APPN - Appian: Growth Is Nice But Profits Will Need To Show Up Soon

2023-11-02 07:08:14 ET

Summary

- Appian Corporation operates a process automation platform that offers a fully integrated solution for workflow, artificial intelligence, process automation, and process mining.

- The company has a high renewal rate of 99% for its cloud business, indicating customer satisfaction and potential for continued growth.

- Appian is experiencing rapid revenue and gross profit growth, but has not yet achieved profitability, which has led to a decline in its stock price.

- If the company can show a path to profitability, it can offer a lot of upside to investors.

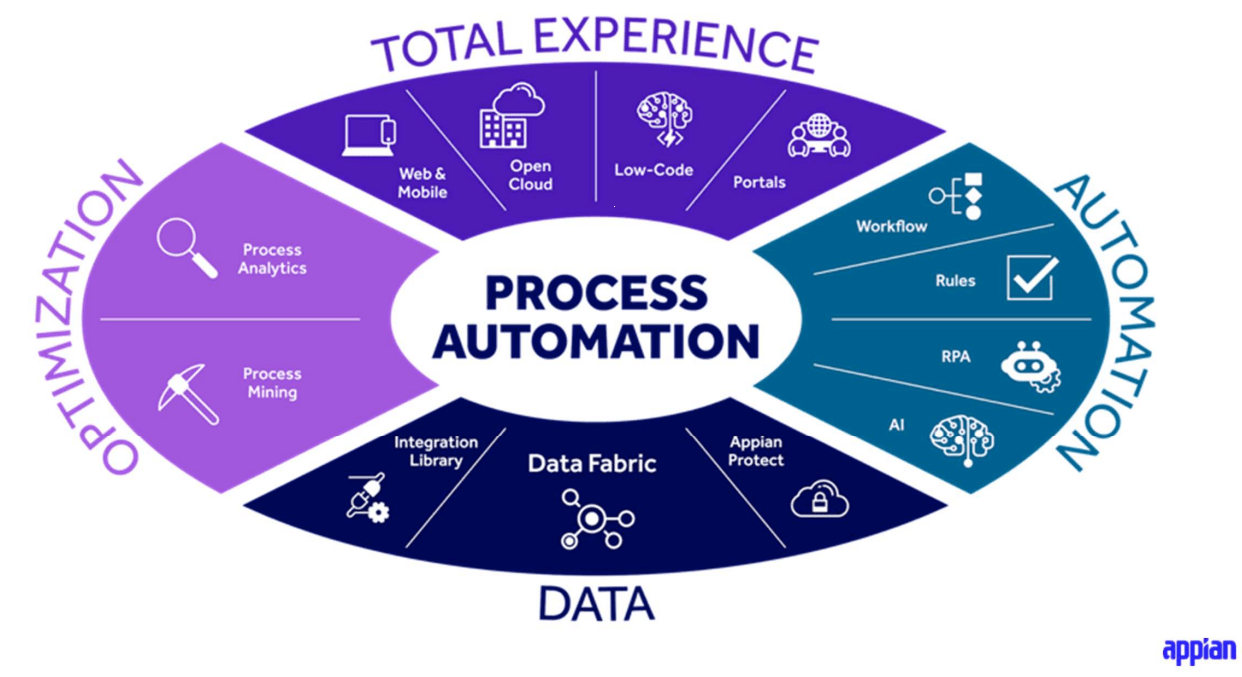

Appian Corporation ( APPN ) operates a process automation platform with a goal of driving efficiency and improving digital innovation in its customers by transforming the way they work. Some of the processes included in the company's platform include artificial intelligence, robotic process automation, data mining, process mining and workflow. Although the company hasn't made any profits so far, it has an impressive growth story which could pave the road to profitability down the line if the company plays its cards correctly.

There are a few strengths to the company and its products. First, there are many platforms that offer services such as Workflow, Artificial Intelligence, Process Automation and Process Mining but very few solutions that offer these all in one place in a fully integrated manner. Appian allows a platform where customers can access multiple packages and services all in the same place. Second, Appian allows customization with minimal amount of heavy coding and minimal amount of adjustments so that customers don't have to struggle hard to fit their business practices into a platform they purchased and they can start working on their optimization projects almost right away after switching to Appian's platform. Often times, companies will spend a lot of time, money and resources in purchasing a platform just to find out that the platform doesn't work well with the company's existing platforms such as its data sources and it will be a total waste of money or time but Appian's solutions seem to be very flexible and easy to integrate with any existing solutions a company is already using.

Today we are witnessing a huge shift in the way companies do business and many people call this a new industrial revolution. In almost every industry there is a shift towards automation, optimization, doing more with less and using resources more effectively. This shift is going to take a long time to fully implement and isn't likely to go away anytime soon. In fact automation in production facilities started as early as 1960s and took off in places like Japan in 1970s and western world in 1980s. This is nothing new and it's been going on for decades but now we can start automizing not only simple repetitive tasks but also more complicated and more challenging tasks because AI, machine learning and our tools got much better over time and they will keep getting better for decades to come.

If Appian plays its cards correctly, the company could benefit from this multi-decade shift as an end-to-end process automation solution that is fully integrated.

{kind=link}

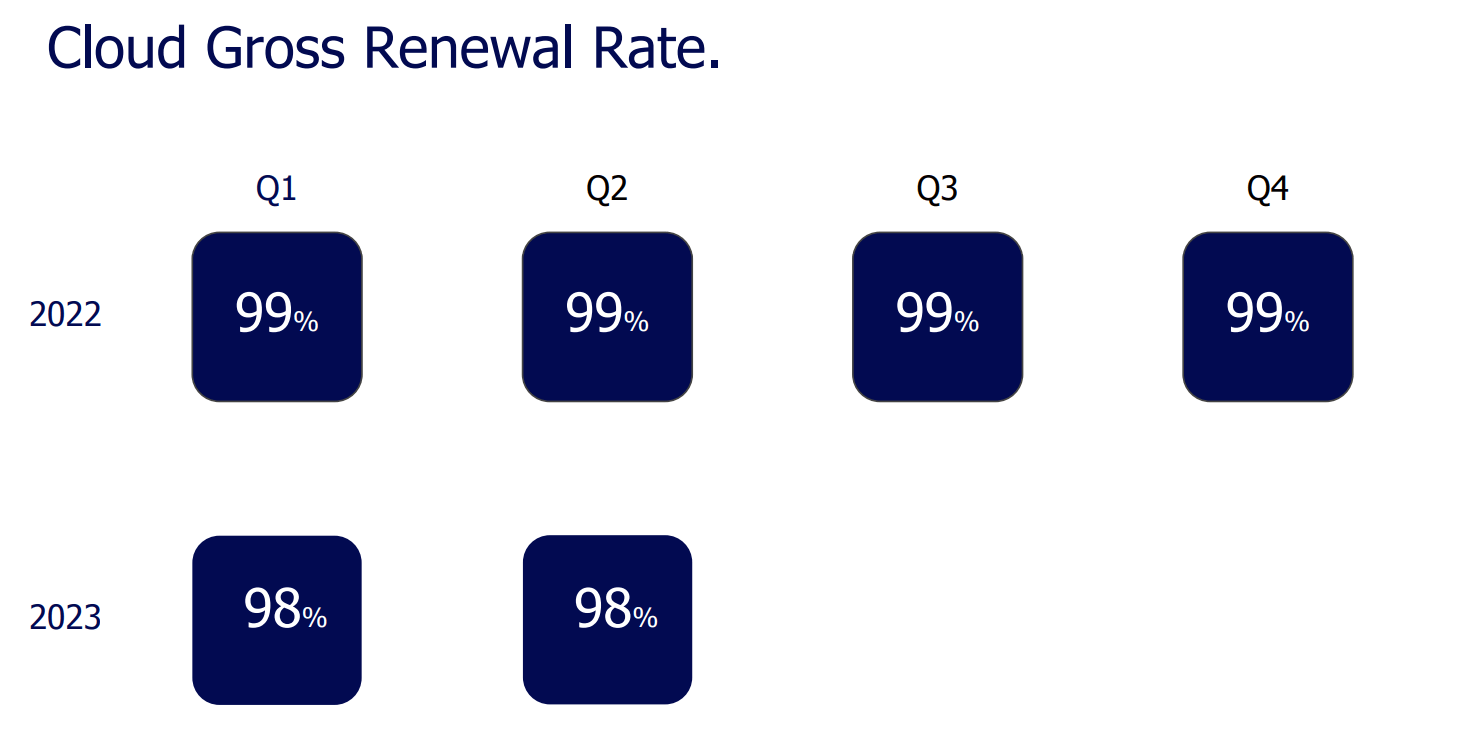

One of the things I find most impressive about this company is their exceptionally high renewal rates for its cloud business. In the last 6 quarters the company boasted an average renewal rate of 99%. In fact there have been only 2 quarters where it fell below 99% and those were still high at 98%. Part of this could be because the company's platform offers a lot of value to customers but another part could also be because once a company makes a heavy investment into a new platform (whether it be money, time or other resources) it is very difficult for them to walk away because it would take additional time and resource commitment. Companies tend to stay with their committed platforms for a long time unless something breaks or gets disrupted. In either case, the company is enjoying a nice renewal rate which can help fuel its growth.

{kind=link}

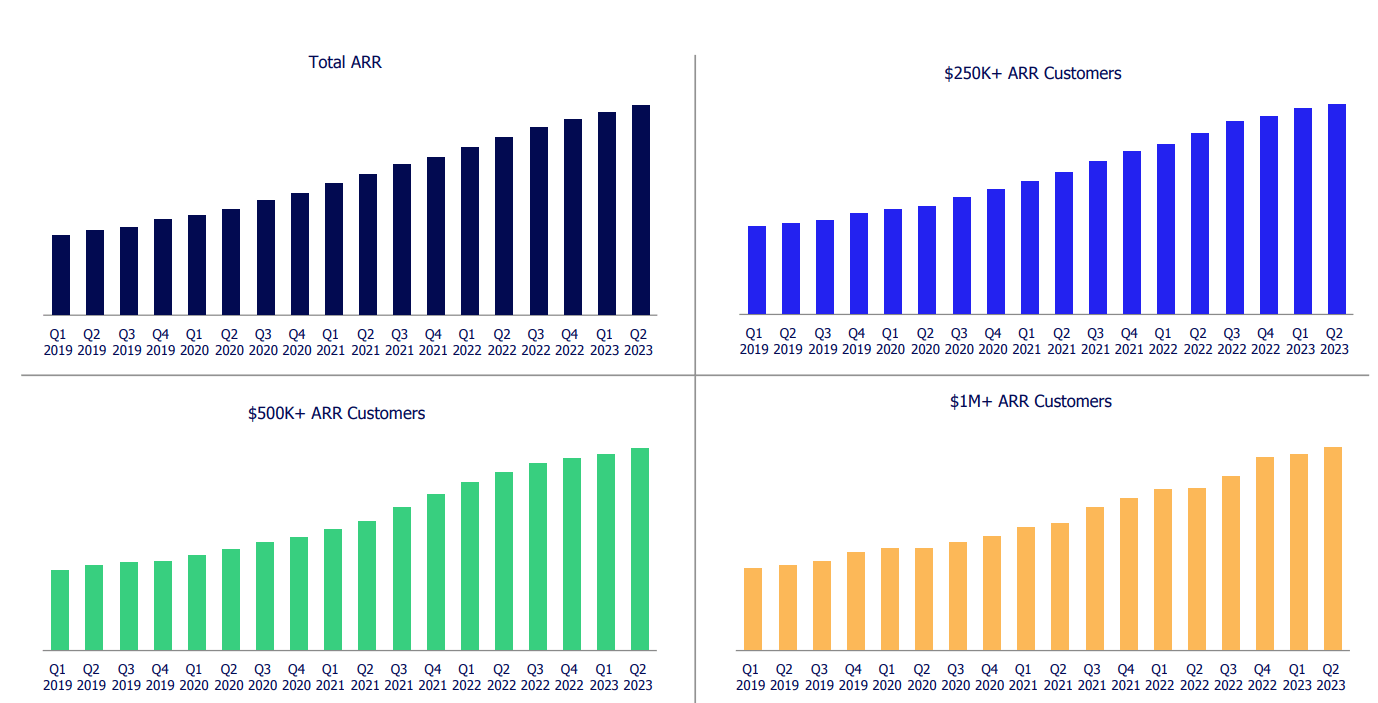

The company has a subscription model where a large portion of its revenues are considered recurring with the exception of service or consulting revenues that are project based. When we look at the company's Annualized Recurring Revenue metrics for the last 18 quarters, we see that it's trending up in all categories defined by the company including Total ARR, $250k ARR customers, $500k ARR customers and $1M+ ARR customers. Since the company has a renewal rate of 99%, almost all new business it obtains counts towards revenue growth. This wouldn't have been possible if the company had a lower renewal rate since a big chunk of new revenues would have to cover the gap before any growth could be obtained. For example if the company had a renewal rate of 80%, it would have to grow its new contracts by 25% just to reach flat revenues but having a strong renewal rate certainly seems to help.

{kind=link}

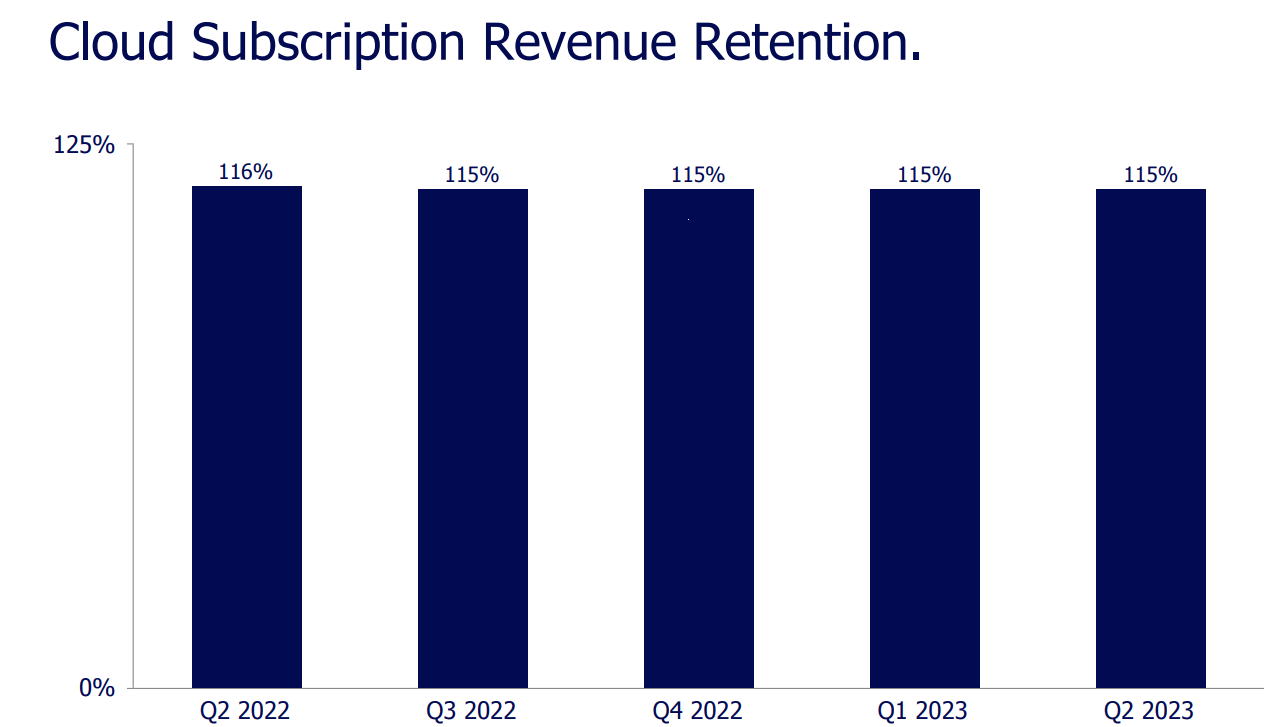

As a matter of fact, the company's Cloud Subscription Revenue Retention is even higher than 100%. You might be wondering how it is even possible to have a retention rate above 100%. There are three ways. First, a company can raise its prices and second, it can upsell more products and services to its existing customers, third, it can increase the scope of existing products that it sold to its existing customers. If a company had an annual contract of $1 million with Appian and it rose to $1.16 million at renewal time, the company can record a retention rate of 116% regardless of whether it came from price hikes, scope enlargement or upselling of new products and services. In either case, it's a net positive for the company. Also, since these are recurring revenues, it's highly predictable and

{kind=link}

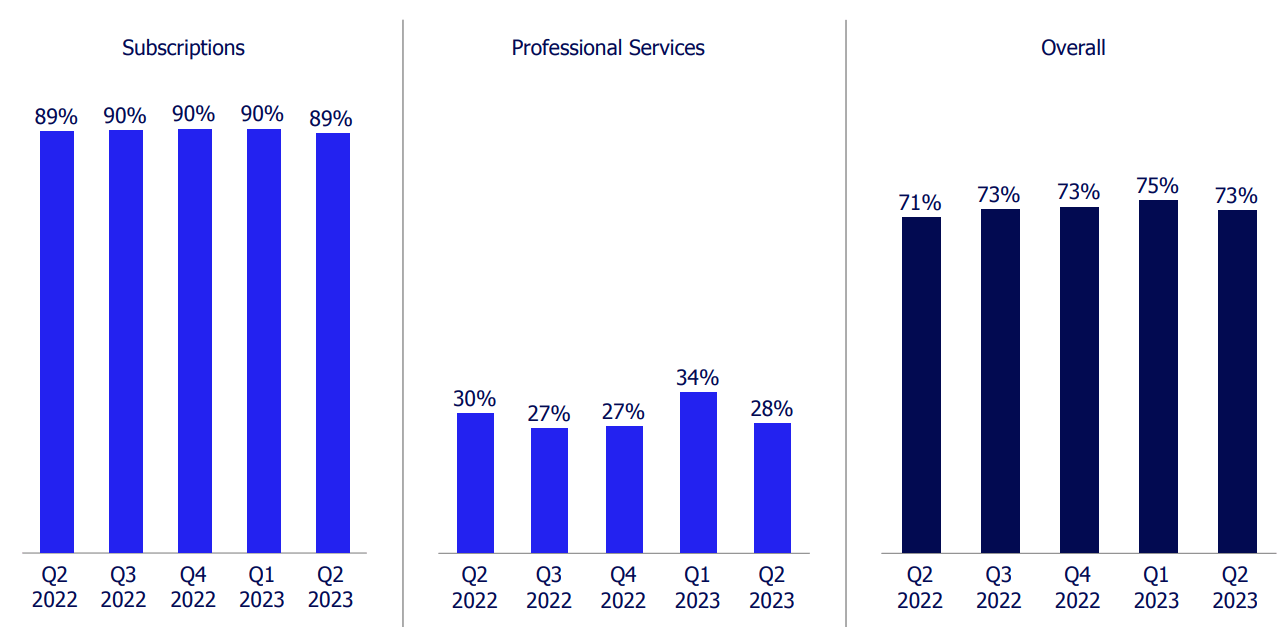

Just about 5-6 years ago half of the company's revenues came from subscriptions while the other half came from professional services & consulting. Since then the company has been making a big shift to turn more and more of its business into subscriptions. Currently about 80% of new contracts signed represent subscriptions. Why is the company making this shift? Because its subscriptions model has much better margins than its professional services model because its costs are fixed and higher revenues translate into higher margins. The company's subscriptions model has been consistently enjoying margins in 89-90% range which puts the company's overall gross margins at 73%. Over time the company's gross margins will move closer to 90% as its total shift towards subscription model is complete.

{kind=link}

One thing is for certain, the company is growing rapidly. Since its IPO in 2017, the company's revenues rose by 280% and its gross profits rose by 340% and there is very little sign of slowing anytime soon.

The problem is that the company's growing revenues and gross profits did not turn into profits in terms of operating income or net income. If anything, the company's profitability situation actually got worse because it had to spend money to grow its revenues and its spending has accelerated even faster than its revenues did. The company will have to reverse this trend if it wants to become sustainable.

The company's operating cash flow has also been negative in the same fashion. Those healthy revenues and gross margins are not translating into profits or cash flows as one would expect.

This is why the stock is down so much in the last couple years. To be exact, it's down 83% from its 2021 highs. Back in 2021 we were in a different environment and investors didn't mind if a company didn't show profits, especially if it was a growth name but today's environment is different and investors want to see profits before putting their money in a company. Even if a company doesn't show current profits, investors would like to see at least a path for profitability.

Calculating a valuation for this company is tricky since it doesn't have profits or positive cash flow but if we were to look at the company's price-to-revenues (sales) ratio, it currently sits at 5.62 which is the lowest it's been since the company had its IPO. The valuation is not compellingly cheap but it's not too unreasonable either.

All in all, Appian is an impressive growth story and the company's growth is likely to continue for years to come but the company also has to show profits or at least a path to profitability for investors to start buying up the stock. Currently the company put all its focus and energy into growth but sooner or later they will have to show that they can be profitable. For those investors who believe in the company's growth story, this could be a good time to start buying up the stock as it sold off 83% from its 2021 highs and while it's not compellingly cheap, it is much cheaper than any time in its history as a public company.

For further details see:

Appian: Growth Is Nice But Profits Will Need To Show Up Soon