APLE - Apple Hospitality: An Impressive Monthly High-Yield Play

2023-04-17 14:25:04 ET

Summary

- Apple Hospitality is a top-tier hospital REIT with a juicy monthly 6.2% dividend yield.

- While it wasn't able to protect the dividend during the pandemic, improving financials and a stellar balance sheet resulted in rapid dividend growth since 2020.

- The company is in a good place to further hike its dividend while shares remain attractively valued.

Introduction

"I didn't know Apple owned hotels!" is what someone told me in a discussion about real estate a few months ago. It's a common mistake as Apple Hospitality ( APLE ) is a stock that continues to fly under the radar. It has also happened quite frequently that people told me that the ticker is AAPL whenever I use APLE on social media. Again, most people don't know about the fascinating company behind the APLE ticker.

I regret not covering Apple Hospitality in 2023, as it is performing exceptionally well despite challenging market conditions. Despite weak consumer sentiment, high rates impacting commercial real estate and somewhat subdued investor sentiment, Apple Hospitality remains resilient.

What makes this stock even more attractive is its impressive yield of 6.2%, along with positive trends such as increasing occupancy rates, strong pricing power, and a healthy balance sheet. In this article, I will guide you through my thoughts and elaborate on why I believe Apple Hospitality is a compelling investment option with significant upside potential.

APLE Is Back

What to make of this high-yielding REIT.

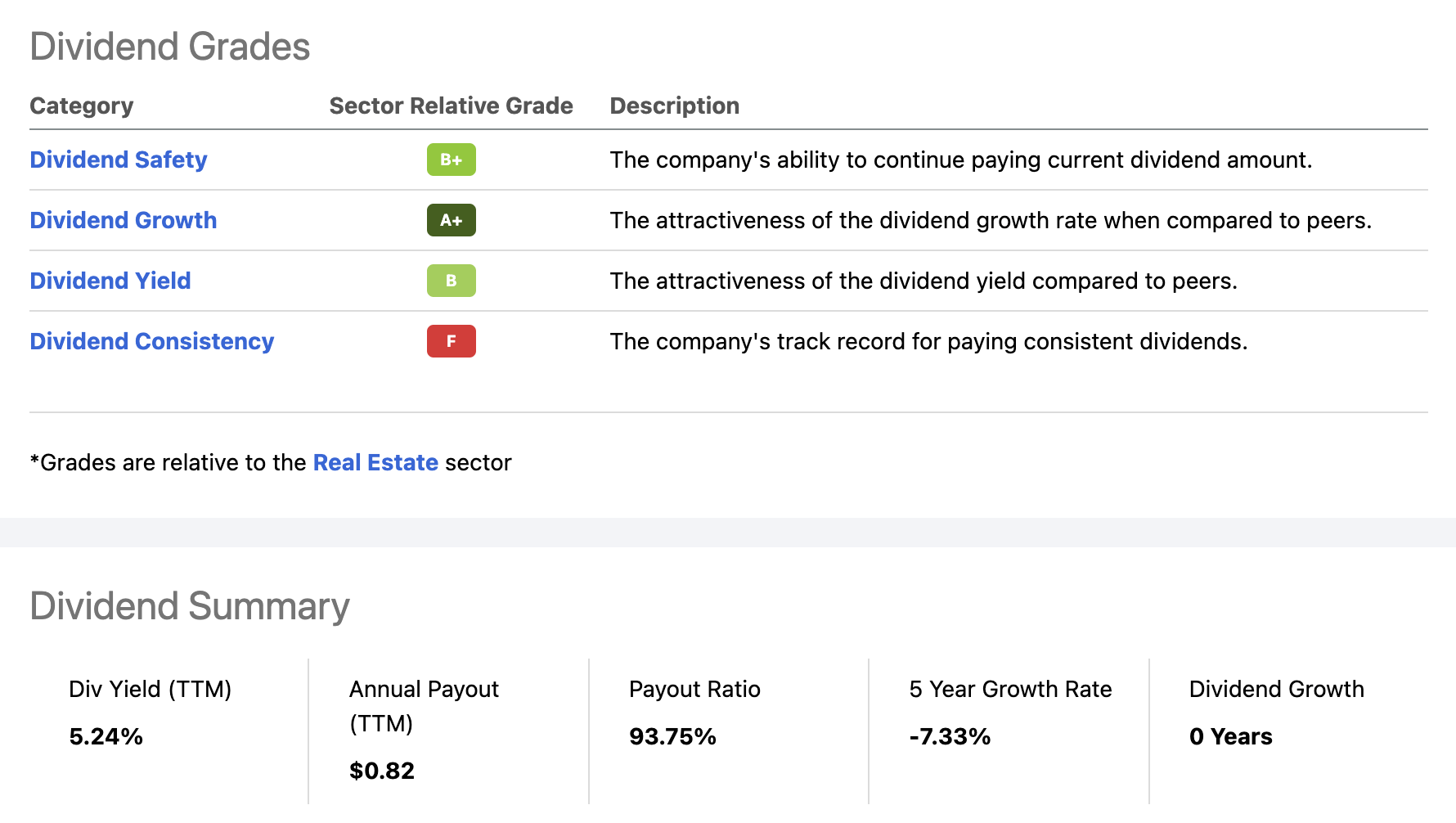

Let's begin this article with some bad news - Apple Hospitality, despite its many strengths, is not bulletproof. As evident from the Seeking Alpha dividend scorecard below, the company fares well in terms of safety, growth, and yield. However, it falls short in terms of dividend consistency, a factor largely impacted by the pandemic. Please note that the yield in the chat below has not been updated. It's 6.2%.

{kind=link}

Seeking Alpha

As everyone knows, the pandemic triggered an unprecedented wave of lockdowns. While the response differed per state, every state participated in the first lockdown - to my best knowledge, that is.

This hurt Apple Hospitality and every single one of its peers.

Founded in 2007, APLE is a REIT that primarily invests in income-producing real estate in the lodging sector in the United States.

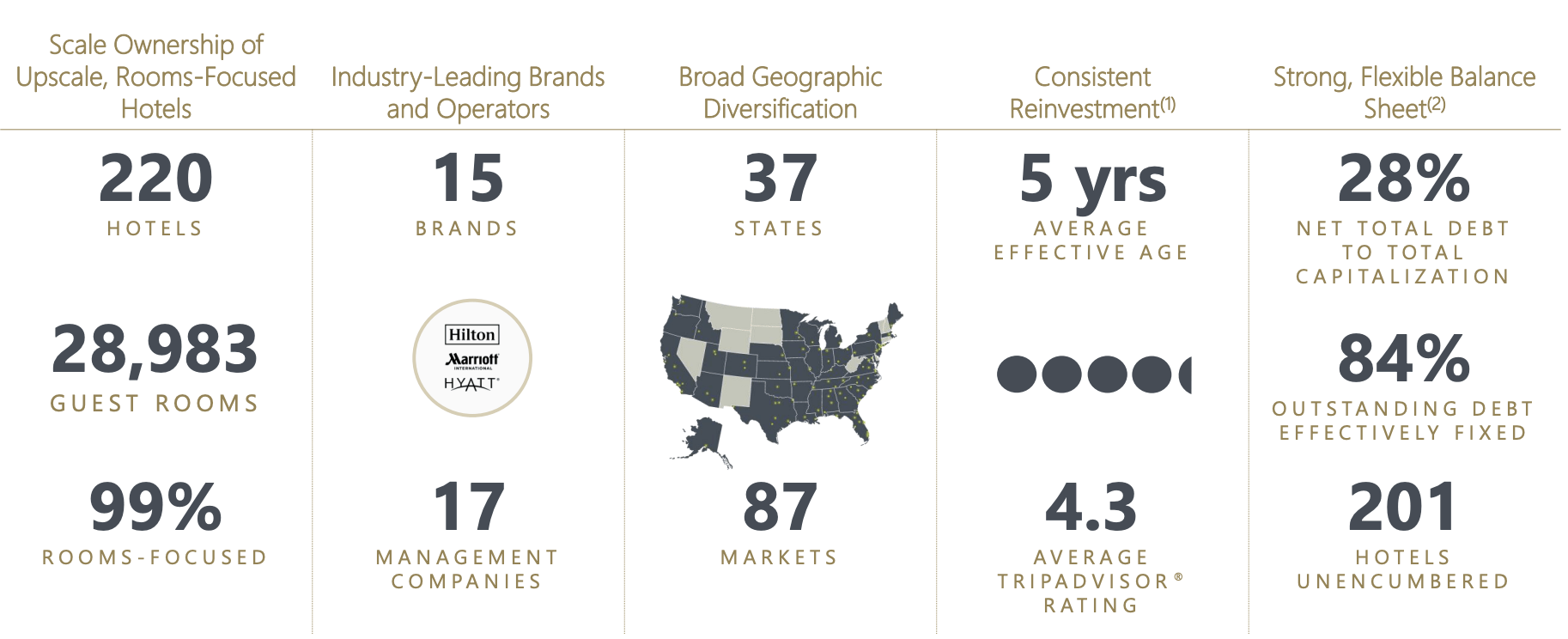

As of December 31, 2022, the company owned 220 hotels with a total of almost 29,000 rooms located in urban, high-end suburban, and developing markets in 37 states. Most of the company's hotels operate under Marriott or Hilton brands, which explains why its target audience is a bit more high-end.

On a side note, this somewhat protects the company against economic downturns, as its target customers are less prone to economic weakness than lower-cost alternatives.

These properties are managed by 17 separate hotel management companies that are not affiliated with the company. These assets are managed under separate management agreements and allow the company to effectively scale its operations.

{kind=link}

Apple Hospitality

Moreover, as stated in the slide above, the company is 99% room-focused, which means it isn't dealing with conventions and similar events.

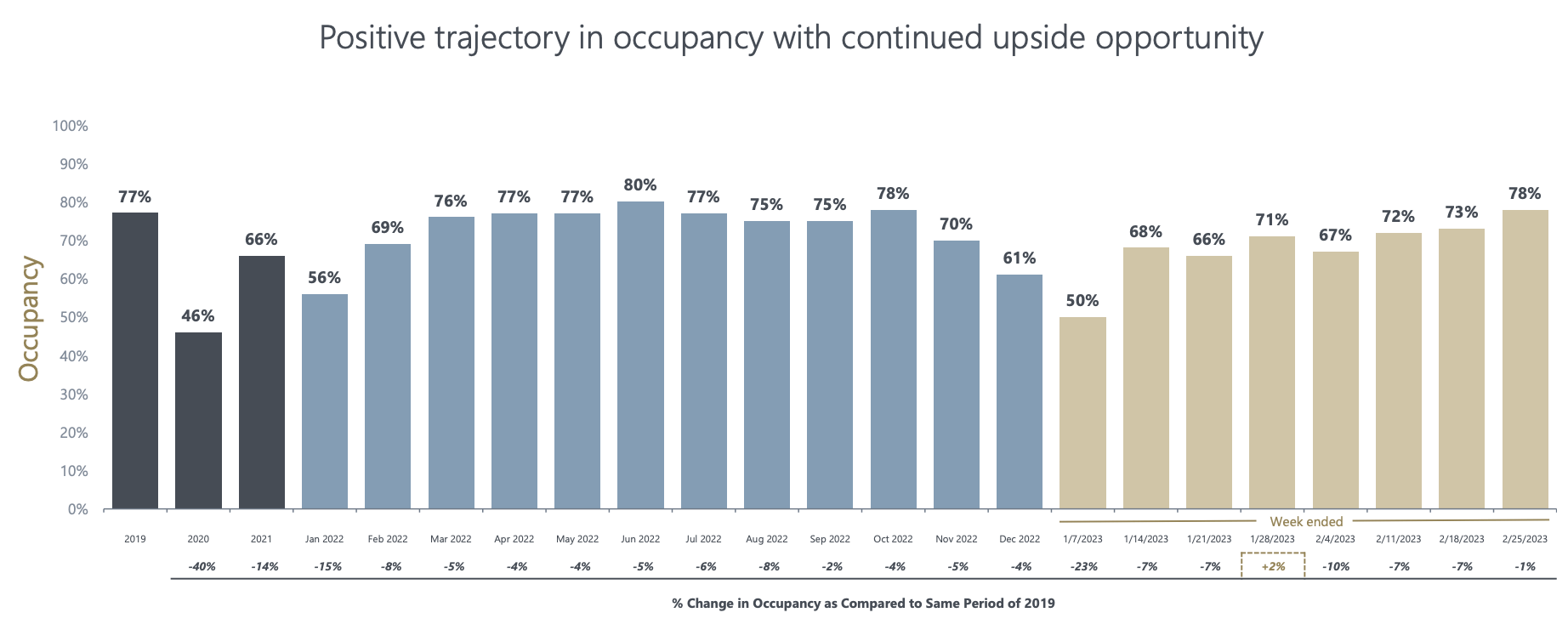

That said, the chart below shows how challenging 2020 was. The occupancy rate was just 46%, 40% below 2019 levels. During the early weeks of the pandemic, that number was close to zero.

{kind=link}

Apple Hospitality

On March 20, 2020, the company announced that it would suspend its dividend while postponing all non-essential capital improvement projects and drawing all of its available cash to withstand the uncertainty that came with these lockdowns. Founder and Executive Chairman Glade Knight volunteered to forego his salary for the six months that followed.

The most recent data shows that the occupancy rate has risen to 78%, a new high in a trend that started in 2020.

In March 2021, APLE's monthly dividend came back. Back then, it was $0.01 per share per month. That number was hiked to $0.05 in February 2022.

In August 2022, the company hiked this number by 40% to $0.07, followed by a 14.3% hike to $0.08. In December, the company also announced a $0.08 special dividend, which explains the spike in the chart above.

The current $0.08 monthly dividend implies an annual dividend of $0.96, which translates to a forward yield of 6.2%. This yield is protected by a 53% funds from operations payout ratio. The sector median is 65%.

I expect the dividend to be hiked to $0.10 (pre-pandemic) before the end of the year.

{kind=link}

Apple Hospitality

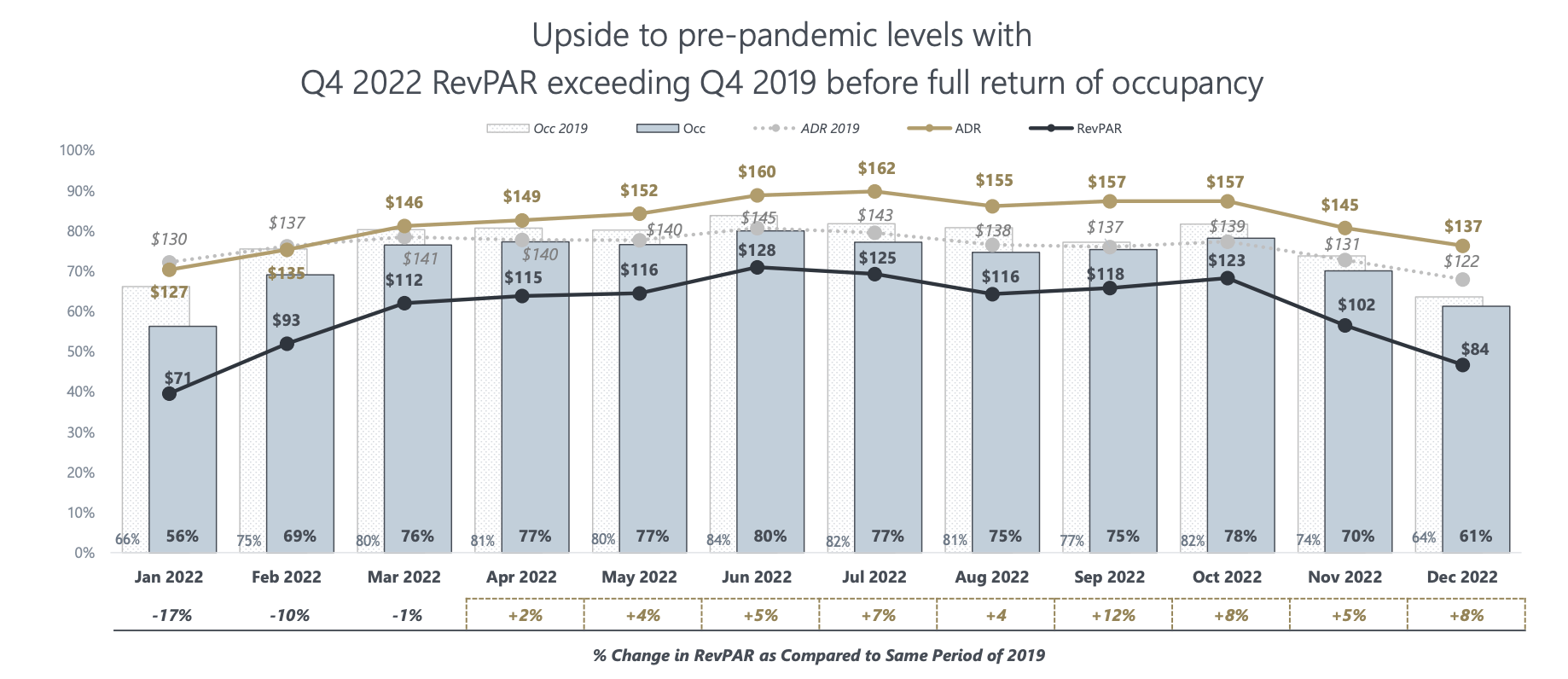

Not only that but in 2022, APLE reported numbers that exceeded pre-pandemic levels. In December 2022, the company had an 8% higher revenue per available room compared to December 2019. In September 2022, RevPAR was up 12%. In January 2023, RevPAR growth was 3%.

According to the company :

With approximately 61% of the Company’s hotels achieving Q4 2022 RevPAR that met or exceeded Q4 2019 RevPAR, there is significant room for additional upside as business travel strengthens, leisure travel remains strong, and the recovery expands into additional markets.

One would think that high inflation in 2022 (and 2023 so far) would have pressured hotels. After all, hotel spending is highly cyclical and prone to consumer weakness.

However, that wasn't the case in 2022. The following comment from the company's 4Q22 earnings call reinforces the quote above:

Strong rate growth and effective cost controls despite the challenging labor and inflationary environment enabled us to achieve fourth quarter comparable adjusted hotel EBITDA of approximately $102 million and comparable adjusted hotel EBITDA margin of approximately 34%, down only 10 basis points to the fourth quarter of 2019. Actual adjusted hotel EBITDA margin for the fourth quarter was also 34%, but up 70 basis points to 2019, highlighting the positive impact of our transactional activity since the onset of the pandemic.

That said, 2023 is likely to be more challenging. Yet, the company is still in a good spot to improve its business.

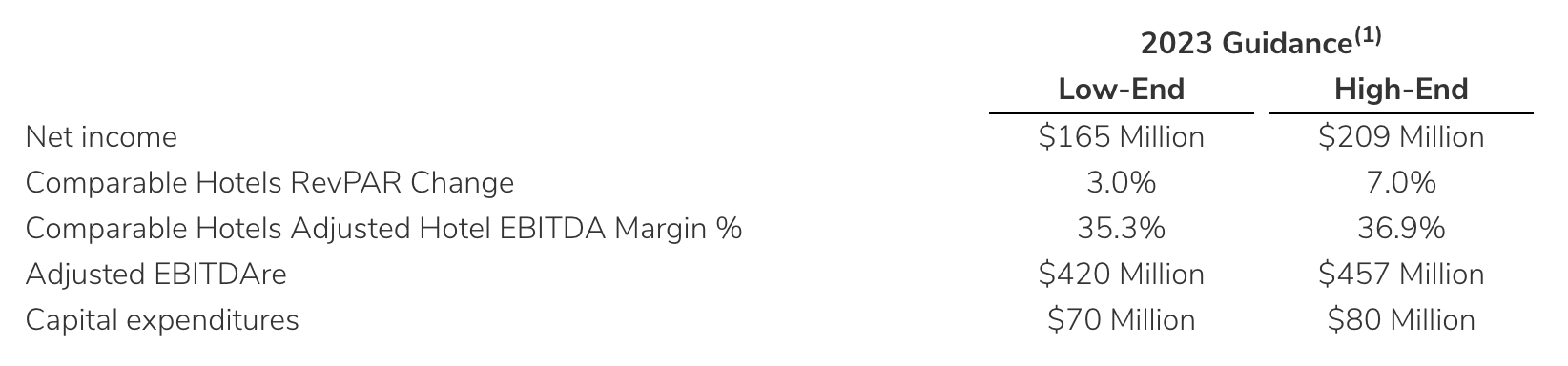

In the same earnings call, the company provided an outlook for 2023, acknowledging limited visibility into future performance due to short-term booking windows and macroeconomic uncertainty.

As a result, their outlook reflects a broader range of RevPAR change and other key metrics for 2023. Despite current forward booking data not indicating a slowdown, Apple Hospitality anticipates that the lodging industry recovery may be impacted by macroeconomic headwinds in the latter part of the year. They expect net income for the full year to be between $165 million and $209 million, with comparable hotels' RevPAR change ranging from 3% to 7%.

{kind=link}

Apple Hospitality

Note that the company generated $413 million in 2022 adjusted EBITDAre, which implies 6% expected growth using the midpoint of the company's guidance.

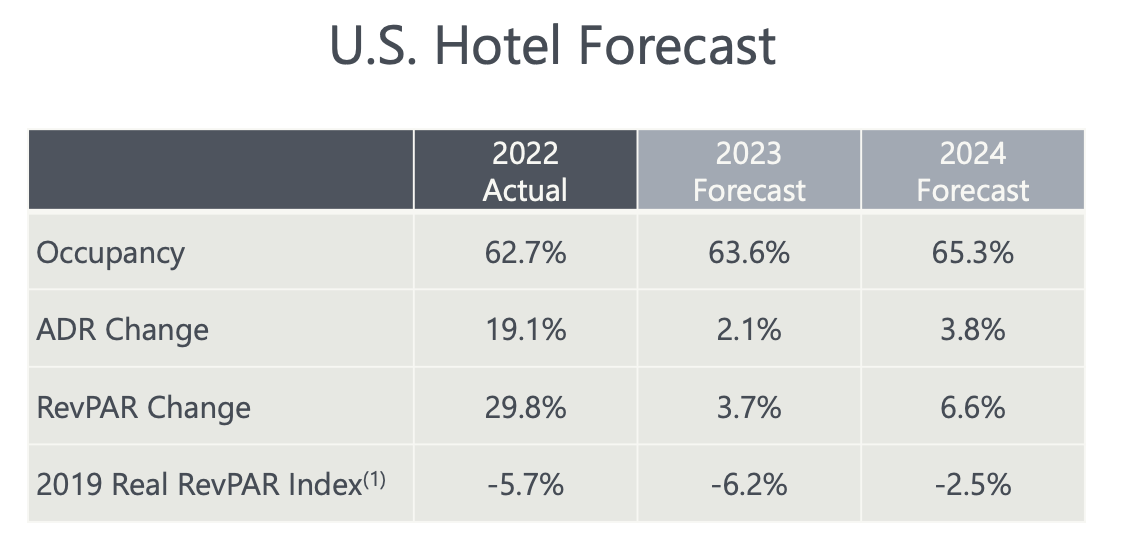

In 2023, the company expects a higher occupancy rate versus 2022 and a positive average daily rate change.

{kind=link}

Apple Hospitality

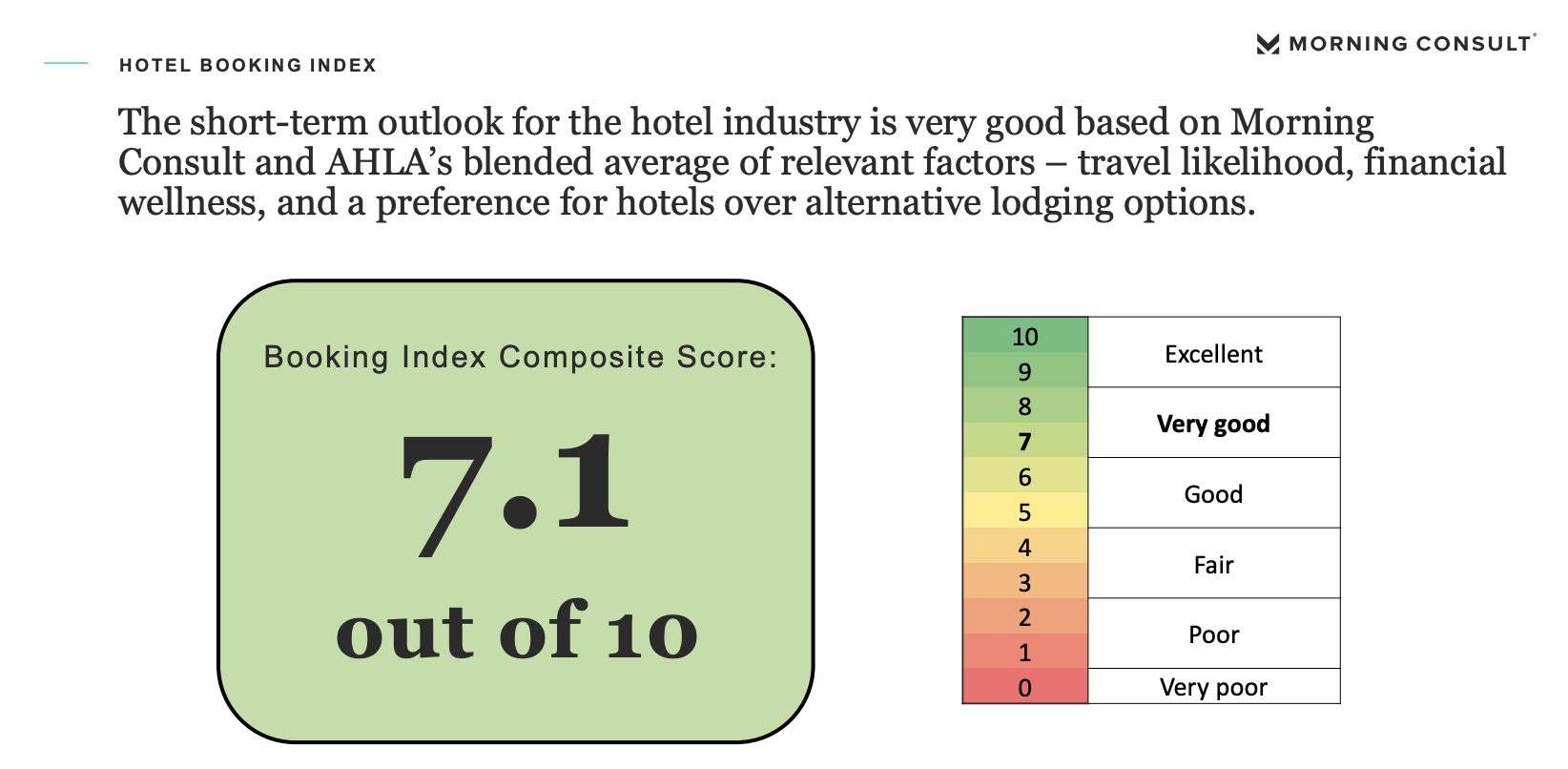

This outlook is supported by a supportive score from the 2023 Travel Outlook, provided by the Morning Consult Hotel Booking Index. Based on the travel likelihood, financial wellness, and preference for hotels over alternative lodging options, the industry scores a 7.1 (out of 10).

{kind=link}

Morning Consult

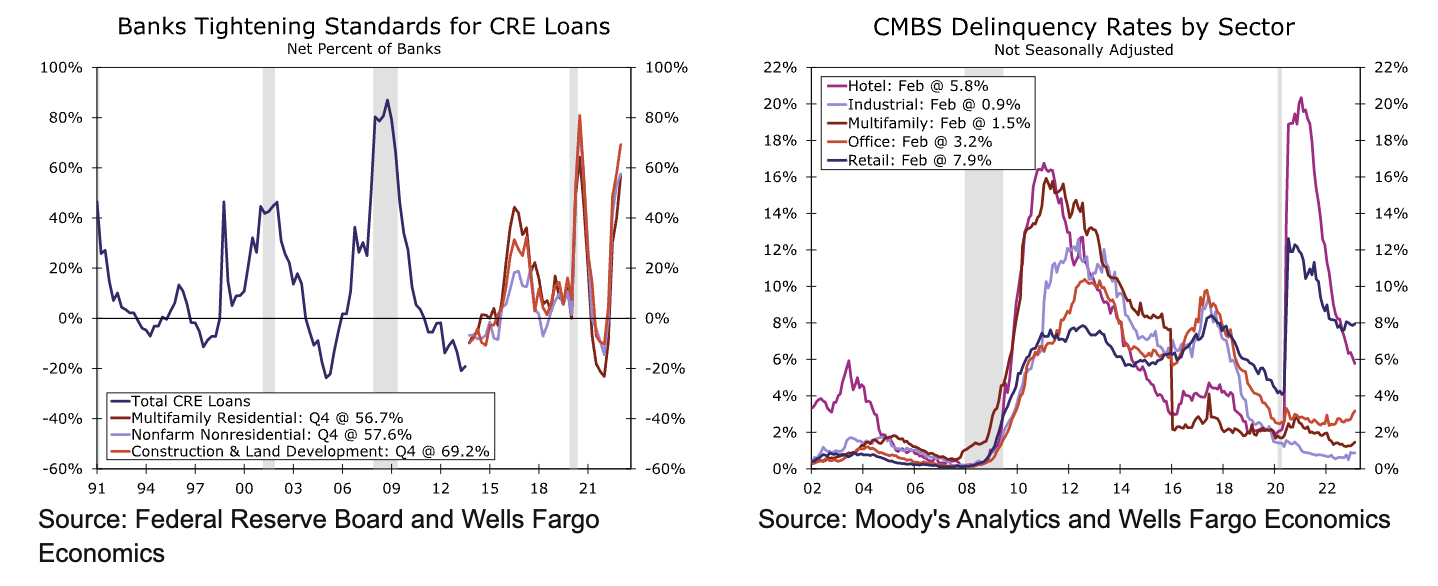

Furthermore, despite the adverse effects of high rates on the commercial real estate sector, there is a silver lining for the hotel industry, as delinquency rates are showing signs of improvement. Although 5.8% is still considered elevated, the sector is witnessing a decline in delinquency rates compared to other segments, thanks to tighter lending standards and positive momentum gaining traction.

{kind=link}

Wells Fargo

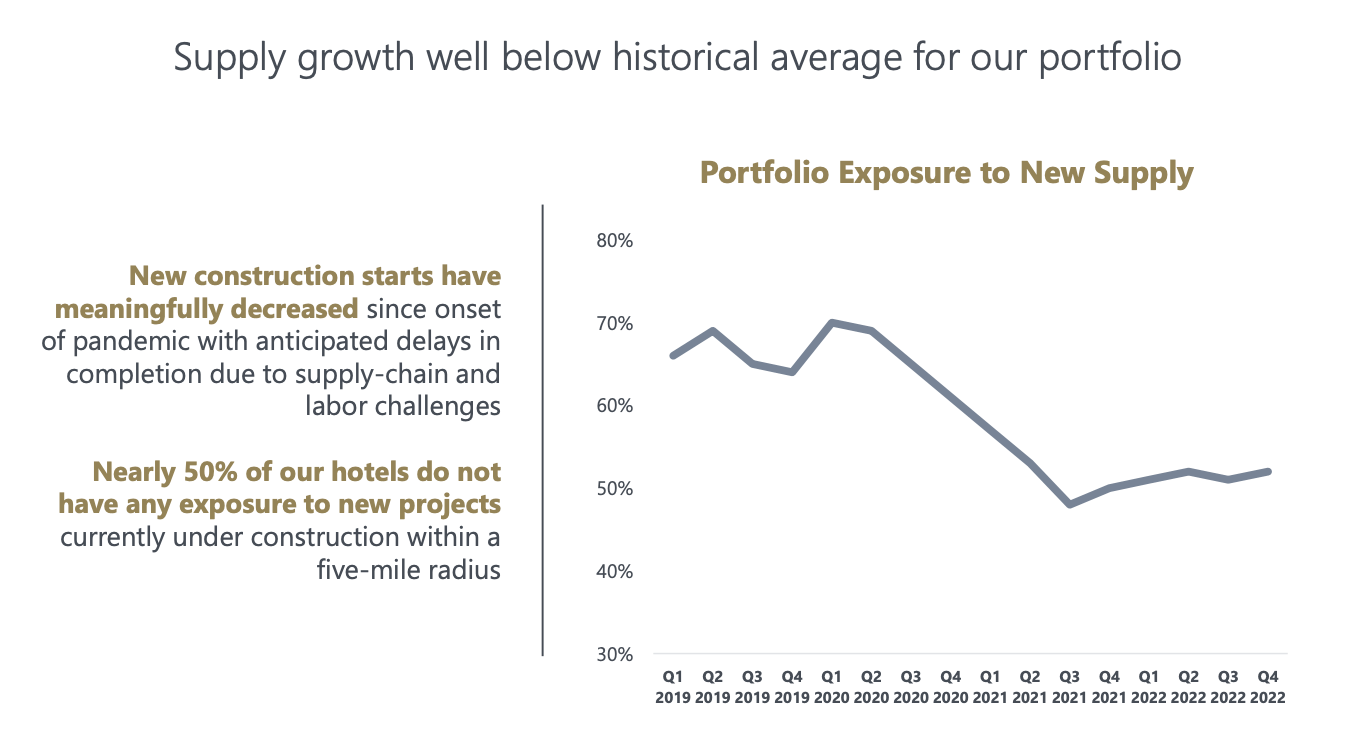

If anything, the pressure of higher rates on the industry is supporting APLE's pricing power. New construction starts are down. Only 50% of APLE's hotels are subject to new projects within a five-mile radius.

{kind=link}

Apple Hospitality

That said, these developments would be useless if the company had a weak balance sheet.

Thankfully, that is not the case.

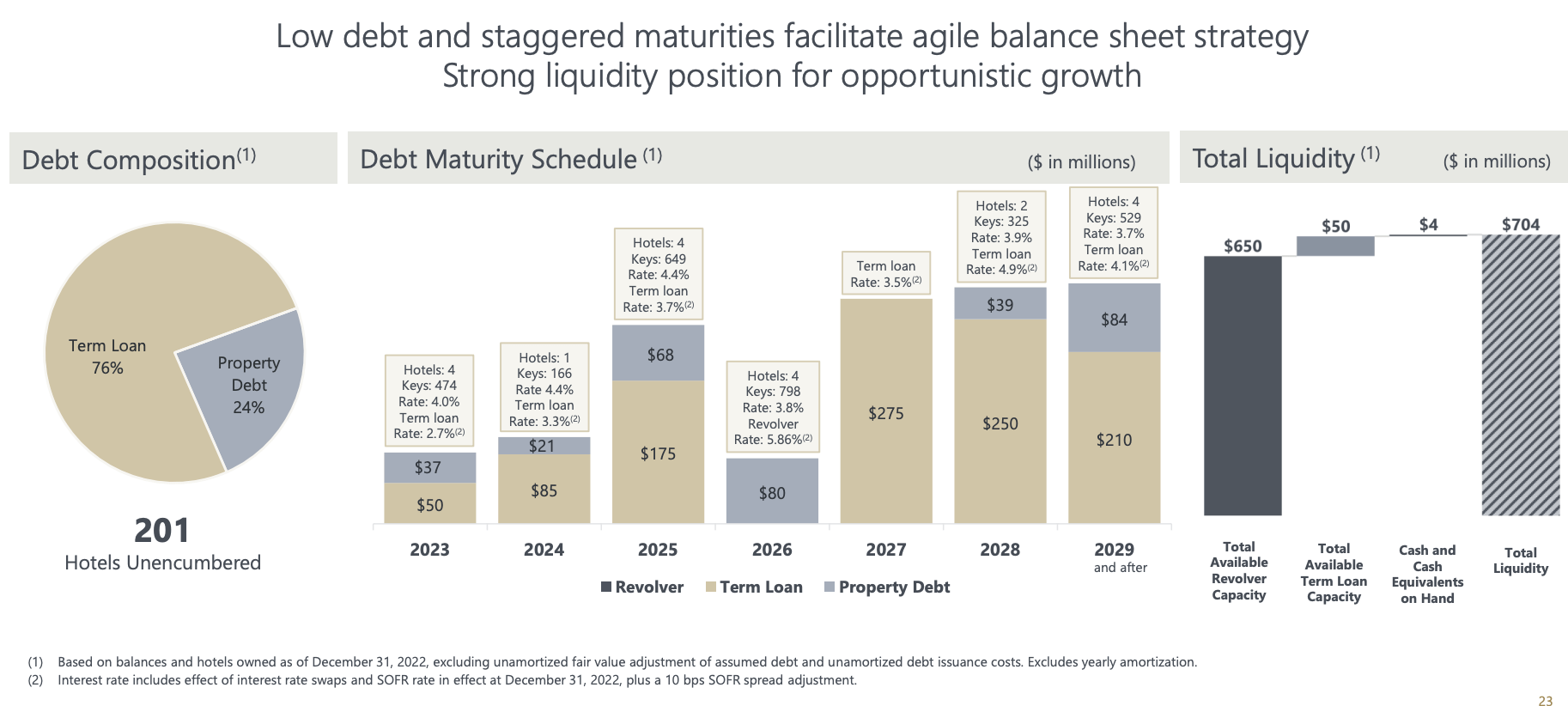

Apple Hospitality, in its 4Q22 earnings call, reported that as of December 31, 2022, it had $1.4 billion in outstanding debt, with a debt-to-EBITDAre ratio of 3.3x and a weighted average interest rate of 3.9%. The outstanding debt consisted of $329 million in property-level debt secured by 19 hotels and $1 billion in unsecured credit facilities. The weighted average debt maturities were nearly five years. In other words, the company has a relatively low average interest rate and a lot of time to wait for better financial conditions. It's not forced to boost lending in the current high-rate environment.

{kind=link}

Apple Hospitality

Furthermore, Apple Hospitality had cash on hand of approximately $4 million, with the availability of approximately $650 million under its revolving credit facility and $50 million under its term loan. 84% of its total debt was fixed or hedged. This, too, is confirmation that APLE is well-protected against the current high-rate environment.

Valuation & Relative Performance

What's interesting is that despite its massive downturn in 2020, the company has erased a lot of its underperformance versus the Vanguard Real Estate ETF ( VNQ ) benchmark.

Note that VNQ started to decline in early 2022. APLE has remained fairly unchanged since then - despite cyclical risks facing the hospitality industry.

Going forward, I expect APLE to outperform VNQ, with a big part of this outperformance coming from its juicy dividend.

That said, APLE is currently trading at 10.1x FFO. Historically speaking, the median is close to 11x, although it's hard to see in the chart below (thanks to the pandemic). The sector median is 12.5x, which means that APLE trades at a discount.

While a slight discount is appropriate, I believe that APLE is undervalued, especially because the forward valuation is just 9.6x FFO.

FINVIZ

Hence, I believe that APLE shares should be trading at $18. The current consensus target is $18.70. In March, Wells Fargo lowered its price target to $17, maintaining an overweight rating.

Takeaway

In this article, we discussed Apple Hospitality, a hotel giant that continues to fly under the radar. While it is far from risk-free dividend income, I like the value this company brings to the table. It has a juicy 6.2% dividend yield, backed by a healthy balance sheet and a pristine portfolio of top-tier hotel assets that benefit from the ongoing post-pandemic recovery.

In addition to a 6.2% yield, I expect that the subdued payout ratio will cause the company to hike its monthly dividend to $0.10, which would imply a 7.7% yield.

In my view, APLE shares are currently trading at an undervalued price, with the potential for an upside to $18 per share. Nevertheless, it's important to note that there is a possibility of new corrections. If economic conditions worsen, there could be a potential downward movement toward the $12-$14 range.

That said, investors looking for a juicy real estate yield might benefit from taking a closer look at this hospitality giant.

For further details see:

Apple Hospitality: An Impressive Monthly High-Yield Play