APLE - Apple Hospitality REIT: Recovering Well With A 6.6% Dividend Yield

2023-05-28 01:04:13 ET

Summary

- Apple Hospitality REIT is a hotel REIT with industry-leading tenants.

- It has been recovering well after the pandemic.

- My analysis leads me to a buy rating for APLE stock.

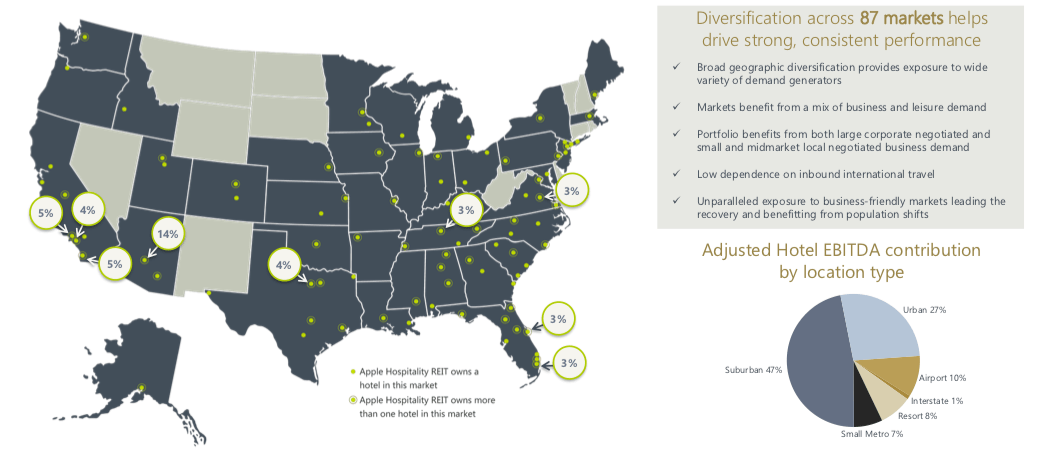

Apple Hospitality REIT ( APLE ) is a room focused hotel REIT with industry leading brands such as Hilton ( HLT ), Marriott ( MAR ), and Hyatt ( H ). They own 220 hotels and are present in 87 markets in 37 US states. 47% of their portfolio is located in suburban and 27% in urban areas. An advantage that APLE has is owning high-end hotel brands with higher income population as their target group. Because of this, even though the hotel sector struggled during the pandemic, the target (affluent) audience of these hotels, which was less likely to incur financial problems during the pandemic, could still travel.

Consequently the REIT was more insulated and rebounded quicker. Moreover, a lot of these hotels are used for business trips, which are now more common again.

{kind=link}

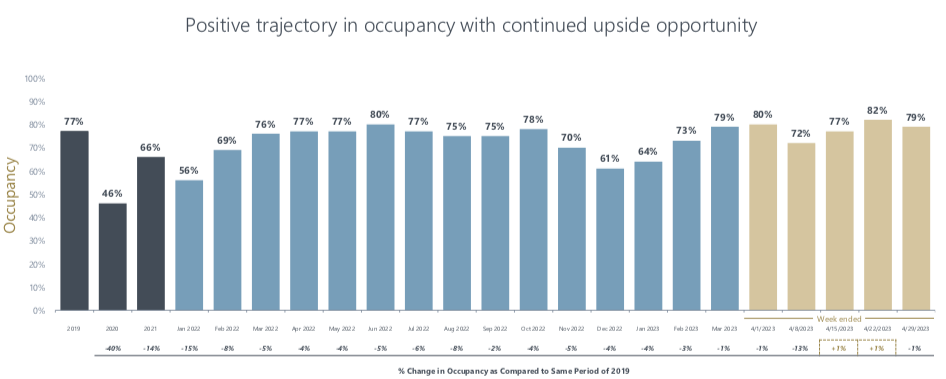

As expected, the REIT struggled during Covid, hence the 46% and 56% occupancy in 2020. However, it has been progressing a lot and occupancy has increased since the pandemic and is now close to 80%. As stated in the results , the occupancy has increased by 6.8% since 2022 but has not fully recovered yet as it is still down 2.8% since 2019 (pre-pandemic). But these are still great results for hotels as the average occupancy of hotels in the US was 65.3% in March of 2023. This again speaks to the quality of their portfolio.

{kind=link}

The company's same store revenue has increased as well by 17.5% since last year, on the other hand, their operating expenses increased also, by 17.3%. As for guidance, the net income is expected to be between $165-209 million compared to $144 million last year. The adjusted EBITDA is between $420-457 million compared to $413 million last year. I want to point out that APLE has the second best EBITDA margin in the industry, after Chatham Lodging Trust ( CLDT ), of 38%. This is significantly higher as peers tend to average around 30-33%.

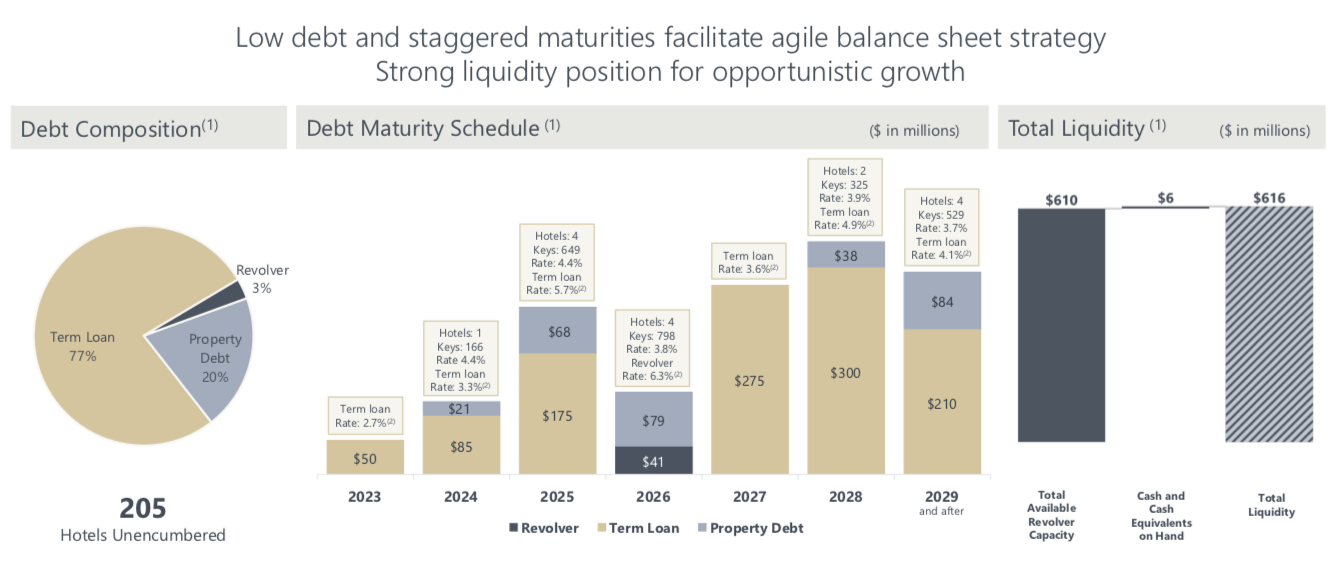

Now I would like to take a look at their balance sheet, because that’s often where the risk lies, especially in the current high interest rate environment. The company has an outstanding debt of $1.4 billion with a weighted-average interest rate of 4.3%. 84% of the debt is fixed. They have $6 million in cash and a revolving credit facility of $610 million. Their maturities for the next two years are on the lower side and the company can use their credit line to repay in the highly unlikely even that they will not be able to refinance. So overall a pretty solid balance sheet that the company should not have major issues with.

{kind=link}

Expectedly the dividend was cut during the pandemic down to a lowest point of $0.01 monthly in March 2021. But the company has been increasing it since then and it has reached pre-pandemic levels as it currently stands at $0.08 monthly so $0.96 annually. This translates to a 6.6% dividend yield and it is well covered with a payout ratio of around 70%. That’s pretty solid for a high quality REIT such as APLE.

APLE's P/FFO currently stands at 9.23x, trading below the historical average of 12.14x. FAST Graphs analysts expect an 8% growth this year and 4% going forward. For comparison, Summit Hotel Properties ( INN ) trades at 6.75x with a historical average of 11.65x. However, INN is a smaller company so I would consider APLE fairly valued here. Even assuming no multiple expansion, if we average the expected growth at 6% and add the 6.6% dividend, the stock could easily offer double digit returns and offers a way of diversifying ones exposure within REITs and also getting some exposure to the hotel business, without owning the hotel operators directly, which can be considerably more risky than being the landlord.

Overall, the company seems solid. They have been recovering well after the pandemic, have industry leading margins and have a manageable balance sheet which should give them plenty of flexibility. It is fairly valued towards peers but slightly undervalued compared to the historical average. So even though not without risk with a dividend yield of 6.6% and an expected double digit return, I rate APLE stock a BUY here at $14.5 a share.

For further details see:

Apple Hospitality REIT: Recovering Well With A 6.6% Dividend Yield