APLT - Applied Therapeutics: Buy For Upcoming Pre-NDA Meeting (I Expect A Positive Outcome)

2023-08-17 04:28:21 ET

Summary

- Applied Therapeutics is a micro-cap with low cash balance, but has major upcoming catalysts (pre-NDA meeting for galactosemia and phase 3 results in diabetic cardiomyopathy) and a huge upside potential.

- Despite missing the primary endpoint in galactosemia ph3 trial, APLT still plans for NDA submission. The pre-NDA meeting with the FDA this summer will be a big catalyst if positive.

- I expect a positive outcome from the meeting considering consistent and meaningful clinical benefit in multiple endpoints, orphan and fast-track designation, no alternative treatments, and the significant burden for affected patients.

- I rate APLT stock as a speculative "Buy" considering the asymmetric risk-reward but bet only what you can afford to lose.

Overview of the thesis

Applied Therapeutics ( APLT ) is a micro-cap biotech stock with a low cash balance and will soon need to raise cash. However, with cash enough for upcoming major catalysts and considering huge upside potential it represents a speculative investment with an asymmetric risk/reward.

APLT has recently completed a phase 3 trial for classic galactosemia and, despite missing the primary endpoint, is pursuing NDA submission based on clinically meaningful efficacy in pre-specified endpoints, supporting biomarker data, fast track designation and absence of other pharmaceutical treatment options for this rare disease. Therefore, the first major catalyst will be the outcome of the pre-NDA meeting with FDA (this summer), during which FDA will decide whether to allow NDA submission based on available data. In this article I will focus on the galactosemia indication, and why I believe the outcome of the pre-NDA meeting will be positive.

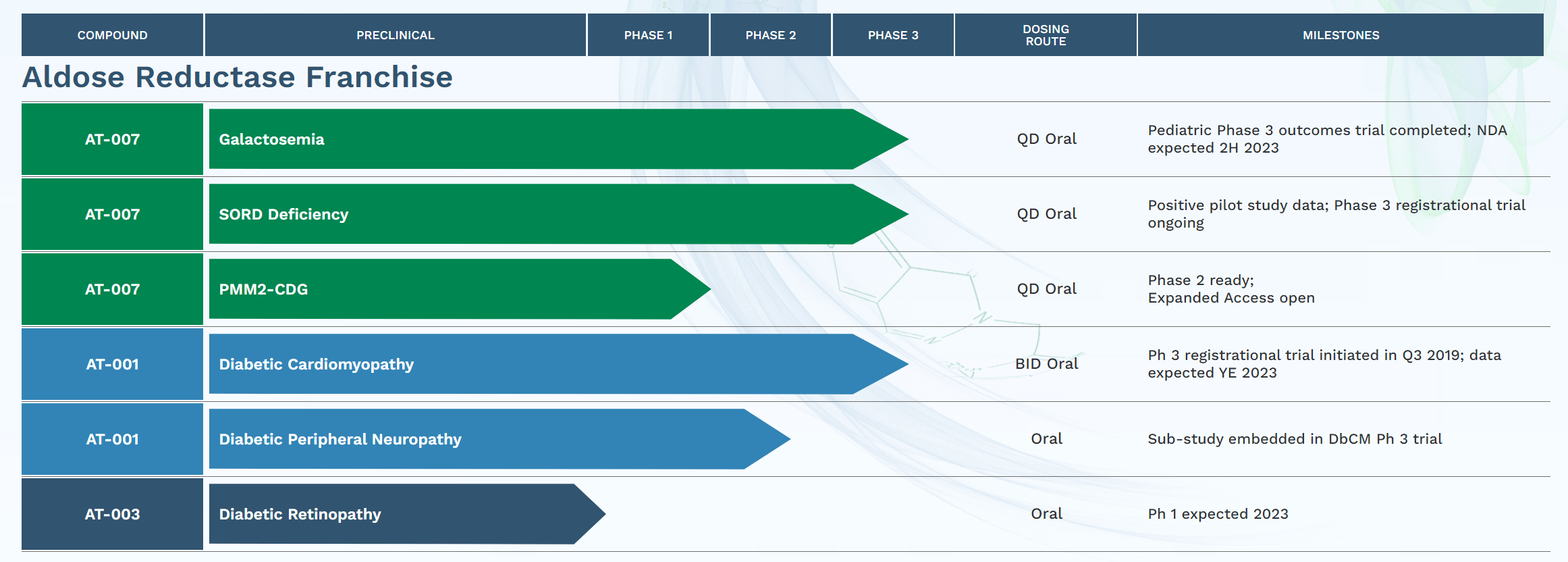

Brief overview of APLT's pipeline

APLT is developing aldose reductase inhibitors with much improved affinity, specificity and safety compared to prior efforts by other biotechs. Specifically, APLT is developing govorestat (AT-007) (for classic galactosemia, Sorbitol Dehydrogenase Deficiency (“SORD”) deficiency and PMM2-CDG), AT-001 (for DbCM and diabetic peripheral neuropathy) and AT-003 (for diabetic retinopathy). Notably, APLT has completed a phase 3 trial for galactosemia (which I will discussed below) and has two ongoing registrational phase 3 trials, one for DbCM and one for SORD deficiency with very promising earlier phase data.

Furthermore, govorestat has received

- From EMA (Europe), Orphan Medicinal Product Designation for both Galactosemia and SORD Deficiency,

- From FDA (US), Orphan Drug Designation for Galactosemia, PMM2-CDG, and SORD Deficiency; Pediatric Rare Disease designation for Galactosemia and PMM2-CDG; and Fast Track designation for Galactosemia.

{kind=link}

APLT's website

Brief overview of potential from SORD and DbCM indications

The purpose of this article is to discuss the galactosemia indication and chances of approval based on available phase 3 data. Nevertheless, it is worth briefly discussing here the potential of the 2 other late stage indications, i.e. SORD and DbCM, as these could serve as important back-up catalysts in case of setbacks with govorestat regulatory pathway for galactosemia.

SORD, like galactosemia, is a rare inherited disorder with no approved treatments, significant burden for affected patients and a target market of about 3300 patients in US and 3700 patients in Europe. Considering orphan designation, pricing can be >$100K per patient per year, corresponding to market potential of $370 million in Europe (of which APLT is entitled 20% royalties ), i.e. $66 million) and $330 million in the US. Considering no alternative treatment option and concentration of affected patients in few expert centers it shouldn't be hard for APLT to capture a significant share. Assuming just 50% capture would correspond to peak revenue potential of about $400 million per year. AT-007 has demonstrated 52% reduction in sorbitol from baseline (p<0.001) vs. placebo in the 3-month interim analysis of ongoing phase 3 trial, which is expected to translate in clinical benefit. Interim assessment of clinical outcomes is planned at 12 months (H2 2023). If the primary clinical outcome measure reaches statistical significance at 12 months, the study will be completed and unblinded. If not, the study will continue in blinded format to 24 months (results are expected in H2 2024).

In contrast to galactosemia and SORD, DbCM has a much larger target population of about 6 million in the US and 5 million in EU5 countries. Current treatment options for DbCM are similar for other causes of heart failure, including SGLT2 inhibitors (average annual price $4506 ) and sacubitril-valsartan (annual price about $6500 ). However, existing therapies do not target the specific pathophysiological mechanisms implicated in DbCM. Therefore, AT-001 could be used as add-on to existing therapies rather than complete with them. Assuming similar pricing (about $5000/patient/year) to SGLT2 and Entresto the total market potential is $30 billion. Even just 10% penetration would mean peak revenue of $3 billion.

It is also worth noting that de-risking for AT-001 comes from prior efforts (including by Pfizer (PFE)) to target DbCM and diabetic neuropathy with earlier generation aldose reductase inhibitors. These efforts have demonstrated promising efficacy but were limited by low binding affinity (= lower efficacy) and low specificity (=off-target effects, resulting in toxicity). Therefore, prior efforts have failed either due to a lack of efficacy or adverse effects. APLT reasonably expects (and I agree) that AT-001 will be successful considering much higher binding affinity and no off-target binding . Promising in-vitro data (much higher affinity with no off-target effect), efficacy in animal models, supportive biomarker data, significant reduction of NT-proBNP levels over 28 days in phase 2 trial, and efficacy signals by prior candidates increase the probability of success for AT-001 in DbCM indication. Topline results from the ongoing registrational phase 3 trial are expected by the end of 2023.

With regards to diabetic peripheral neuropathy (DPN), there are currently no approved disease-modifying treatments in Europe and US. Epalrestat (currently the only commercially available aldose reductase inhibitor) is approved in some countries (Japan, India and China) for DPN, but is limited by 3- to 5- times daily dosing (vs once daily for AT-001). Target market is 23 million patients in the US and 29 million patients in Europe. Since many DbCM patients often also suffer from DPN, DPN endpoints have been incorporated as a sub-study into the DbCM phase 3 trial. APLT plans to seek a strategic partnership to further develop AT-001 for treatment of DPN.

About galactosemia

Galactosemia is a rare inherited disease resulting in impaired ability to metabolize galactose. The most common form is "classic galactosemia". The reported incidence of galactosemia varies geographically; the estimated incidence is 1 in 30,000 to 40,000 births in Europe and 1 in 53,000 births in the United States. Considering 3.9 million live births per year in Europe and 3.6 million live births per year in the US this corresponds to 97-130 and 68 new cases per year, respectively (i.e., 160-200 new cases per year in US and Europe). Symptoms become apparent during the first days of life. Fortunately, galactosemia can be diagnosed early with newborn screening which is routine practice in US as well as several countries in Europe . Currently there are no treatments for galactosemia and patients are managed with nutritional therapy (to minimize dietary galactose). Prompt nutritional therapy results in resolution of early clinical features, but does not prevent various long-term complications (including various neurodevelopmental issues and primary ovarian failure in females).

In-depth interviews of affected adult patients and their caregivers, participating in the ACTION-Galactosemia trial, highlight the significant disease burden and challenges with daily living: "Most adults were not able to live independently, and all required support with day-to-day activities. Short- and long-term memory difficulties and tremors were identified as the most frequently experienced and challenging symptoms. Other difficulties such as fine motor skills and slow/slurred speech contribute to the significant impact on daily activities, affecting ability to communicate and interact with others. Symptoms were first noticed in early childhood and worsened with age. Classic Galactosemia impacted all areas of daily functioning and quality of life, leading to social isolation, anxiety, anger/frustration and depression." Therefore, AT-007 fills a significant unmet need. Keep the above in mind when assessing results of the phase 3 trial below.

The phase 3 study in galactosemia

The phase 3 study was a double-blind, placebo controlled study in pediatric patients (ages 2-17 years-old) diagnosed with classic galactosemia. Final assessment of patients was at 18 months of treatment and after that the trial is continuing as an open-label extension study. The study enrolled 47 patients (n=16 placebo, n=31 AT-007).

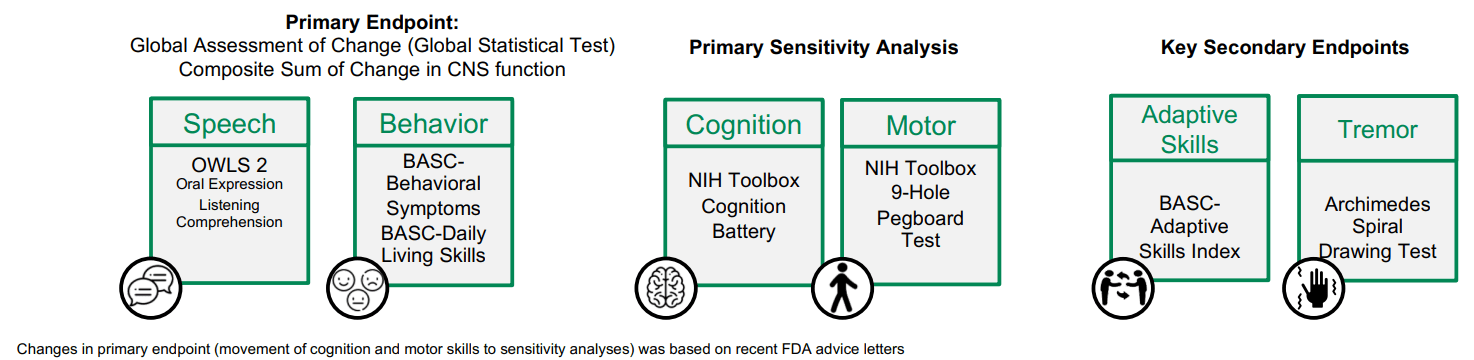

Pre-specified clinical endpoints can be seen in the figure below. The reason I want to emphasize this is because it is very important to differentiate pre-specified outcomes from post-hoc analysis. The latter cannot establish effectiveness for FDA approval. Notably, below endpoints are somewhat different from primary endpoints according to clinicaltrials.gov . As clarified by APLT: "Changes in primary endpoint (movement of cognition and motor skills to sensitivity analyses) was based on recent FDA advice letters". I like the transparency here.

{kind=link}

Pre-specified endpoints in galactosemia phase 3 trial (APLT presentation)

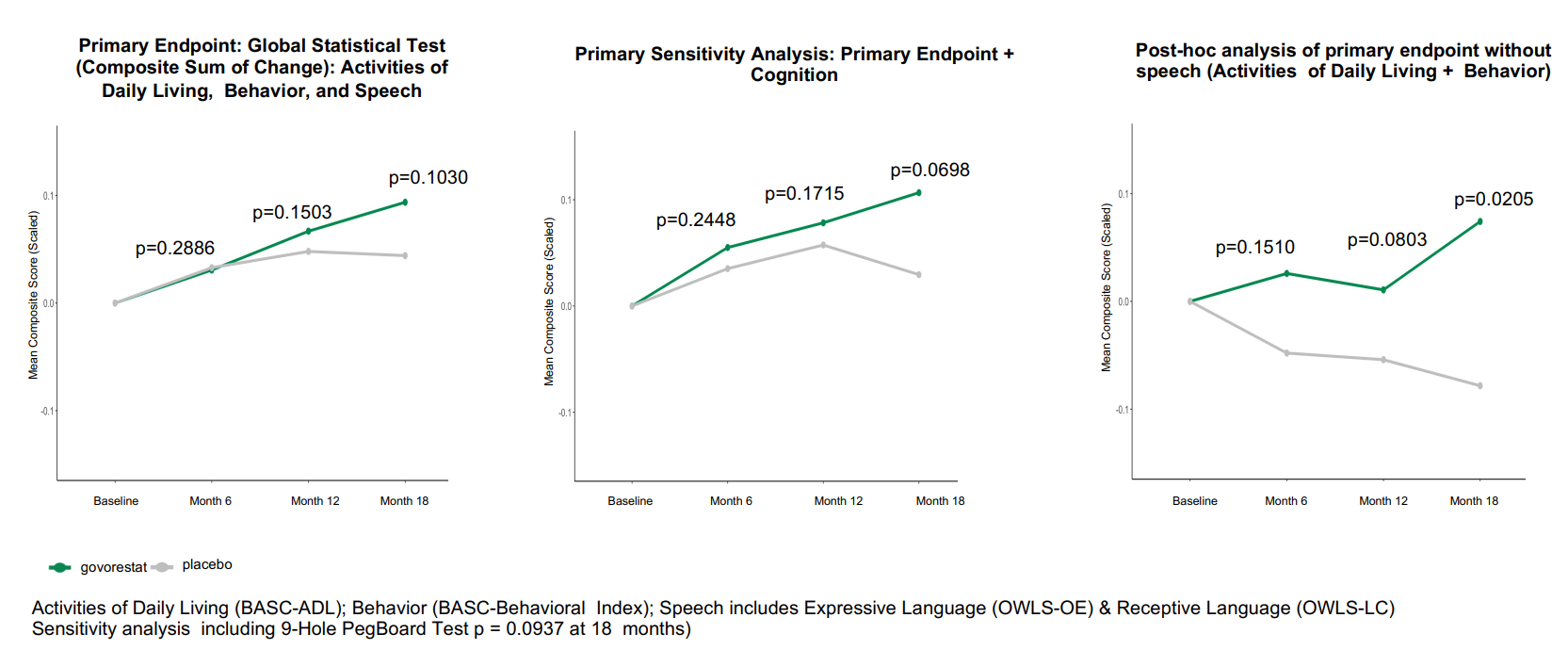

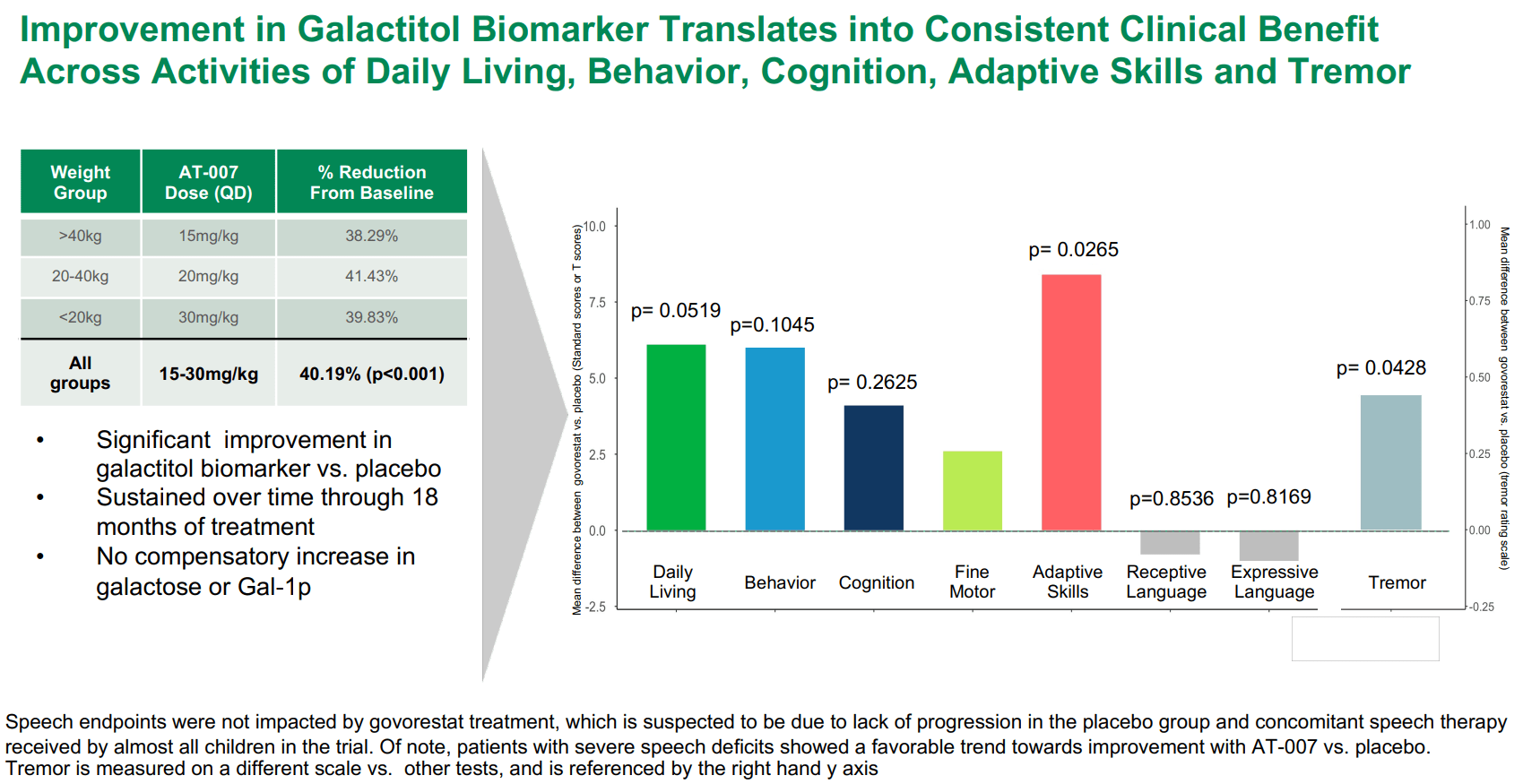

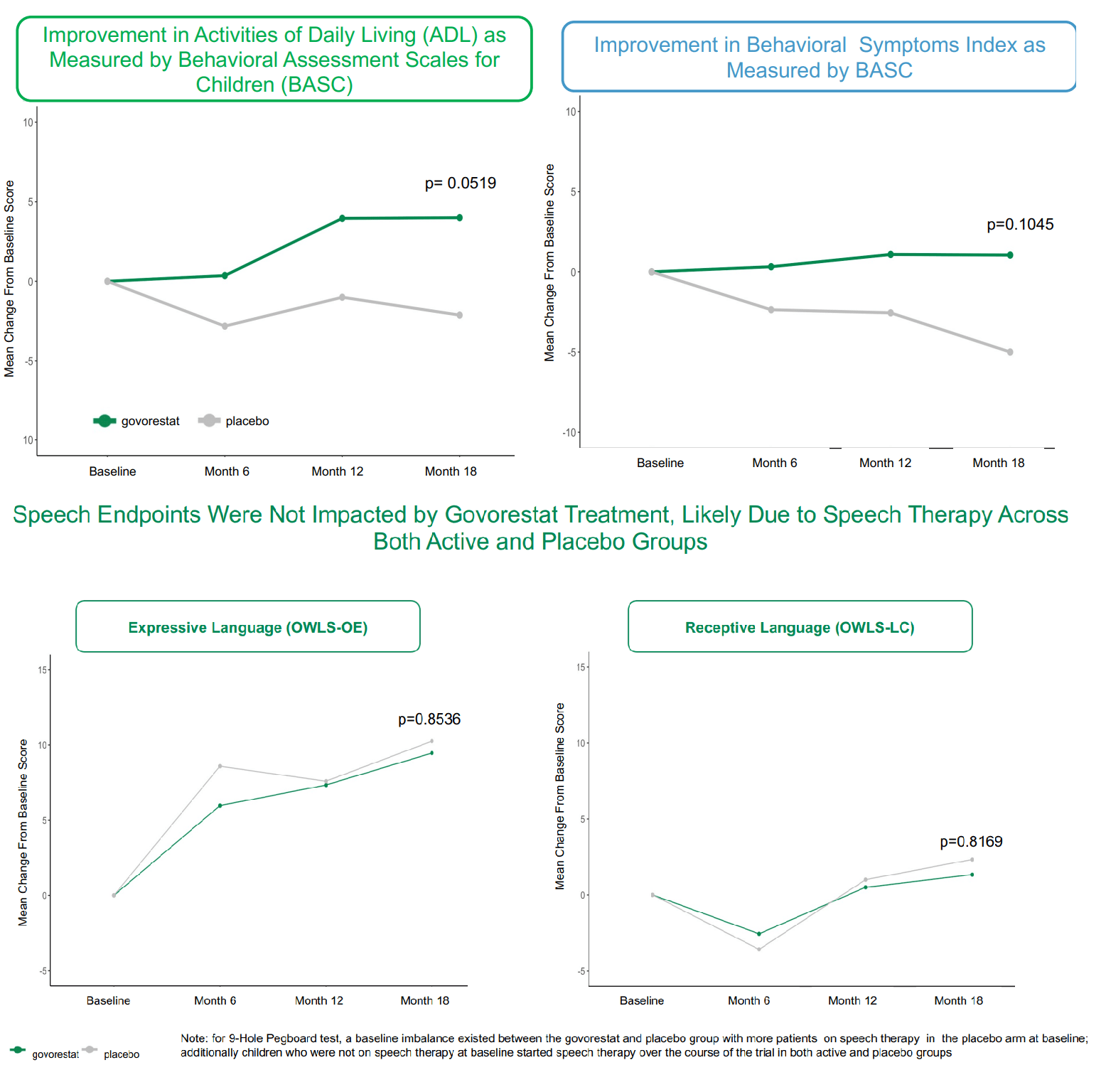

Results of the phase 3 trial can be summed-up by the two images below. Briefly, govorestat demonstrated consistent long-term clinical outcomes benefit across a range of functional measures, confirming prior biomarker data. Specifically, treatment improved activities of daily living, behavior, cognition, fine motor skills, adaptive skills and tremor vs. placebo. However, the study failed (barely) to reach statistical significance in the primary endpoint and primary sensitivity analysis. Nevertheless, as seen in first image below, systematic improvement over time was demonstrated for the overall primary endpoint (p=0.1030) and for a pre-specified sensitivity analysis including cognition (p=0.0698). Consistent benefit was seen in all secondary endpoints (except language). Notably, key secondary endpoints of adaptive behavior skills and tremor (which leads to "extensive burden on patients’ day-to-day lives") achieved robust and clinically meaningful improvement with p-values of 0.0265 and 0.0428, respectively.

{kind=link}

Summary of primary endpoint and primary sensitivity analysis (APLT presentation)

{kind=link}

Summary of pre-specified secondary endpoints (APLT presentation)

Based on the above, the consistent clinical benefit by AT-007 is evident. So why did the study fail to meet the primary endpoint? The primary endpoint is a composite sum of scales that assess speech (OWLS 2) and behavior (BASC-Behavioral symptoms and BASC-Daily Living skills). Despite consistent benefit in behavioral symptoms and daily living skills, there was no difference between AT-007 and placebo in speech assessments (see image below). This was most likely attributable to effective speech therapy in the placebo group. Post-hoc analysis of the primary endpoint without speech showed statistical significance (first image above). Furthermore, patients with severe speech deficits showed a favorable trend towards improvement with govorestat vs. placebo.

{kind=link}

Breakdown of the primary endpoint (APLT presentation)

Finally, it is important to note that galactosemia is a slowly progressive disease. Outcomes in the phase 3 trials were assessed at just 18 months, suggesting the potential for much larger benefit with long-term use. I wish APLT had continued the study for another 6 month (by which time point evidence of benefit should be much clearer, thus avoiding regulatory hurdles).

With regards to safety, AT-007 was well-tolerated with no serious adverse events.

What are the chances of approval after missing the primary endpoint?

Missing the primary endpoint in a pivotal trial typically means no NDA and no approval. However, this is not always the case! Below are some useful statistics from a recent study that reviewed 210 FDA drug approvals between 2018 and 2021;

- 21 drugs (10%) were approved despite null findings for one or more primary efficacy endpoints in pivotal studies!

- 10 of these 21 drugs (47.6%) were designed as orphan drugs (a reminder here that AT-007 has orphan designation for galactosemia).

- 13 of these 21 drugs (61.9%) were granted expedited review (a reminded here that AT-007 has been granted Fast track, which means eligibility for accelerated approval and priority review).

- Four drugs received FDA approval despite null findings in primary endpoints in a single pivotal study.

- Among cited reasons for approval by FDA; secondary or exploratory endpoint positive outcomes in 10 approvals (47.6%) and “favorable post hoc analysis” in 7 approvals (33.3%). As discussed above, AT-007 showed consistent and clinically meaningful improvements in various pre-specified secondary outcomes and a post-hoc analysis excluding language.

- In 7 drug approvals, the agency “required or requested post-marketing studies”

Based on the above stats, AT-007 fulfills several variables that improve chances of approval; orphan designation, Fast track designation, consistent and clinically meaningful improvements in many outcomes which were pre-specified, absence of alternative treatment options for galactosemia patients, and significant burden for patients and caregivers with current standard of care.

Furthermore, considering Fast track designation, AT-007 is eligible for accelerated approval based on surrogate endpoints and in fact APLT was expecting accelerated approval before the completion of the phase 3 trial, until FDA changed course and requested clinical outcome data. In the case of AT-007 there is strong supportive biomarker data (40.19% improvement in galactitol biomarker vs placebo, p<0.001) in addition to the above-described clinical efficacy data.

Finally, on the European front, "Applied Therapeutics and its European commercial partner, Advanz Pharma, met with the European Medicines Agency ((EMA)) rapporteurs earlier this summer, and plan to proceed with an EMA Marketing Authorization Application ((MAA)) submission as expeditiously as possible. The EMA submission is anticipated in the fall in order to provide sufficient time for approval of the Pediatric Investigational Plan ((PIP)), as well as incorporation of rapporteur comments and suggestions from the meeting."

Prediction of outcome of FDA meeting

Based on the above I believe the following are possible outcomes of the meeting with the FDA (starting from the most probable to the least probable);

- FDA will allow application for accelerated approval based on a combination of biomarker data and positive clinical data (+- ADCOM)

- FDA will allow application for full approval (+- ADCOM)

- FDA will decline NDA application and will ask for a new confirmatory trial.

I believe the first two scenarios are the most likely and would be very positive for APLT despite financial hurdles. The third scenario (much less likely in my opinion) would be detrimental to the stock price and APLT would have to raise cash from a dismal financial position. APLT could in theory object to the decision but this would take time. Also positive results from DbCM phase 3 trial could be a very useful back-up.

Financials

According to the Q2 quarterly report APLT's cash and cash equivalents totaled $35.6 million as of June 30, 2023. Total operating expenses were $17 million (R&D $12 million and G&A $5 million). At this burn rate APLT's cash should be barely enough for another 2 quarters (Q3-Q4 2023), which nevertheless means that APLT has sufficient cash for upcoming catalysts (pre-NDA meeting, potential NDA submission in the fall, potential MAA submission in the fall, results from ongoing DbCM phase 3 trial by the end of 2023).

This runaway does not account for potential milestone payments by European partner. APLT has granted Advanz Pharma the exclusive right and license to commercialize AT-007 for use in treatment of SORD and Galactosemia in the European Economic Area, Switzerland and the United Kingdom. APLT is entitled development milestone payments upon clinical trial completions and receipt of marketing authorization in the territory, as well as certain commercial milestone payments, totaling $142.2 million, plus royalties of 20% of net sales. According to APLT , "If actualization of these milestones aligns with the projected timelines, and product approvals are received in the timeframes expected, this source of capital may be sufficient to cover operating expenses through expected product approvals and potential revenues".

It is important to note here the multiple Orphan designations that govorestat has received from both FDA and EMA. Average annual cost of orphan drugs is >$100K per patient . Galactosemia affects approximately 3,000 patients in the US and 4,000 in Europe, with a growth year over year of approximately 200 patients (due to new births). This means a target market of >$700 million; $400 million from Europe (of which APLT is entitled to $80 million based on 20% royalties) and $300 million in the US. Assuming 80% of patients will receive the treatment (considering lack of other options) this means a peak income potential for APLT of >$380 million/year. Considering an EV/revenue multiple of 7.1 (typical for biotech stocks), this means that just the galactosemia indication is worth $2.7 billion of enterprise value (vs a current EV of just $56 million). Therefore, it is likely that following positive outcome of pre-NDA meeting with the FDA, APLT will be able to raise much needed cash in much better terms.

Risks to the thesis

As described above, the pivotal trial missed the primary endpoint and despite several factors collectively pointing to the potential of an NDA submission based on available data this may not be the case. This could be detrimental for APLT and current shareholders, especially in the absence of good news by DbCM phase 3 results.

Either of ongoing Phase 3 trials (for diabetic cardiomyopathy and SORD) may not meet the primary endpoints. This would have very serious implications for APLT following a negative outcome from the FDA meeting.

Even with a positive outcome from the FDA meeting, APLT would still need to raise cash. Furthermore, delays in the regulatory process are possible. Nevertheless, APLT would be in a much better position to do so following a positive meeting.

Recommendation

I recommend APLT as a speculative "Buy" based on an asymmetric risk-reward and based on the expectation of the FDA allowing NDA application for galactosemia despite missing the primary endpoint in the pivotal trial. As long as you understand the risks and invest what you can afford to lose, APLT looks like a promising (but risky) investment.

For further details see:

Applied Therapeutics: Buy For Upcoming Pre-NDA Meeting (I Expect A Positive Outcome)