AMAT - Applied Materials: Still Firing On All Cylinders

2023-07-26 05:01:07 ET

Summary

- Applied Materials, a global leader in the development of semiconductor manufacturing equipment, is in a strong financial position, despite facing challenges from Chinese export restrictions and industry cyclicality.

- The company's commitment to research and development, along with its robust product portfolio, positions it well for future growth in the semiconductor industry.

- With the semiconductor industry expected to keep growing at a strong pace and poised to reach a market value of over $1 trillion, this should bode well for AMAT.

- While the near-term outlook may be challenging, patient long-term investors could find value in Applied Materials. While the current share price is too demanding for my taste, its growth prospects, especially beyond FY24, offer potential for solid returns.

Investment thesis

I initiate my coverage of Applied Materials, Inc. ( AMAT ) stock with a hold rating following my in-depth analysis of the company and the underlying industry. While the company might face several significant headwinds, it remains in an excellent financial position with a robust longer-term outlook.

Applied Materials is a global leader in semiconductor manufacturing equipment. With a strong market position and a comprehensive product portfolio, the company caters to the demand for faster and more efficient chips, supporting innovative technologies like AI, 5G, and autonomous vehicles. Its revenue is driven primarily by the semiconductor systems segment, supported by a growing services segment with recurring revenues from long-term agreements. Moreover, Applied Materials maintains a shareholder-friendly approach with consistent dividend hikes and share buybacks, backed by strong cash flow generation.

While facing challenges from Chinese export restrictions and industry cyclicality, Applied Materials shows resilience and long-term growth potential. The company's commitment to research and development positions it for future advancements and market dominance. The semiconductor industry is projected to grow significantly over the next decade, which should benefit Applied Materials through increased demand for semiconductor manufacturing equipment.

In this article, I will take you through the company fundamentals, latest developments and financial results, and underlying industry trends to end up with a revenue and EPS forecast through 2026 to determine whether this company is an attractive buy today.

AMAT is a shareholder-friendly semiconductor giant navigating an industry downturn

Applied Materials is a leading global company specializing in materials engineering solutions for the semiconductor industry and other advanced manufacturing sectors. Established in 1967 and headquartered in Santa Clara, California, Applied Materials has grown to become one of the world's largest suppliers of equipment, services, and software used in the fabrication of integrated circuits.

The company's cutting-edge technologies and products enable the production of faster, more efficient, and higher-performing chips that power the world's most innovative devices and technologies, including artificial intelligence, 5G, autonomous vehicles, advanced data centers, and more. Applied Materials' portfolio includes systems for chemical vapor deposition ((CVD)), physical vapor deposition ((PVD)), etching, ion implantation, and other critical processes involved in semiconductor manufacturing. This comprehensive product portfolio encompasses state-of-the-art equipment, materials, and software designed to optimize every stage of the semiconductor manufacturing process, from precision wafer fabrication to advanced packaging and assembly. That the company is very much focused on innovation is perfectly highlighted by its 17,300 patents.

Through this technological expertise, Applied Materials has risen to become one of the most influential and trusted names in the semiconductor manufacturing space. Its global presence extends worldwide, allowing it to serve customers in virtually every corner of the world.

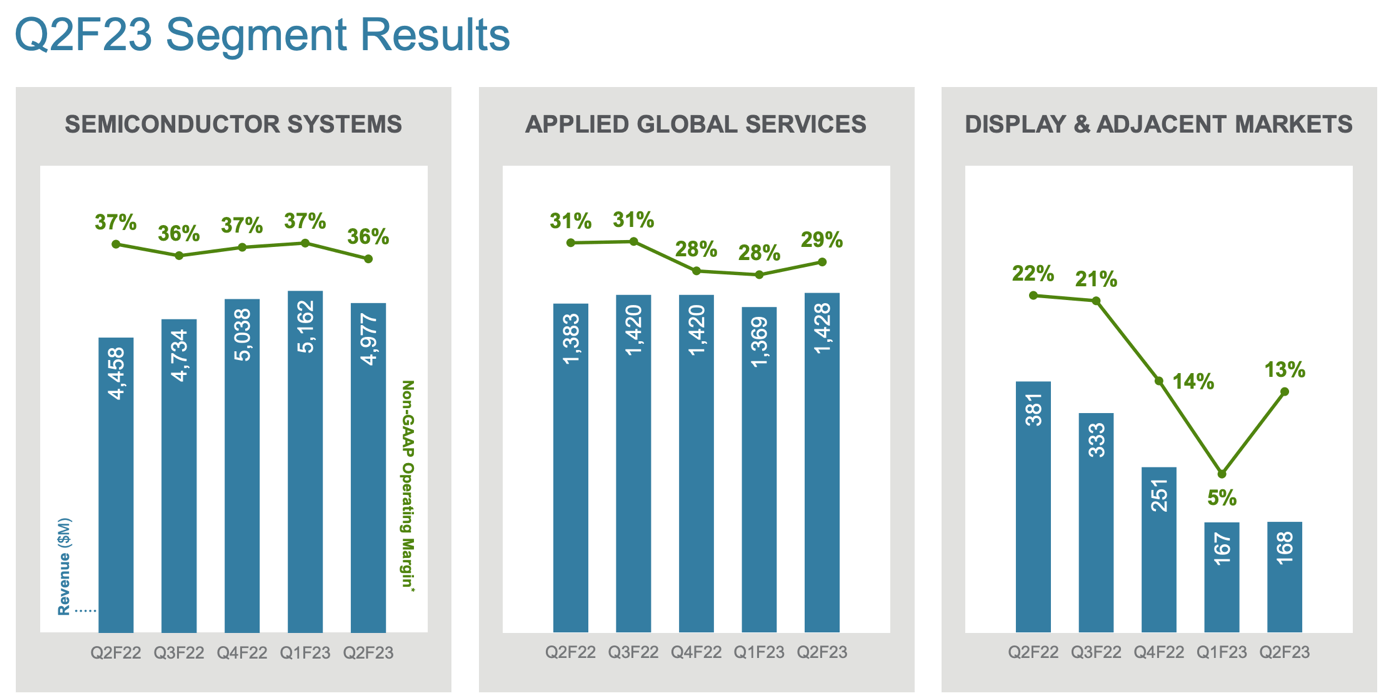

The company operates through three segments, which are semiconductor systems, applied global services, and display and adjacent markets. As of Q2, semiconductor systems accounted for the far majority of revenue with 75% while also reporting the best operating margin of 36%. This segment practically includes all of Applied Materials’ semiconductor hardware.

{kind=link}

AMAT

The applied global services segment came in second and accounted for 22% of revenue and reported an operating margin of 29%. This segment includes all the company’s services offered to clients, like spare parts, service contracts, installation services, updates, and software solutions. And while this only accounts for 22% of revenue, the segment is incredibly important as it derives 60% of these service revenues from subscriptions in the form of long-term agreements, making these recurring and much less sensitive to an economic slowdown, highlighted by a renewal rate of above 90%. These agreements are growing rapidly as customers are eager to service their equipment regularly to be able to use these for many years.

Finally, the display and adjacent markets segment is responsible for a very minimal 2.5% of Q2 revenue, down over 50% from last year. This also caused the operating margin to decline by nine percentage points to just 13%. With this segment accounting for a very minimal slice of total revenue, I recommend that investors focus on the previous two segments when checking out AMAT.

Getting somewhat deeper into its latest financial performance , AMAT reported Q2 revenue of $6.3 billion, which represented a 6% increase YoY and was on the upper end of the guidance range. AMAT is seeing its lead times and inventory levels come down as it has been able to catch up with the decreasing demand.

Driving last quarter’s growth was the semiconductor systems segment, which grew 12% YoY as demand remained resilient, in line with the resiliency seen in customer capex. Meanwhile, the services segment grew 3% YoY, which was the segment's 15 th consecutive quarter of YoY growth as the growing installed base of equipment allows service revenues to keep growing as well.

AMAT was able to maintain a flat gross margin sequentially at 46.8% as it was able to offset most headwinds like trade restrictions, inflation, and continued supply chain difficulties. This resulted in an operating margin of 29.1%, which has been trending down ever so slightly over recent quarters due to the impact of continued investments and slowing revenue growth. Overall, the company reported a net income of $1.69 billion, resulting in an EPS of $2, up 8%.

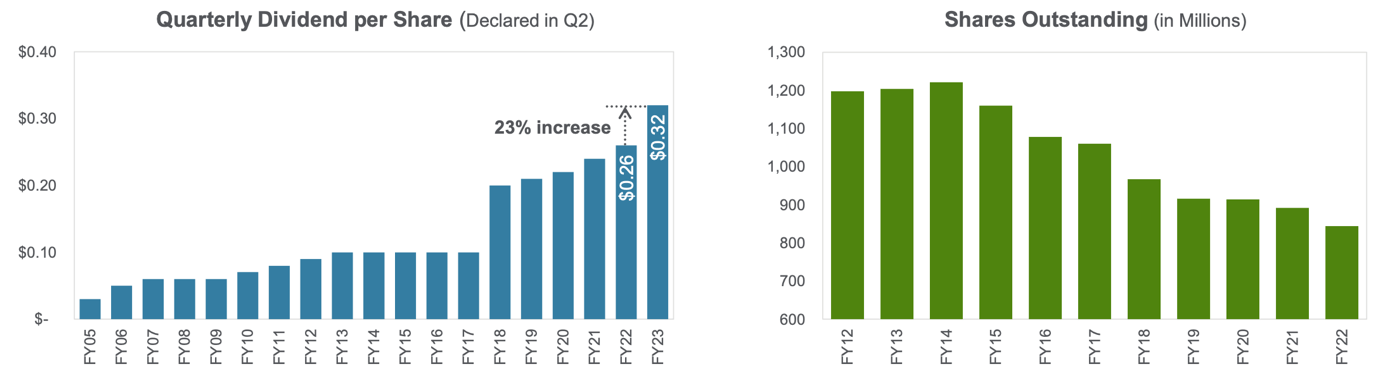

Free cash flow generation for AMAT was strong last quarter as it reported $2 billion in FCF, which equals an FCF margin of 31%. As a result of these excellent margins, FCF comfortably covered shareholder returns as the company returned $1 billion to shareholders through $219 million in dividends and $800 million in share buybacks

Shares currently yield just below 1% after a 23% dividend hike announced in Q1, which was the most significant increase in 5 years and brought the 5-year dividend growth CAGR to 17%. Meanwhile, the payout ratio remains at a very low 14%, leaving management with plenty of room to further grow the dividend at an accelerated pace while maintaining dividend safety. This is what management said regarding this during the last earnings call :

We believe our free cash flow can continue to grow and support increasing the dividend at an accelerated rate over the next several years, which would double our previous dividend per share. As our services business grows along with our installed base of equipment, it alone produces more than enough operating profit to pay the company's dividend.

This sounds promising and makes AMAT an exciting dividend growth opportunity despite its relatively low starting yield. Considering the expected growth in the semiconductor industry, AMAT’s leading market position, and the company’s excellent cash generation abilities, I believe it should be able to keep growing the dividend at an above 15% CAGR.

In addition to these excellent dividend payments, AMAT also continues to buy back its own shares at a rapid rate. In Q1, the company announced a new $10 billion repurchase authorization, which equals close to 9% of the current market cap, after lowering the outstanding share count by 30% over the last ten years already.

{kind=link}

AMAT's dividend and share repurchase history (AMAT)

Management is very shareholder-focused and plans to return significant amounts of cash to its shareholders over the next decade. And it definitely has the financial abilities to do so. The company currently holds a total cash and investments position of $7.1 billion on the balance sheet, up over $1 billion from a year ago, which is a testimony to the company’s cash generation abilities, even as the operating environment turns slightly negative. Meanwhile, long-term debt stands at $5.5 billion and is very manageable with $4.05 billion due before 2030. This should be easily covered by the company’s free cash flow.

Chinese export restrictions, the CHIPS Act, and management’s commitment to R&D

When considering an investment in Applied Materials, I believe there are three important recent developments and fundamental strategic decisions to consider.

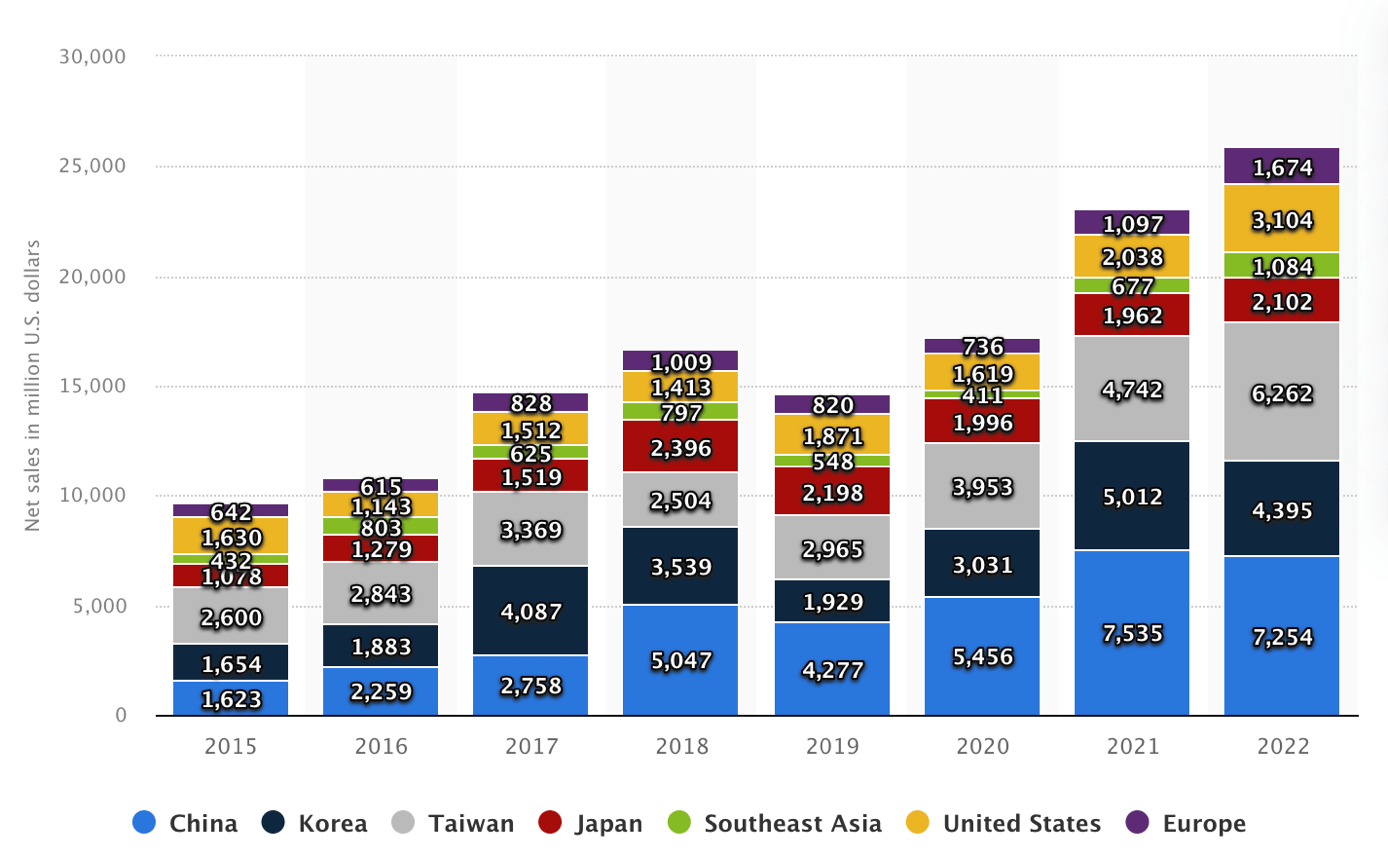

The first one is the impact of the imposed Chinese export restrictions in relation to certain advanced semiconductor equipment and chips. As of FY22, AMAT derived 28% of its revenues from China, making it the largest region by revenue for the company. Taiwan came in second with 24% of revenue and the Western alliance of Japan, Europe, and the US together only accounted for 26% of FY22 revenue. Moreover, AMAT has a total Asia exposure (excluding Japan) of 73.6%, making it quite sensitive to geopolitical situations in this area. Of course, this exposure should not come as a surprise as 70% of semiconductors are manufactured in the Asia Pacific region.

{kind=link}

AMAT revenue by region (Statista)

Still, this exposure to Asia and, specifically, China does worry me as it makes the company incredibly sensitive to the Chinese export restrictions, the threat of a Taiwan invasion, and unpredictable governments in the region. The Chinese export restrictions imposed by the US government last year are predicted to have a $2.5 billion negative impact on AMAT’s FY23 results as the company cannot ship its most advanced equipment to Chinese customers, decreasing the revenue derived from the region. And highlighted the unpredictability of some of these governments, just over a month ago the Chinese government blacklisted US memory maker Micron ( MU ) due to a so-called security risk, in response to the US restrictions with regard to AI. Altogether, I do view this exposure as a significant negative to a potential AMAT investment.

Still, on a more positive note, we should see AMAT’s revenue from Western regions grow over the next several years as semiconductor manufacturing in these regions gets boosted by government incentives. This should also result in AMAT shipping more of its equipment to these regions. Also, AMAT can still ship most of its semiconductor manufacturing equipment to Chinese customers, making the impact rather minimal on a full-year basis. Of course, the threat of further restrictions remains an overhang on the stock, in my view, requiring a somewhat higher discount to fair value. Further restrictions could have a meaningful impact on growth for AMAT.

A more positive development for AMAT is the introduction of the US Chips Act. Recent changes to the regulation also allow semiconductor equipment manufacturers to benefit and receive funds for local investments. Following the introduction of the Chips Act, Applied Materials has already announced that it plans to build a new $4 billion R&D facility in the heart of Silicon Valley. The massive R&D center should become operational in 2026 and will be the world’s largest and most advanced facility for collaborative semiconductor process technology and manufacturing equipment R&D. And it will be the center of a further $25 billion in R&D investments in the following ten years, again supported by funding from the Chips Act.

I believe the act will benefit AMAT over the next several years to partially offset high capex levels for increased manufacturing capacity like the new research center. Also, this will allow AMAT to speed up investments in the US and to solidify its competitive position by increasing its R&D capabilities.

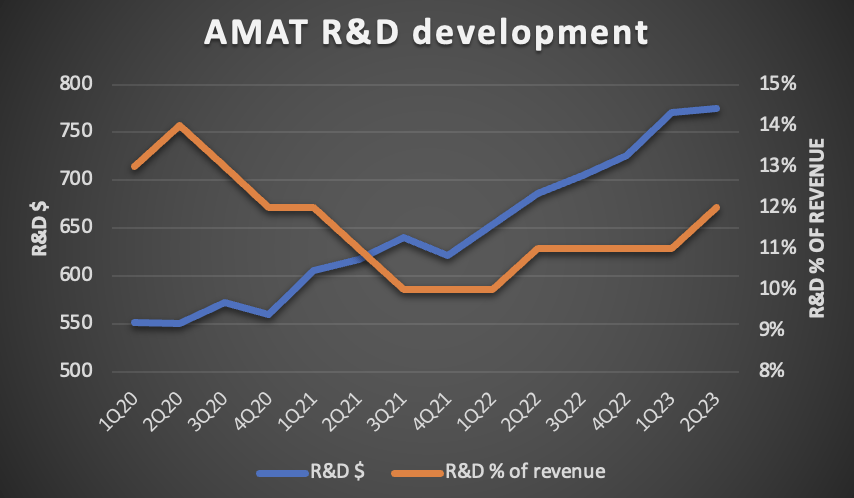

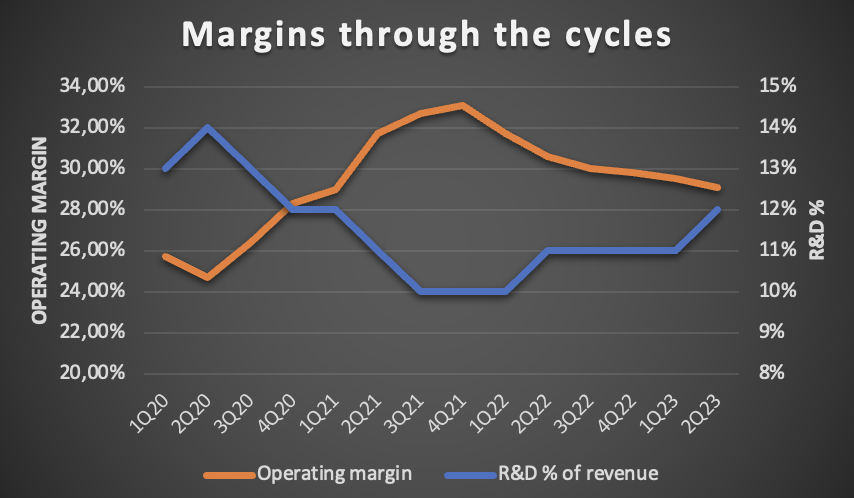

In the semiconductor industry, the company with the most advanced technology will end on top, which is why consistently growing the R&D budget is what allows Applied Materials to stay on top of its game and deliver the most advanced machines to customers to boost semiconductor manufacturing in ways like higher production, improved energy efficiency, and of course smaller wafers. In 2022, R&D amounted to $2.8 billion after showing consistent growth, as highlighted in the graph below. To keep its technological advantage and market share, AMAT has grown its R&D investments by nearly 50% over the last three years. If AMAT can keep delivering these advancements, it assures itself to remain the leader in its industry and the #1 choice among customers, allowing it to fully benefit from the expected industry growth. This is why R&D is crucial to monitor here and why management will keep growing its R&D investments even as the industry is experiencing a cyclical downturn. During the latest earnings call, management commented on the following regarding its approach toward continued investments despite an industry-wide slowdown:

We are planning to make a multibillion-dollar investment in new infrastructure over the next several years to significantly expand our capacity to collaborate more closely and productively with our customers as we develop next-generation materials, process technologies and equipment.

While we expect our capital expenditures to be higher over the next several years, there is no change to our longer-term financial model and our strong commitment to shareholder returns.

{kind=link}

By Author

The graph above shows a very steadily growing R&D budget for AMAT as management wants to grow this through the cycles, even as the industry is experiencing a downturn over recent quarters. Something that should be viewed as a very positive strategic priority by management. Yet, this does impact the company’s margins as the operating margin tends to drop to the mid-twenties from around 30% during times of slow or negative top-line growth (as witnessed in 2019/20 and today), also negatively impacting earnings. I believe this is not something to worry about. It is crucial that investors look through the cycles and cheer on AMAT’s consistent focus on investing in technological developments to drive long-term growth. This is what management stated during the earnings call:

Given our confidence in the trajectory of the industry and Applied Materials, we are taking actions and making associated investments to support our growth, accelerate our customers roadmaps and drive productivity and efficiency as the industry scales.

{kind=link}

By Author

That AMAT is indeed entirely focused on continuously improving its offering can be seen in its latest product release. Earlier this month, the company introduced a new wafer manufacturing platform called Vistara , which is designed to provide chipmakers with the flexibility, intelligence, and sustainability required to tackle growing chipmaking challenges. It is the company's most significant wafer manufacturing platform release in over a decade and demand for the product should be solid as it is especially useful in the ramp-up to smaller nodes and high-volume manufacturing.

Another noticeable recent product release was the Centura Sculpta, which is a cost-effective alternative to EUV double patterning. In short, it should be able to lower the manufacturer's capital cost by $250 million for each layer of adoption per 100,000 wafer starts, driven by its simpler and faster design. The company is already shipping this new product and expects it to bring in multiple hundreds of millions annually, eventually growing out to become a $1 billion product annually. The machine is a strong contribution to AMAT's already superior product portfolio.

Overall, I believe AMAT’s financial size advantage, significant intellectual property, and strong capital allocation strategy discussed above should allow it to maintain its technological advantage and superior product offering as seen today, driving above-industry growth through the cycles. Management shares this opinion as highlighted during the most recent earnings call:

Applied's broad and differentiated portfolio, market diversity and growing services business make us more resilient today than in the past and set us up to outperform our markets.

On that note, let’s take a look at the outlook for the semiconductor industry, a very important proxy for AMAT’s financial performance.

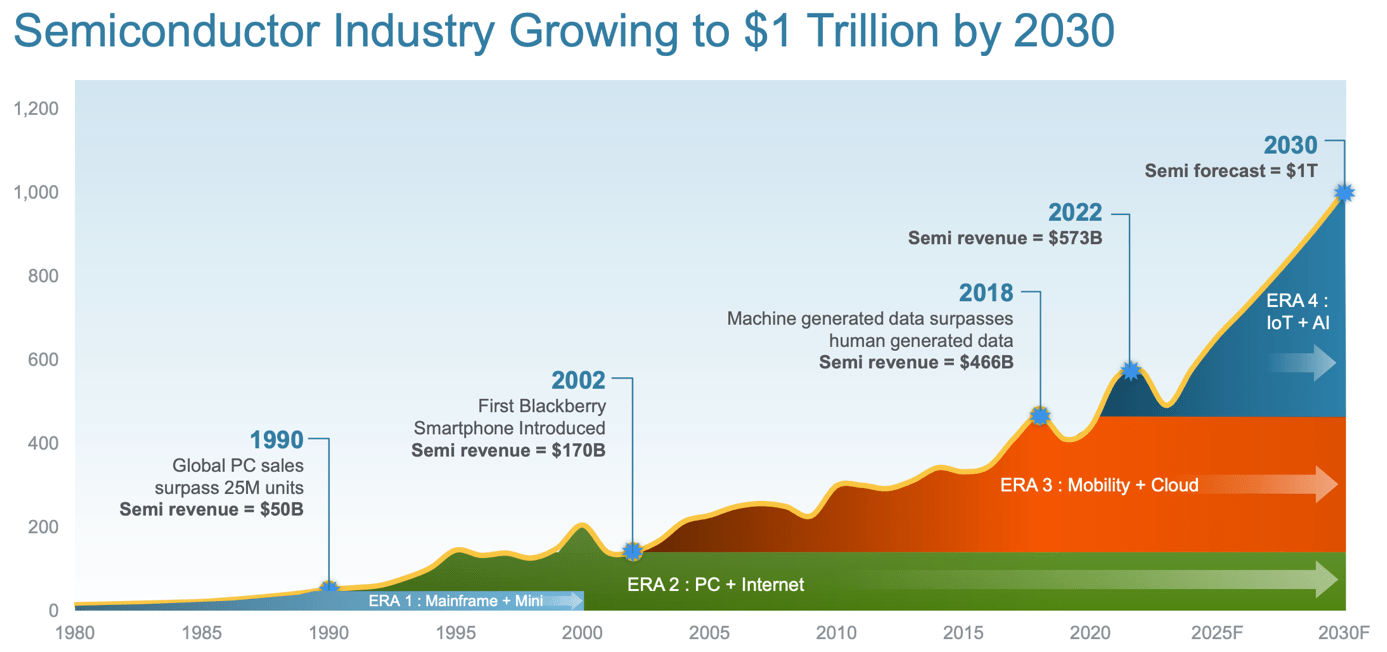

The semiconductor industry is poised to cross the $1 trillion mark by 2030

Crucial to the performance of AMAT is the health of the semiconductor industry, which is why I will discuss this one somewhat more extensively in this article. The performance of AMAT is heavily correlated with industry health as the company is dependent on capex spending by semiconductor manufacturers. As these companies increase their investments in capacity growth to satisfy the growing demand for semiconductors, demand for AMAT’s products also increases to fill up these newly built fabs. Yet, as companies slow down their investments due to falling demand like we are witnessing today, demand for AMAT’s products also falls.

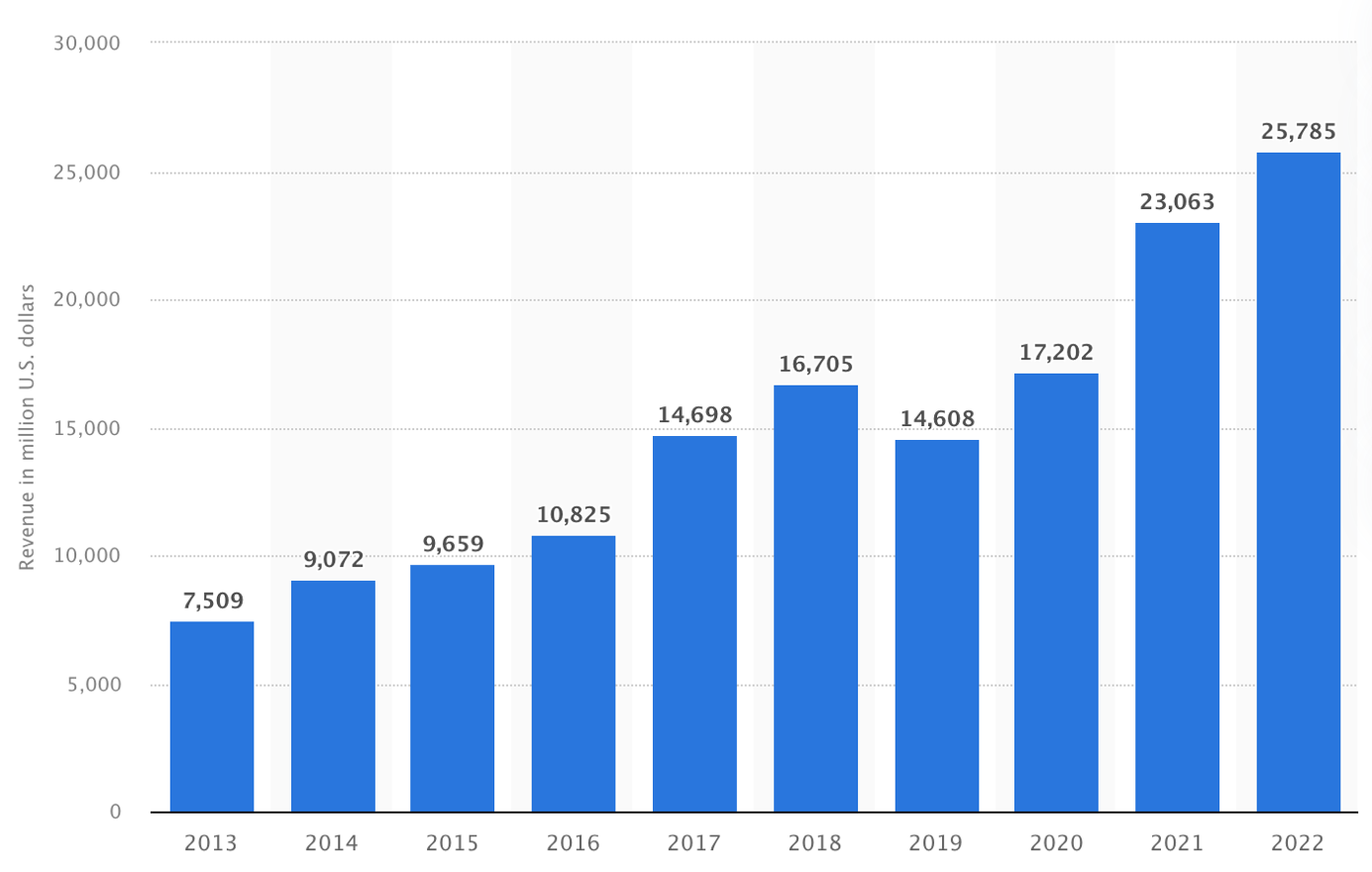

The incredible health of the industry is what helped the company massively grow revenues over the last 10 years as shown in the graph below.

{kind=link}

AMAT revenue (Statista)

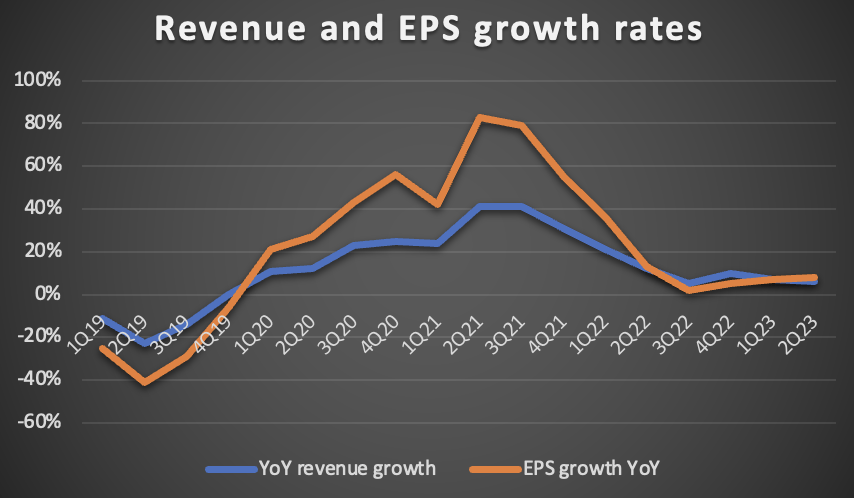

At the same time, the downturn in the industry over the last year is what caused the slowdown in growth reported by AMAT. The graph below highlights this as we can see a clear revenue and EPS growth slowdown from the peak levels in 2021 and flattening out over the last several quarters as capex from AMAT customers has remained stable. Furthermore, the industry downturn should continue to impact the company in the near term as the industry continues to see decreased demand, highlighted by monthly data. Semiconductor sales in May fell by 21.1% as demand weakness continues. Yet, there was a positive in the monthly data as a 1% sequential increase was recorded, the third consecutive sequential increase, possibly indicating a bottom in the cycle.

{kind=link}

By Author

The most recent TSMC ( TSM ) quarterly report and earnings call also provided several interesting and crucial insights for the whole semiconductor sector, including Applied Materials. For one, the company, a global benchmark for semiconductor demand, lowered its full-year outlook as it now expects to report a 10% decline in revenue due to lower demand. The company continues to see a challenging operating environment as customer inventories remain relatively high and decreased consumer spending is a drag on demand for electronics. Management explained during the earnings call that while it is seeing growing demand for AI-specialized chips, this tailwind cannot offset the multitude of headwinds, slightly lowering the expectations of an AI impact on the industry in the near term.

At the same time, the company is guiding for sequential growth in the third quarter, which could indicate a slight improvement in demand and the start of an expected gradual improvement in the second half of the year and into FY24. According to World Semiconductor Trade Statistics , the industry should grow by around 12% in 2024 as it gradually recovers.

Meanwhile, the overall outlook for semiconductor manufacturing equipment remains quite resilient despite a meaningful drop in semiconductor demand over the last years, as reflected in the TSMC quarterly results and AMAT’s reported growth rates visualized above. Also visible in TSMC’s latest quarterly report and management commentary is that capex used for capacity expansion remains high overall, obviously supporting demand for AMAT’s products, driven by the continued drive for western capacity expansion and resilient growth in demand for AI and automotive applications, which can offset some of the weakness across smartphone and PC, for example.

Still, the weakness in consumer electronics has caused a significant decrease in investments in 2023 for memory customers of AMAT. Management even points to investments in memory sitting at the lowest level in over a decade. Meanwhile, reports show that fab construction remains high, with about 80 fabs coming online in 2024-2027. This, in part, is why AMAT remains able to report growth despite an industry-wide slowdown – semiconductor manufacturers remain committed to their capacity investments.

Yet, despite several positive drivers, I expect capex growth to slow down over the next several years as overall demand will need to catch up first to allow for further investments and the current capex level is already relatively high following a boom during the COVID-19 pandemic. A gradual recovery of the semiconductor industry as predicted by TSMC and the already high capex levels witnessed across the industry could result in much slower or even negative capex growth among semiconductor manufacturers as their capacity should not outgrow semiconductor demand and a lower demand environment does not allow for increased investments, negatively impacting the outlook for AMAT. The outlook sure is not looking too rosy in the near term.

Meanwhile, the long-term outlook should be solid as growth in demand for semiconductors is expected to grow significantly with the semiconductor industry reaching a value of close to $1.4 trillion by 2029 , according to Fortune Business Insights. This reflects an expected CAGR of 12%, driven by the increasing number of consumer electronic devices, a boost in industrial digitalization, the emergence of advanced technologies like AI and IoT, and the growth in cloud computing, among many others. Overall, demand for semiconductors across most industries is expected to grow significantly.

{kind=link}

AMAT

This, in turn, results in semiconductor manufacturers having to spend significant amounts of capex on capacity expansion to satisfy demand, increasing demand for semiconductor manufacturing equipment produced by the likes of ASML and AMAT. Samsung ( OTCPK:SSNLF ), for example, recently announced its plans to invest $228 billion in an advanced facility in South Korea and TSMC is planning on investing over $40 billion in a new facility in Arizona, which should come online in 2025.

These investments, among many others, should drive a 7.7% CAGR for the global semiconductor manufacturing equipment market through 2030, driven in part by a push for manufacturing capacity in the US and Europe and the increasing complexity of chip technology. The latter is especially important to AMAT as the increasing complexity causes an expanding available market for the company as equipment spending grows and more advanced equipment is needed. With AMAT holding a 19.8% market share in the global semiconductor manufacturing equipment market, it should be able to fully benefit from this expected growth

In the medium term, the gradual improvement in semiconductor demand should also result in stable capex as the likes of TSMC, Intel ( INTC ), and Samsung increase capacity, boosted by government incentives in Western regions. As a result, investment firm B. Riley recently stated that it expects solid capex growth in FY24 and FY25, boosting its outlook for Applied Materials.

Outlook & AMAT stock valuation

For Q3, AMAT expects to report revenue in the range of $5.75 billion and $6.55 billion, which indicates a YoY revenue decline of 5.6% at the midpoint of $6.15 billion. This shows that AMAT is increasingly seeing a drop in demand for its products in response to semiconductor manufacturers' lower or stagnant capex levels. This revenue decrease is expected to be primarily driven by a significant decline in the semiconductor systems segment, which is projected to report revenue of around $4.5 billion, down 5%. Meanwhile, growth in the more resilient services segment is expected to remain positive, with a revenue projection of $1.43 billion, up 1% YoY.

As a result of this lower revenue base and a continued focus on investments, the gross margin is expected to decrease from 46.8% last quarter to 46.3% in Q3. This should result in EPS in the range of $1.56 to $1.92, down 10% at the midpoint of $1.74.

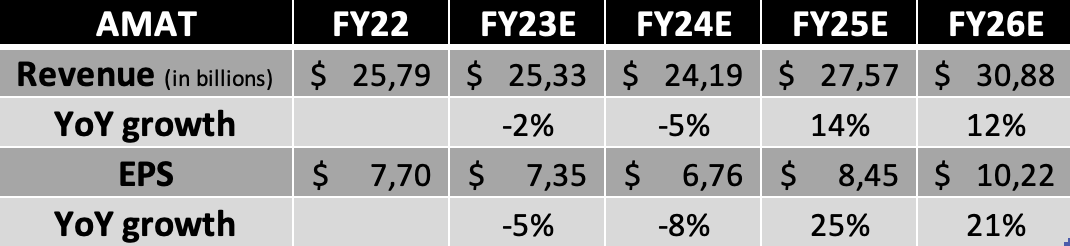

Following this guidance from AMAT, the company’s recent financial performance, its competitive position, and the underlying industry growth expectation, I now expect the following financial performance until FY26.

{kind=link}

Financial estimates (Author)

(I expect Q3 revenue of $6.15 billion and EPS of $1.74)

Shortly explaining these estimates, I expect AMAT to report revenue of $25.33 billion for the full year as I project a further growth deceleration in the second half of the year and into FY24. As this lower revenue base will impact margins, EPS will decline at a faster rate. I expect the same circumstances also to impact FY24. While the semiconductor industry will gradually see improved demand, I expect capex levels to remain stagnant and AMAT customers to postpone equipment purchases. This should result in lower demand for AMAT products, which is why I expect a negative growth rate for the following years with a recovery from FY25 onward as manufacturing capex increases to fulfill the demand for semiconductors.

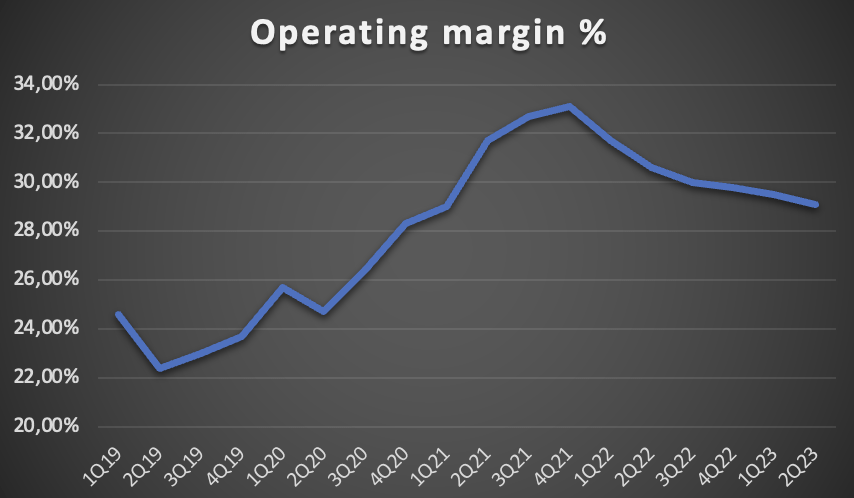

Meanwhile, while capex slows down at semiconductor manufacturers, AMAT must continue its investment rate to keep up with the latest innovations. This is why I expect margins to fall over the next 1.5 years for AMAT as investment growth will be greater than its sales growth. Operating margins will likely fall back to the mid-twenties percentages as we saw in 2019/2020. As a result, I also expect a more pronounced drop in EPS.

{kind=link}

Operating Margin development (By Author)

From FY25 onward, my outlook for AMAT is largely tied to the earlier-discussed outlook for the semiconductor industry, which is a really positive one with stellar growth expected over the remainder of the decade. This is why AMAT will return to reporting solid growth from FY25 onwards, starting with a recovery in FY25 and FY26 as investments across the semiconductor industry accelerate to satisfy the growing demand.

So, while the near-term outlook is challenging, long-term investors could benefit from discounted valuations by looking through the cycles and benefitting from share price weakness. Yet, is now the time to use this strategy with AMAT shares, or is the current share price unfavorable, even for long-term investors?

Shares are currently valued at a forward P/E of 19x, which sits above its 5-year average of 15.6x and is in line with peers Lam Research ( LRCX ) and KLA Corporation ( KLAC ). Furthermore, on a P/E (FY3) basis, AMAT is clearly the cheapest among its peers.

{kind=link}

Valuation peer comparison (Seeking Alpha)

Yet, I still believe that after a 43% share price increase YTD and considering its China/Asia exposure, shares are far from cheap. Of course, there are several positives to consider, like the company's shareholder-focused capital allocation strategy, impressive intellectual property, the exceptional growth outlook of the underlying industry, and its strong competitive position.

Considering all these aspects and my expectation of AMAT to outperform the industry and its peers, a forward P/E of 18x, which sits above its 5-year average, is fully justified. Based on this belief and my FY25 EPS estimate, I calculate a target price of $152, leaving an upside of 9%. (Please note, this target price is solely based on its forward P/E and is only for indicative purposes.)

Taking an annual return of 10%, a fair per-share price sits around $120. Therefore, I believe shares are a buy below $120 per share as this should allow for solid long-term returns and a sufficient margin of safety.

Conclusion

Despite facing challenges from Chinese export restrictions and a temporary downturn in the semiconductor industry, the company remains resilient and focused on long-term growth.

Applied Materials' strong financial position, significant intellectual property, and commitment to R&D make it well-positioned to benefit from the expected growth in the semiconductor industry. Additionally, the company's shareholder-friendly capital allocation strategy, including dividend growth and share buybacks, adds to its appeal for investors.

While the near-term outlook may be challenging, patient long-term investors could find value in Applied Materials. While the current share price is too demanding for my taste, its growth prospects, especially beyond FY24, offer potential for solid returns. An ideal buying opportunity could be below $120 per share, providing a sufficient margin of safety and potential for long-term gains.

Yet, with a current share price of close to $140, I rate shares a hold and recommend waiting for a better entry point. For investors currently holding the shares, I see absolutely no reason to sell. AMAT clearly has a very promising long-term outlook.

For further details see:

Applied Materials: Still Firing On All Cylinders