LRCX - Applied Materials: A Preview Of Upcoming Earnings In Light Of Severe Headwinds

2023-05-16 07:30:00 ET

Summary

- Applied Materials was vague about guidance in the last earnings call as competitors provided dour assessments for 2023.

- Applied Materials' main tailwind is a close synergy with TSMC in supplying equipment for the <7nm node market leader.

- AMAT’s 2.1% revenue increase underperforming the global 8.9% increase, while KLA’s share increased by 40.3% in 2022.

- Competitors KLA and Lam Research both guided down 20% last quarter and Applied Materials should be no exception.

Applied Materials ( AMAT ) is expected to report earnings on May 18 after market close. The report will be for the fiscal Q2 ending April 2023.

During fiscal Q1, Applied generated revenue of $6.74 billion. On a non-GAAP adjusted basis, the company reported on February 16, 2023 gross margin of 46.8%, operating income of $1.99 billion or 29.5 percent of net sales, and EPS of $2.03.

For Q2 of fiscal 2023, Applied expects net sales to be approximately $6.40 billion, plus or minus $400 million. Non-GAAP adjusted diluted EPS is expected to be in the range of $1.66 to $2.02.

Applied Materials expects its Semiconductor Systems' revenue to come in at about $4.84 billion, marking an 8% increase YoY.

Interestingly, in its guidance for Q2, AMAT noted ongoing supply chain challenges and a negative estimated impact of $250 million dollars related to a "cybersecurity event recently announced by one of its suppliers." I had previously noted in a February 16, 2023 Seeking Alpha article entitled " MKSI's Ransomware Attack Could Have Significant Implications For Applied Materials ."

My article was published at 10:57 am on February 16 and the earnings call was after 4:30 pm where MKS Instruments ( MKSI ) was mentioned. What is interesting is that Lam Research ( LRCX ) reported its fiscal Q3 2023 earnings on April 19, 2023 and the only mention of MKSI in the earnings call came from me in a comment on the Seeking Alpha-published earnings call transcript!

In this article, I present a comprehensive analysis of Applied Materials and its position in the semiconductor equipment industry.

Tailwinds for Applied Materials

China

China represents a strong growth area for AMAT, even as U.S. sanctions have imposed strong restraints on shipping advanced semiconductor equipment to the country, which are:

- Logic chips with non-planar transistor architectures (i.e., FinFET or GAAFET) of 16nm or 14nm, or below;

- DRAM memory chips of 18nm half-pitch or less;

- NAND flash memory chips with 128 layers or more.

Although these stipulations were set in place on October 7, 2022, sanctions had been put in place several years earlier. A little-known fact is that ASML sold an EUV system to China's SMIC in April 2018 with delivery at the end of 2019 and installation in mid-2020. Under pressure from the U.S., the Dutch government caved and blocked the deal.

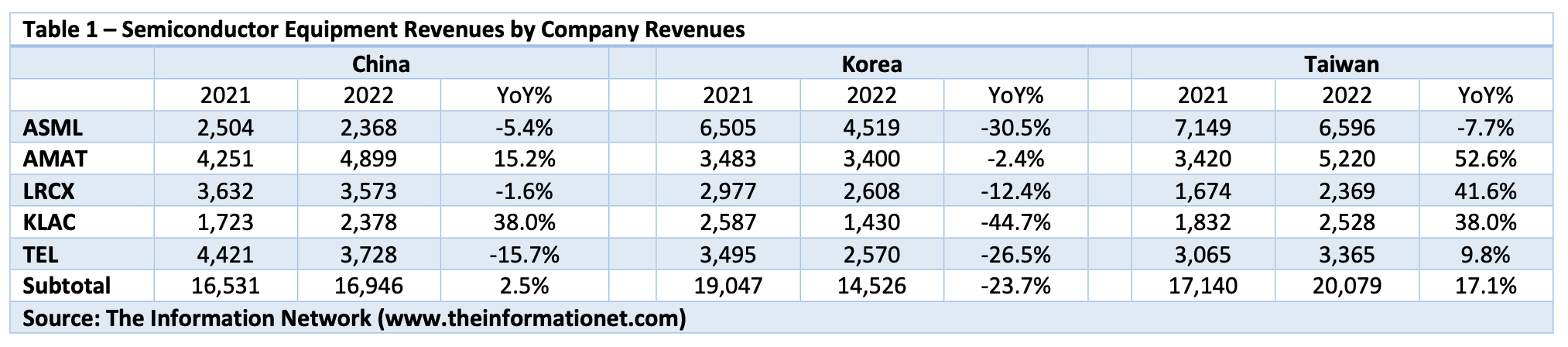

Table 1 shows the YoY WFE revenues change by the Top 5 equipment companies in 2022 from sales to China, Korea, and Taiwan.

{kind=link}

On a revenue basis, Applied Materials had the greatest exposure, but, on a percentage of revenue basis, Lam Research and Tokyo Electron ("TEL") ( OTCPK:TOELY ) had the greatest exposure.

This is important. With U.S. sanctions against China continuing to be expanded, these three companies will be most impacted in 2024. But all these companies will experience an impact. Table 1 shows that the % of revenues for all companies decreased QoQ in Q4 2022.

There are several takeaways:

For China, despite ongoing sanctions, equipment revenues for the Top 5 companies increased 2.5% YoY. KLA (KLA) had the greatest increase in YoY revenue growth at 38.0% followed by AMAT at 15.2%. Demand from China came from foundry SMIC as it purchased equipment not only for 14-28nm nodes but for 7nm and below.

For Korea, revenues were -23.7% for the year, tied to the downturn in capex spend by SK Hynix. KLAC fared the worst at -44.7%, but these negative YoY revenues are tied to those of ASML, which was down 30.5%. The need for KLAC is greatest at smaller nodes, since the price of a completed wafer is greater at the small nodes, resulting in the need for KLAC's inspection equipment. SK Hynix and Samsung Electronics ( OTCPK:SSNLF ) have moved to EUV lithography for DRAMs, and Samsung has moved to EUV in its foundry business, establishing a synergy between ASML and KLAC.

Artificial Intelligence

Generative Artificial Intelligence, of which ChatGPT has taken all the air out of the room in the past several months, has become a hot topic. Nvidia ( NVDA ) is the leading chip company supplying its A100 and H100 GPUs as the brains behind not only ChatGPT but by hyperscalers developing generative AI to stay competitive by accelerating the roll out of AI processes for their own applications.

I already discussed Generative AI in my February 24, 2023 Seeking Alpha article entitled " TSMC Makes The Chips, But Nvidia Gets The Glory."

What is important is that Nvidia's chips, and most other AI accelerator chips, are made by Taiwan Semiconductor (TSMC) ( TSM ) foundries. Importantly for AMAT, as shown above in Table 1, the company had strong exposure to Taiwan through its sales to TSMC.

For Taiwan, the need for equipment for TSMC's <5nm nodes using EUV lithography again corresponds to a synergy between EUV lithography for <7nm and the processing equipment from AMAT and LRCX and the inspection equipment from KLAC. The high exposure of these three equipment companies to Taiwan and TSMC's lead in <5nm are positive tailwinds.

Headwinds for AMAT

Underperformance Against Peers

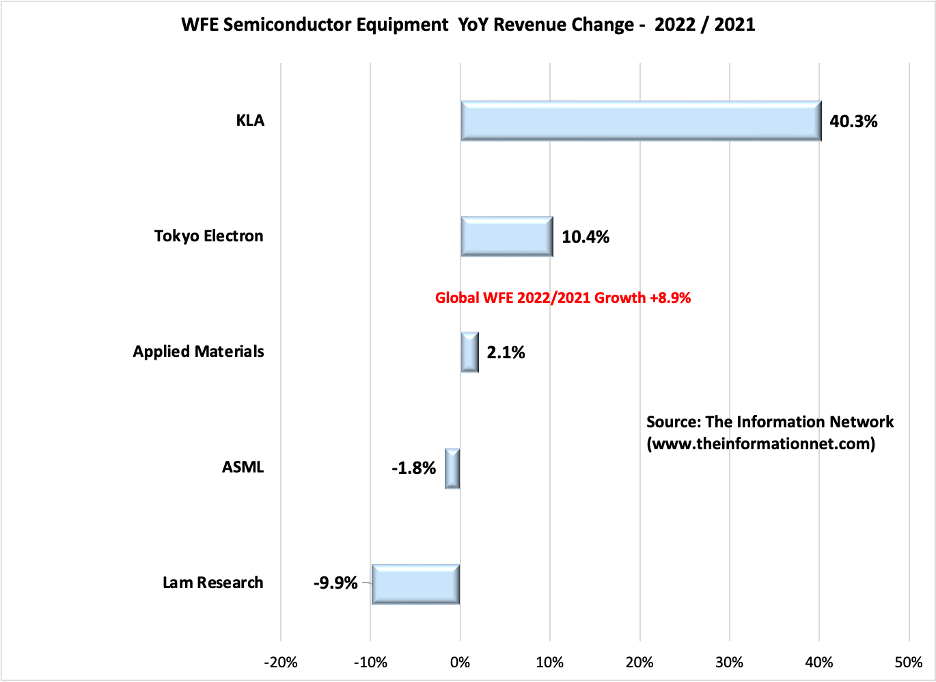

Applied Materials may be the largest semiconductor manufacturer, but the company continues to underperform competitors based on YoY equipment revenue growth. Chart 1 shows YoY wafer front end ("WFE") semiconductor equipment revenue growth for 2022 based on a bottom-up analysis of all companies. This revenue growth is for semiconductor equipment only and does not include service, spare parts, or non-semiconductor business segments.

Applied Materials revenue grew 2.1%, underperforming the overall WFE semiconductor equipment market, which grew 8.9% to $95.0 billion in 2022 from $87.2 billion in 2021, according to The Information Network's report entitled " Global Semiconductor Equipment: Markets, Market Shares and Market Forecasts . "

Chart 1 shows that not only did AMAT lose market share against KLA ( KLAC ) with a 40.3% YoY growth, a major competitor in metrology/inspection equipment, but also TEL, a major competitor in deposition and etch equipment.

{kind=link}

Chart 1

China Long Term

While exposure to China is a near-term tailwind as discussed above and shown in Table 1, in the long term, an expanding domestic China equipment suppliers will be a headwind.

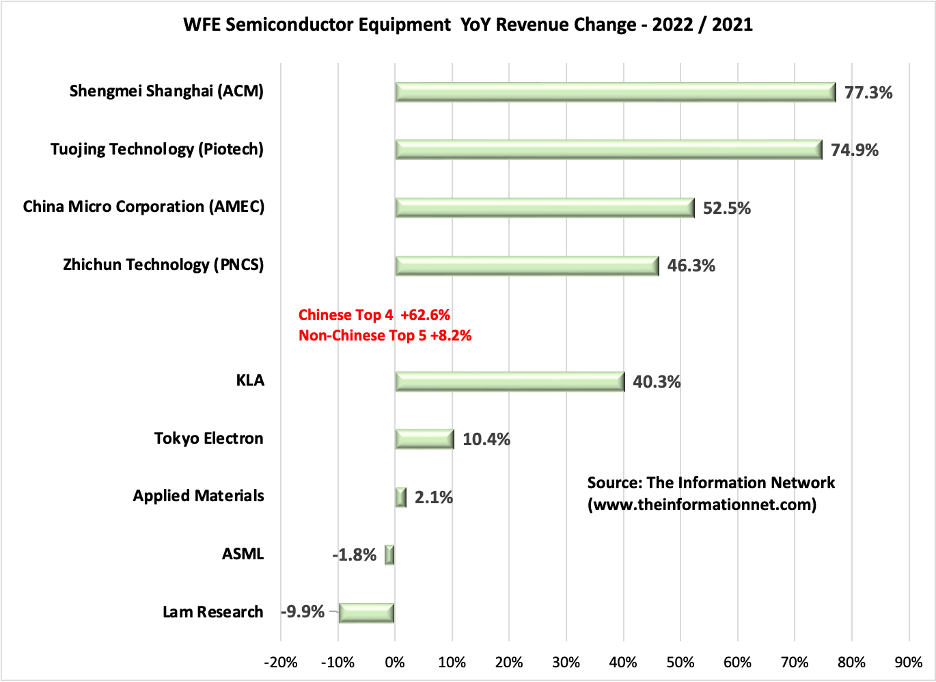

Chart 2 shows AMAT's performance compared to Chinese and non-Chinese equipment companies, showing YoY growth for 2022 versus 2021. There are two takeaways from the Chart:

- The mean growth for the Top 5 non-Chinese companies was 8.2%, and AMAT's performance of just 2.1% indicates a significant underperformance against other top WFE competitors..

- The mean growth for Chinese companies was 62.6%, indicating that Chinese equipment companies are gaining in the market, although their revenues are significantly lower than non-Chinese counterparts, according to The Information Network's report entitled " Mainland China's Semiconductor and Equipment Markets: Analysis and Manufacturing Trends ."

{kind=link}

Chart 2

Equipment Revenue Meltdown in 2023

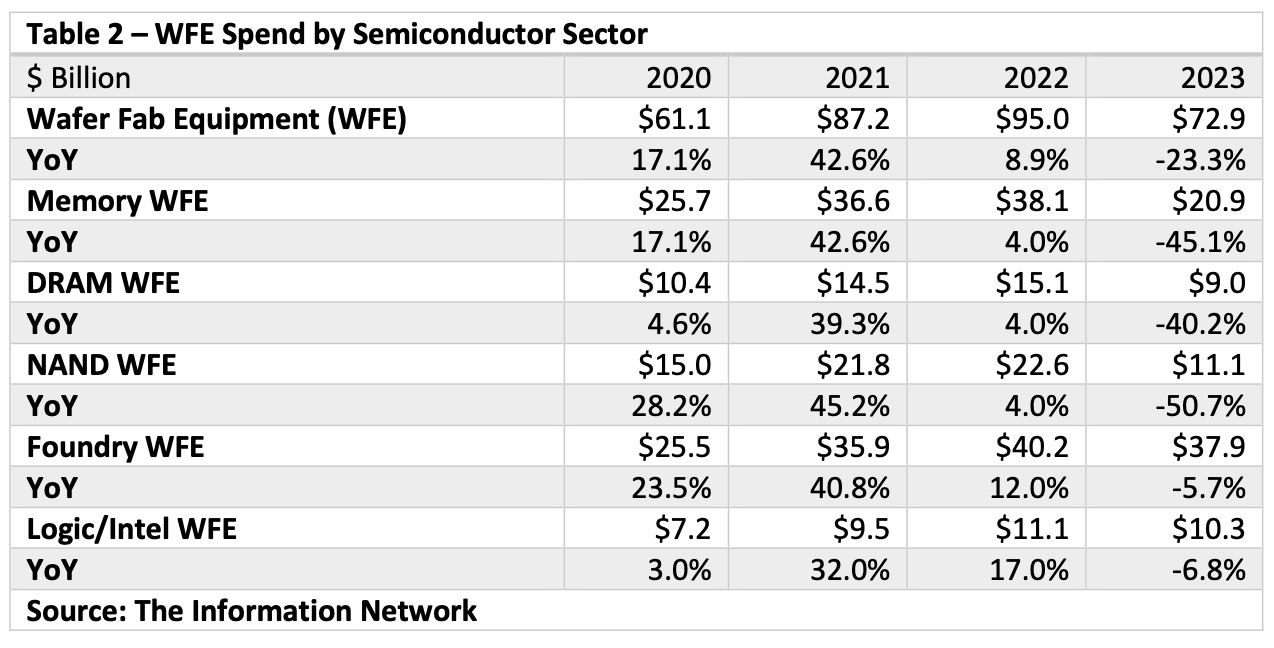

In Table 2, I present my analysis of the WFE spend by semiconductor sector from 2020 to 2023.

I continue to call for a significant semiconductor equipment revenue collapse in 2023, which I first detailed in my July 25, 2021 Seeking Alpha article entitled " Applied Materials: Tracking A Likely Semiconductor Equipment Meltdown In 2023 ."

{kind=link}

In that mid-2021 article I warned that excessive capex spend would give rise to an oversupply of semiconductors and a drop in equipment spending in 2023. The poor fiscal and monitory policy coming from the U.S. Fed has pulled in the downturn into 2022, particularly in the Memory sector. WFE spend for memory dropped from a +42.6% growth in 2021 to just 4.0% in 2022 and I forecast -45.1% in 2023.

Investor Takeaway

AMAT should beat consensus at its Thursday earnings call. Short term is positive for the company. There are also positive tailwinds from fab builds as a result of the U.S. Chips Act, with an additional eight National Chip Incentive Programs across the world as I discussed in my January 18, 2023 Seeking Alpha article entitled " KLA Corp.: My Top Equipment Company With Strong Tailwinds From National Chip Incentive Programs ."

In addition, capex and WFE spend has been responsible for the crash of the memory market, first by excessive capex spend in 2020 and 2021 causing oversupply memory chips followed by macroeconomic factors that significantly reduced demand. Poor fiscal and monetary policy by the U.S. Federal Reserve has exasperated the economic situation in the U.S., which has also impacted other countries, where people are choosing to spend discretionary money on food and fuel rather than electronic gadgets needing chips.

Much of AMAT's revenues come from Taiwan foundry TSMC, and equipment sale pull-ins from TSM buoyed AMAT's revenues in CY Q4 2022, particularly at <5nm nodes. Unfortunately, TSM has cut back capex spend, which would decrease to $32-36 billion in 2023 from $36.3 billion in 2022 following guidance for a first quarter 2023 revenue drop as much as 5%.

Investors need to "separate the wheat from the chafe" when listening to AMAT's earnings call, particularly guidance. Statistically they underperformed top competitors in 2022 and yet management stated they are in a "very strong position" in 2023 when KLAC and LRCX both guided down 20%.

Frankly, after analyzing AMAT since 1985, I don't concur, and rate the company a Sell.

For further details see:

Applied Materials: A Preview Of Upcoming Earnings In Light Of Severe Headwinds