APPN - Appian: Shifting To Neutral On Heightened Risks

Summary

- Shares of Appian have dropped more than 30% over the past year, with losses accelerating since the company's third-quarter earnings print.

- Growth is decelerating, both due to FX pressures plus a lengthening of sales cycles.

- The company's adjusted EBITDA losses have also spiked, due to unseasonably strong hiring.

- Now trading at ~5x forward revenue, Appian is cheap - but not substantially more so than other SaaS stocks to justify these added risks.

Amid market volatility and a potential early-year rebound in 2023, investors have to be incredibly diligent about stock-picking and pruning their portfolios in order to beat the market. Valuations have jumped all over the place in the past few quarters, and different companies have reacted very differently to changing macro conditions.

Appian ( APPN ) is one of the positions I have recently re-assessed. This low-code business process management (BPM) software company, which helps companies design automated software solutions to manual processes without much technical implementation, has been in the penalty box since it reported rather weak Q3 results in early November, and is down more than 30% over the past year.

Now, the bull and bear case is roughly equal weighted for Appian

Though I was bullish on Appian in the early half of 2022, I am now shifting my recommendation on the stock back to neutral. At this point, I see Appian as a relatively balanced bag of positives and negatives. On the bright side for this company:

- Broad use cases and deeply greenfield market. Appian estimates its TAM at roughly $37 billion, indicating that its present ~$500 million annual revenue run rate is only a fraction penetrated into the BPM space (business process management). Automation is a benefit to any industry, any department, and any workflow - and with the dearth and expense of technical workers to go solve these problems, businesses are finding it faster and easier to have line-of-business users automate their own processes instead, as long as limited technical knowledge is needed.

- Stellar growth is now coming from subscriptions. Appian continues to generate >30% y/y subscription revenue growth, and its mix of low-margin professional services revenue continues to shrink, which has pushed up Appian's gross margins to be closer in line with software peers.

At the same time, however, we have new worries to be concerned about:

- Sales cycle slowdown. Appian reported that macro headwinds have lengthened the process of winning new deals. From this, it can become evident that corporate leaders may see BPM and Appian as a "nice to have" when IT investment budgets are high - but right now, as companies are slashing spend and de-prioritizing projects, Appian may continue to see demand weakness.

- Deep red ink. Despite the fact that Appian has greatly improved its gross margin profile thanks to leaning into its subscription revenue, the company's adjusted EBITDA losses have grown thanks to ballooning opex.

Valuation is no longer a draw

One of the central reasons why I'm selling out of my Appian position, however, is simply the fact that Appian's valuation vis-a-vis other growth stocks is no longer quite that favorable.

At current share prices near $35, Appian trades at a market cap of $2.57 billion. After we net off the $92.7 million of cash (another key concern here: Appian's liquidity is rather stretched! The company recently raised ~$100 million via debt after the close of its third quarter, but the path to profitability still seems far from here) from the company's most recent balance sheet, Appian's resulting enterprise value is $2.48 billion.

Meanwhile, for the current fiscal year FY23 (the year for Appian ending in December 2023), Wall Street analysts have a consensus revenue expectation of $532.1 million for the company (data from Yahoo Finance ), representing a deceleration to 14% y/y growth (which seems appropriate given Appian's recent bearish comments on its sales momentum). This puts the company's valuation at 4.7x EV/FY23 revenue.

This is certainly still cheap relative to historical standards - but considering that a ~4-5x forward revenue multiple has become the norm for SaaS companies (some of which are growing faster or are more profitable than Appian), I'd say it's hard to make a bull case for Appian based on its current valuation. Because so many other SaaS companies have seen massive re-ratings, I think there are far better deals in the market to buy (some of my top plays at the moment include Palantir ( PLTR ), DocuSign ( DOCU ), Zoom ( ZM ), and Asana ( ASAN )).

Q3 download

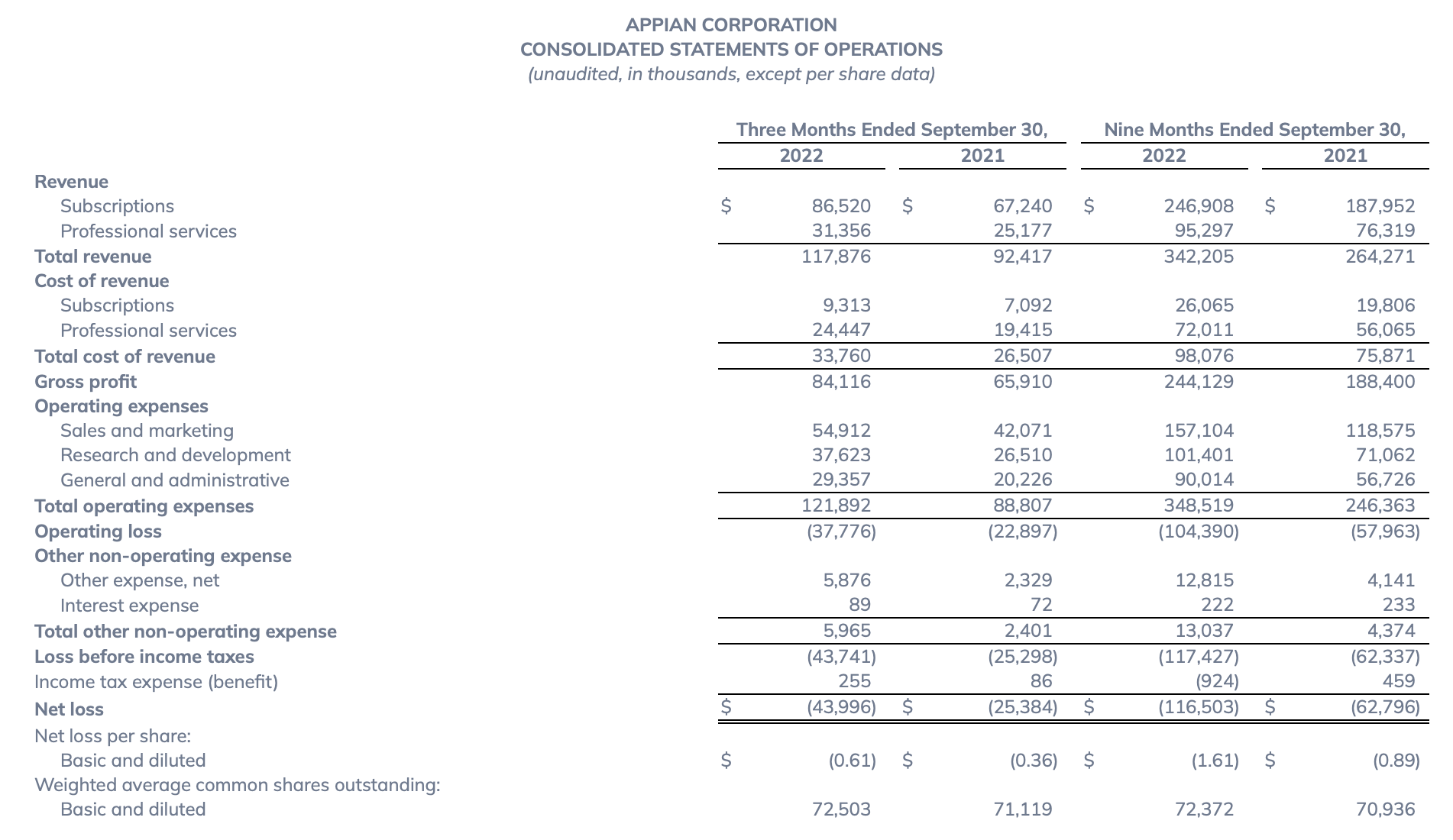

Let's now go through Appian's latest third-quarter results to highlight some of the key risks the company revealed. The Q3 earnings summary is shown below:

{kind=link}

Appian's revenue grew 28% y/y to $117.9 million, only slightly beating Wall Street's expectations of $116.7 million (+26% y/y). Growth decelerated sharply from 33% y/y in Q2, owing both to a bona fide sales slowdown as well as sharpening FX headwinds.

The company notes that sales cycles have slowed - which can be reflective of both recessionary trends, or, put in a more positive light, the fact that Appian is now selling more into the federal government which typically has a seasonal slowdown in the third quarter. Per CEO Matt Calkins' remarks on the Q3 earnings call :

Last quarter, I predicted an economic slowdown and said we were not feeling it yet. This quarter, we did feel it. We are entering a period of uncertainty [...]

If a recession arrives, you might see ARR slowdown or the top dollar bracket grow more slowly than the lower brackets [...]

In addition to these charts, I want to add my reflection on sales cycle length. In Q3, we saw a mild lengthening roughly 10%, which is consistent with a recessionary scenario. It might also however reflect that Q3 is characterized by federal business and those deals have slightly longer sales cycles."

The worst has not come yet, as Appian's guidance calls for overall growth to slow to 16-18% y/y in Q4; and as previously mentioned, consensus expectations call for Appian's growth to slow to 15% y/y in FY23.

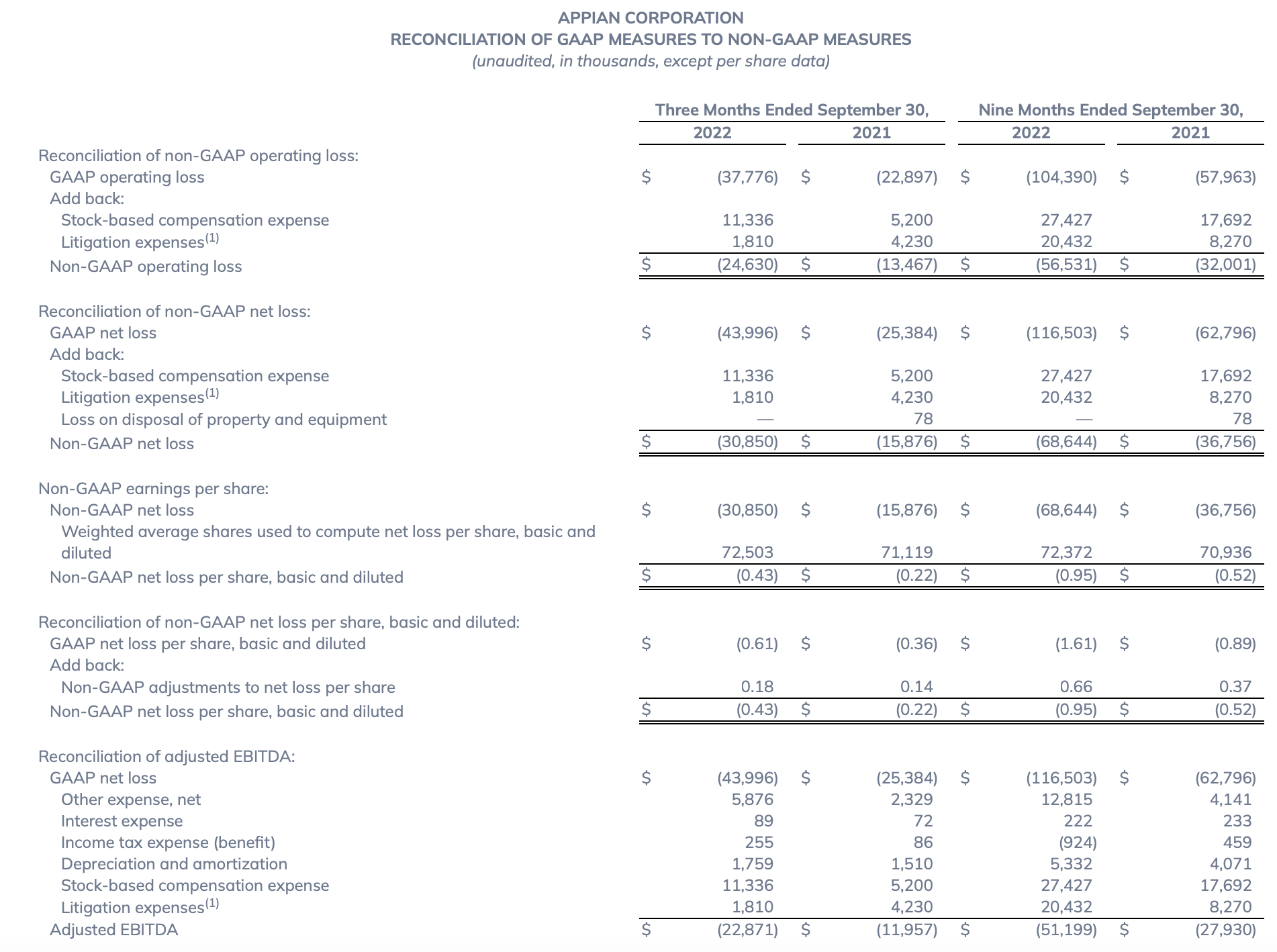

There's more bad news on the profitability front, however, as Appian's adjusted EBITDA losses nearly doubled to -$22.9 million in the quarter, representing a rather unfavorable -19% adjusted EBITDA margin (six points worse than -13% in the year-ago Q3).

{kind=link}

Especially in this volatile market where investors have re-prioritized investing in profitable companies, this is a bad look for Appian. The company attributes the opex inflation to faster-than-expected hiring and lower-than-expected churn, which it hopes to correct for in FY23. Per Calkins' remarks on the Q3 earnings call:

In Q3, our personnel plans succeeded beyond my expectations. Our attrition dropped all the way down to 3.2% company-wide for the total quarter, which is to say that 97% of our team stayed. Recruiting meanwhile performed much stronger than I predicted. In Q3, we added 221 employees compared to 203 in the prior three quarters combined – the prior three quarters combined. 77% of those people joined the sales, engineering and consulting departments, our three areas of focus in that order. We hired more than 100 people into the sales department alone, repairing a longstanding shortage of account executives. We hired 56 engineers, many of them the founding cohort of our new dev center in Chennai. We hired 38 consultants addressing a scarcity of billable resources.

This third quarter turned out to be an exceptionally advantageous time for finding elite new talent, as periods of economic turmoil often are. Without the effects of FX and the personnel surge, which is to say the cost of acquiring retaining training and onboarding these employees, adjusted EBITDA would have been in range this quarter. With this bountiful hiring, we staffed the team we need for 2023 and we did it in 3 months instead of three quarters like we had expected."

Even though a slower pace of hiring in 2023 should help margins start to climb upward again, the company's double-digit loss margins plus the fact that it recently took on additional debt to boost its liquidity will continue to be a drag on investor sentiment.

Key takeaways

With the expectation of slowing sales cycles and a sharp deceleration in revenue, on top of terrible profitability optics, Appian isn't that great of a bargain trading at just under 5x forward revenue. Ditch this name and invest elsewhere.

For further details see:

Appian: Shifting To Neutral On Heightened Risks