APPN - Appian: Losses Stand Out

Summary

- Shares of Appian have gained ~30% year to date, though the company's recent Q4 earnings print has somewhat soured momentum.

- Appian continues to grow cloud subscription revenue at a high-20s pace and believes it can sustain that growth rate through 2025.

- At the same time, however, Appian is committed to investing in growth, so it's not making much progress on slimming down its losses.

- With investors zooming in on profitability this year, and with Appian already trading at a ~5.5x forward revenue multiple, there's not much room for upside.

With the rapid rise and rebound in tech stocks since the start of the year, investors have to be careful to trim portfolios as certain names get too hot. Valuation multiples have re-rated upward, but in many cases companies aren't showcasing a tremendously better business climate than last year.

Appian ( APPN ) is one company that requires a re-assessment. This cloud PaaS company, which helps organizations build more automated and efficient workflows with minimal use of code, has seen its share price appreciate by 30% since the start of the year. This is, however, in the wake of deceleration in revenue growth due to tightening macro conditions, as well as deep red ink that stands out in this more conservative market.

While Appian remains on my watch list, I remain neutral on the company for now. I agree that its low-code business process management software is an attractive product - as many companies trim expenses and lay off staff, a common question that arises is how processes can be improved and automated - a core use case for Appian software. The company has done an excellent job in recent years of adding new logos, signing large deals, pawning off low-margin services and implementation work to partners and focusing on recurring-revenue software sales.

At the same time, however, I don't think there's much room for upside for Appian, at least in the near term. Growth rates are deflating, especially for total subscription revenue growth - which is going to make Appian's upward multiple re-rating since the start of the year difficult to justify. Equally compromising for this stock is its relatively persistent pattern of deep Adjusted EBITDA losses - which stand out more in today's more conservative market, where investors are paying stricter attention to losses and path to profitability.

Perhaps the deepest nail in the coffin for Appian right now that prevents me from investing is the fact that Appian is simply not a compelling value play. At current share prices near $42, Appian trades at a market cap of $3.05 billion. After we net off the $196.0 million of cash and $118.0 million of debt off Appian's most recent balance sheet, the company's resulting enterprise value is $2.97 billion.

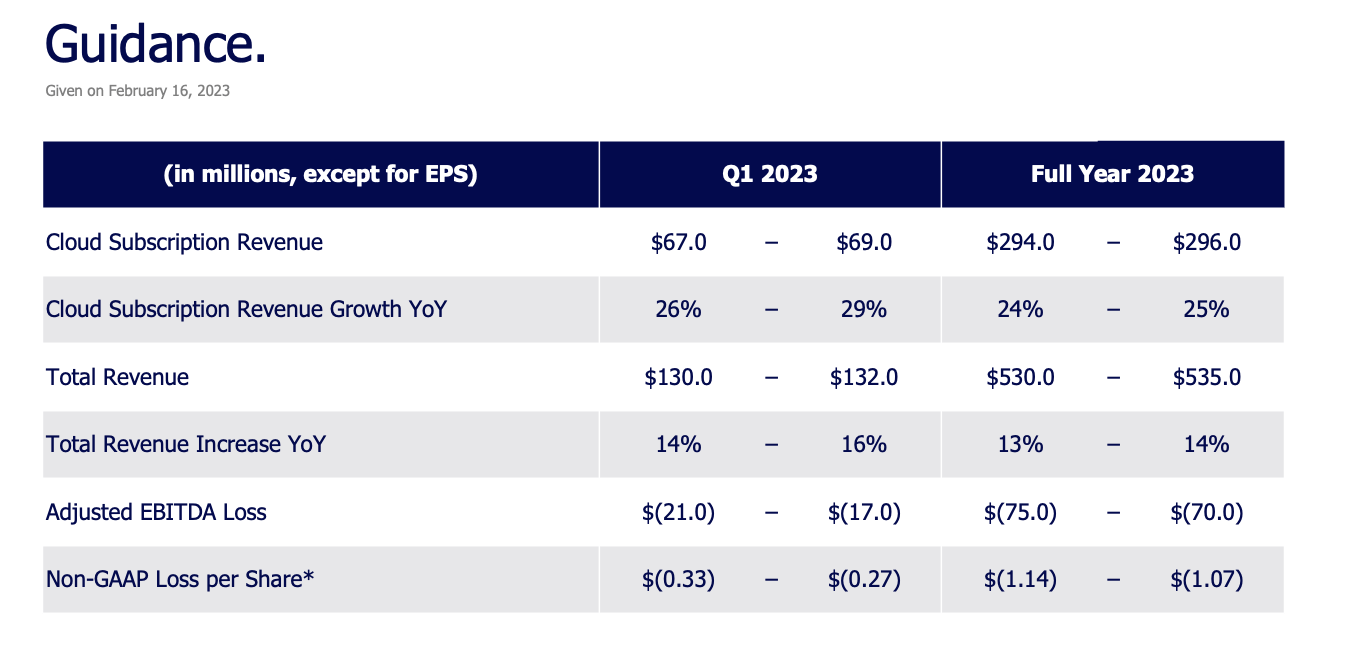

Meanwhile, for the current fiscal year, Appian has guided to $530-$535 million in revenue, representing just 13-14% y/y growth (the continued offloading of services work is a factor here - underlying cloud subscription revenue growth, meanwhile, is much stronger at 24-25% y/y).

{kind=link}

This puts Appian's valuation at 5.6x EV/FY23 revenue - which is rich for a company with a roughly one-quarter revenue mix in low-margin services. We should note as well that guidance calls for no improvement in adjusted EBITDA nominal losses (though with a roughly two-point improvement in margins), as the company has chosen to continue investing in growth.

All in all - I see no "dynamite" reasoning for buying this stock in 2023, at least not at current prices. Keep watching this name, but for now steer clear here and invest elsewhere.

Q4 download

Let's now review Appian's latest fourth-quarter results in greater detail, which the company released in mid-February. The Q4 earnings release in shown below:

{kind=link}

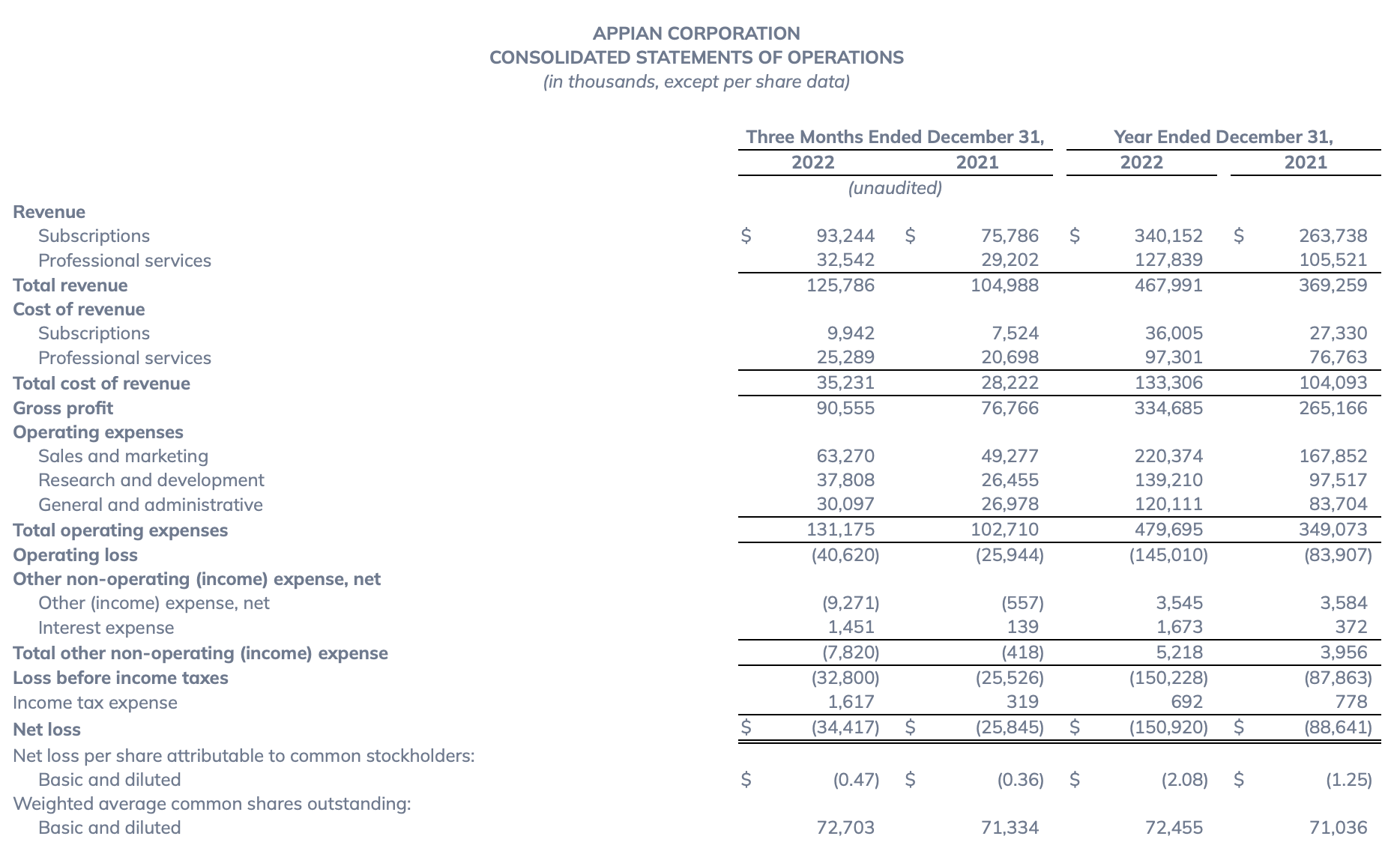

Appian's revenue grew only 20% y/y to $125.8 million, edging out over Wall Street's expectations of $122.8 million (+17% y/y). Revenue did, however, decelerate from 28% y/y growth in Q3.

Growth was slightly stronger on cloud subscriptions, however, which grew 29% y/y to $65.8 million and represented slightly over half of total revenue. This is the silver lining that prevents me from being overly bearish on Appian - note as well that Appian management believes that in the absence of severe macro turndowns, the company expects to maintain 26-29% y/y growth in cloud subscriptions throughout FY25.

The company ultimately believes that demand for its product will be driven by a growing organizational desire for greater efficiency and reducing wasteful spend. Per CEO Matt Calkins' remarks on the Q4 earnings call :

Appian's value proposition emphasizes efficiency, productivity, time to value and ROI, the very things buyers seek in a downed economy. Speaking of productivity, I think there may be a revolution on the horizon. Last year's productivity growth in the U.S. was negative 1.3%, the worst result since 1974.

This reflects changing post COVID labor patterns but also a certain corporate indifference to the topic. For years now, businesses haven't had to focus on productivity, since money was cheap and labor was plentiful. Now that money is expensive and labor is tight, they'll return to the topic in earnest, and there is a surprise waiting for them.

The science of productivity enhancement has come a long way in the past few years. Software is ready to be more than a tool to help people do work. Software is ready to do the work for us. That's the revolution."

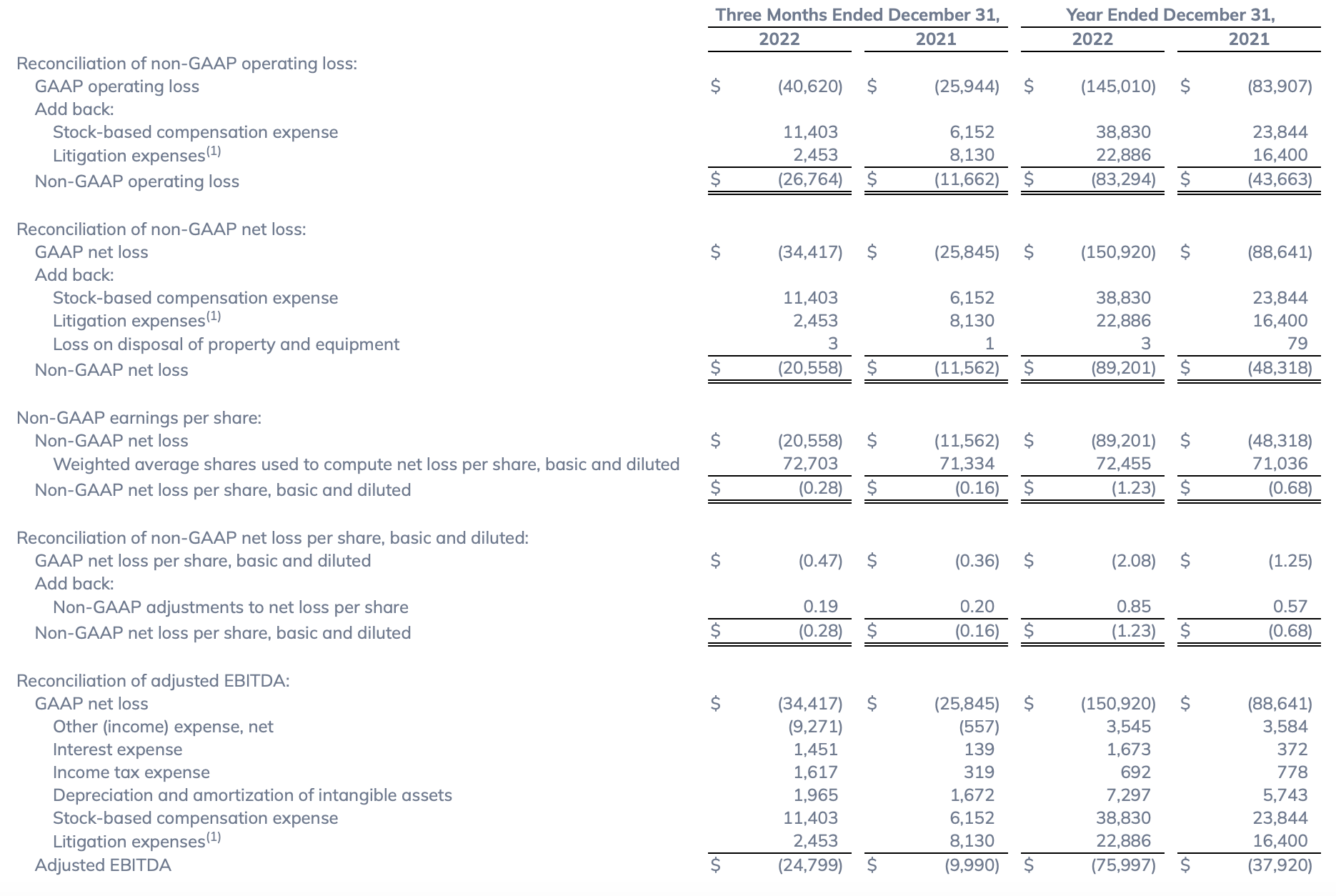

At the same time, however, because Appian sees a greenfield market for its software-enabled automation products, it is choosing to invest in growth at the expense of its bottom line. As seen in the chart below, adjusted EBITDA losses more than doubled to -$24.8 million, representing a -20% margin versus last year at a -$10.0 million loss and a -10% margin.

{kind=link}

Full-year adjusted EBITDA losses of -$76.0 million were also roughly double the prior-year losses, despite gross margin benefits from the greater revenue mix owing to subscriptions. Recall that FY23 guidance doesn't call for adjusted EBITDA losses (at a -$75 million to -$70 million range) substantially improving.

Key takeaways

All things considered, I don't view Appian to be an attractive investment at the moment. The company will likely see investor pressure for persistently high adjusted EBITDA losses, and the stock's current revenue multiple near 6x doesn't afford much room for error unless growth materially outperforms (unlikely in this macro climate). Keep tracking this one, but don't rush in to buy just yet.

For further details see:

Appian: Losses Stand Out