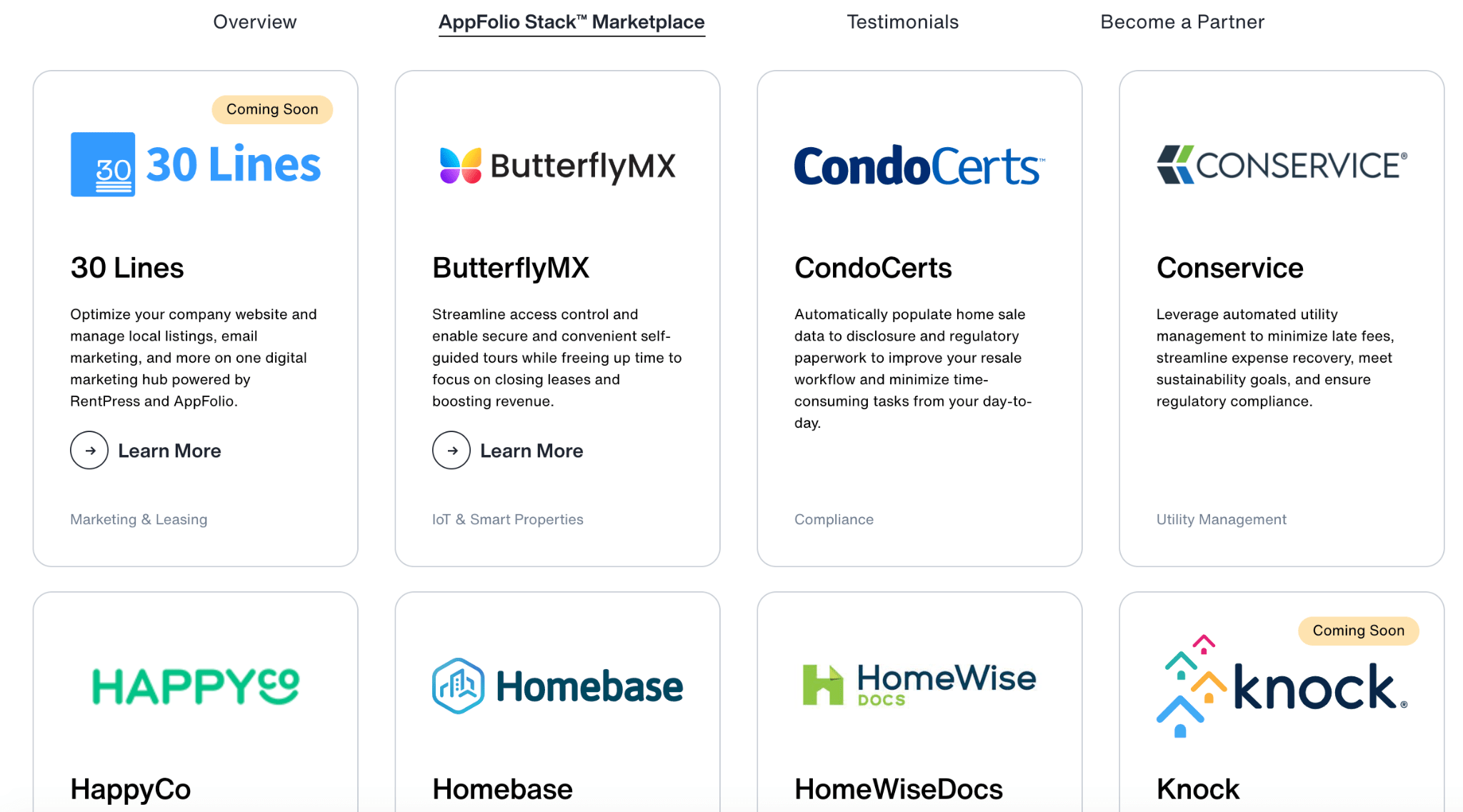

In Q1, the company highlighted its intention to move further upmarket to improve its ARPU / Average Revenue Per Unit. It is a sensible move considering AppFolio's unit-based pricing in its business model. As part of the strategic initiatives, the company launched AppFolio Stack last year, which is pretty much a marketplace that helps its customers, the property managers, to integrate 3rd party related rental-related online services into their AppFolio accounts.

{kind=link}

AppFolio has partnered with a few companies providing online solutions to manage utilities, paperwork, digital marketing, as well as self-guided tours. The company claims that the integration helps streamline and centralize all aspects of property management in one platform, the APM.

While AppFolio often highlights the aspect of providing a better customer experience with the integration, I believe that the move provides another strategic benefit, whereby AppFolio can eventually gain better intelligence into what areas of expansion it should enter to enhance its VAS business by monitoring the integration activities to its core platform.

{kind=link}

AppFolio would certainly know better the importance of strengthening its VAS business, which the management describes as a growth pillar . As discussed previously, AppFolio has been generating most of its revenues from two VAS - payment and tenant screening services. In FY 2022, VAS did not only generate more than twice as much revenue as the core subscription business, but at 36% YoY growth, it was also the fastest-growing segment of the business.

In addition, while the company has not yet announced a timeline to enter the short-term rental market, it already highlighted it as part of the TAM during the investor day , indicating that the management is at the very least considering an expansion there in the future. I believe that short-term rental property management can be a potential long-term growth driver for AppFolio for two reasons: 1) the biggest use case for short-term property management would be vacation rentals, which has an attractive TAM and will over time balance out the cash flows seasonality of AppFolio. 2) Given AppFolio's limitation to grow internationally due to resource and capability constraints, the vacation-oriented short-term rental property management market can provide a convenient entry point for international expansion.

Valuation/Pricing

In estimating the stock's fair price today, I consider two extreme probability-based scenarios in my 5-year target price model for AppFolio:

-

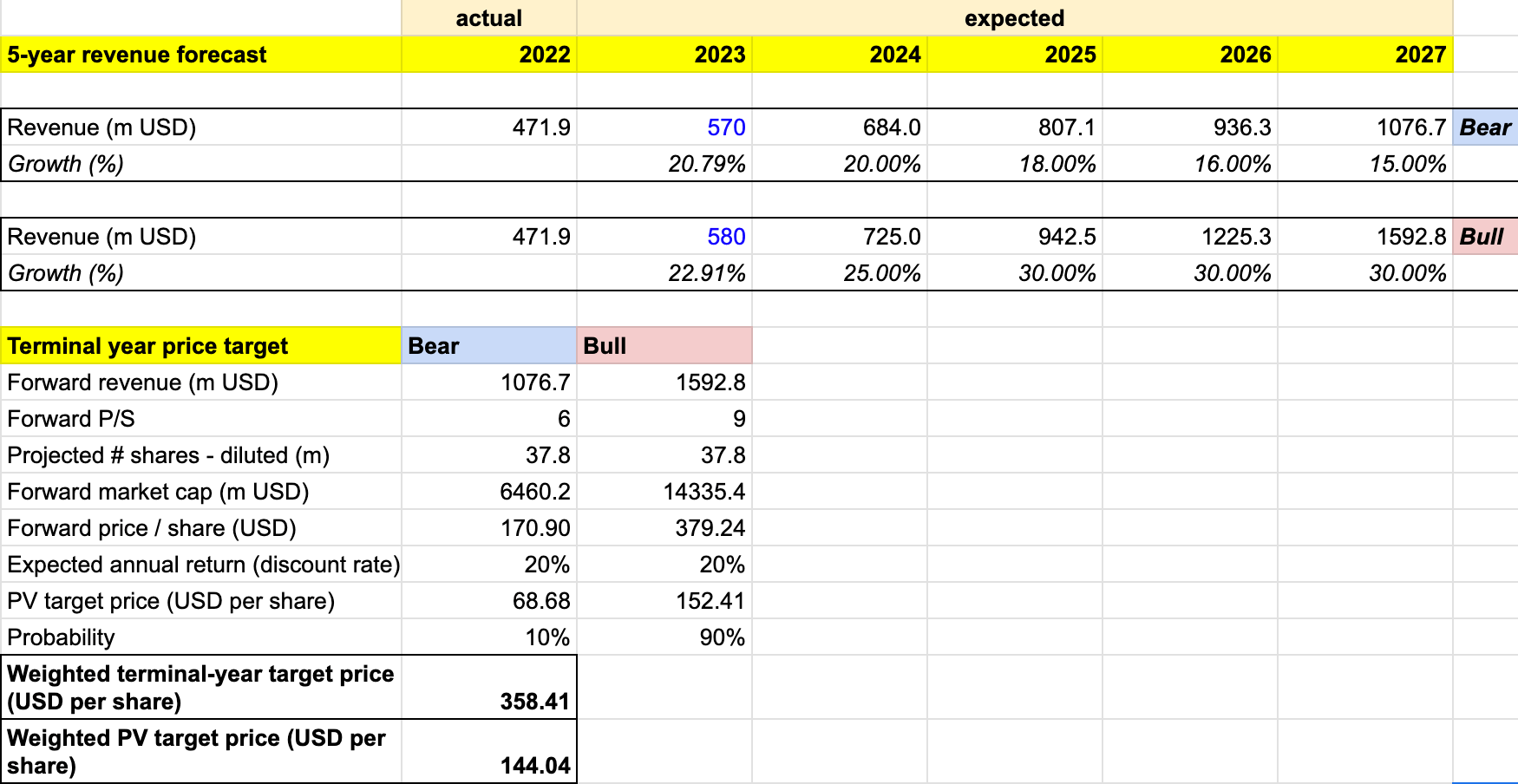

Bull scenario (90% probability): I expect the profitability, FCF / OCF, and growth outlook to improve as a result of the successful upmarket move and consistent +15% growth in units under management, driving ARPU up. Growth to reaccelerate to 30% in FY 2025 as the company decides to strategically enter another VAS vertical, either through M&As or organically. I also suggest a likely possibility of AppFolio entering the cloud-based short-term rental market possibly in the second half of the projection period. Given the robust fundamentals and growth, I assign a P/S of 9x to AppFolio in FY 2027 - a figure that is only slightly lower than today's 9.5x to account for the potential size of the business in FY 2027, where I expect AppFolio to be a $14 billion company.

-

Bear scenario (10% probability): AppFolio to have a less ambitious roadmap than in the bull scenario. Though profitability and cash flows continue to be maintained, growth will slow down annually as the company decides not to expand into adjacent markets. AppFolio in FY 2027 is pretty much a $6 billion company growing at 15% YoY under this scenario. P/S to contract from ~9.5x today to ~6x, closer to the average P/S of cloud software stocks in the comparable universe I gathered.

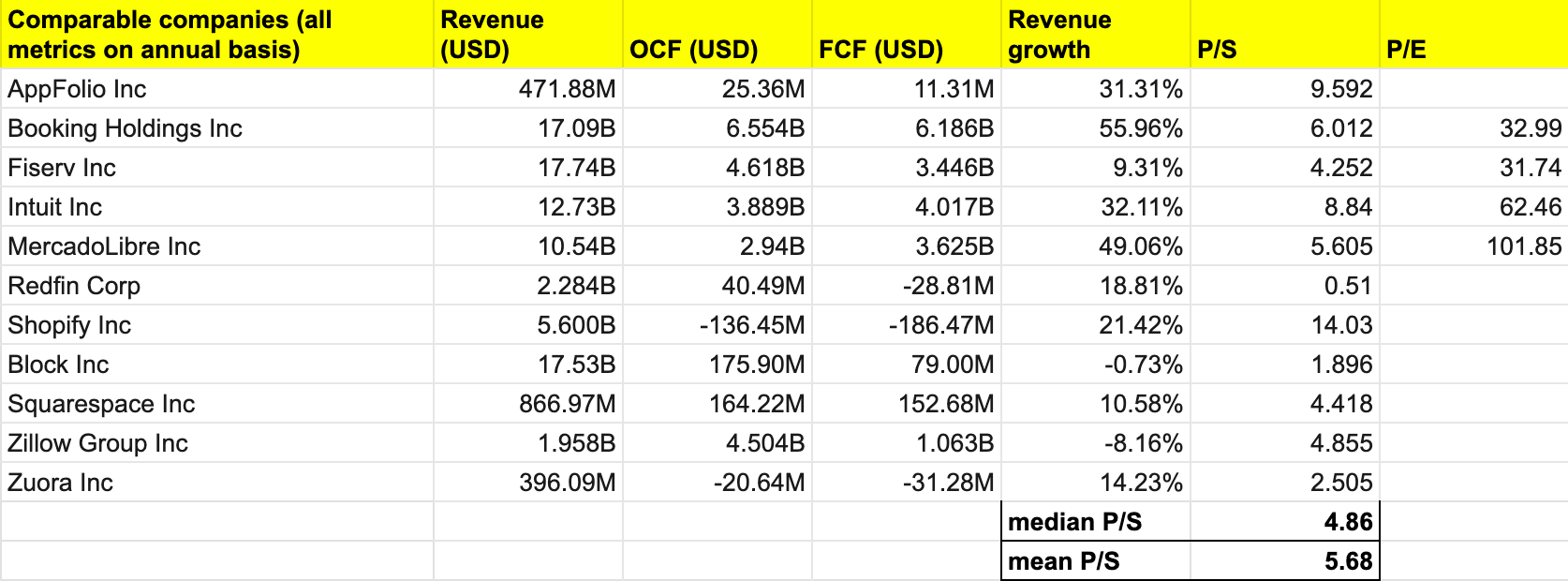

author's own analysis - APPF comparables

{kind=link}

In addition to Zillow or Redfin which more or less offer similar solutions but are marketplace platforms, I also select a few software companies with a similar B2B (Business to Business) model to AppFolio that generate a considerable portion of its revenue from payment processing, despite not being payment companies themselves. AppFolio remains the stock with the highest P/S in this group, second only after Shopify (SHOP). AppFolio, however, is also one of the second-smallest-cap stocks in this group after Zuora (ZUO).

author's own analysis - APPF target price

{kind=link}

I consolidate the two scenarios above in estimating the probability-weighted target price for FY 2027, before discounting that price back to today with a 20% discount rate. The 20% rate here represents the minimum annual return that investors can expect for holding AppFolio.

I arrived at a weighted target price of ~$358 per share for FY 2027, which is comparable to ~$144 per share today. Investors can interpret the $144 per share as the maximum entry point to initiate a long position to realize the 20% annual return as outlined in the model.

As such, at ~$137 today, AppFolio is undervalued by just about 5%, giving some room for investors to realize higher excess returns if AppFolio is to achieve or outperform the projection.

Risk

While I expect AppFolio to do relatively well in its current market, there are always risks when it comes to TAM expansion. Expanding to adjacent markets, for instance, is something that AppFolio needs to actively consider to accelerate its growth though it certainly will face more challenges and intense competitions.

{kind=link}

In the short-term/vacation rental space, there are currently competitors such as iGMS. iGMS largely provides a solution for Airbnb hosts to manage their rental operations. However, while there seems to be a market validation here, the opportunity to generate payment fees from VAS in this space may also have limited upside, since those payments are generally made in-platform at the time of bookings (at Airbnb or the e-commerce platform). As discussed, AppFolio generates most of its revenue not from its core platform subscription but from payment processing. As Airbnb serves as a marketplace platform that minimizes counterparty risk, their hosts would prefer to get paid through Airbnb, limiting AppFolio's payment revenue opportunities in this market segment.

Ultimately, a cloud-based property management platform is a technology that is relatively easy to replicate. Speculatively, there may exist a potential threat from well-funded e-commerce marketplace players like Airbnb, Zillow (Z), or Redfin (RDFN), who in a circumstance where they found the market to be strategic and attractive enough, may establish/acquire a competing business to develop a similar offering at lower subscription fees with similar value-added services. This obviously would lead to a potential loss of market share for AppFolio.

On the other hand, despite my projection indicating that AppFolio is undervalued, it is still trading at ~9.5x P/S, which is considered expensive by some investors. My bullish projection also depends on a number of key assumptions, one of those being the expected 25% - 30% growth rate into FY 2027. I would expect increased volatility in the stock price and a potential decline in valuation if growth expectations are not met.

Conclusion

AppFolio, a leading provider of cloud-based property management software possesses attractive fundamentals, though has been quite underfollowed. The launch of AppFolio Stack marketplace services and potential growth in the short-term rental property management market present potential catalysts for AppFolio to become a sufficiently attractive growth story. There are potential risk factors coming from TAM expansion initiatives, but I think that overall, AppFolio remains a good business and is well-positioned to tackle those challenges.

With ~9.5x P/S, AppFolio has a relatively premium valuation. There is a buying opportunity today, though my target price model suggests that AppFolio is just slightly undervalued by 5% from the current price with a target price of ~$144 per share.

For further details see:

AppFolio: Attractive Growth Prospect, But Priced Almost Perfectly