APLE - Apple Hospitality REIT: A Healthy Fruit

2023-08-17 08:26:44 ET

Summary

- Apple Hospitality REIT is one of the largest hospitality REITs in the US, with a portfolio of 220 hotels and close to 29,000 rooms.

- The company had a strong first half to the year, with increases in average daily rate and revenue per available room compared to the same period last year.

- Apple Hospitality REIT has a low dividend payout ratio and a history of increasing dividends, suggesting potential for future dividend increases.

Introduction

I have covered Apple Hospitality REIT (APLE) several times in the past, most recently in May . In that article, I changed my rating on the company from a "Hold" to a "Buy", with the belief that the shares were undervalued and provided an attractive entry point. Since my article, the company has lagged behind the S&P 500 slightly. With the recent release of the company's Q2 2023 earnings earlier this month, I will evaluate the company again to determine if my viewpoint on the company has changed.

Seeking Alpha

The Portfolio

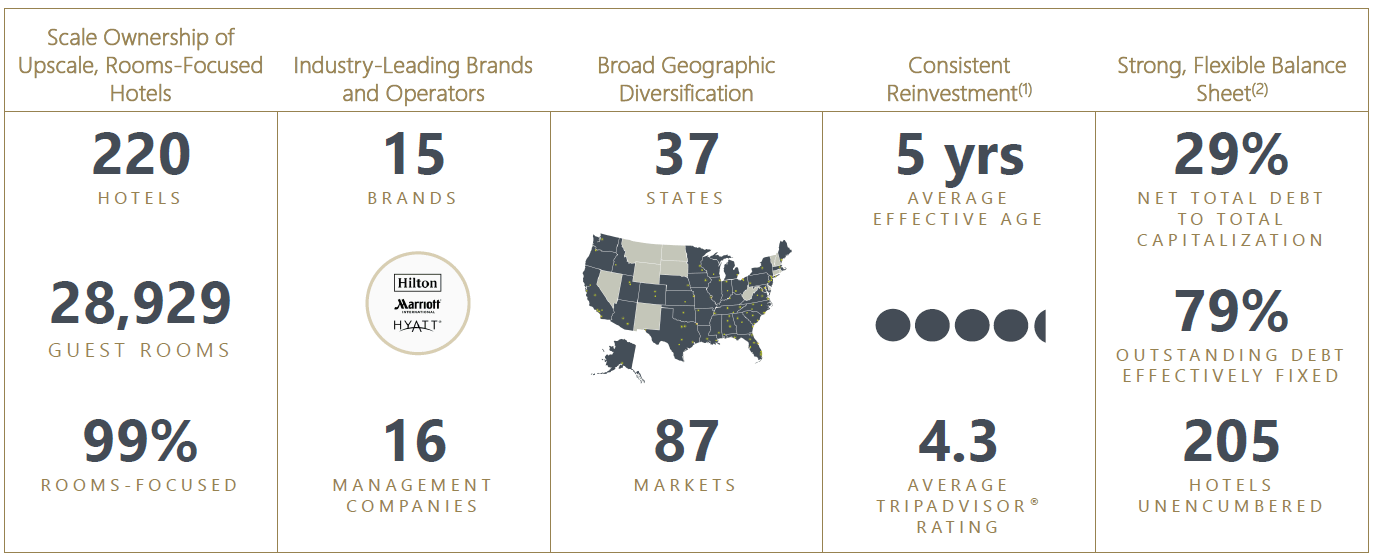

Apple Hospitality REIT, an internally managed select-service REIT, is one of the largest hospitality REITs in the country, both in terms of the number of hotels and the number of rooms. As of Q2 2023, the company's portfolio comprises 220 hotels and close to 29,000 rooms. Its hotels are rooms-focused, meaning the company derives the majority of its revenue from the sale of rooms. Its hotels are operated under prominent brands such as Marriott and Hilton, allowing the company to tap into the strong reservation systems and loyalty programs of these brands.

The company's portfolio of hotels are geographically diversified, strategically spread across 87 markets in 37 states. This allows the company to smooth out any fluctuations from volatility in a particular region. Additionally, the company continually "refreshes" its hotels by reinvesting in them, with its hotels having an average effective age of 5 years. This ensures its hotels are able to maintain their competitive edge.

{kind=link}

Q2 2023 Earnings

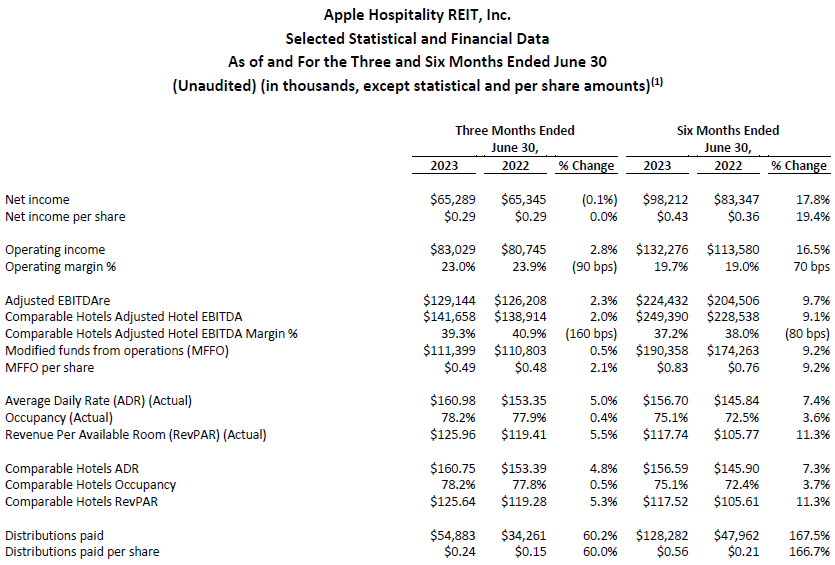

Earlier this month, the company reported its results for the second quarter. The average daily rate (ADR) for comparable hotels increased by 4.8%, coupled with an even larger increase of 5.3% in its revenue per available room (RevPAR) when compared to the same period last year. Looking at the first half of the year as a whole, the company saw a 7.3% increase in ADR and an even larger 11.3% increase in RevPAR compared to the first half of 2022.

In terms of net income, the net income for Q2 2023 was roughly flat compared to Q2 2022, with approximately $65.3 million for both periods or $0.29/share. However, looking at the first half of the year as a whole, there was a substantial increase in net income, from $83.3 million ($0.36/share) for the first half of 2022 to $98.2 million for this year ($0.43/share). The company's modified funds from operations (MFFO) also saw an improvement compared to the prior year - MFFO for Q2 2023 and the first half of 2023 was $0.49/share and $0.83/share respectively, a 2.1% and 9.2% increase respectively compared to the same periods last year.

{kind=link}

Following the release of its Q2 2023 results, the company revised its guidance for the FY 2023. The company now projects comparable hotels RevPAR growth of between 4% and 8%, up from the initial estimate of between 3% and 7%. There was also a slight increase in the guidance for comparable hotels adjusted EBITDA margin. However, amidst this increased outlook for growth, the company also adjusted its projections for net income and adjusted EBITDAre downwards due to heightened anticipated general and administrative expenses. Net income is now projected to fall between $163 million and $202 million, down from the initial estimate of between $165 million and $209 million.

Nevertheless, it is important to note that despite the adjusted projections, the company is still poised to surpass its performance for the FY 2022. To give some context, the FY 2022 net income came it at just under $145 million, well below even the low end of the revised guidance.

{kind=link}

Dividend

Apple Hospitality REIT had a monthly dividend payout structure, with the company maintaining a consistent monthly dividend of $0.08/share for the quarter, translating to an annualized dividend of $0.96/share. When assessed against the current share price of $14.74, this gives the company an attractive dividend yield of 6.5%. This dividend yield is comfortably covered by the company's MFFO, highlighting the company's ability to sustain its dividend distribution. Looking at the first half of the year, the company's dividend payout of $0.48/share for the period translates to a dividend payout ratio of 57.8% based on the MFFO of $0.83/share for the period.

Considering the low dividend payout ratio, the prospect of future dividend increases comes into view. Before that though, it is worth taking a look at the company's dividend history. For many years, from 2015, the company consistently delivered a monthly dividend of $0.10/share. However, the pandemic led to a suspension of dividends, with only sporadic payments of $0.01/share during that period. For instance, the company only paid out $0.04/share in dividends for the whole of 2021. However, that changed in 2022 when the company resumed its monthly dividends. The company initially paid a monthly dividend of $0.05/share, followed by an incremental increase to $0.07/share in the latter half of the year. The latest dividend of $0.08/share was announced for November 2022, a level the company has maintained since.

In light of the company's previous history of paying a $0.10/share dividend, its recent willingness to increase its dividends recently and, most significantly, its low dividend payout ratio, it is entirely plausible that the company will increase its dividends in the near future.

Balance Sheet

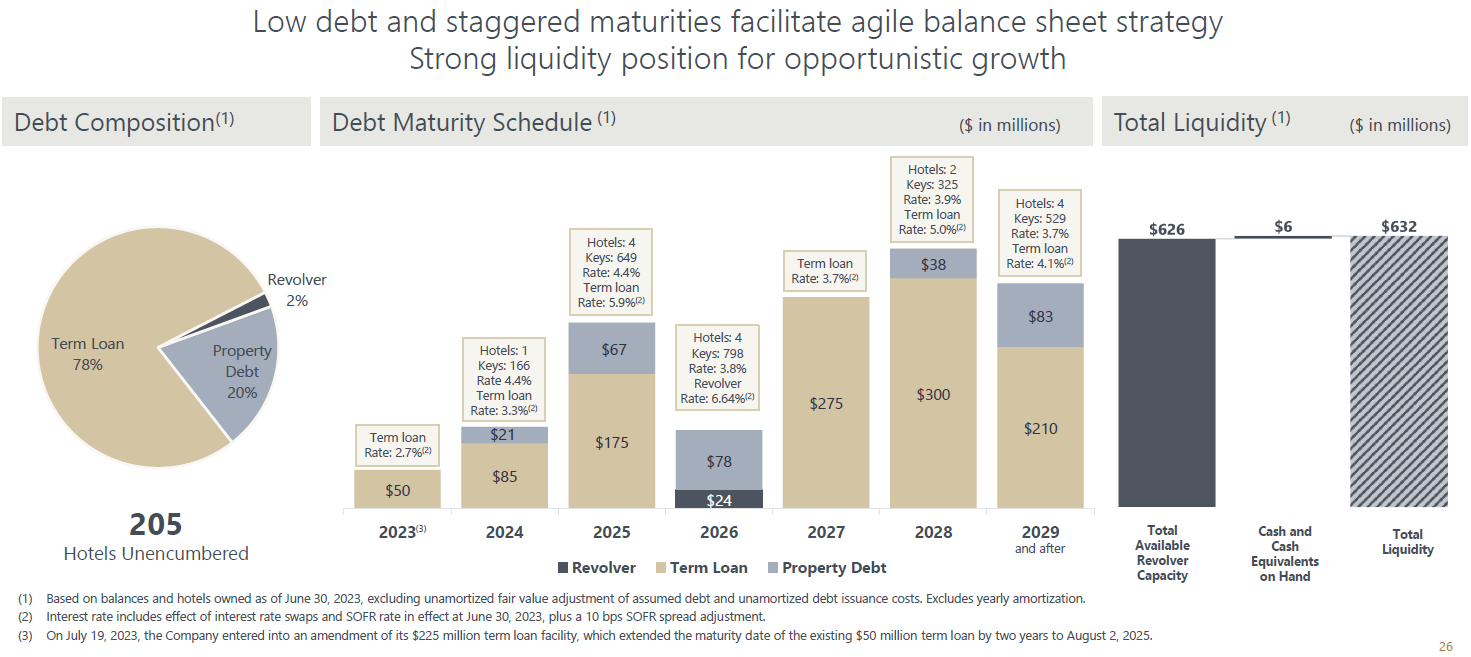

Moving on to the company's balance sheet, the company had $1.4 billion in outstanding debt as at Q2 2023, with a weighted average maturity of 4.1 years and a weighted average interest rate of 4.35%. Of this debt, approximately $287 million is secured by 15 of the company's hotels, with the remaining $1.1 billion outstanding on the company's secured credit facility. A sizable proportion of the company's debt, at 79%, is fixed debt, which serves as a safeguard against fluctuations in interest rates.

The image below shows a fairly well-distributed debt maturity schedule. It should also be noted that subsequent to quarter end, the company extended the maturity of its existing $50 million loan from 2023 to 2025, thus there are actually no more maturities for the rest of the year and just over $100 million due next year.

Apart from a well-managed debt schedule, the company stands in a strong liquidity position. Though the company currently maintains only $6 million in cash, it has a substantial $626 million available to it under its revolving credit facility. This ensures that the company is well-equipped to fulfill its debt commitments over the coming years. Furthermore, this financial flexibility positions the company to seize any opportune moments to pursue any accretive transactions to enhance its portfolio.

{kind=link}

Share Price and Valuation

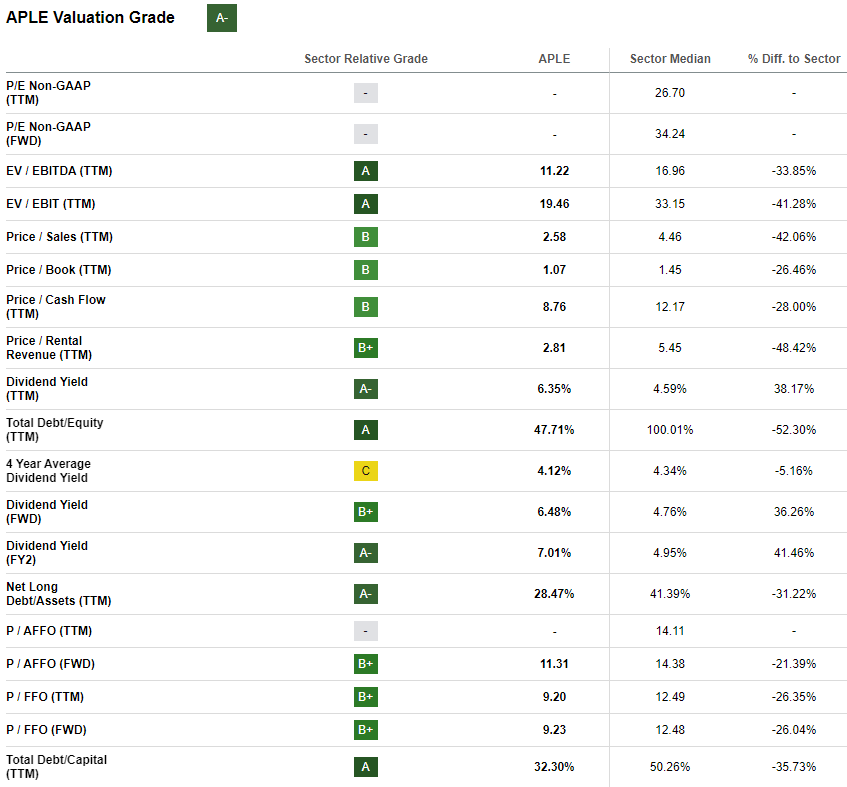

The Seeking Alpha quant system gives the company an "A-" rating in terms of valuation, highlighting its value in comparison to its peers in the hospitality industry based on various valuation metrics. Both the company's price-to-book ratio (P/B ratio) and price-to-AFFO ratio, or in this case price-to-MFFO ratio (P/MFFO ratio) are substantially lower than the sector median, indicating the company's shares are undervalued relative to its peers. This favorable valuation is also validated by the actions of the company. During the earnings call , it was mentioned that that the company had purchased approximately 226,000 shares at a weighted average price of $14.47/share. This is a continuation of the previous quarter, whereby the company repurchased 250,000 shares at a weighted average price of $14.22/share. These shares were purchased under the company's share repurchase program, with approximately $335 million remaining in this program. These actions serve to indicate that the management believes the current share price to be undervalued.

{kind=link}

Another aspect to consider would be the company's historical performance over the past year. At its current price of $14.74, the company's shares are close to its 52-week lows of approximately $14, which suggests the potential for further upside. Of course, even if the share price does not increase, one could do worse than collecting the 6.5% dividend yield in the meantime.

Conclusion

When I last wrote about the company in May, I had a "Buy" rating on the company with the belief that the company's shares were undervalued. While the shares initially appreciated, it has subsequently come back down towards the level back in May. With no changes in the company's fundamentals, I maintain my "Buy" rating on the company.

For further details see:

Apple Hospitality REIT: A Healthy Fruit