APPN - Appian Corporation: Navigating Challenging Growth Landscape With Promising Potential

2023-07-14 05:29:55 ET

Summary

- APPN continues to exceed its guidance expectations and achieved 18% increase in total revenue. The migration to cloud also remains strong.

- Macroeconomic slowdown has some pressure on the growth rate and cloud retention rate.

- APPN's product will still be in demand given its big value proposition to its customers.

- However, APPN is only one of the players in the industry. I don't see how it can surely dominate its competition.

- The stock is fairly valued, but worth keeping a close watch.

Appian Corporation (APPN) is a leading automation SaaS platform that provides immense value to its customers by serving as their software infrastructure. The company has demonstrated a track record of stable revenues and profitability. However, despite a significant drop of 75% from its all-time highs, the current valuation of APPN does not appear to present a compelling bargain. The future outlook for APPN has become less certain, raising questions about the company's growth trajectory and potential challenges ahead.

Business upgrade

APPN's financial performance exceeded expectations. The company achieved an 18% increase in total revenue 132.5M, with subscription revenue accounting for 73% of the total in Q1 2023. The cloud subscription revenue retention rate reached an impressive 115%, surpassing the target range of 110% to 120%. Additionally, the gross margin improved to 75% from 74% in the previous year. Share count only saw a minimal increase of 0.2 million, minimizing shareholder value dilution.

In terms of business development, APPN demonstrated significant progress by doubling their new seven-figure deals compared to the previous year. The company also made strides in the US public sector, obtaining state ramp certification for their cloud platform, which enhances their chances of winning sensitive government contracts. Additionally, APPN has developed contract writing and constituent case management functionalities.

During the earnings call , the management also highlighted the adoption of artificial intelligence ((AI)) in their tools. They emphasized the importance of low-code AI, which allows customers to leverage AI capabilities using Appian's datasets. As Appian respects customer data privacy, they can assemble customized datasets and train AI models specifically for individual customers. An early example of this application includes a leading European automotive manufacturer utilizing AI functionality to process warranty claims. While this AI push seems to bring APPN lots of leverage to grow its business, I don't think it sets APPN apart from competitors as all others are also using AI. It is more like a catch-up move to me.

Pressure from the macroeconomic slowdown

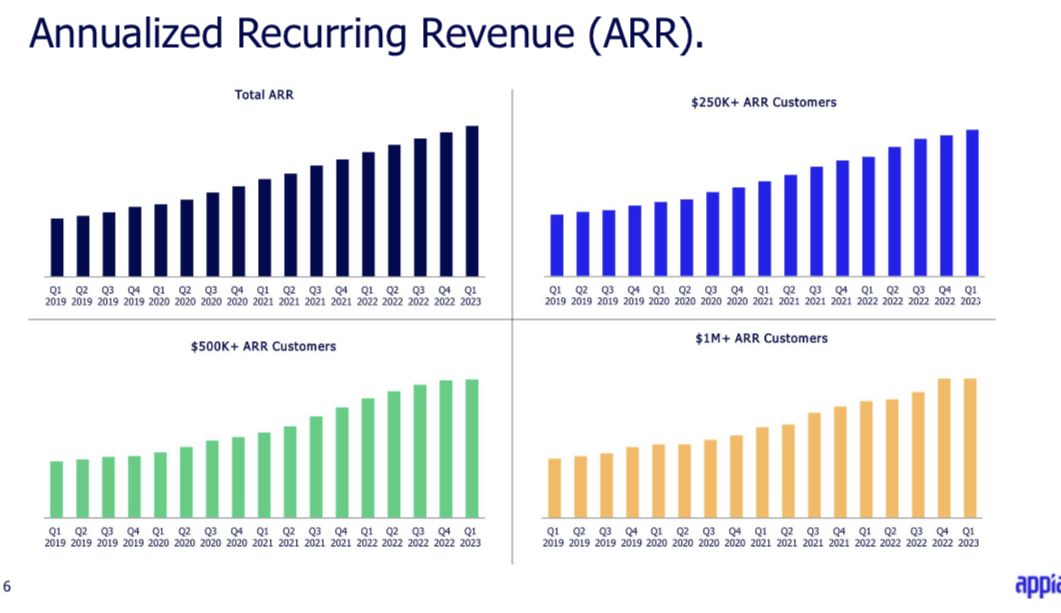

Like other SaaS companies, APPN is also facing pressure to secure large and fast deals as customers are becoming more cautious in their commitments. The cloud retention rate has decreased to 105% compared to last year's 107%. Additionally, the growth of customers with large deals (500k+ and 1M+) has clearly plateaued (chart below), although the overall customer growth remains healthy. I think APPN's product is still well-received by the market, and the company will continue to grow. However, it is experiencing some weakening.

APPN user growth (APPN presentation)

{kind=link}

APPN product offers real value to customers

APPN is a powerful platform that enables organizations to streamline their business processes and deliver exceptional customer experiences. Their unified platform offers a comprehensive set of tools for data management, process automation, total experience, and process optimization. This enables data-driven decision-making, enhances customer experiences, and optimizes processes for maximum efficiency and effectiveness. The focus on low or no-code solutions allows for easier and faster development, with simple drag-and-drop functionality. Additionally, the APPN cloud eliminates the need for server administration and support, making it a cost-effective and convenient choice for businesses. In a time when skilled developers are in high demand, APPN's value proposition is particularly appealing for businesses looking to digitize their operations which should offer APPN a long runway ahead.

Competition is a concern moving forward

Moving forward, a key concern for APPN is its ability to defend its business against growing competition. The market is seeing an influx of competitors entering the space, which poses a challenge for APPN.

One area where APPN faces limitations is customization. It may struggle with advanced or large-scale implementations, often catering to internal applications or processes that citizen developers can handle without the need for expensive developer teams. This leaves APPN vulnerable to competitors offering more extensive customization options. Notable players such as UiPath (PATH), Camunda, Pega, and Bizagi are expanding into APPN's major strongholds in industries like finance, government, and insurance. Even established companies like Salesforce (CRM) and ServiceNow (NOW) are venturing into this space. Microsoft's Power Automate platform has also gained significant momentum lately.

Corporate politics and existing technical environments can act as barriers to further penetration for APPN. Some customers prefer sticking to a single vendor they are accustomed to, which makes it challenging for APPN to gain traction unless its toolsets offer significant advantages over competitors.

Furthermore, while APPN's focus on process automation and the integration of data and AI is promising, there is a risk of overinvestment in this area. The market for process automation is highly competitive, with strong players like UiPath and Microsoft (MSFT) having more resources and experience. To succeed, APPN must differentiate itself clearly and effectively articulate the unique value it brings to customers.

Price actions

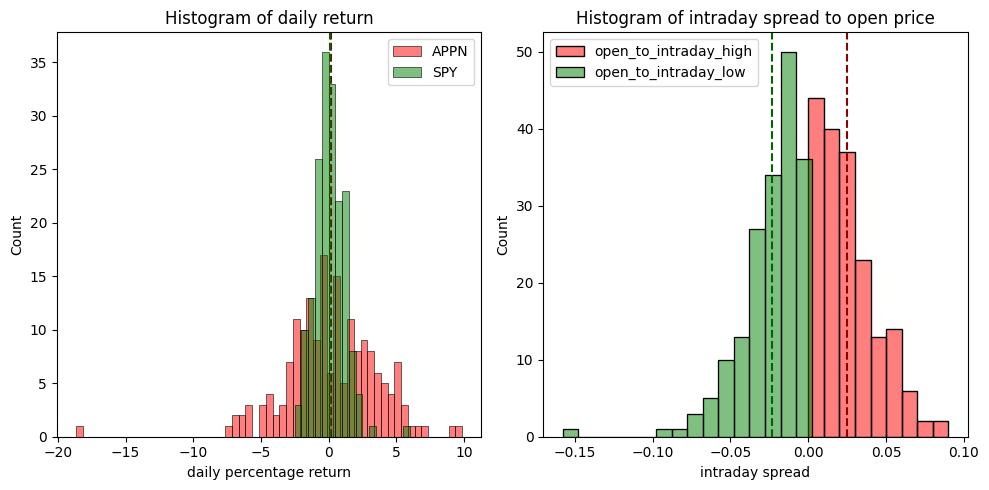

When it comes to price movements, the chart below shows the price action characteristics between 2022-10-17 to 2023-07-10. APPN showed wider daily return fluctuations than the market average, with a standard deviation of about 3x of SP500. Most days have positive returns. The stock often traded in an intraday range, with most times dropping or raising 3% from the open price. When shocking good/bad news comes, you could see one day raise/fall for 8%+. There was one time it dropped 15% in a day from the open.

{kind=link}

If we calculate the correlation ratio of APPN prices to all major sector ETFs, APPN's trading is mostly correlated with sectors like Consumer Discretionary ( XLY ), Technology ( XLK ), Semiconductor ( SMH ), etc. Especially, Consumer Discretionary ( XLY ) has a correlation ratio of 0.76 with APPN.

Sector correlation (Author)

Bottom line

Moving forward, APPN aims to increase cloud subscription revenue to between 296 to 298M indicating a YOY growth of 25%. For full year total revenue, APPN aims for 530M to 535M,Representing a 13% growth. The company is also expecting to turn profitable from Adjusted EBITA loss to be around 70M. While I believe APPN is definitely capable to hit this guidance, the current EV 3.69B seems fairly valued. My major concern is still about the competition and new entrant coming to the industry. APPN's all-in push to process automation also adds little uncertainty. It is also trading at slightly higher EV/sales multiple with UiPath which I felt has better qualities.

APPN has set targets to achieve a robust 25% year-over-year growth for full-year cloud subscription revenue being $296 million to $298 million. Total revenue guidance is $530 million to $535 million, representing a growth rate of 13%. Furthermore, the company anticipates a shift to profitability, with an expected Adjusted EBITA of around $70 million. While I have confidence in APPN's ability to meet these targets, certain factors warrant consideration. Competition and the entry of new players into the industry pose challenges that cannot be ignored. Additionally, APPN's all-in push toward process automation introduces an element of uncertainty. It is worth noting that the current enterprise value (EV) of $3.69 billion appears to be fairly valued, but it is essential to acknowledge the slightly higher EV/sales multiple in comparison to UiPath, a competitor that is perceived to possess stronger qualities.

For further details see:

Appian Corporation: Navigating Challenging Growth Landscape With Promising Potential