GFS - Applied Materials Q3 Earnings: ICAPS And Service Revenues Drive Surprising Resiliency

2023-08-21 08:40:26 ET

Summary

- Applied Materials delivered resilient Q3 results, outperforming expectations and showcasing its ability to weather industry fluctuations.

- The company's focus on ICAPS and growing services segment contribute to its continued outperformance and reduced cyclicality.

- AMAT's commitment to R&D investments, shareholder-friendly capital allocation, and leadership in advanced technologies make it an attractive proposition for investors seeking growth and stability.

- The recent outperformance and solid outlook allow me to upgrade my rating.

Investment thesis

I upgrade my rating on Applied Materials, Inc. (AMAT) stock to a Buy following the company’s Q3 results, which blew past the consensus. Applied Materials delivered a very resilient performance and believes it should continue to be able to report resilient YoY growth rates despite a downturn in the semiconductor equipment industry.

This is what I previously wrote about the company:

Applied Materials is a global leader in semiconductor manufacturing equipment. With a strong market position and a comprehensive product portfolio, the company caters to the demand for faster and more efficient chips, supporting innovative technologies like AI, 5G, and autonomous vehicles. Its revenue is driven primarily by the semiconductor systems segment, supported by a growing services segment with recurring revenues from long-term agreements. Moreover, Applied Materials maintains a shareholder-friendly approach with consistent dividend hikes and share buybacks, backed by strong cash flow generation.

While facing challenges from Chinese export restrictions and industry cyclicality, Applied Materials shows resilience and long-term growth potential. The company's commitment to research and development positions it for future advancements and market dominance. The semiconductor industry is projected to grow significantly over the next decade, which should benefit Applied Materials through increased demand for semiconductor manufacturing equipment.

I was quite bullish on the company when I covered it for the first time a few weeks ago and the investment case has improved further over recent weeks as AMAT delivered outstanding financial results for its fiscal third quarter. The results highlighted several essential developments within the business, including a larger focus on anti-cyclical service revenues and the company’s early efforts into ICAPS paying off, offering improved resiliency.

Long story short, the company is delivering much more resilient quarterly results as the business is visibly becoming less cyclical, further fueling its long-term attractiveness for investors.

If you are unfamiliar with the company and its structure, I recommend reading my initial article on the company to get a better understanding of it.

This article will be a quick update on my recently introduced thesis following the blowout Q3 results and incorporating its improved resiliency in my financial projections.

AMAT’s financials are turning out to be less cyclical than anticipated

I recently initiated my coverage of Applied Materials with a hold rating following my in-depth analysis of the company and the semiconductor equipment industry outlook. As the semiconductor industry continued to struggle for traction and semiconductor manufacturers lowered their Capex plans, as highlighted by the fact that manufacturers like GlobalFoundries ( GFS ) and TSMC ( TSM ) guided for Capex at the low end of their guided range, my expectations for the semiconductor equipment market weren’t very bullish in the short term. In the end, lower Capex spending from the likes of TSMC and GlobalFoundries results in less demand for semiconductor equipment.

As a result, I was expecting quite a slowdown in this market, and this to impact Applied Materials in its fiscal third quarter and the second half of its fiscal year. However, as it reported its third-quarter results last week, the company illustrated its resilience as it blew past the expectations of Wall Street analysts and my own and reported a very resilient quarter.

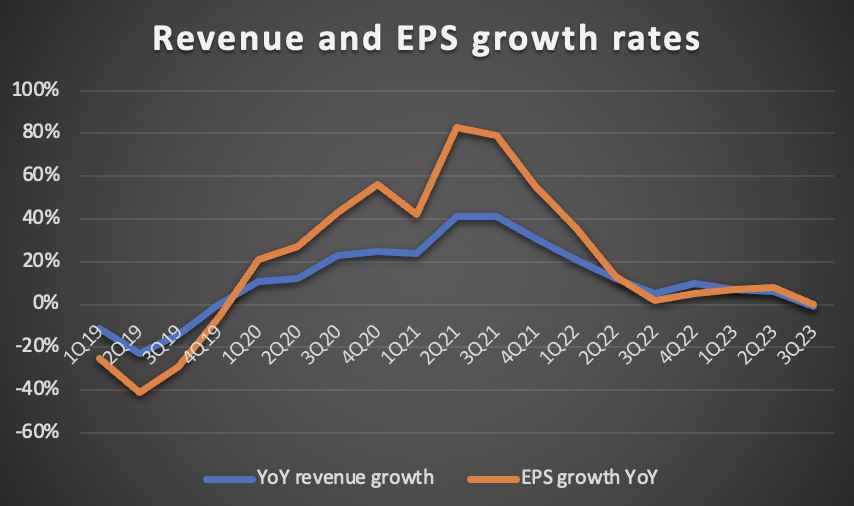

Yes, there was a continued slowdown from previous quarters visible in its YoY growth rates, as I expected, but these still came in far more resilient than I anticipated in my financial projections. The company is simply seeing more resilient demand for its semiconductor equipment products and margins are holding up much better as well.

The company reported earnings on August 17. AMAT reported revenue of $6.43 billion, beating the Wall Street consensus by $250 million and my own estimates by $280 million. Still, revenue was down 1.4% YoY.

Looking at the graph below, we can see that revenue continued to decelerate after a number of very impressive years. These lines will likely fall further over the next several quarters, likely at an accelerated pace. However, I do expect these rates to bottom in the first half of its fiscal 2024, starting a recovery going into H2 as Capex spending should start to accelerate again.

{kind=link}

Still, the current rates reported by AMAT and expected for the next several quarters reflect a clear outperformance versus its peers and the overall semiconductor industry. We should not forget that the semiconductor industry as a whole is expected to fall by double digits in 2023 to then recover in 2024 by mid to high single digits again, as discussed in my previous article.

For comparison, AMAT is now expected to report revenue growth of 2%, although also expected to report a decline in FY24.

The outperformance by AMAT last quarter was driven by its excellent and broad portfolio of differentiated products, balanced market exposure, efforts into high-growth areas, and growing services business, all of which create more stability and make the company less volatile and sensitive to the cyclical semiconductor industry. Also, in Q3, the company was able to lower its inventories.

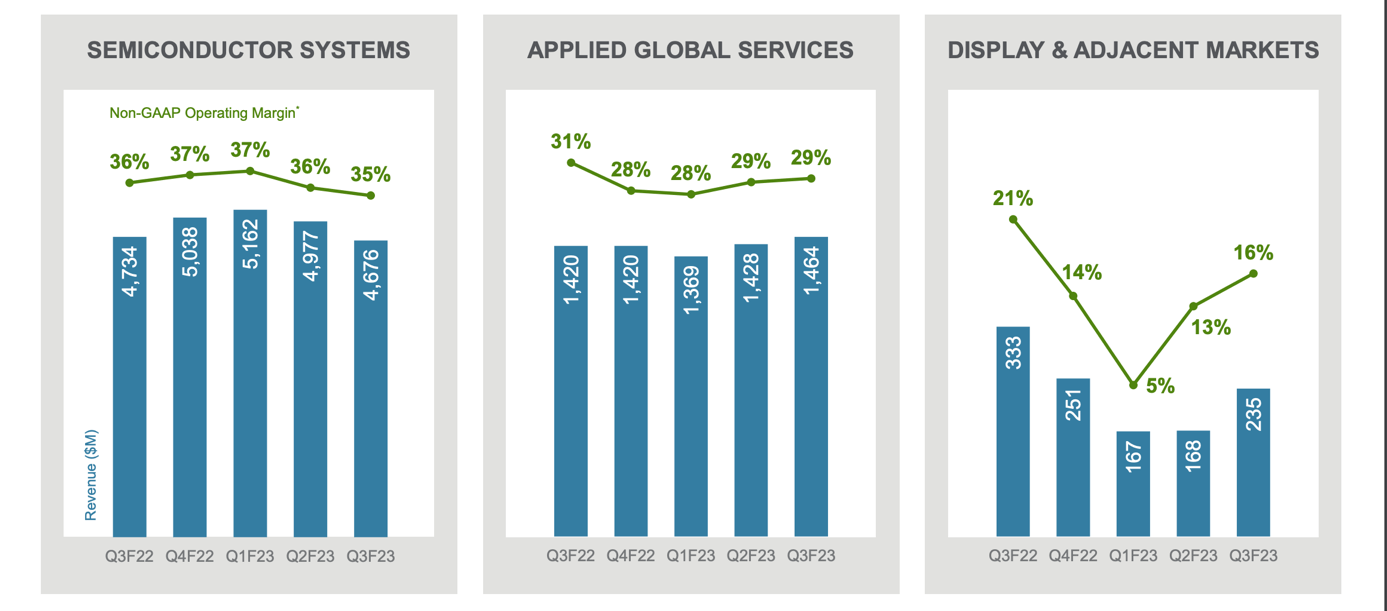

The performance in its semiconductor systems segment, in particular, was quite impressive despite a 1% YoY decline. I was expecting significantly more weakness in this segment. Yet, the real outperformer was the services segment as this one reported growth of 3%. More on this later.

Q3 financial data by segment (Applied Materials)

{kind=link}

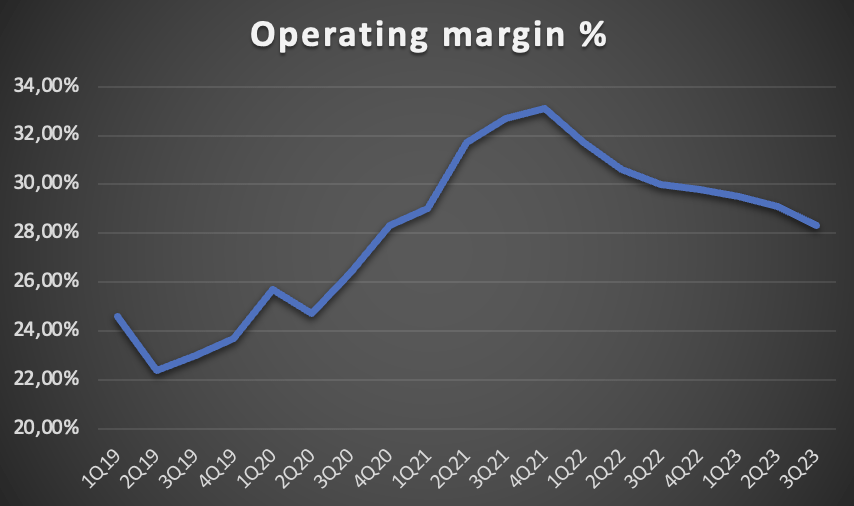

Moving to the bottom line, the company saw a very good performance in its gross margin as this was up 20 basis points YoY and came in at 46.4%.

However, the operating margin was down 170 basis points YoY and 80 basis points sequentially as it came in at 28.3%. This margin decline was as expected and in line with historical movements, although it came in stronger than I anticipated, largely due to a stronger-than-expected top-line performance.

{kind=link}

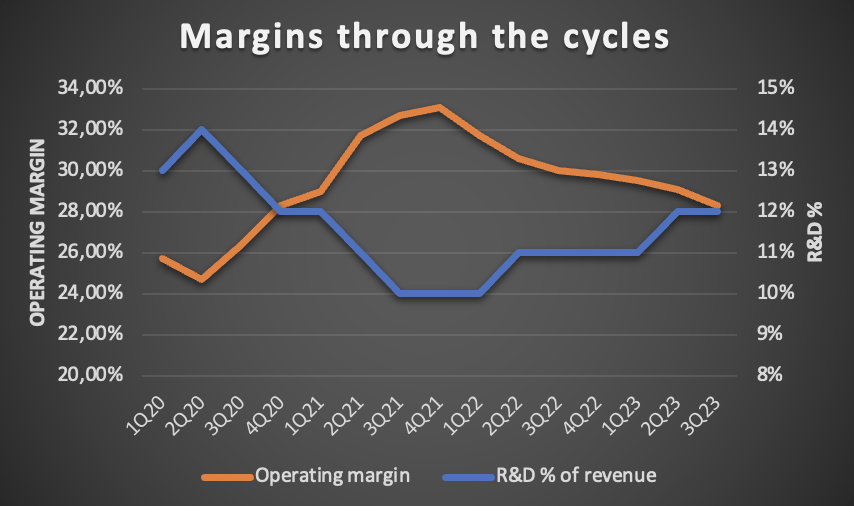

The reason for the lower margins both YoY and sequentially is the declining top-line performance and continued investments in R&D made by management. Crucially, while its sales growth may be slowing or even turning negative, the company remains committed to its R&D investments, which results in lower operating margins.

I expect the operating margin to drop further in the next couple of quarters but to remain stronger than in previous cycles, mainly due to its services revenues. I believe the company should be able to keep its operating margin above 25%.

It is the strong expected industry growth that drives management to keep heavily investing in R&D through the cycles, and last quarter was no different. R&D costs were up close to 9% YoY in Q3 and up 13% for the first nine months of its fiscal year. This shows that management remains committed to its capital investment in technological progress, allowing it to maintain a strong competitive position.

R&D as a percentage of revenue remained relatively stable from last quarter but was up 100 basis points YoY and up 200 basis points from 3Q21, again highlighting management’s commitment to these investments.

{kind=link}

Furthermore, I believe this percentage will increase further going into 2024, potentially reaching a 13%/14% level as I expect further weakness in product shipments and R&D investments to remain a focus point for the company.

However, I expect this growth to slow down in FY24 and drop to low single-digit growth. I also believe this should be of no worry to investors as this simply means the company and its management team remain committed to its future and remain confident in its growth potential.

Overall, I believe the margin profile delivered by the company in Q3 is everything investors could have wished for in the current operating environment. EPS in Q3 was $1.90, down 2% YoY but topping the consensus by $0.15. Also, despite the current downcycle, the company continues to report very strong cash flows. Free cash flow came in at $2.3 billion at an FCF margin of 36%.

These strong cash flows also allowed the company to return $707 million to shareholders through dividends and share repurchases. This number already reflects the 23% dividend hike announced by the company in March and means shares yield a respectable 0.9%.

Obviously, AMAT is not a company designed for dividend investors as it is still a growth-focused business. However, it is quite interesting for dividend growth investors. The company has, over recent years, shown that it is focused on delivering value to shareholders, highlighted by its 5-year average dividend growth rate of over 17% and its latest hike of 23%.

As the company is expected to deliver very strong growth over the remainder of the decade, while revenues are also expected to become more stable due to an increase in service revenues, I believe we should see the dividend continue to grow strongly. Also, the current dividend payout ratio of just 14.5% offers significant dividend safety and room for continued increases, even through the cycles.

AMAT exposure to ICAPS and other resilient categories drive a continued outperformance

In large part boosting the company's strong performance in Q3 was continued strength in ICAPS (IoT, communications, automotive, power, and sensors), which largely offset weakness in leading-edge foundry-logic and NAND.

{kind=link}

Without getting too much into the technicalities, AMAT management believes its early focus on ICAPS (driven by secular growth in these technologies) has positioned it favorably for continued outperformance. It has already released 20 products to leverage growth in ICAPS demand, which positions the company favorably to benefit from the growing demand for IoT and AI-driven technologies. This is what management said during the earnings call regarding these secular drivers:

Advanced chips are at the foundation of major global inflections and as the IoT-AI era takes shape, it is driving a new wave of growth and innovation for the semiconductor industry. At Applied, we have focused our strategy and investments to deliver high-value technologies that enable key IoT and AI-driven inflections.

Due to their rapid growth today, these technologies are seeing more resilient demand compared to more traditional technologies like PCs and smartphones, which positions AMAT favorably to outperform the overall semiconductor industry. AMAT believes this should also drive an outperformance into 2024.

Furthermore, in a time of very low investments by memory makers, AMAT continues to see high demand for ICAPS-enabling products from these customers. This is nicely highlighted by the fact that AMAT reported higher revenue in DRAM than its two closest process equipment peers combined. The company is the clear leader in equipment that enables these technologies. This strength in DRAM from AMAT is underpinned by several factors and for those interested in the technicalities anyway, this is what management stated concerning these factors:

We have gained a significant share in DRAM patterning, both for EUV-based and multi-patterning. We have developed unique, co-optimized hardmasked solutions, which are a key enabler for capacitor scaling. We have successfully ported key technologies developed for logic to DRAM, where they are used in the peripheral circuitry to significantly increase I/O speed. And, we are the largest supplier of advanced packaging solutions with leadership positions in micro-bump and through-silicon via that enable multiple generations of high-bandwidth memory.

AMAT is already delivering a strong (out)performance in DRAM today, which should mean that these customers should meaningfully boost growth for AMAT in future years once they start boosting spending again as the industry recovers. I expect to see the results of these increased investments reflected in AMAT’s revenues starting from its fiscal 2Q24.

The overall growth of the semiconductor industry, as explained in my previous article should further boost growth in demand for Applied Material’s products, potentially even driving it to outperform the semiconductor equipment outlook.

This is what I previously wrote regarding the industry outlook, and I believe not much has changed since, apart from AMAT showing the ability to perform better than expected. I recommend reading my previous article on the company for the full industry analysis and expectations.

These investments, among many others, should drive a 7.7% CAGR for the global semiconductor manufacturing equipment market through 2030, driven in part by a push for manufacturing capacity in the US and Europe and the increasing complexity of chip technology. The latter is especially important to AMAT as the increasing complexity causes an expanding available market for the company as equipment spending grows and more advanced equipment is needed. With AMAT holding a 19.8% market share in the global semiconductor manufacturing equipment market, it should be able to fully benefit from this expected growth

In the medium term, the gradual improvement in semiconductor demand should also result in stable capex as the likes of TSMC (TSM), Intel (INTC), and Samsung increase capacity, boosted by government incentives in Western regions. As a result, investment firm B. Riley recently stated that it expects solid capex growth in FY24 and FY25, boosting its outlook for Applied Materials.

Growing service revenues de-risk the company’s revenue stream

Also crucial to the AMAT investment thesis is the company’s services segment which is becoming increasingly important for AMAT’s overall performance. As of the latest quarter, the segment still accounted for just 23% of total reported revenue, but this has been growing quickly. The segment continues to report growth even with this year's low fab utilization rates and after absorbing the impact of new U.S. trade rules. The segment reached a record revenue level last quarter, growing 3% YoY.

Crucially, 60% of these service revenues come from long-term agreements, creating a high level of revenue stability and making the company quite a bit less cyclical than it used to be, especially as these contracts have a high renewal rate of over 90%. Moreover, the growth of these agreements outpaces growth in the installed base due to the increasing complexity and importance of these systems.

Driven by the strong outlook for semiconductor equipment and the factors discussed above, management believes it is on track to deliver double-digit growth in its services segment. As these service revenues will then start to account for a larger part of AMAT’s revenues, this should bode well for its financial position and consistency.

Updates outlook & AMAT stock valuation

For its fiscal Q4, AMAT is guiding for revenue of $6.51 billion, plus or minus $400 million. This reflects a 3.6% decline YoY, which is far from bad and far better than my $5.8 billion expectation. As a result of the resilient top line, the gross margin is expected to be around 47%, up from 46.4% last quarter. This should result in an EPS of $2.00.

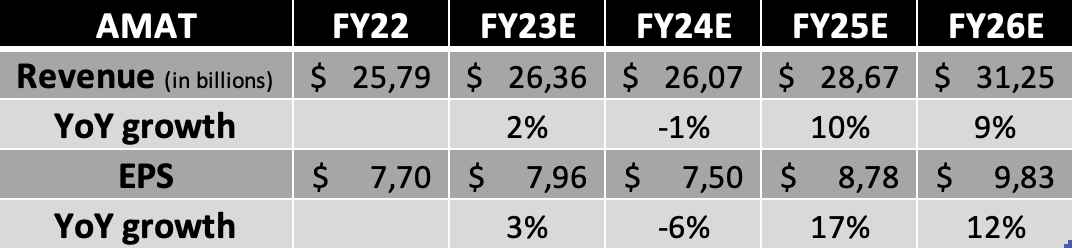

After already delivering Q3 results that easily beat my estimates, this Q4 guidance from management is also far above my expectations and requires a significant upgrade of my FY23 financial estimates. Following this guidance and the Q3 beat, I now expect the following financial results through 2026.

Financial projections (Author)

{kind=link}

(This includes Q4 revenue of $6.55 billion and EPS of $2.03)

Shortly explaining these estimates, I now expect AMAT to report revenue of $26.36 billion, which sits close to $1 billion above my previous estimate. The company has shown that it is able to report very resilient results, partly due to its exposure to fast-growing semiconductor verticals and a growing services segment. This should result in better-than-expected results across the board.

As a result of this and the expected gradual recovery in the semiconductor industry from the second half of the year onward, I expect AMAT’s FY24 to come in far better than analysts previously anticipated. However, while my estimates have massively improved for these two years, I still expect negative growth rates in FY24 with a bottom in Q2 of AMAT’s fiscal year. EPS will decline somewhat faster as I expect the operating margin to fall further over the next several quarters but to remain above 25%.

For the following years, my estimates have also increased somewhat, largely due to better-than-expected growth in the services segment and the company seeing strong demand for its semiconductor systems, driven by growth in the semiconductor industry. The early focus on ICAPS should continue to boost above-industry growth for AMAT.

As for the valuation, this is what I wrote recently:

Shares are currently valued at a forward P/E of 19x, which sits above its 5-year average of 15.6x and is in line with peers Lam Research ( LRCX ) and KLA Corporation (KLAC). Furthermore, on a P/E (FY3) basis, AMAT is clearly the cheapest among its peers.

Yet, I still believe that after a 43% share price increase YTD and considering its China/Asia exposure, shares are far from cheap. Of course, there are several positives to consider, like the company's shareholder-focused capital allocation strategy, impressive intellectual property, the exceptional growth outlook of the underlying industry, and its strong competitive position.

Considering all these aspects and my expectation of AMAT outperforming the industry and its peers, a forward P/E of 18x, which sits above its 5-year average, is fully justified.

Not much has changed since and the company today trades at a forward P/E of 18x as expectations have increased and the share price has remained relatively flat since. My beliefs remain the same, although I am slightly tweaking my fair value P/E as the company’s resilience lowers its risk profile, allowing for a higher multiple. Therefore, I now believe a 20x P/E multiple is justified.

Based on this and my FY25 EPS, I calculate an improved target price of $177, up from $152. (Please note, this target price is solely based on its forward P/E and is only for indicative purposes.). Going with a 10% annual return, I believe a fair share price currently sits at $142, resulting in a 1-year price target of $156, leaving an upside of 9.35%.

Conclusion

Applied Materials has demonstrated remarkable resilience in the face of a challenging semiconductor market. Despite a slowdown in the industry and lower Capex spending by major manufacturers, AMAT has surprised with a robust performance in its recent quarter.

While YoY growth rates have moderated, they remained stronger than anticipated, showcasing the company's ability to weather industry fluctuations. The services segment's growth, driven by long-term agreements, provides stability to AMAT's revenue stream, reducing its cyclicality and positioning it for future growth.

AMAT's commitment to R&D investments, even during downturns, underscores its strategic approach to long-term success. Additionally, its shareholder-friendly capital allocation strategy, dividend growth history, and leadership in advanced technologies make it an attractive proposition for investors seeking both growth and stability.

Following this outperformance and a very strong Q4 outlook, I have meaningfully upgraded my financial projections, resulting in a target price upgrade from $152 to $177. This results in a 1-year price target of $156, leaving an upside of 9.35%.

Therefore, I upgrade my rating on the company from hold to buy and believe a share price of around $142 offers a sufficient margin of safety and potential for solid long-term returns.

For further details see:

Applied Materials Q3 Earnings: ICAPS And Service Revenues Drive Surprising Resiliency