APPN - Appian Expects Slowing Growth But Private AI Opportunity Beckons

2023-05-11 11:40:07 ET

Summary

- Appian recently reported its Q1 2023 financial results.

- The firm provides low-code process automation software technologies to organizations worldwide.

- APPN has guided 2023 revenue growth to be substantially lower than 2022's growth rate and operating losses remain large.

- I'm Neutral [Hold] on Appian until growth can improve and operating losses are substantially reduced.

A Quick Take On Appian

Appian ( APPN ) reported its Q1 2023 financial results on May 9, 2023, beating revenue and EPS consensus estimates.

The firm provides low-code software for organizations to automate various aspects of their operations.

While I’m encouraged by the firm’s growth potential in the U.S. public sector, dealing with public agencies and their bidding processes can be a time-consuming and ‘lumpy’ endeavor.

Until leadership makes a serious move toward operating breakeven and growth improves, I’m Neutral [Hold] on APPN.

Appian Overview

McLean, Virginia-based Appian was founded in 1999 to provide a low-code development platform for organizations of all sizes to implement process automation and optimization capabilities.

The firm is headed by founder and CEO Matthew Calkins, who was previously Director, Enterprise Product Group at MicroStrategy ( MSTR ).

The company’s primary process automation offerings are focused on the industry verticals of financial services, insurance, government and life sciences companies.

Appian acquires customers through its direct sales and marketing efforts and through a robust partner program that includes education, reseller, services, technology and public sector partners.

Appian’s Market & Competition

According to a 2023 market research report by Grand View Research, the global market for robotic process automation was estimated to reach $30.9 billion by 2030.

This represents a forecasted high CAGR (Compound Annual Growth Rate) of 39.9% from 2023 to 2030.

The main drivers for this expected growth are the increasing demand for greater efficiencies by organizations of all sizes and types and the reduction in complexity of business operational tasks.

Also, major industries affected by RPA innovation include:

-

BFSI

-

Healthcare and Pharma

-

Retail

-

IT and Telecom

-

Communication & Media

-

Manufacturing

-

Logistics

-

Energy & Utilities

Major competitive or other industry participants include:

-

Automation Anywhere

-

Blue Prism

-

EdgeVerve Systems

-

FPT Software

-

KOFAX

-

NICE

-

NTT Advanced Technology

-

OnviSource

-

Pegasystems

-

UiPath

Appian’s Recent Financial Trends

-

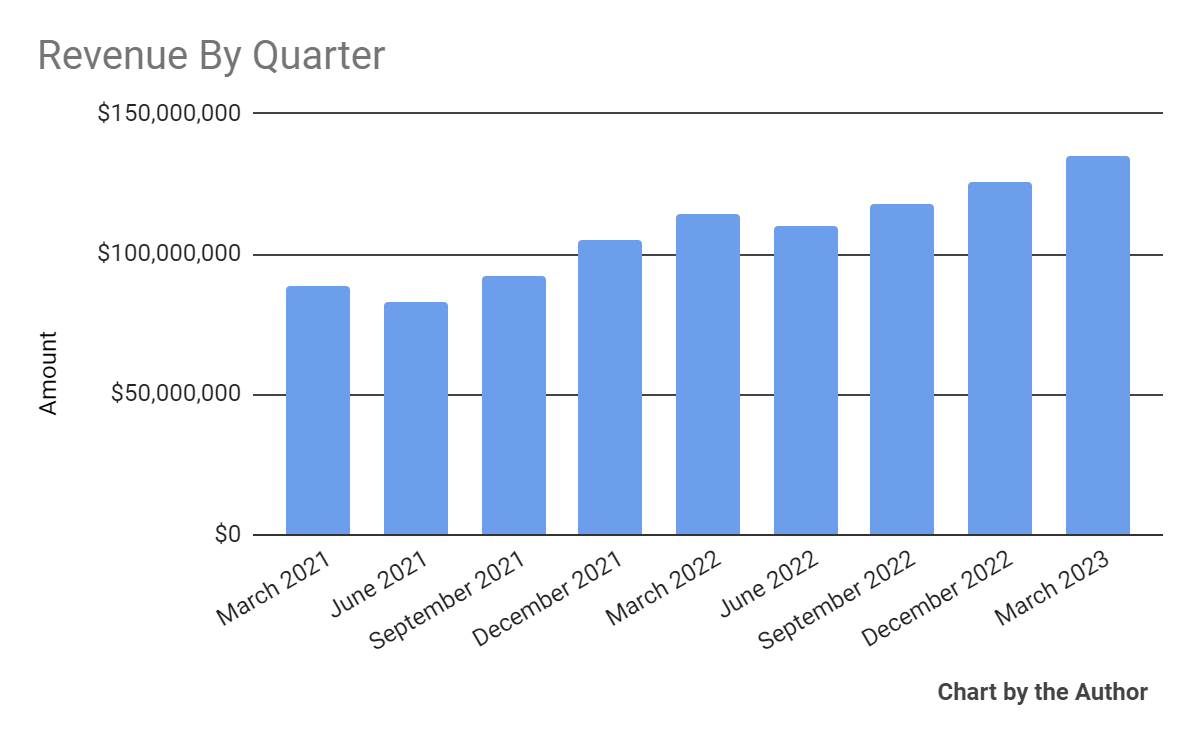

Total revenue by quarter has grown revenue per the following chart:

{kind=link}

-

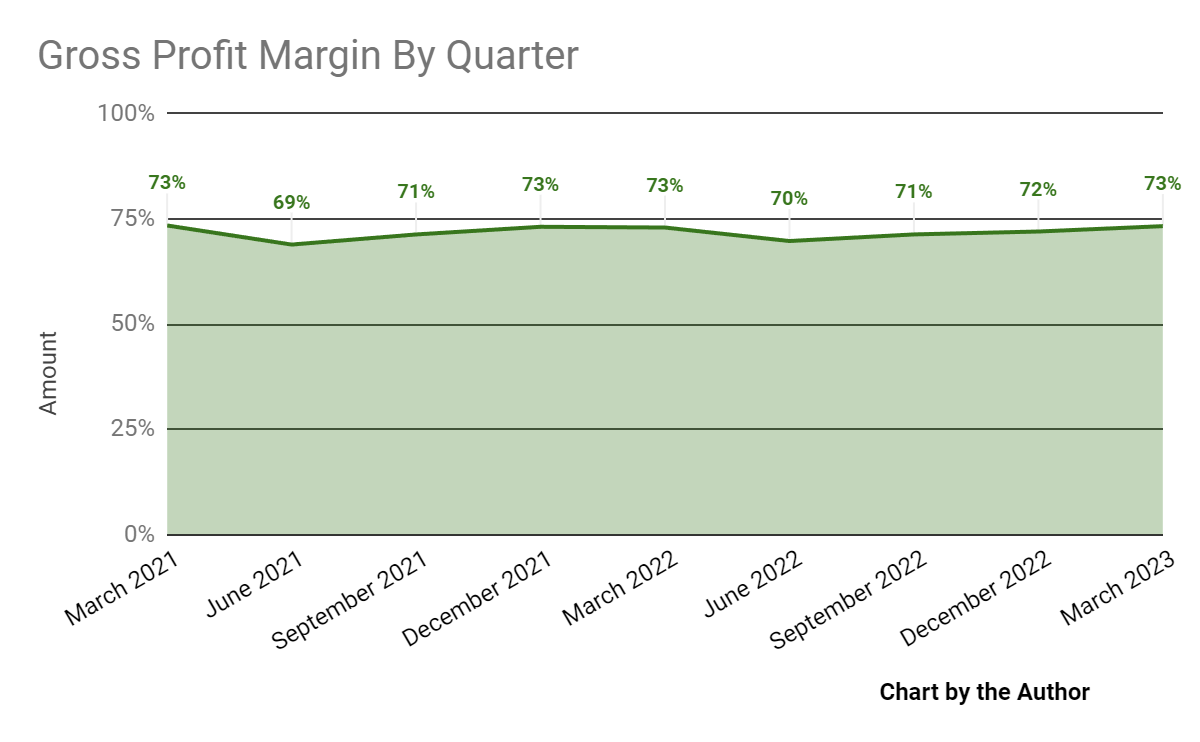

Gross profit margin by quarter has fluctuated within a narrow range:

Gross Profit Margin (Seeking Alpha)

{kind=link}

-

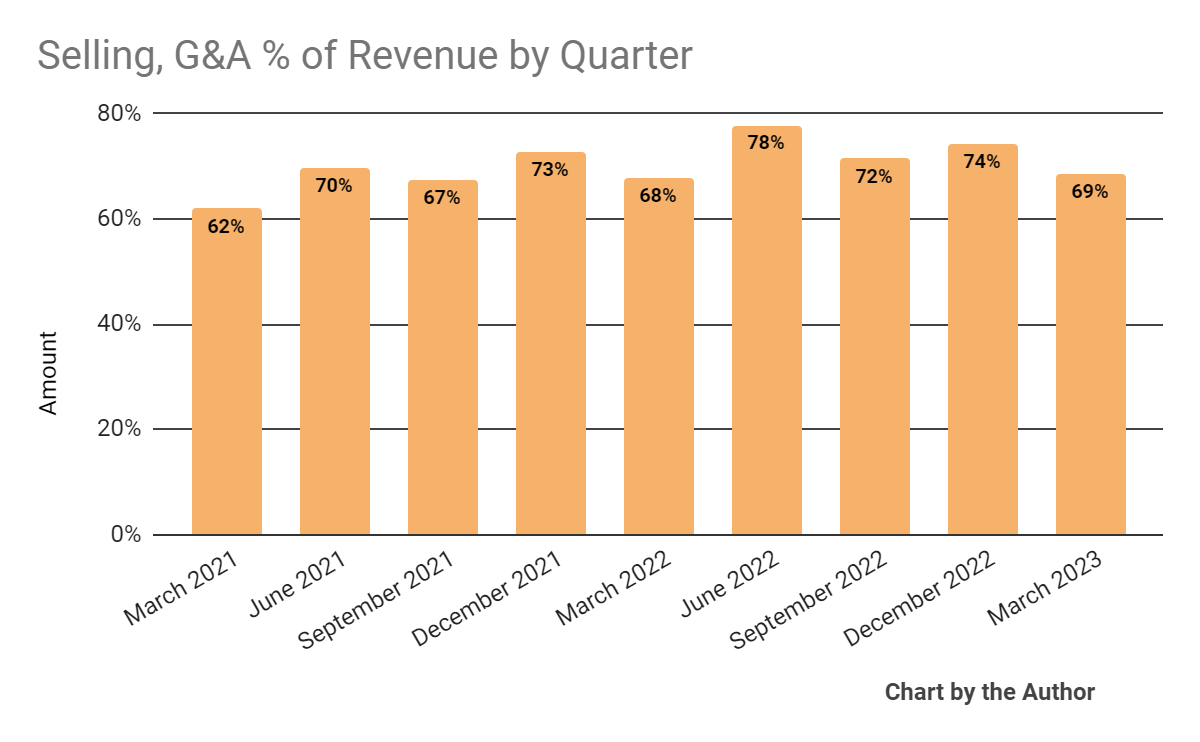

Selling, G&A expenses as a percentage of total revenue by quarter have trended higher in recent quarters:

Selling, G&A % Of Revenue (Seeking Alpha)

{kind=link}

-

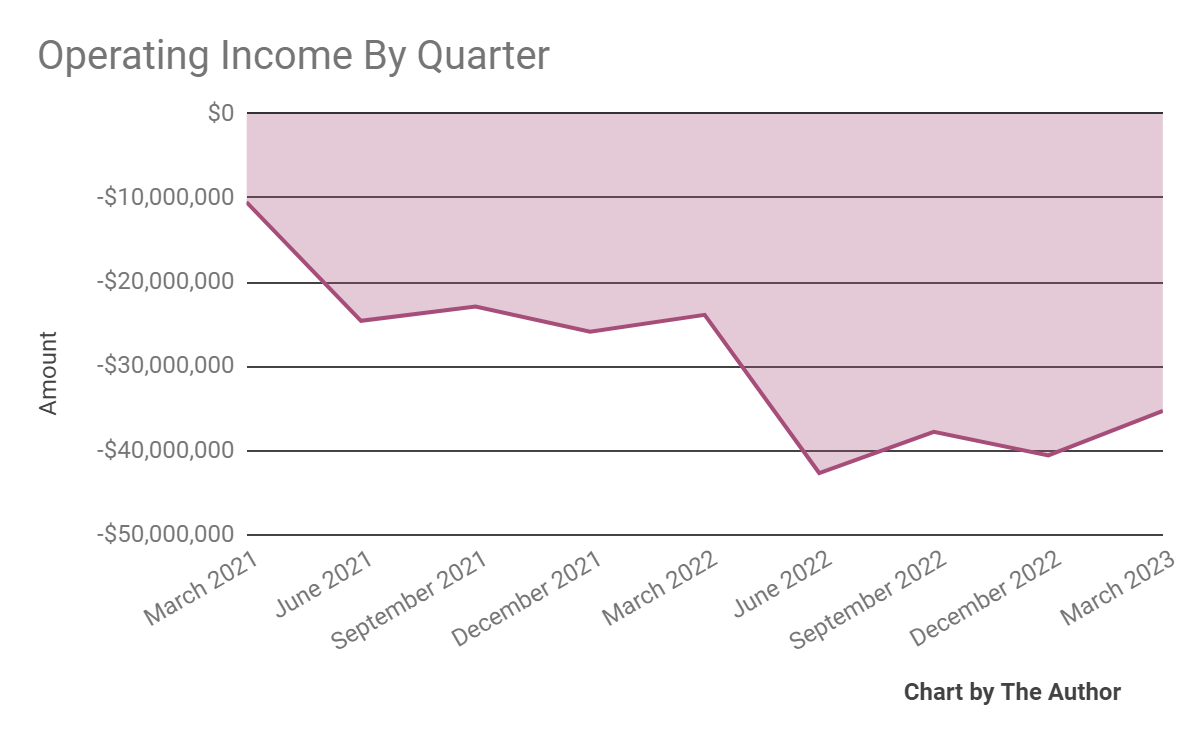

Operating losses by quarter have worsened further in recent quarters:

Operating Income (Seeking Alpha)

{kind=link}

-

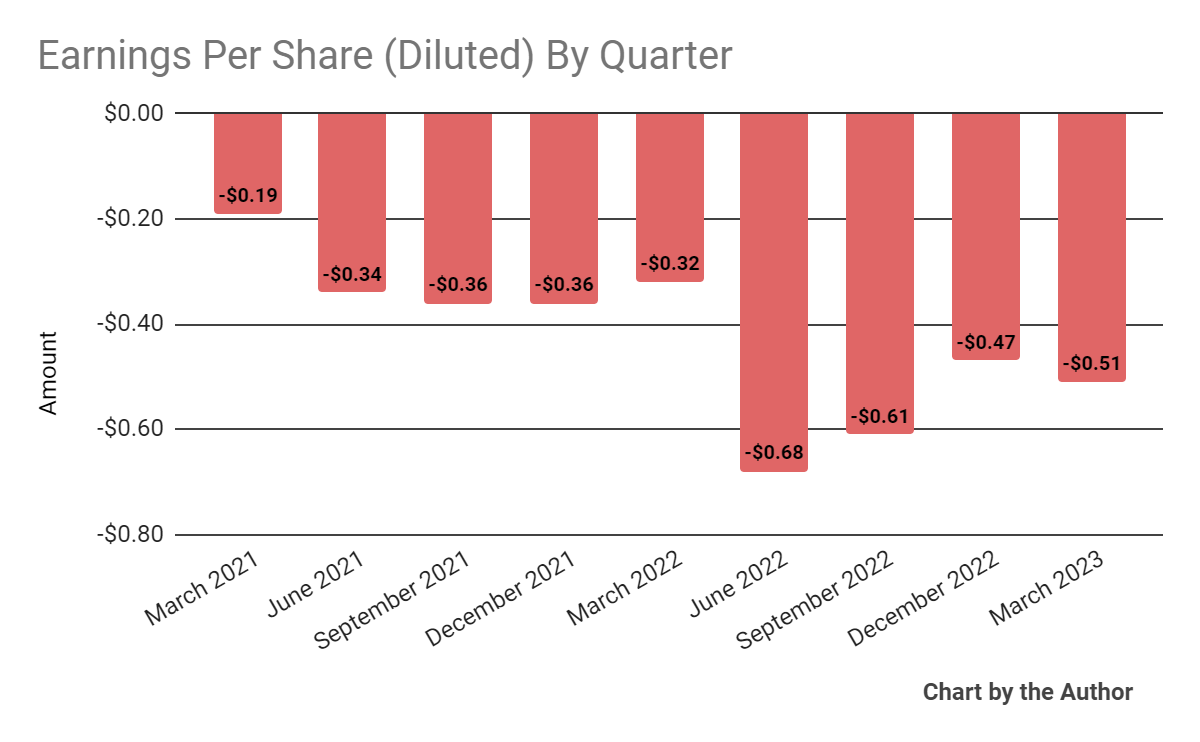

Earnings per share (Diluted) have remained heavily negative, as the chart shows below:

Earnings Per Share (Seeking Alpha)

{kind=link}

(All data in the above charts is GAAP)

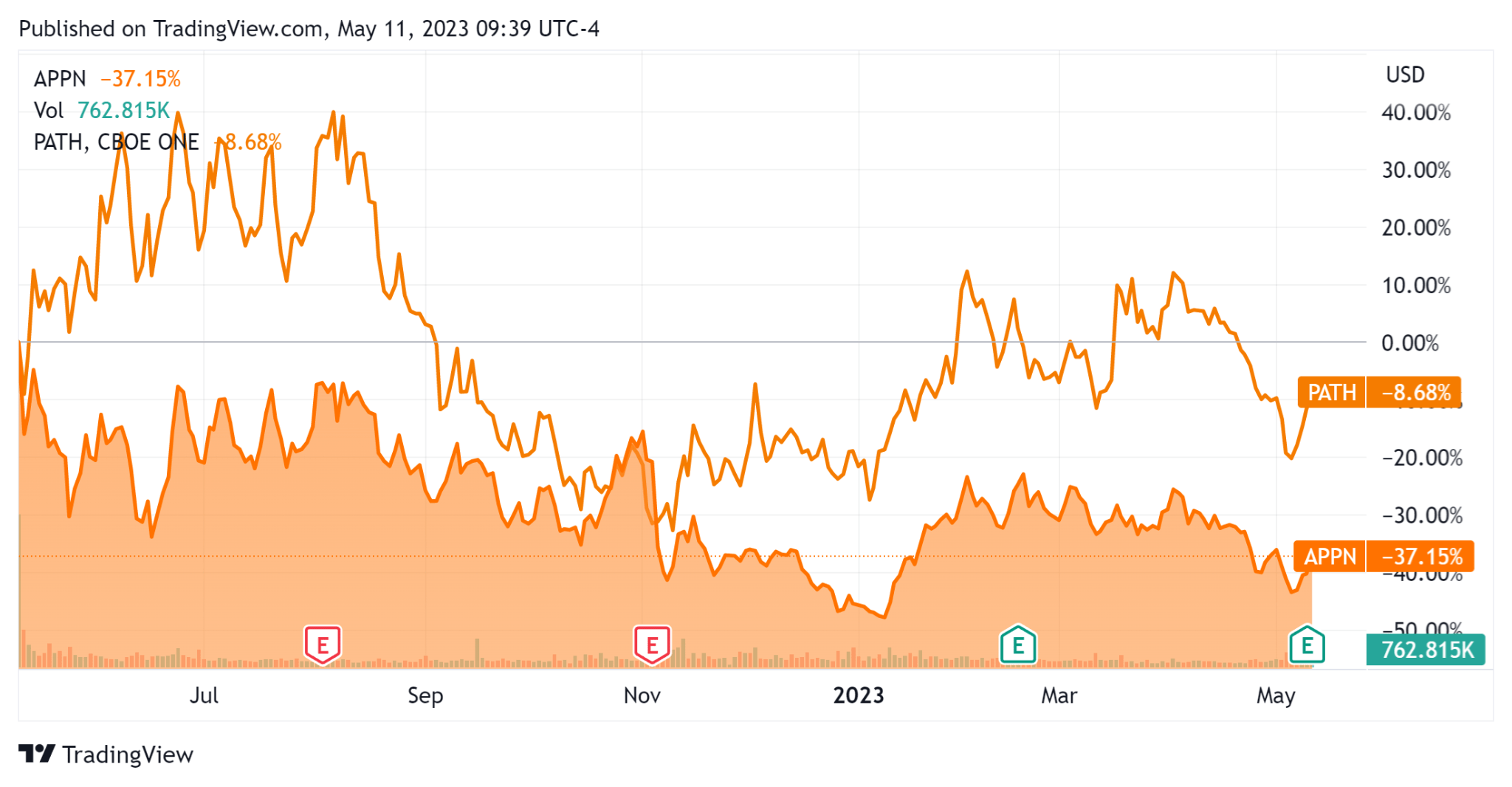

In the past 12 months, APPN’s stock price has fallen 37.15% vs. that of UiPath’s ( PATH ) drop of only 8.68%, as the chart indicates below:

52-Week Stock Price Comparison (Seeking Alpha)

{kind=link}

For the balance sheet, the firm ended the quarter with $254.5 million in cash, equivalents and short-term investments and $209.1 million in total debt, of which $65.4 million was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash used was $121.3 million, of which capital expenditures accounted for $10.1 million. The company paid $42.9 million in stock-based compensation in the last four quarters, the highest figure in the last eleven quarters.

Valuation And Other Metrics For Appian

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 5.5 |

| Enterprise Value / EBITDA |

| NM |

| Price / Sales |

| 5.5 |

| Revenue Growth Rate |

| 26.7% |

| Net Income Margin |

| -32.3% |

| EBITDA % |

| -29.4% |

| Market Capitalization |

| $2,600,000,000 |

| Enterprise Value |

| $2,590,000,000 |

| Operating Cash Flow |

| -$106,550,000 |

| Earnings Per Share (Fully Diluted) |

| -$2.27 |

(Source - Seeking Alpha)

As a reference, a relevant partial public comparable would be UiPath; shown below is a comparison of their primary valuation metrics:

| Metric [TTM] |

| UiPath |

| Appian |

| Variance |

| Enterprise Value / Sales |

| 6.0 |

| 5.5 |

| -7.5% |

| Enterprise Value / EBITDA |

| NM |

| NM |

| --% |

| Revenue Growth Rate |

| 18.6% |

| 26.7% |

| 43.5% |

| Net Income Margin |

| -31.0% |

| -32.3% |

| 4.0% |

| Operating Cash Flow |

| -$9,980,000 |

| -$106,550,000 |

| 967.6% |

(Source - Seeking Alpha)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

APPN’s most recent Rule of 40 calculation was negative (2.7%) as of Q1 2023’s results, so the firm has performed poorly in this regard, per the table below:

| Rule of 40 Performance |

| Calculation |

| Recent Rev. Growth % |

| 26.7% |

| EBITDA % |

| -29.4% |

| Total |

| -2.7% |

(Source - Seeking Alpha)

Commentary On Appian

In its last earnings call (Source - Seeking Alpha), covering Q1 2023’s results, management highlighted its confidence in ‘private AI’ clouds, as companies wish to keep their proprietary data for competitive and regulatory reasons.

As a result, the company is investing resources in developing ‘low code AI’ for customers using its Data Fabric functionality and calling it “Process HQ”. The service is planned for beta testing in Q2 2023.

Notably, Appian is seeing strong growth from the U.S. public sector for its automation technologies and the company has launched two new solutions, ‘contract writing for federal and constituent case management for state and local.’

Total revenue for Q1 2023 was 18.3% higher than the same period in 2022 and gross profit margin increased 0.3 percentage points.

The company’s cloud subscription revenue retention rate was 115%, indicating reasonably good product/market fit and sales & marketing efficiency.

SG&A as a percentage of revenue rose by 0.9 percentage points year-over-year and operating losses increased by 47.7%.

Looking ahead, management is focused on 2023 using a ‘growth with scrutiny’ approach as it seeks to exert greater effort in evaluating its various investment programs.

For 2023, management guided topline revenue growth to 14.5% at the midpoint of the range and non-GAAP net loss to around $1.12 at the midpoint.

If achieved, this growth rate would be significantly lower than 2022’s 26.7% growth rate over 2021.

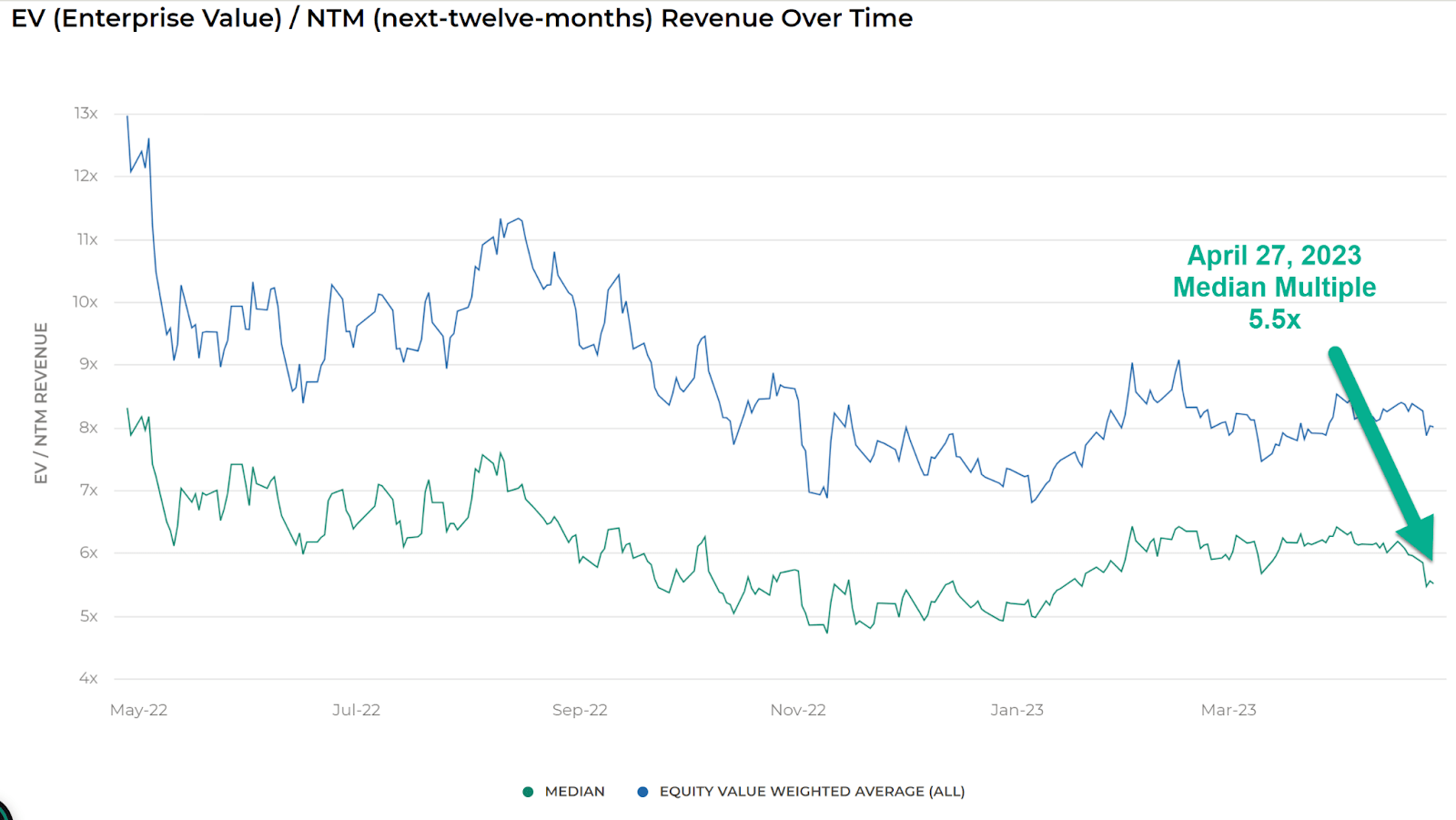

Regarding valuation, the market is valuing APPN at an EV/Sales multiple of around 5.5x.

The Meritech Capital Index of publicly held SaaS software companies showed an average forward EV/Revenue multiple of around 5.5x on April 27, 2023, as the chart shows here:

EV/Next 12 Month Revenue Multiple Index (Meritech Capital)

{kind=link}

So, by comparison, APPN is currently valued by the market at equal to the broader Meritech Capital SaaS Index, at least as of April 27, 2023, likely due to its robust revenue growth performance.

The primary risk to the company’s outlook is a macroeconomic slowdown that appears to be already underway and tightening credit conditions which may delay, reduce or prevent customer and prospective customer spending plans.

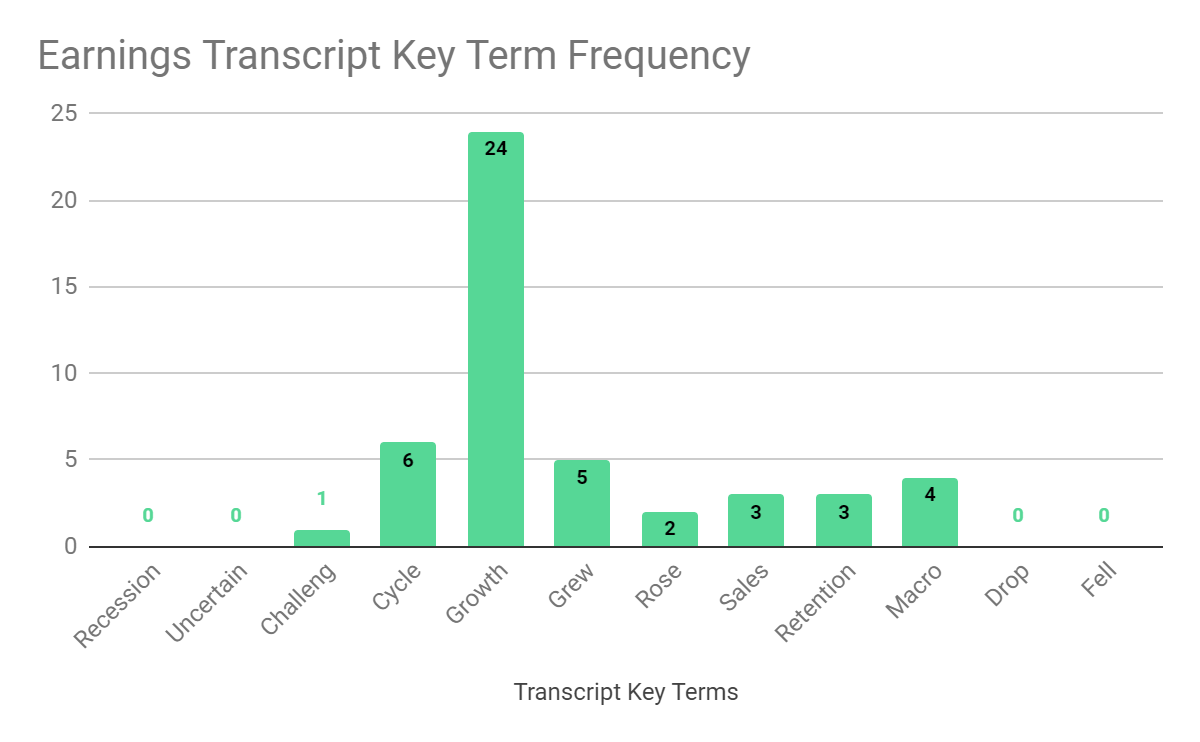

From management’s most recent earnings call, I prepared a chart showing the frequency of key terms mentioned (or not) in the call, as shown below:

Earnings Transcript Key Term Frequency (Seeking Alpha)

{kind=link}

I’m most interested in the frequency of potentially negative terms, so management cited ‘Challeng[es][ing]’ once and ‘Macro’ four times in various contexts.

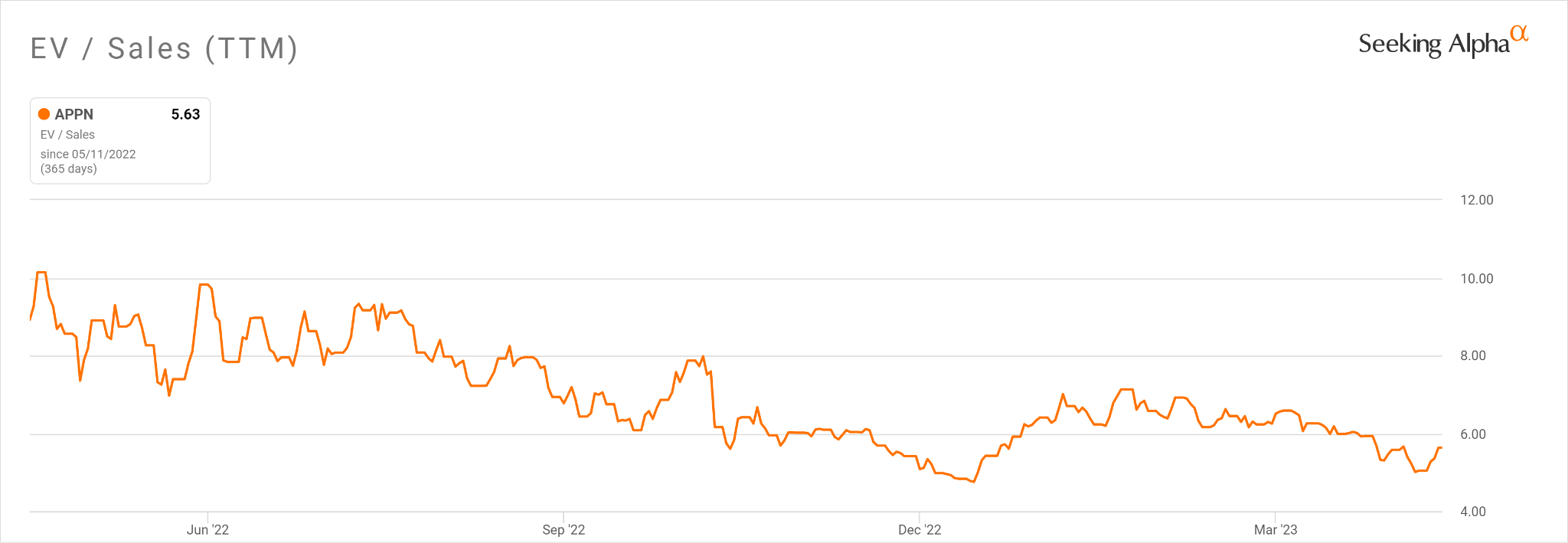

In the past twelve months, the firm's EV/Sales valuation multiple has compressed by 37%, as the chart from Seeking Alpha shows below:

EV/Sales Multiple History (Seeking Alpha)

{kind=link}

A potential upside catalyst to the stock could include the end of U.S. Federal Reserve interest rate hikes, reducing downward pressure on its stock valuation multiples.

While I’m encouraged by the firm’s growth potential in the U.S. public sector, dealing with public agencies and their bidding processes can be a time-consuming and ‘lumpy’ endeavor.

Until leadership makes a serious move toward operating breakeven and growth improves, I’m Neutral [Hold] on APPN.

For further details see:

Appian Expects Slowing Growth But Private AI Opportunity Beckons