APPN - Appian: More Risk Than Reward

2023-08-15 09:18:03 ET

Summary

- Appian's stock has declined since reporting Q2 results, but is still up 50% for the year.

- The company faces challenges such as delayed deal closings, competition in the BPM space, and deep losses.

- Appian's revenue growth has decelerated and its profitability lags behind its peers, making it a risky investment.

Though the mood in the markets just a month ago was one of pure exuberance, sentiment has faded dramatically since earnings season began. Even hopes of slowing inflation and the chances of interest rate cuts can't offset the notion that stocks are expensive again.

Appian ( APPN ), the business process re-engineering software company, reported results in early August and like most of its tech peers, the stock is down since then. Still, the company remains up nearly 50% on the year, leading many investors to think: is now the right time to buy the dip in a name that still seems to have momentum?

I remain bearish on Appian, especially after parsing through the company's latest results. The company is arguing that macro challenges are causing a delay on deal closings rather than cancellations, but we've seen multiple quarters of sequential revenue deceleration as well as a slight softening of the company's renewal rates, challenging that notion.

Appian's management is future-oriented, and is encouraging investors to recognize the opportunities in AI (though this is similar verbiage as we've heard from the rest of the chieftains of the software industry). It's true that AI is an opportunity for Appian that the company has already leveraged: it leverages its virtual database capabilities to drive content processing and workflow automation tools for its clients. At the same time, however, we should also note that Appian is hardly alone in this space: the list of other companies in the BPM space is large, from ServiceNow ( NOW ) to Atlassian ( TEAM ).

I still see the following key fundamental risks for Appian:

- Large transformational projects are being delayed in the current macro climate. Efforts to automate entire business processes are large capital projects, which are being delayed until better times. In the software sector, it's the products that can generate quick wins and instant ROI that are winning out, and this tilt may hurt Appian, whose integration process may be more involved than other products.

- Still a large chunk of professional services revenue. To Appian's credit, at the time of its IPO, the company had a roughly 50/50 revenue mix split between professional services and subscriptions, and that has since improved to only a ~25% mix of professional services. The mix shift has improved gross margins, but Appian's margin profile as well as services mix are poorer than most of its peer software companies.

- Deep losses. In spite of improving gross margins, Appian continues to spend more and more, particularly on sales and marketing. The company doesn't see a path to breakeven adjusted EBITDA on a full-year basis until FY24.

And amid these challenges, Appian still isn't cheap. At current share prices near $48, Appian trades at a market cap of $3.51 billion. After we net off the $236.9 million of cash and $208.3 million of debt on Appian's most recent balance sheet, the company's resulting enterprise value is $3.48 billion.

For FY24, Wall Street consensus is pegging Appian's revenue at $625.8 million, up 16% y/y (data from Yahoo Finance ). I'd argue there's more risk than opportunity in this outlook, given Appian's revenue growth has already decelerated to 16% y/y in the current quarter. In order to protect against the natural deceleration that we've already seen play out over the past several quarters, you'd have to believe that AI-related products and implementations will drive substantial growth throughout the next year. And in my view, if you really think this is the case, it makes much more sense to bet on companies specializing in AI/ML like Palantir ( PLTR ) and C3.ai ( AI ).

Against consensus expectations, Appian trades at 5.6x EV/FY24 revenue - not expensive, of course, but not cheap either considering growth decelerating to the mid-teens as well as Appian's persistent margin deficit relative to software peers.

The bottom line here: I don't see many reasons to remain invested in Appian. In my view, quarterly results will continue to disappoint here and there are very few catalysts to spark a renewed rebound. Stay on the sidelines and invest elsewhere.

Q2 download

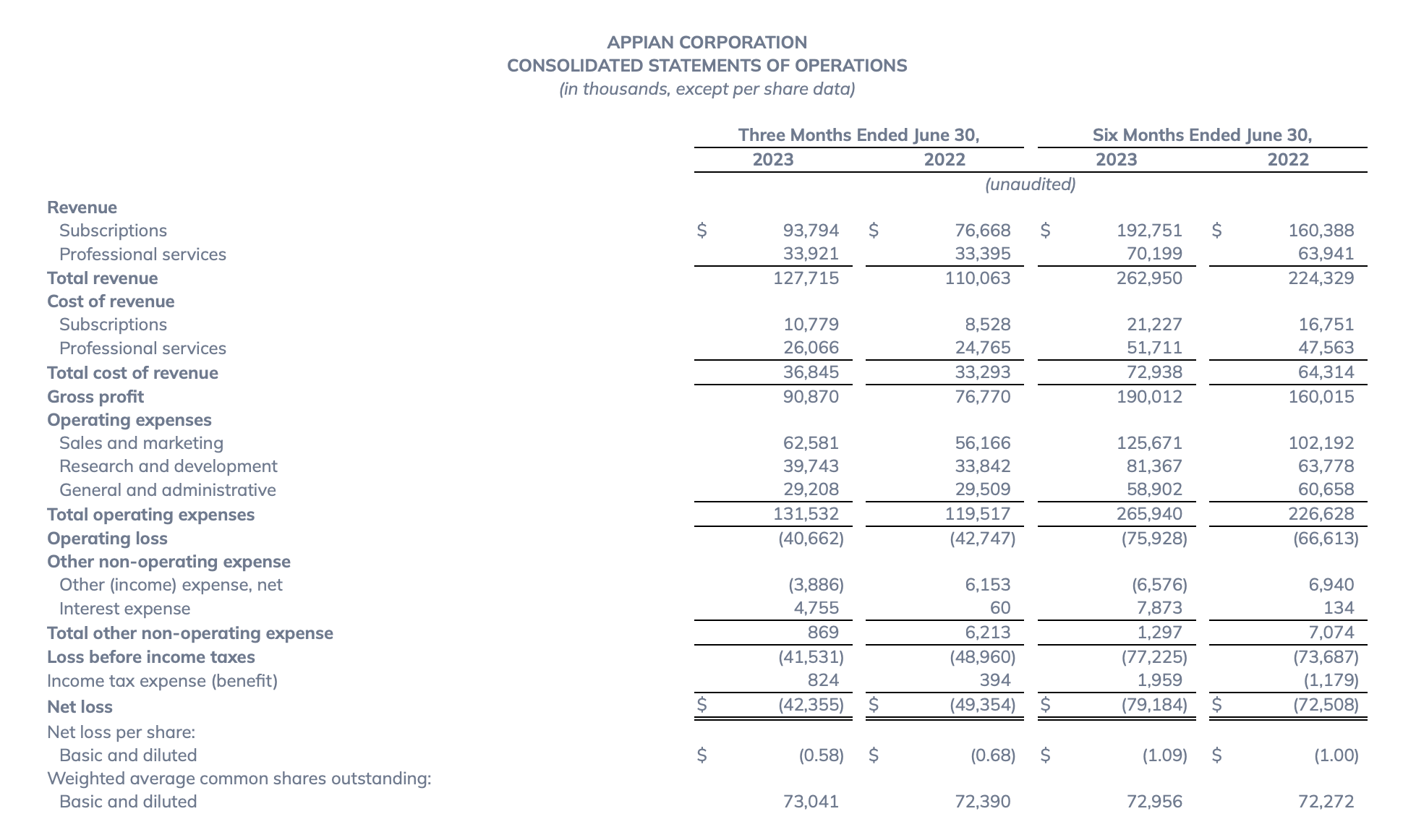

Let's now go through Appian's latest quarterly results in greater detail. The Q2 earnings summary is shown below:

{kind=link}

Appian's revenue grew 16% y/y in the second quarter to $127.7 million, only slightly ahead of Wall Street's expectations of $123.8 million (+12% y/y) - but decelerating two points versus 18% y/y growth in Q1, which in turn had decelerated from 20% y/y growth in Q2.

Asked about the deal environment on the Q&A portion of the Q2 earnings call, CEO Matt Calkins noted as follows (key points bolded):

Well, I think there was a tremendous amount of excitement around AI. But I also think it's a little bit early for us to appraise that because the AI boom happened less time ago than the length of our sales cycle. So I think it would just be premature to speak to the way that's open pocket books. I don't know yet.

I will say that it appears that customers are applying extra scrutiny to purchases this year that their sales cycles are slightly extended by that. There's been some delays, more delays than cancellations. There's just, I think, just extra consideration around investment to be made. And the counterpoint to that is an extreme amount of excitement about the way technology could create better efficiency, specifically around AI [...]

I would say that it's somewhat consistent with last quarter. We see deals taking longer, but not disappearing, just taking longer. The interest is there. And I don't deny you could see it in the numbers, right? If you were to see side-by-side of a regular year versus what we're seeing now, there would be an evident difference would be a delay. But I also don't want to make it sound like that's an enormous difference because it's not."

These are similar remarks to the rest of the software industry - though I'll say that with consensus expecting 16% growth from Appian next year, Appian may have a tougher bar to cross to keep growth rates at its current pace.

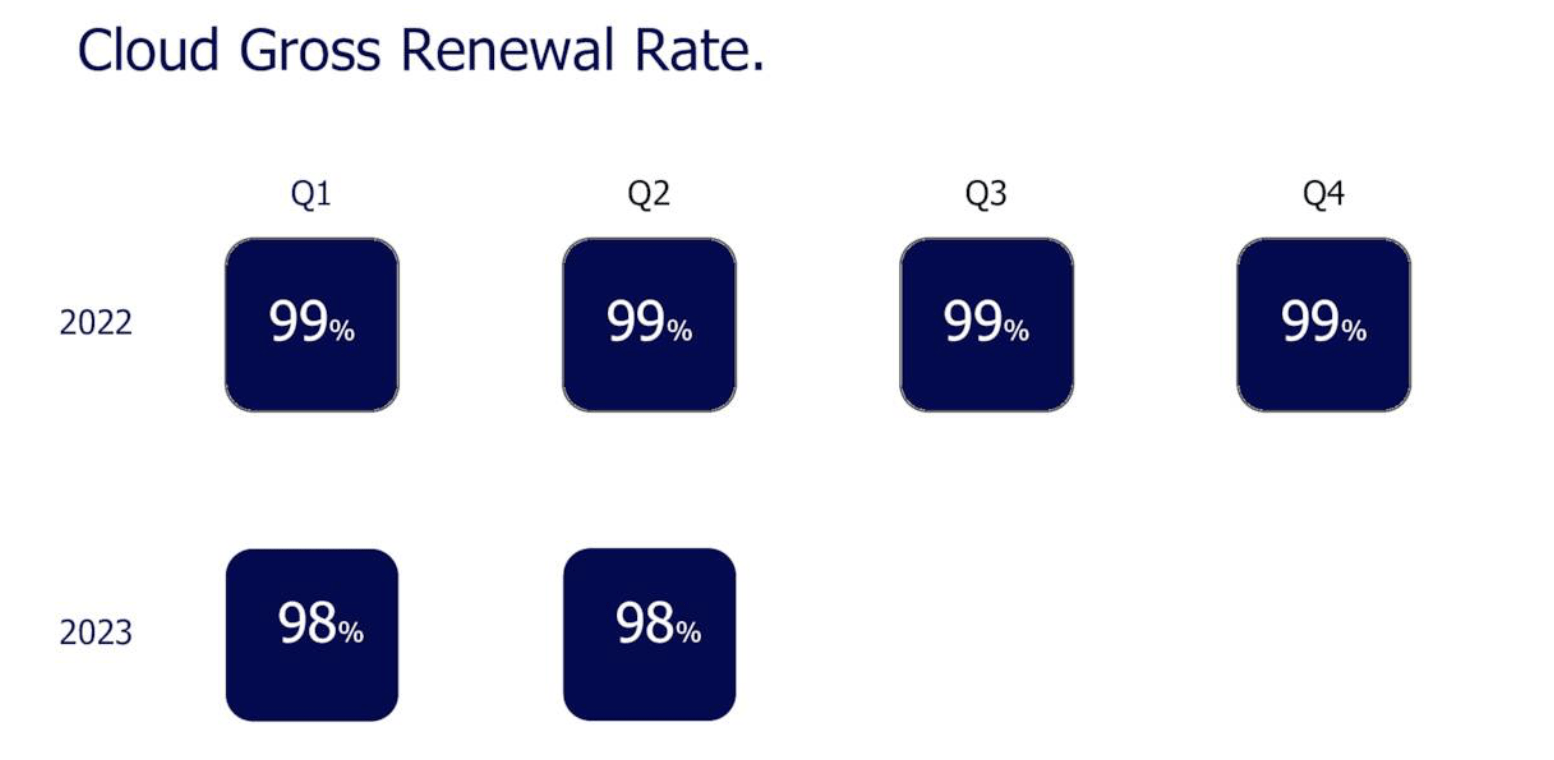

We note as well that cloud gross renewal rates have softened by one point relative to last year:

{kind=link}

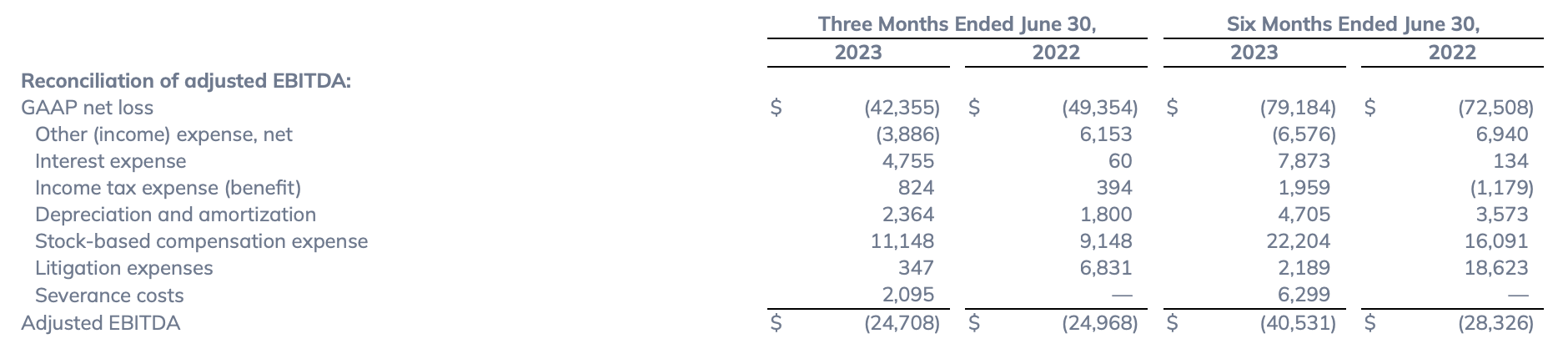

And on profitability, the company hasn't made many meaningful strides either. Adjusted EBITDA losses of -$24.7 million were the same magnitude as in Q2 of last year, though from a margin perspective the -19% margin this quarter was slightly better than -23% in the year-ago Q2.

{kind=link}

This is where Appian could use work: though most software companies are reporting deceleration, the majority are making huge strides on profitability (the list of such companies is long: Dropbox ( DBX ), Twilio ( TWLO ), Smartsheet ( SMAR ), and DocuSign ( DOCU ), just to name a few). In this more cautious environment, Appian's losses stand out.

Key takeaways

In my view, there's not much incentive to invest in Appian. The stock is undergoing a fundamental deceleration, and consensus expectations call for the company to hold its growth rates next year - which I view unlikely. At the same time, double-digit adjusted EBITDA loss margins also weigh on sentiment for the stock, which isn't cheap either at ~5.6x forward revenue. Look elsewhere for buying opportunities.

For further details see:

Appian: More Risk Than Reward