APPF - AppFolio: Exposure To Real Estate Without Capital-Hungry Growth

2024-01-04 16:00:00 ET

Summary

- Basic materials and industrial sectors offer compelling risk-reward calculus in the next 12 months.

- AppFolio provides access to the real estate market at a differentiated point of the value chain.

- APPF has strong growth potential, with steady revenue growth and high capital turnover.

Investment briefing

Background

With the beatdown in commercial and residential real estate across 2022-'23 the question must be asked whether allocation to the sector is now worthwhile. Equally, as notable, valuations on the basic materials and industrials sectors (where many are tied to real estate markets) are heavily compressed relative to their embedded growth prospects.

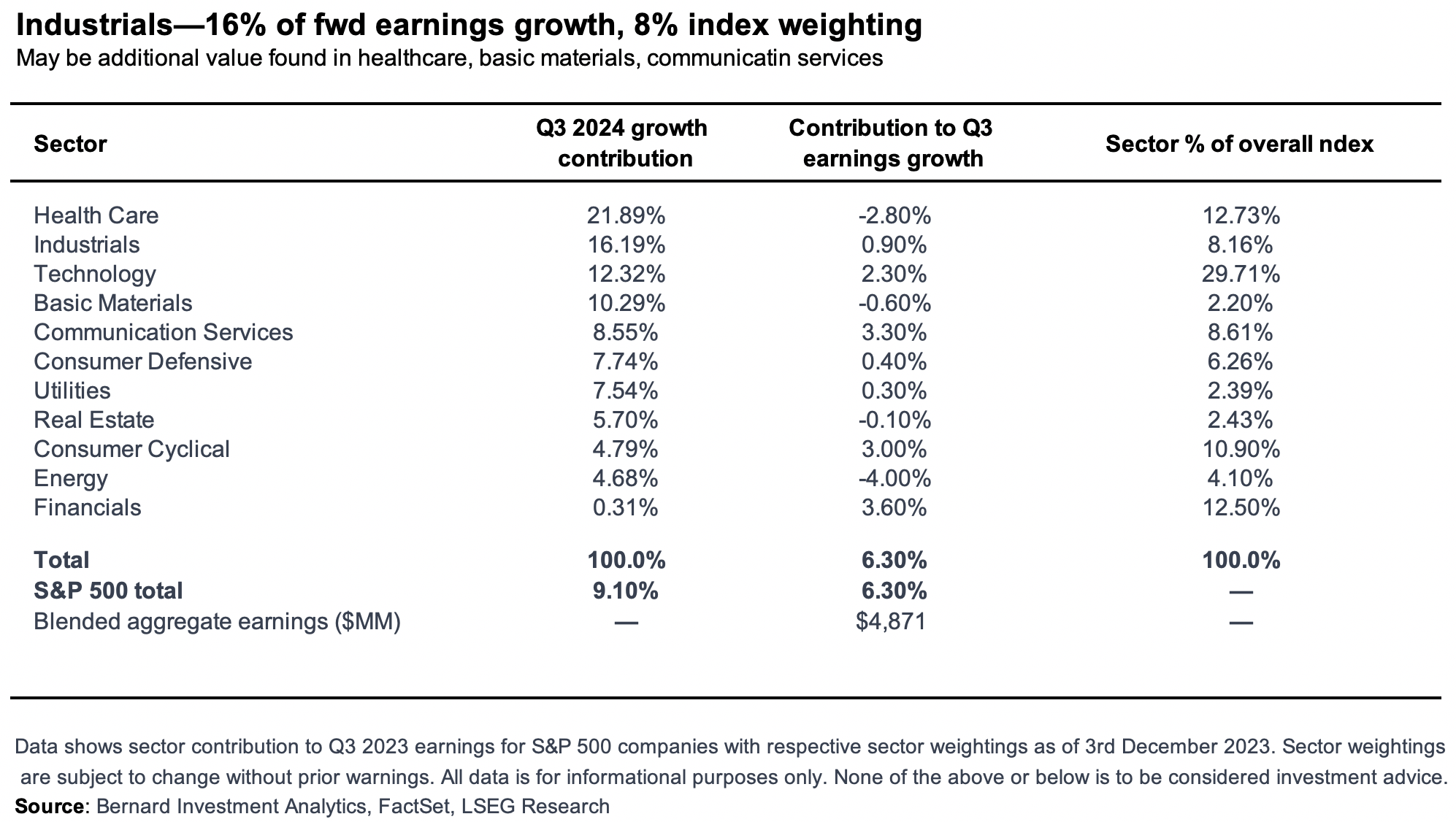

For instance, our research on Q3 S&P 500 earnings found that industrials and basic materials made up just 8% and 2.2% of the S&P 500 market-cap weighted index respectively, but were poised to deliver 16.2% and 10.3% of the next 12-months earnings growth respectively (Figure 1).

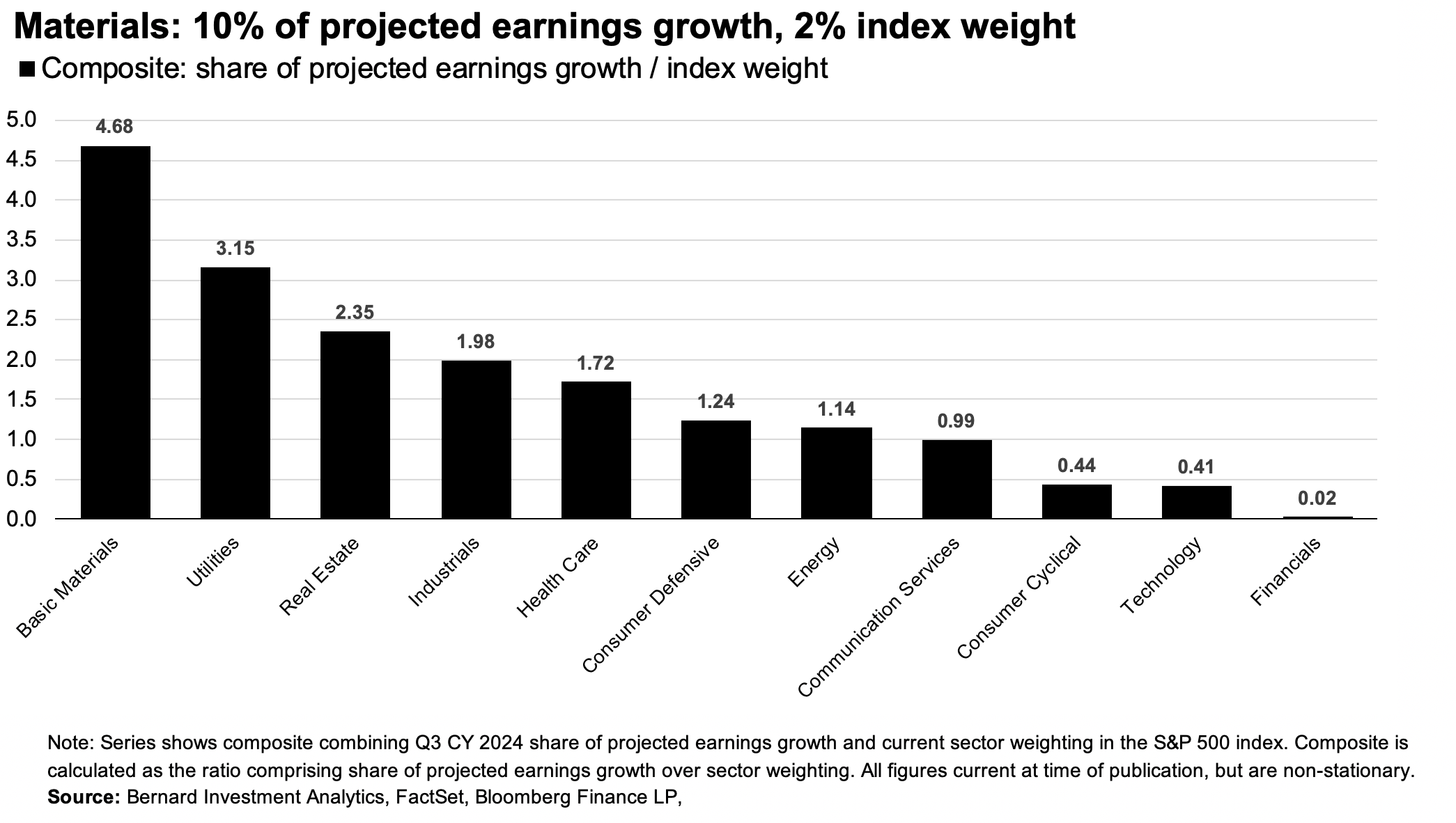

In fact, basic materials as a domain offered the highest risk-reward calculus, producing the highest outcome in a composite of projected earnings growth vs. current index weight/market valuation (Figure 2). As a top-down analysis of where to allocate precious capital in 2024, therefore, these two sectors are an excellent place to start looking.

Figure 1.

{kind=link}

Figure 2.

{kind=link}

With these points in mind, thinking should move to how to gain exposure to each sector, keeping in mind there are multiple avenues to do so.

Consider the following reasoning when it comes to positioning at various points along the value chain:

- The real estate business (commercial, residential, et al.) is a capital-hungry domain. Heavy CapEx and reinvestment requirements are needed to maintain a competitive advantage. Earnings produced on incremental capital are often lumpy and sluggish, reducing the prospects of investor returns (capital gains) over cash flows. Not to mention the inflationary impacts on asset replacement costs seen since 2022.

- Intangible-heavy software companies are one potential remedy to this situation, mitigating the capital-intensive nature of various industries. Software by its very nature offers multiple benefits to the asset owners. For instance, once commercialized:

- Multiple agents can use it at once (vs. tangible machinery for instance),

- It offers benefits of scale due to the above and no further CapEx,

- Both points (1) and (2) mean the tail of asset returns if both fat and long

- MOST CRITICALLY- and most often, software can be viewed as capital provided to a business. This is imperative to know. Software typically falls under a subscription or licensing model and is therefore treated as an operating expense to the user versus cash outflow from investing, financing, or operating activities. Under this notion, software owners therefore sit at the top of the capital structure, because providers of the software (capital) are paid before any other providers of capital- debt or equity. This is because it is an operating expense vs. an investment/financing expense, a unique position to be in as the asset/software owner.

Opportunity

Based on these data points AppFolio, Inc. ( APPF ) offers investors potential access to play potential upside moves in the markets for real estate, whilst sitting downstream of construction, physical ownership (inc. REITs), and/or buying and selling of immovable property.

APPF was established in 2006 and is in the business of workflow solutions for real estate companies. The core product, AppFolio Property Manager, automates workflows, whilst Property Manager Plus adds customizations, integrations, and so forth. Whereas AppFolio Investment Management prioritizes communication and such for real estate investment firms. Growth in the real estate industry is therefore good for APPF, albeit without the cyclicality in asset valuations.

The prospect of buying APPF is currently balanced by positive and negative factors. Fortunately, the positives outweigh the negatives in my opinion, and the market has revised its expectations lower on the company following its Q3 FY'23 numbers, providing an exciting opportunity to enter at the $160s per share.

Net-net, I rate APPF a buy, eyeing a price objective of $211 per share over the next 6-12 months. Supportive reasoning is outlined below.

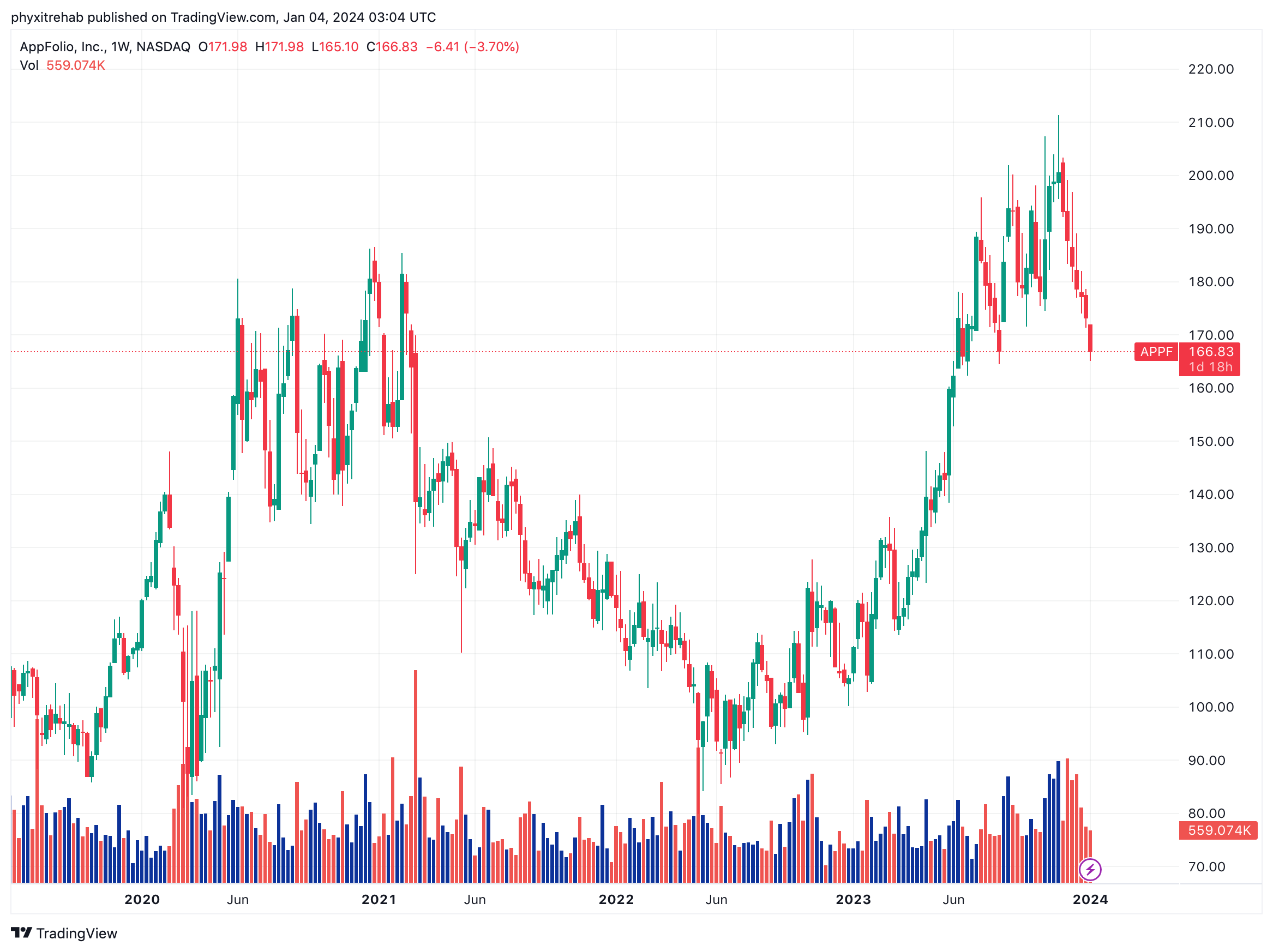

Figure 1. APPF Weekly Returns since 2020

{kind=link}

Overview of economic value drivers

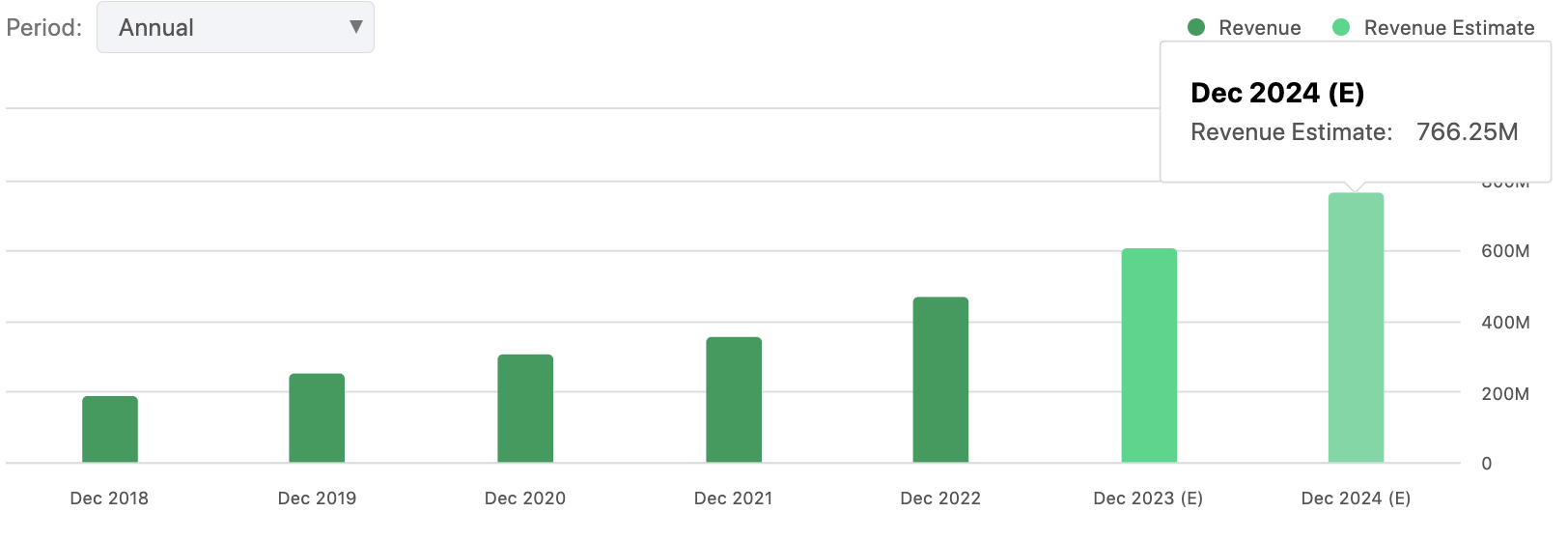

APPF has grown sales at a reasonable clip since 2018 and looks to push $612mm in annual sales for FY'23 (Figure 2). Wall Street has it to do $766mm of business in FY'24 and this has been well captured in APPF's market value by my estimation. Still, over the next 1-3 years, the consensus has 18-30% in sales growth forecast out to FY'26, on 105% earnings growth by FY'24.

This is constructive for investor returns over the coming 1-3 years.

I would point out that the company is still unprofitable at the GAAP level. Therefore, I will be watching any revisions to adj. earnings forecasts very closely as the company's stock price is highly sensitive to this by best estimation.

Figure 2.

{kind=link}

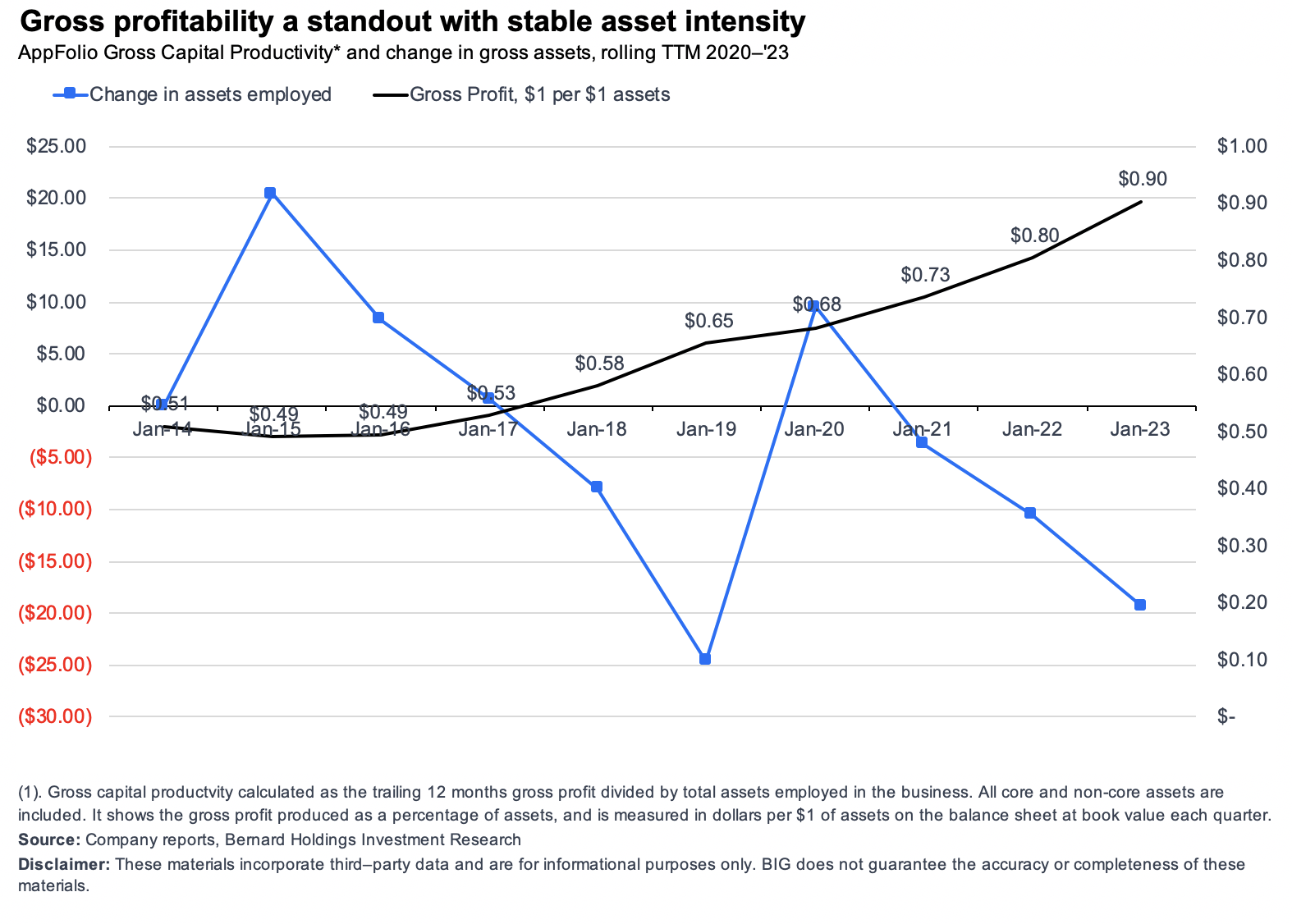

Aside from the financials, gross productivity is a standout for the company. This comes down to the nature of its software business, as discussed earlier. As seen in Figure 3, the firm produced $0.90 in TTM gross profit for every $1 of assets employed on the balance sheet last quarter, near parity in efficiency. This means it recycles basically all revenues to gross, as it costs just $0.10 on the dollar of investment to produce $1 in revenues when scaled to assets.

Again, this comes down to the fact that:

(i) Software providers are paid first in the capital structure (ensuring strong working capital and cash flows)

(ii) The capital required to produce sales is exceptionally low given it the intangible [software] capital produces the revenues.

These two points must be heavily considered in the investment debate in my opinion, especially as asset growth has been trending lower generally for APPF since 2020 (Figure 3).

Figure 3.

{kind=link}

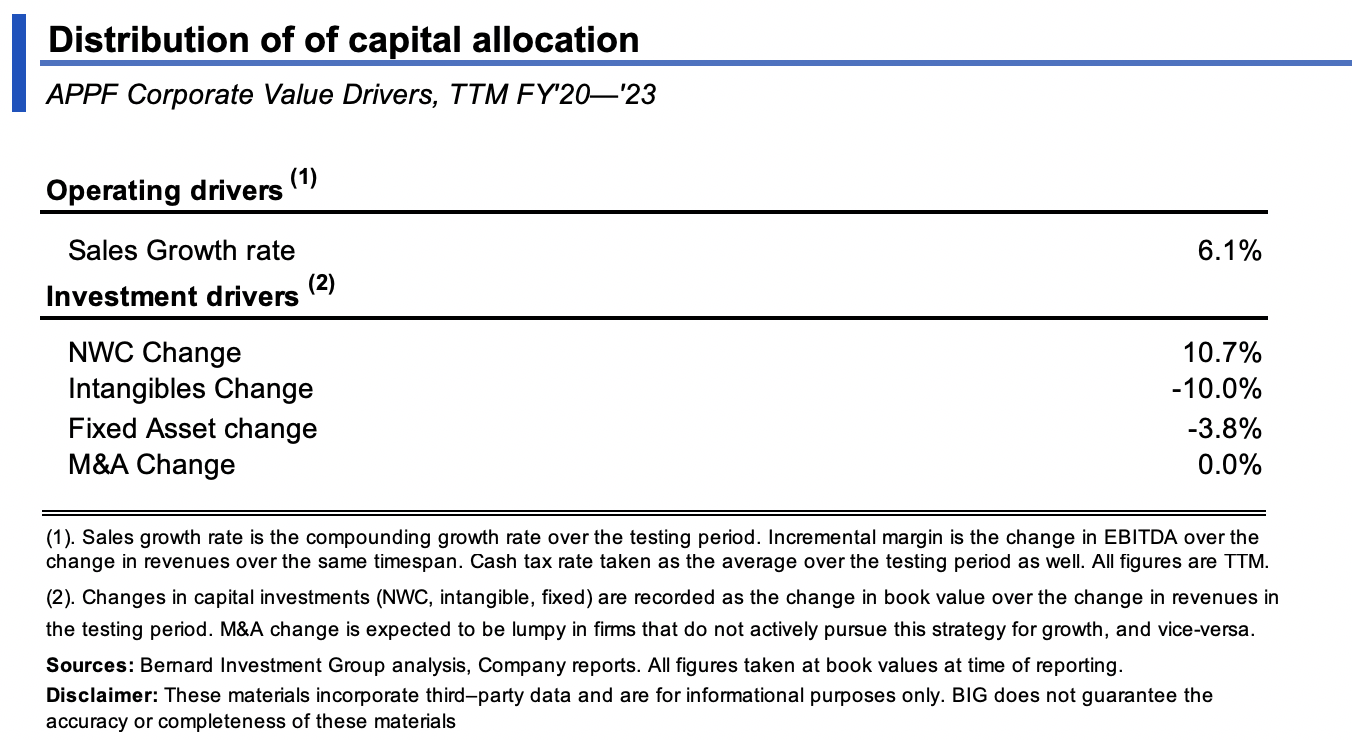

As to the economic value drivers for APPF, our analysis reveals the below findings:

- Since 2020, revenues have compounded at 6.1% per period, which is a strong growth rate.

- Most of the company's capital is tied up in NWC and receivables. To grow sales these last 3 years, APPF required investment mostly in working capital, vs. long-term, fixed capital (fits with the numbers so far).

- For each $1 in sales in the last 3 years, it required a $0.10 investment in NWC to achieve - still relatively small reinvestment requirements.

Each of these points confirms APPF is a low margin, high capital turnover business that produces a high percent of sales for every $1 of investment made into the company. This is a bullish point in the debate.

Figure 4.

{kind=link}

This data provides excellent insights moving forward. If the company were to maintain this steady state of operations, it could do $770mm in revenues by 2024 and $990 by (in line with consensus) and turnover capital invested by 2-2.1x in doing so.

In my opinion, this could see the company compound its intrinsic value at 6-7% per TTM period should it hit these numbers routinely.

Insights from Q3 earnings

For reference, the company posted its Q3 FY'23 numbers on October 26th last year. APPF put up Q3 revenues of $165.4mm, up 32% YoY. Growth was underscored by the company's AppFolio Property Manager platform, now running ~7.8mm total units in Q3 '23. In terms of operational efficiency, the company exited the quarter with 1,683 employees, with the headcount down 4% YoY as planned.

The following points scrutinize the divisional highlights, namely:

- Core Solutions

- Revenues booked were $39.8mm, up 17% YoY. Growth was fuelled by the acquisition of new customers, a rise in total units on the platform, and the continued adoption of AppFolio Property Manager Plus .

- As mentioned, by the end of Q3, the company managed 7.8mm units from 19,418 customers, representing a 7% increase in customers and a 10% increase in ending units from Q3 '22.

- Value Added Services

- APPF did $123mm of business in Q3 in its VAS segment, a 39% YoY growth. Upsides were driven by a combination of factors. Critically, adoption rates of online rent payments were up alongside the higher volume of rental transactions using debit or credit cards.

- This complimented APPF's strategic decision to eliminate eCheck fees, therefore ushering customers to this route of payment. This has not gone unnoticed by the market in my view.

Financials-FCF and outlook

Moving down the P&L, the company booked a loss from operations of $0.1mm, adjusted to $26.7mm or 16.1% of revenue after removing one-off items. It printed adj. free cash flow of $33.6mm, or 20.3% of revenue, versus 9.5% of turnover from the prior year. To me, this is a standout and provides APPF excellent capacity to reinvest this cash flow for growth in 2024 and beyond.

As to the forecasts for FY'24, management are constructive on the company's outlook in a potentially more attractive economic environment. The table below summarizes management's forecasts for the year:

| Financial Metrics | Range |

|---|---|

| 2024 Revenue | |

| $608mm-$612mm | |

| Operating Margin (as % of revenue) | |

| 10.5% to 11.0% | |

| Free Cash Flow Margin (as % of revenue) | |

| 10.5% to 11.5% |

Source: APPF Q3 Earnings Transcript

Valuation and conclusion

The stock trades at 9.8x forward sales and a staggering 20x EV/invested capital. This tells me the market values APPF's operating assets tremendously high and expects strong cash flows/earnings produced off these going forward. Has it overshot the mark here? The question is answered well in the growth prospects going forward. Consensus has 28% growth in sales next year and 66% growth in OCF. Adjusted for growth, you're paying 0.35x sales, a far more reasonable expectation.

We are also comfortable with The Street's sales and earnings forecasts at 9.8x my FY'24 estimates of $770mm in sales this gets me to $211 per share in the base case. I get to $191/share at 9.8x the downside case sales estimate of $700mm. Therefore, valuations included, there is scope to buy APPF to harvest return across all 3 investment horizons (short to long term).

Circling back to the talk on top-down allocation to basic materials in the introduction (which includes the real estate industry)- in my opinion, APPF's positioning in the value chain as a 'value-add' to real estate companies should be looked at positively in this regard. Should those firms running money in property catch a strong bid in '24 + beyond, APPF is well positioned to ride on the laurels of this. I am therefore initiating APPF as a buy for a 1-3 year horizon looking to capture a reversal back to the prevailing uptrend and a price objective of $211 per share. Net-net, rate buy.

For further details see:

AppFolio: Exposure To Real Estate Without Capital-Hungry Growth