APPF - AppFolio's Financial Resilience: Robust Free Cash Flows And Debt-Free Status

2024-01-19 03:29:33 ET

Summary

- AppFolio is expected to grow by +25% CAGR in 2024, propelled by robust free cash flows, a debt-free status, and a substantial $190 million cash reserve.

- AppFolio faces near-term challenges, including a recent 9% team downsizing and a concerning deceleration in total units served adoption, suggesting potential reliance on price increases for revenue growth.

- Despite challenges, AppFolio's financials remain strong, featuring improving free cash flow margins expected to reach around 18% in 2024.

Investment Thesis

AppFolio (APPF) is a real estate technology company that provides innovative tools for property management. They help property managers streamline tasks, enhance communication, and improve overall efficiency in managing rental properties.

The business is growing at a very rapid rate, which I estimate to reach around 25% CAGR in 2024. The investment thesis is not blemish-free. However, given that the business is clearly reporting very strong free cash flows, which are growing, as well as the fact that the business has approximately $190 million of cash on its balance sheet, with no debt, altogether makes this investment compelling.

AppFolio's Near-Term Prospects

AppFolio is a company that works in real estate technology, providing tools and services to make property management more efficient. They help people who manage properties (like apartments or houses) do their job better.

For example, they introduced a new tool called Realm-X, which uses AI to let users talk to AppFolio in regular language. This can help with tasks like getting reports or managing maintenance requests. AppFolio also focuses on improving relationships between property managers, owners, and residents, and they offer features that make processes like leasing and maintenance more streamlined.

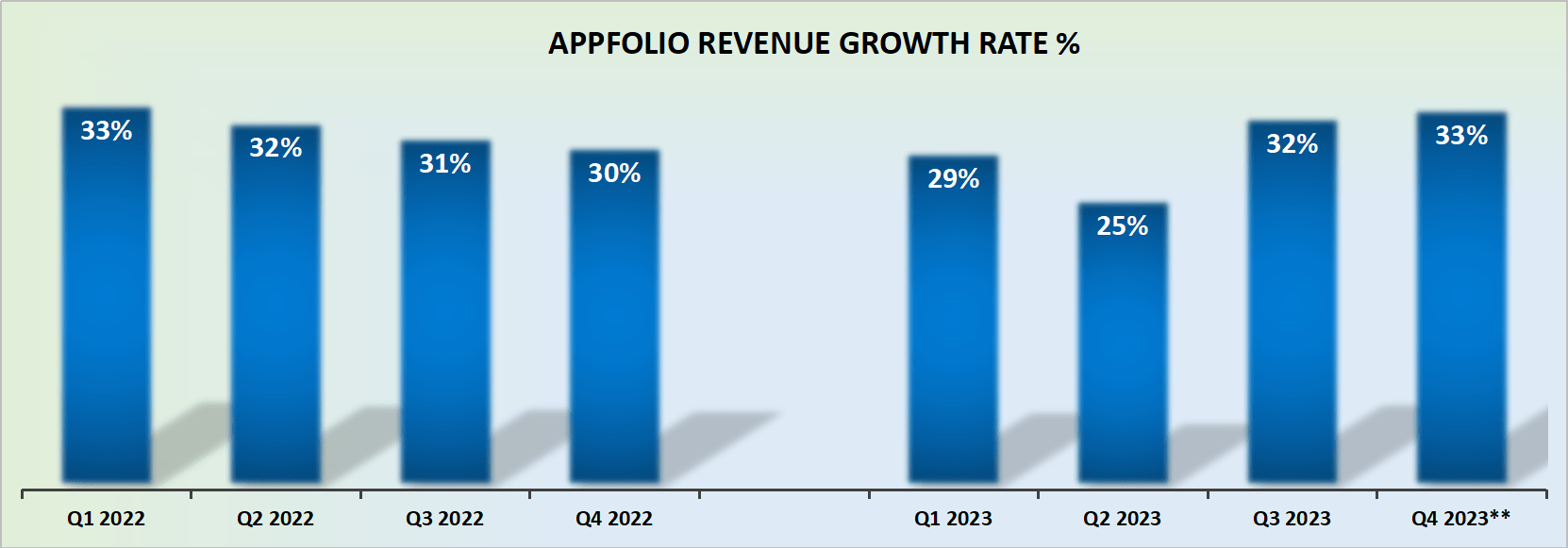

Moving on, AppFolio appears to be in a robust position with promising prospects in the real estate technology industry. The company's third-quarter earnings report reflects a commendable 32% year-over-year growth in revenue to $165 million (more details on its financials to come).

Through Realm-X's interface, users can streamline critical workflows, improve operational efficiency, and enhance customer experience. The strategic pillars of expanding customer relationships, unlocking unit growth, and expanding customer adoption demonstrate a comprehensive approach to sustaining and advancing AppFolio's market position.

However, AppFolio does face some near-term challenges that warrant consideration. One significant hurdle is the recent reduction in the size of their team by nearly 9%. If I'm going to back a high-growth company, I want to see the company increasing headcount, particularly if the stock is priced at a high multiple (discussed more soon).

While this decision was made to better focus on the real estate industry and improve operational efficiency, downsizing can pose challenges in maintaining high-quality service and innovation.

The other key aspect worthwhile noting is illustrated in the following graphic.

APPF presentation

It's not immediately obvious from the graphic above, but what is clear is that AppFolio's total units served are not rapidly increasing. In fact, see if you see a trend in the figures that follow, for the increase in total units served.

- Q3 2022: 18% y/y

- Q4 2022: 16% y/y

- Q1 2023: 14% y/y

- Q2 2023: 13% y/y

- Q3 2023: 10% y/y

What should be obvious from the figures above is that, with time, the units served adoption curve is decelerating.

As a growth investor, I would much rather back a company whose growth is in units (or users), rather than a company that's reliant on price power to increase its revenues. With that in mind, let's discuss its financials.

Revenue Growth Rates Remain Strong

{kind=link}

When AppFolio first guided for 2023, together with its Q4 2022 results, the company guided for $575 million in revenues at the high end. This figure was then steadily increased throughout 2023, with the latest quarter pointing towards $620 million in revenues for 2023.

Consequently, there appears to be a strong likelihood that in 2024 the business will continue to grow at a rapid rate. That being said, as alluded to in the previous section, given that more than half of the revenue growth rates are being driven by an increase in pricing power, I am slightly cautious to extrapolate a 30% CAGR for 2024.

That being said, I believe that something in the ballpark of 25% CAGR appears to be a fair estimate of revenue growth for 2024, which incidentally is practically in line with what analysts also estimate for AppFolio.

APPF Stock Valuation -- Priced at 46x Forward Free Cash Flow

AppFolio has been steadily increasing its underlying free cash flow guidance throughout 2023. At the start of 2023, the best that investors could hope for was 3% free cash flow margins. And this looked more than satisfactory given it would be a solid increase from the 1% free cash flow margins reported in 2021, see below.

{kind=link}

And then, throughout 2023, AppFolio steadily increased its free cash flow margins to around 12% free cash flow margins at the high end (note, only the midpoint shown in the table).

Furthermore, given that Q3 2023 delivered 20% free cash flow margins, this leads one to believe that, without any heroics, 2024 should see AppFolio's free cash flow margins reaching around 18%.

Here's the math. 2023 is guided to approximately 11.5% free cash flow margins at the high end or $67 million of free cash flow for 2023. This means that Q4 most likely points to around $27 million of free cash flow, or 17% free cash flow margins.

Therefore, I believe that in 2024, there's a significant likelihood that AppFolio's free cash flow could reach approximately 18% free cash flow. Hence, assuming that in 2024 AppFolio would grow by approximately at least 25% CAGR, this would see its revenues growing to $765 million.

And from that figure, taking the 18% free cash flow margins forward to 2024, would see around $140 million of free cash flow. This would leave the stock priced at 46x forward free cash flow.

That is a multiple that strikes me as fair. It's not the most attractive stock in the stock market, but given that it's still early days for this business, there's the potential for even more upside, with more free cash flow in the ensuing years beyond 2024.

The Bottom Line

In conclusion, AppFolio's investment thesis seems compelling, driven by its rapid revenue growth and strong free cash flows, coupled with a debt-free balance sheet and a substantial cash reserve of around $190 million.

A noteworthy concern is the decelerating trend in the adoption of total units served, suggesting a potential reliance on price increases rather than user expansion for revenue growth.

Despite these challenges, AppFolio's financials showcase robust revenue growth rates, with an estimated 25% CAGR in 2024, and improving free cash flow margins reaching around 18%.

The stock's valuation at 46x forward free cash flow appears fair, considering the business's growth potential and early-stage development, leaving room for further upside in the coming years beyond 2024.

Altogether, I'm bullish on the stock's prospects.

For further details see:

AppFolio's Financial Resilience: Robust Free Cash Flows And Debt-Free Status