BILL - AppLovin: This Plunge In Price Presents A Great Opportunity (Rating Upgrade)

Summary

- The past year has been incredibly painful for shareholders of AppLovin Corporation, as shares of the business plunged in response to a weakening in some parts of the firm.

- Other aspects of the AppLovin Corporation business, however, remain strong and growing, and investors should look there for opportunity.

- Add on top of this how cheap AppLovin Corporation shares are now, and it represents a really attractive opportunity.

When it comes to investing, it's important to note that nobody has a perfect win rate. At least in the short term, and even sometimes in the long term, investments that one once thought would be attractive could turn out to be duds or worse. One company that has proven to be a real pain so far for me is AppLovin Corporation ( APP ), an enterprise that provides services for the mobile app space and that also produces and monetizes its own portfolio of apps centered around mobile gaming. For most of 2022, AppLovin Corporation was demonstrating continued revenue growth. Cash flows were also rising nicely. But in the latest quarter, the company experienced something of a downturn from a revenue perspective, with weakness in a couple of areas significantly impairing operations. The end result has been a sizable decline in the company's share price. But even with its fundamental condition weakening, the firm now does seem to offer investors attractive upside moving forward.

A tough time

For countless years now, the app space has been viewed as an area of perpetual growth for investors to enjoy. But this year has been evidence that this is not necessarily the case - at least not in the short term. You see, when I last wrote an article about AppLovin Corporation back in May of this year, I felt optimistic because of the company's continued rapid growth. Even though financial performance leading up to that point had been somewhat mixed, the overall trajectory of the company was positive, and the guidance management provided made the company look like a true GARP play that might be worth a bit of a premium compared to what most value investors would be willing to pay. Fast forward to today, and shares of the company are down 73.7%. That compares to the 3.7% decline experienced by the S&P 500 over the same window of time. Considering that I had previously rated the company a "buy," that's quite a letdown.

At the time that I wrote my bullish thesis on AppLovin Corporation, the company was already experiencing a steady and severe share price decline. From its 52-week high point, for instance, shares are down a whopping 89.4%. Even though the company was forecasting robust financial results for the 2022 fiscal year, concerns over some portions of the enterprise that have historically been rather significant to the business were instrumental in pushing the stock lower. But before we get to that, we should touch on the broader financial performance of the company.

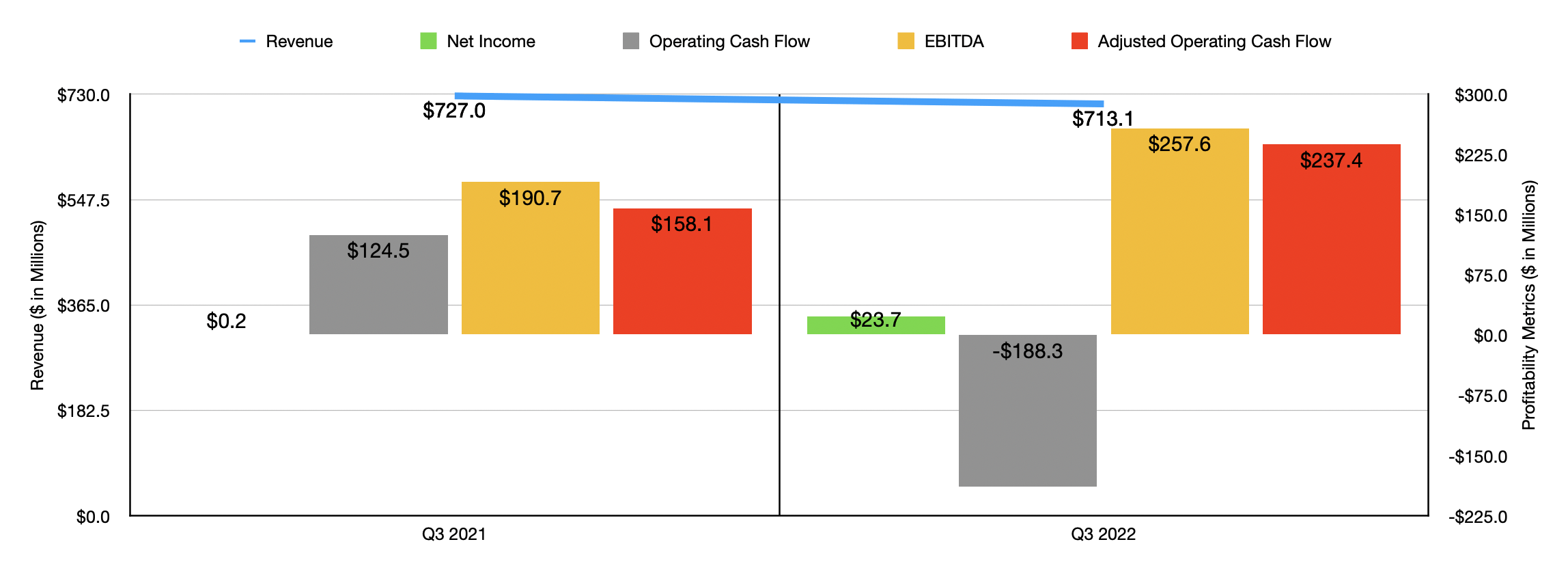

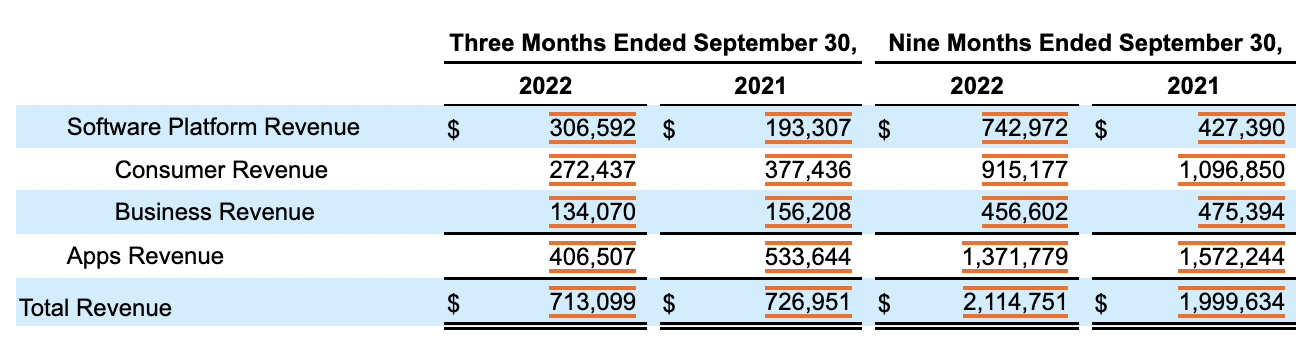

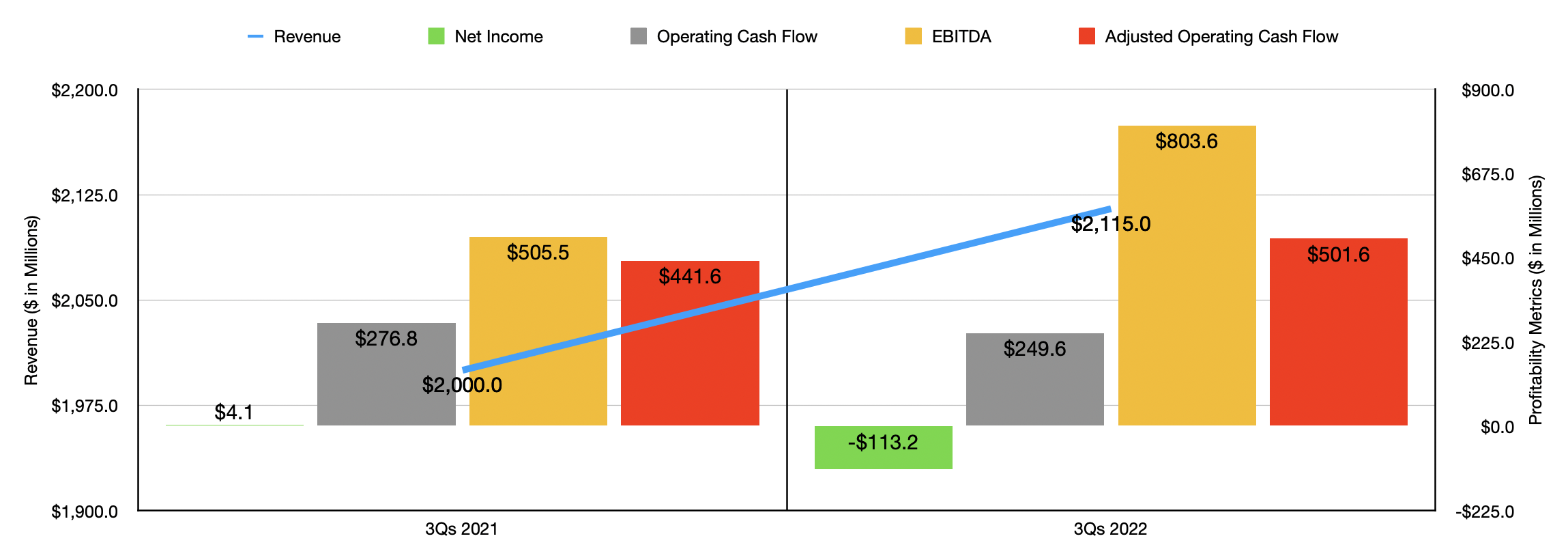

In the latest quarter for which data is available, the third quarter of the company's 2022 fiscal year, sales came in at $713.1 million. This represents a decrease compared to the $727 million generated the same time last year. This is particularly noteworthy because, for the first nine months of 2022 as a whole, AppLovin Corporation sales are actually up compared to the same time last year. Revenue of $2.12 billion is 5.8% higher than the nearly $2 billion generated the same time of 2021. To call the financial weakness the company experienced in the latest quarter "newfound" would be a mistake. In fact, in some respects, that weakness has been building for some time.

{kind=link}

The biggest culprit from a sales perspective has been the consumer revenue the company generates. In the latest quarter alone, sales of $272.4 million pale in comparison to the $377.4 million reported the same time last year. This 28% plunge was driven primarily by decreases in revenue from two of the company’s leading apps. These are Project Makeover and Machington Mansion. These two apps, combined with a third app called Wordscapes, still represent around 20% of revenue despite the plunge in sales associated with the first two. Unfortunately, this should not be all that surprising to investors. After all, the app space, particularly when it comes to gaming, can fluctuate significantly over short windows of time based on consumer sentiment. Games that were once popular can become unpopular almost overnight. When it comes to the company's app operations, weakness has been building for some time. In the third quarter of 2021, for instance, the firm had 2.9 million monthly active players across its ecosystem that generated, on average, $44 apiece. By the third quarter of this year, this number had dropped to 2.2 million and $41. It's also important to note that business revenue under the apps operations for the company also dropped, falling 14% from $156.2 million to $134.1 million. This decline, management said, was mostly driven by a decrease in price per advertising impression even as the number of advertising impressions remained flat.

{kind=link}

For an app company to be experiencing this kind of pain is truly awful. In most cases, this would lead me to become incredibly bearish about the firm in question. However, there is another side of the company that happens to be doing incredibly well. This is the software platform side of the business, which centers on a variety of activities such as offering a comprehensive suite of tools for developers in order to get their mobile apps discovered and downloaded by the right users, much of which is centered around marketing and advertising activities. This portion of the company continues to thrive even during these difficult times. During the latest quarter alone, revenue here came in at $306.6 million. That's 59% higher than the $193.3 million reported the same time last year. AppLovin Corporation management chalked this up largely to AppDiscovery, with installations coming in 19% higher year-over-year and price per installation climbing 33% during this time. Other drivers included the contribution from Wurl and continued growth of its MAX offering.

This is a portion of AppLovin Corporation that continues to grow. For instance, as of the end of the latest quarter, the company boasted 538 SPECs (Software Platform Enterprise Clients), which the company defines as third-party clients from whom they have collected greater than $125,000 in revenue over the prior 12-month window. This was up from the 292 reported the same time last year and compared to the 503 reported in the second quarter of this year. The average revenue per SPEC has also been on the rise, totaling $1.90 million over the prior 12 months compared to the $1.59 million reported the same time one year earlier. In the latest quarter alone, this portion of the enterprise carried the largest level of profitability, accounting for 73.8% of the company's segment EBITDA.

{kind=link}

This portion of the business remains alive and well, with overall profitability for the firm improving as of late. Net income in the latest quarter was $23.7 million. That compared to the $0.2 million reported the same time last year. Operating cash flow over this year has fallen from $124.5 million to negative $188.3 million. But if we adjust for changes in working capital, it would have risen from $158.1 million to $237.4 million, while EBITDA increased from $190.7 million to $257.6 million. Profitability for the company has been somewhat mixed for the first nine months of 2022 compared to the first nine months of 2021 as a whole. This much can be seen in the chart above.

When it comes to the 2022 fiscal year in its entirety, management has had to scale back expectations. Now, they are forecasting revenue of between $2.80 billion and $2.81 billion. Previously, the range was between $2.84 billion and $3.14 billion. When it comes to profitability, the only metric that they provided guidance on was EBITDA. This is expected to be between $1.05 billion and $1.07 billion for the current fiscal year. That compares to the $1.20 billion previously anticipated. If we assume that operating cash flow, on an adjusted basis, will rise at the same rate that EBITDA is forecasted to at the midpoint, then we would anticipate a reading this year of $641.8 million.

{kind=link}

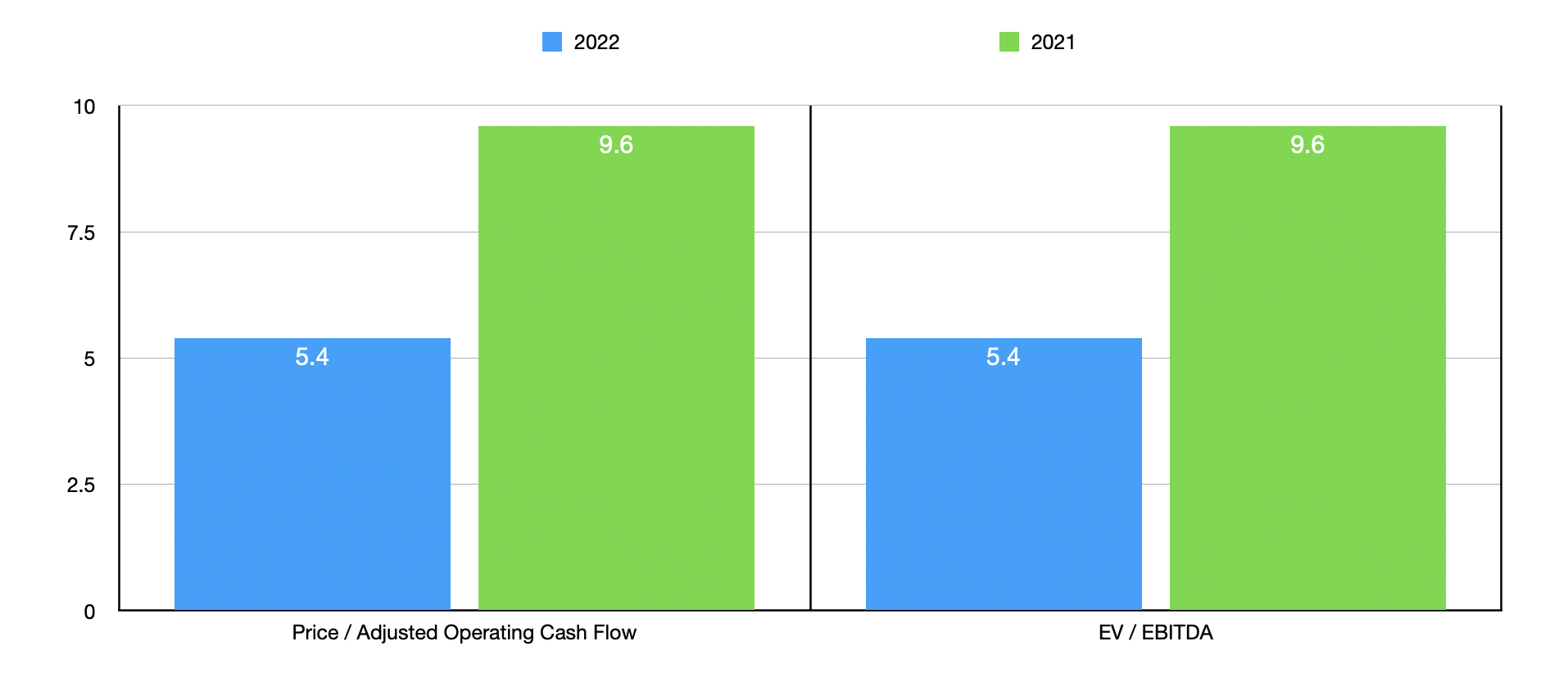

Based on these figures, AppLovin Corporation stock is trading at a forward price to adjusted operating cash flow multiple and at a forward EV to EBITDA multiple of 5.4. By comparison, if we were to use the data from 2021, these multiples would both come in at 9.6. As part of my analysis, I compared the company to five similar firms. On a price to operating cash flow basis, these companies ranged from a low of 8.8 to a high of 534.5. Only one of the five companies was cheaper than AppLovin. Meanwhile, using the EV to EBITDA approach, the range was from 11.3 to 40.5 for the four firms that had positive results. In this case, our prospect was the cheapest of the group.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| AppLovin |

| 5.4 |

| 9.6 |

| Bill.com Holdings ( BILL ) |

| 534.5 |

| N/A |

| Black Knight ( BKI ) |

| 30.6 |

| 18.9 |

| Aspen Technology ( AZPN ) |

| 44.9 |

| 39.9 |

| Open Text ( OTEX ) |

| 8.8 |

| 11.3 |

| Bentley Systems ( BSY ) |

| 37.9 |

| 40.5 |

Takeaway

Based on all the data available, it seems to me as though AppLovin Corporation definitely has some issues. But when you look at what I believe would be the core of the business, you see an enterprise that is continuing to grow nicely even during difficult times. Investors should be prepared for additional pain on the app development side because of the nature of that market. And because of the pain experience, I do understand why AppLovin Corporation shares have fallen rather significantly.

In truth, AppLovin Corporation stock probably did deserve to fall some. But by this point, shares look significantly cheaper than they probably should be. Because of this, I've decided to increase my rating on the company from a "buy" to a "strong buy," reflecting my belief that shares should significantly outperform the market moving forward.

For further details see:

AppLovin: This Plunge In Price Presents A Great Opportunity (Rating Upgrade)