TANNI - April's 5 Dividend Growth Stocks With 6.30%+ Yields

2023-04-18 17:10:24 ET

Summary

- With a rocky market, we seem to have some new names appearing in this latest month with higher yields available.

- Three of the five names we will touch on are related to the financial space, though they are not banks.

- Expecting a recession later this year could bring even better valuations, but it's always worth scouring the landscape to see what could be out there.

Written by Nick Ackerman. This article was originally published to members of Cash Builder Opportunities on April 5th, 2023.

Dividend growth stocks aren't always the most exciting investments out there. They often aren't grabbing the headlines; they aren't the stocks running up hundreds of percentages in a year. In fact, they are often some of the least exciting stocks. And that is precisely their strongest selling point. With such a vast world of dividend growth stocks available out there, it is important to screen through to see if there are any worthwhile investments to explore.

They are stocks that provide growing wealth over time to income investors. Dividend growers are often larger (not always), more financially stable companies that can pay out reliable cash flows to investors. Some are slower growers than others. Some are going to be cyclical that require a strong economy. Some are going to be secular, which doesn't generally rely on a more robust economy.

Dividend growth can promote share price appreciation. Of course, that is if these companies are growing their earnings to support such dividend growth in the first place. Trust me. There are yield-traps out there - I've owned a few that I'm not particularly proud of.

I like to think of investing in dividend stocks as a perpetual loan of sorts. Essentially, every dividend is a repayment of your original capital. Eventually, holding long enough, you have the position "paid off." It is all return back into your pocket from that point forward.

The market has been rocked by bank collapses, and that has led to the idea that we will only need another one or two rate hikes of 25 basis points each. The bank failures show us that things are starting to break due to the higher rates. This idea of potentially seeing fewer rate hikes was further supported by the latest inflation data continuing to show cooling.

While still high, the trend is going lower. The latest payroll data showed jobs are weakening, as well as they came in below expectations for the month. Additionally, job openings slumped to below the 10 million level , which is seen as another good sign in terms of the fight against inflation.

However, the latest OPEC+ cuts announced put another wrinkle into the future. Higher energy prices could cause inflation to remain sticky once again as it impacts prices across the board.

All of this being said, it's important to understand my approach to dividend stocks and why screening dividend stocks can be important for income investors. These are April's 5 dividend growth stocks that might be worthwhile for a deeper exploration. As with any initial screening, this is just an initial dive - more due diligence would be necessary before pulling the trigger.

The Parameters For Screening

I'll be using some handy features that Seeking Alpha provides right here on their website for this screen. In particular, I will be screening utilizing their quant grades in dividend safety, dividend growth and dividend consistency.

Dividend Safety is relatively self-explanatory. These will be stocks that SA quants show reasonable safety compared to the rest of their various sectors. The grade considers many different factors but earnings payout ratios, debt and free cash flow are amongst these. This category will be stocks with A+ to B- ratings.

For the dividend growth category, we have factors such as the CAGR of various periods relative to other stocks in the same sector. Additionally, the quants also look at earnings, revenue and EBITDA growth. As we will see, this doesn't mean that every stock with a higher grade has the growth we are looking for. This just factors in that the dividend has grown or earnings are growing to support dividend growth possibly. For these, the grades will also be A+ through B- grades.

Finally, for dividend consistency, we want stocks that will be paying reliable dividends for us for a very long time. In particular, hopefully, they are raising yearly, though that isn't an explicit requirement. We will also include stocks with a general uptrend in dividend payments, which means there could have been periods where they paused increases for a year or two.

After looking at those factors alone, we are left with 547 stocks at this time from March's 540 listings. I'll link the screen here , though it is a dynamic list that constantly updates regularly. When viewing this article, there could be more or less when going to the link.

From there, I wanted to narrow down the list a lot more. I then sorted the list by forward dividend yield, highest to lowest. Since these will be safer dividend stocks in the first place, screening for those among the higher payers shouldn't hurt.

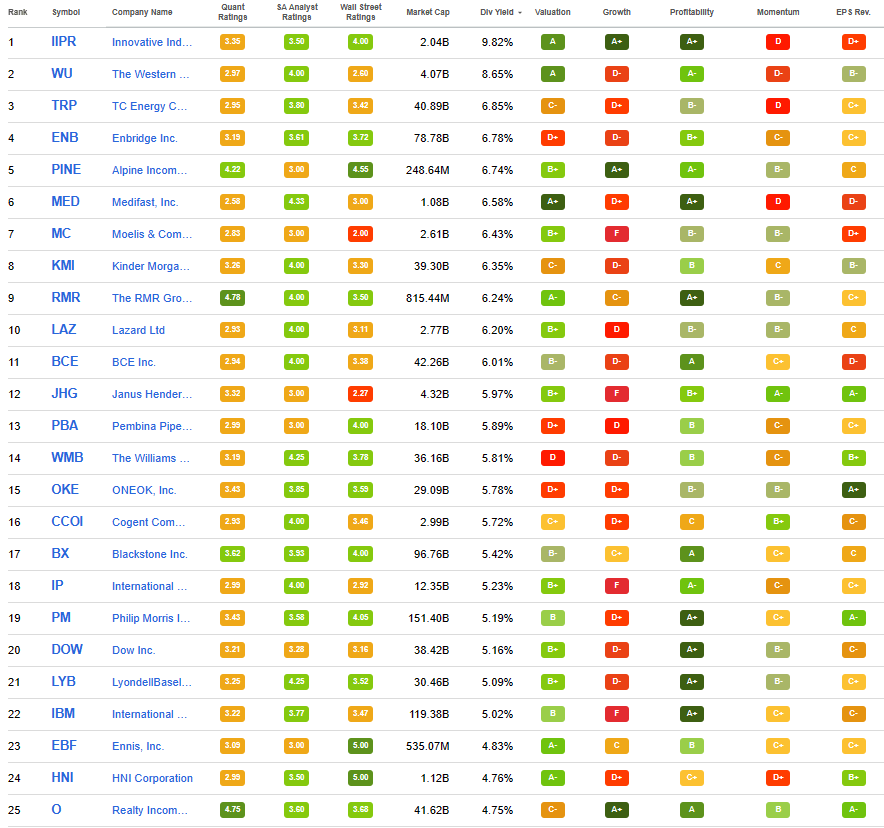

I will share the top 25 that showed up as of 04/05/2023.

{kind=link}

We've covered The Western Union ( WU ), TC Energy Corp ( TRP ), Enbridge ( ENB ), Alpine Income Property Trust ( PINE ) and Medifast ( MED ) within the last couple of months, so we will be skipping over looking at those today.

That leaves us with Innovative Industrial Properties ( IIPR ), Moelis & Company ( MC ), Kinder Morgan ( KMI ), The RMR Group ( RMR ) and Lazard Ltd ( LAZ ) to touch on today. KMI and RMR are new names to the list that we haven't covered since beginning these screens. IIPR and MC were touched on last in January 2023, and LAZ last appeared on this list in June 2022.

Innovative Industrial Properties 9.89% Yield

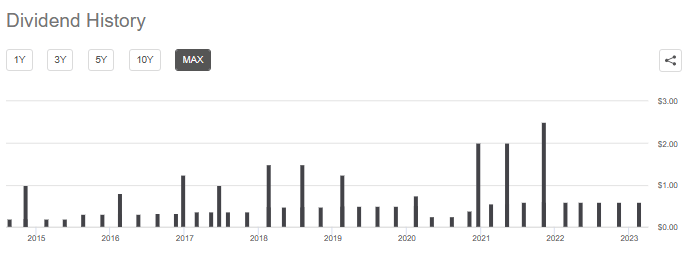

IIPR is particularly of interest to me as it's a position I own personally. At one point, being the best investment I made at its highs, the position is now firmly in the red. Of course, with a cannabis REIT position, that's par for the course. This has seen IIPR's yield rise rapidly as the share price collapsed.

YCharts

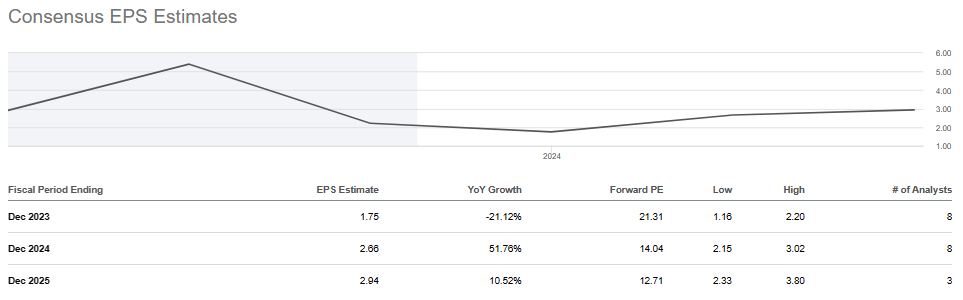

They had a track record of raising their dividend every quarter, then switched to a schedule of looking at raises every two quarters. However, given the headwinds in the space, they are holding firm at the $1.80 quarterly for now. The rapid growth has stopped, but the expectation for some small growth in FFO going forward remains if the forecasts are right. Based on the current dividend and next fiscal year's forecast, we are looking at a payout ratio of around 90%.

{kind=link}

Looking at FCF per share, in 2022, this came to $8.51, which would drop the payout ratio on that metric to around 85%.

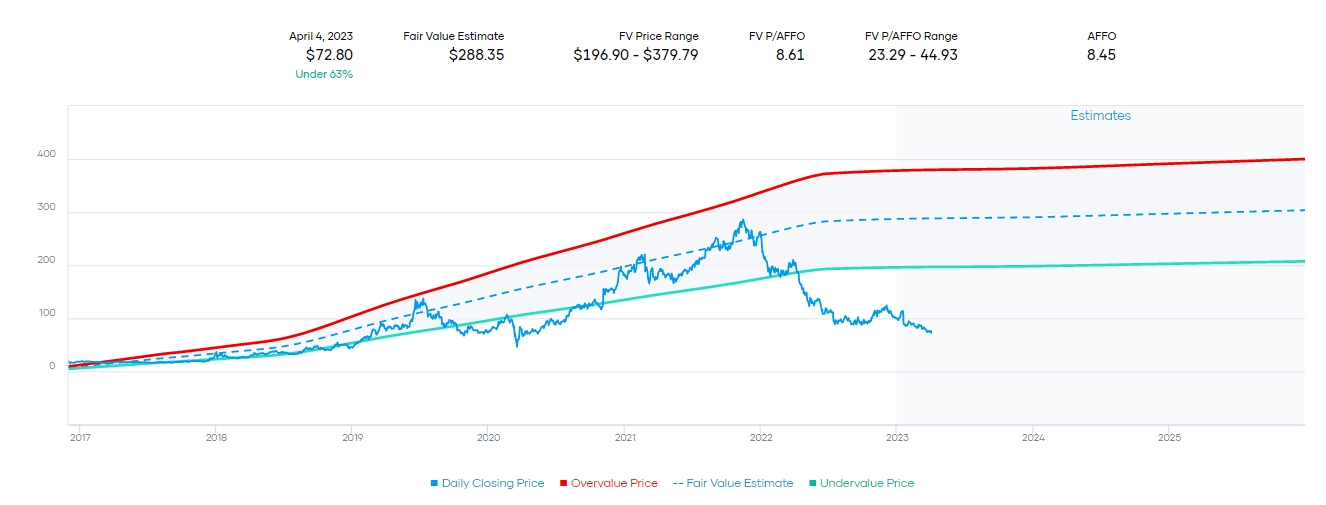

Based on the fair value historically, it would appear that IIPR is dirt cheap. Of course, that fair value is also based on the rapid growth that they had been experiencing. With that drying up, the valuation at the current level appears to make more sense.

{kind=link}

IIPR continues to remain a highly speculative name, but I wouldn't expect any less with the industry they are in, providing properties and buildings to a speculative industry.

Moelis & Company 6.43% Yield

MC has been hit particularly hard as they operate as an investment banking advisory firm, providing services for capital market transactions, mergers and restructurings. With our current environment and a lack of interest in these particular areas, the company has shown a significant drop in its earnings power. Jeremy Blum put together a recent article detailing the headwinds for capital market activities. While it will recover at some point, most likely, it isn't likely to be in this current year, given analysts' expectations.

{kind=link}

This doesn't make it a bad potential play, but with a recession expected later this year and weaker earnings still anticipated, investors could get a better price later. Calling the bottom would be extremely hard, though, as this is the type of name you buy when things look ugliest - at least, that is the basic idea. For a longer-term investor, it can make sense to dollar-cost average, assuming you aren't a psychic that can forecast the future.

Along with EPS estimates going lower, FCF per share dropped to $0.41 in 2022. That means that their freezing of the dividend at $0.60 quarterly will likely continue for the foreseeable future. However, that's on the bright side if they maintain the same dividend. On the other hand, a dividend cut can't be ruled out if we are following the numbers.

{kind=link}

The last time they cut their regular dividend was during the 2020 pandemic, but they quickly upped it as market activity was strong following that crash. The next recession might not see such a quick recovery, but that doesn't mean it won't recover in the future.

Kinder Morgan 6.35% Yield

Seeing KMI show up on this list is quite interesting; it's the first time we've seen this name. Historically, KMI was incredibly popular with income investors in the earlier 2010s as they showed huge promise as the U.S. shifted to energy independence.

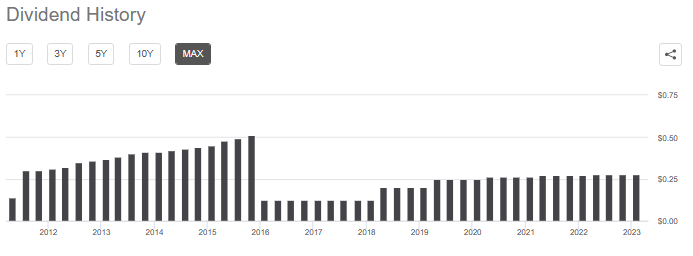

Of course, we all know how that ended with a glut by the mid-decade and in 2016 , KMI slashed its dividend. Making it an income favorite no more, and instead repelled investors. However, the pressure on the share price began earlier, even before this. This was also shortly after KMI was reorganized into a single C-corp. Since then, the dividend growth hasn't necessarily been the strongest, but they are heading in the right direction.

{kind=link}

Anyway, that's the quick history version of KMI. Energy prices have once again been coming down more recently, but OPEC+ cutting production sent a clear message that they were looking to support the price of crude oil further. That saw the price per barrel rising rapidly. While KMI is primarily a natural gas pipeline company , the share price at first reacted positively before the overall market slumped due to the anticipation of a weaker economy.

KMI Business Mix (Kinder Morgan)

Analysts have an average price target of $20.16 on this name, which would suggest a bit of upside from here. However, they get an overall "Hold" rating from analysts with five strong buys, one buy, 15 holds and two strong sells.

As a midstream company, they shouldn't be so susceptible to energy prices, but that doesn't mean they aren't impacted at all. They highlight that 93% of their cash flows are "take-or-pay, hedged, & fee-based cash flows."

History shows us that they are impacted nonetheless, meaning we should expect them to be a cyclical play. We could see added weakness during a recession, which could present a better opportunity to pick up a position. The added pressure of weaker energy prices is likely to weigh on this name for now, and dividend growth could remain slow for that reason.

On the brighter side, net debt has come down from the levels they were at years ago, which could leave them in a better financial position. The current dividend also appears to be covered.

{kind=link}

The RMR Group 6.24% Yield

RMR is an interesting name, and admittedly, not a name I've heard of. In their words, they are "a leading U.S. alternative asset management company, unique for its focus on commercial real estate and related business."

They have around $37 billion in AUM, so relatively small compared to some of the other players in the space. Apollo Group ( APO ) has around $513 billion, and Blackstone ( BX ), the world's largest alternative asset manager, is close to the trillion-dollar mark. That's to provide some perspective on the size of RMR.

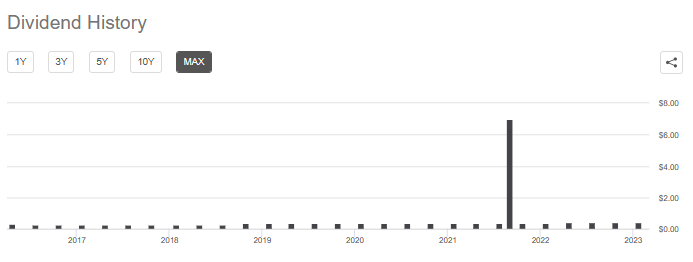

Size alone doesn't tell us if they can be successful or not, as they've been able to provide a growing dividend to investors. However, a sizeable special makes this a bit visually harder to see.

{kind=link}

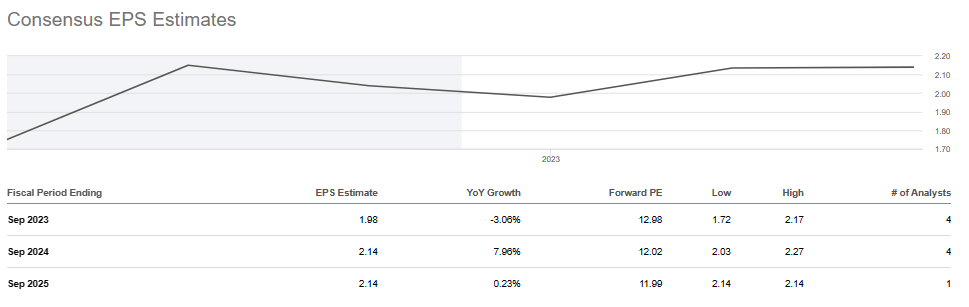

Earnings expectations for the coming year are weaker, but this isn't a surprise, as we've seen this from many other companies, too, large, small, and everything in between. Analysts are just realistic for the current environment. For RMR, the decline is only expected to be quite shallow, though, meaning that continuing the same dividend shouldn't be a problem. The forward payout ratio based on consensus EPS would be around 81%.

{kind=link}

Though they also provide distributable earnings that were higher in the latest quarter, meaning that the payout ratio is likely lower. Based on that metric provided, they highlighted that the payout ratio was 62.4%.

This quarter we reported adjusted net income of $0.51 per share, distributable earnings of $.58 per share, adjusted EBITDA of $26.4 million, and adjusted EBITDA margin of 50.8%. Finally, we again declared our dividend of $0.40 per share this quarter, which remains secure and well covered as evidenced by our 62.4% distribution payout ratio.

A win for RMR recently seems to be BP's ( BP ) buyout of TravelCenters of America ( TA ). Ross Bowler recently outlined more details on those events.

Lazard Ltd 6.30% Yield

Perhaps unsurprisingly, this is another company tied to the market fortunes as an investment banking and brokerage firm. I say unsurprisingly because, given the current environment we are in, the share prices of asset managers have been sliding. AUM has been challenged when valuations are declining with the broader markets. So, we have three names that are significantly impacted by what the broader markets are doing this month, with LAZ being the third one after MC and RMR.

LAZ's latest announcement saw AUM down 3% in February from January 2023. The biggest hit was from market depreciation, but outflows also played a role. At a total AUM of $224.2 billion, this is quite a bit larger than RMR as an alternative asset manager. It also makes it fairly small compared to other traditional asset managers. The financial advisory business segment they have also is impacted, just as MC is, due to a slowdown in M&A and other market activities.

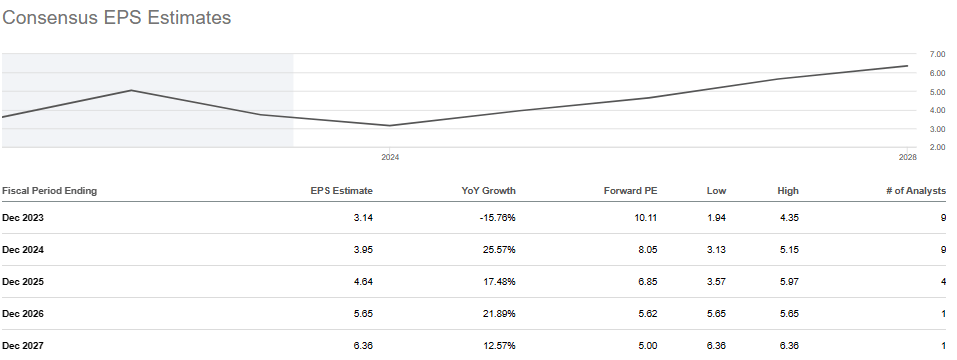

With that being said, again, it's no surprise to see EPS estimates show a decline in the coming fiscal year. However, analysts are also expecting a quick recovery for LAZ.

{kind=link}

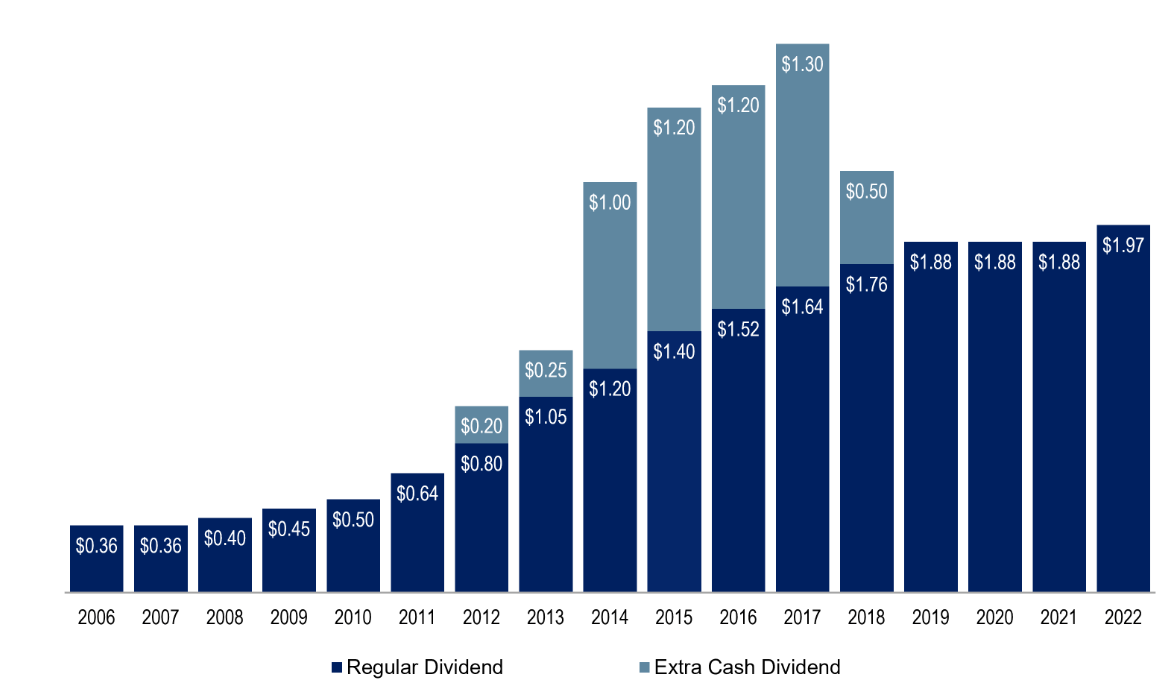

The extra large distributions have ended that they were able to provide from around 2012 to 2018 . After that, there was a hiatus in raises, but they more recently bumped it up once again in 2022.

Based on the anticipated $2 in the annualized dividend at this time against the expected EPS, we see a payout ratio of 63.7%. This leaves a lot of room for safety or where a raise would be expected later this year even.

Worth noting is that LAZ is a partnership , so it will issue its shareholders a K1.

{kind=link}

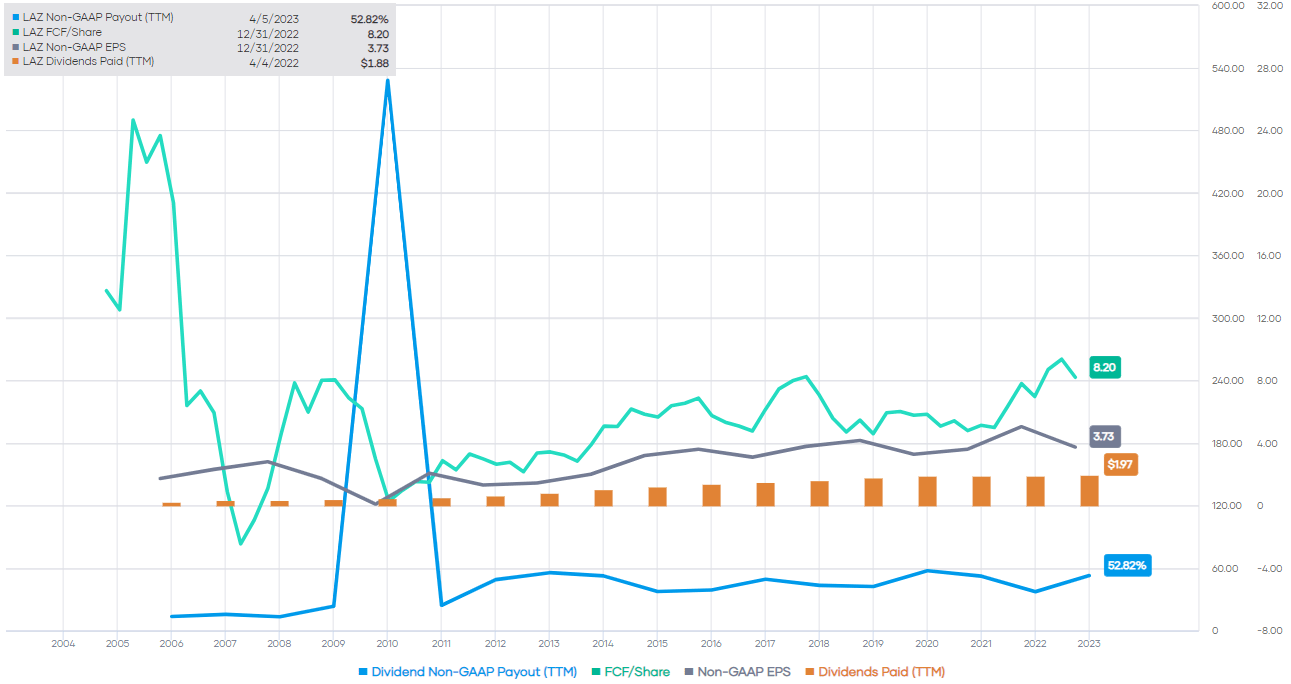

Perhaps even more impressively, LAZ has been able to provide some monster FCF. That could make an investor feel even more comfortable with the current level of distribution for investors.

{kind=link}

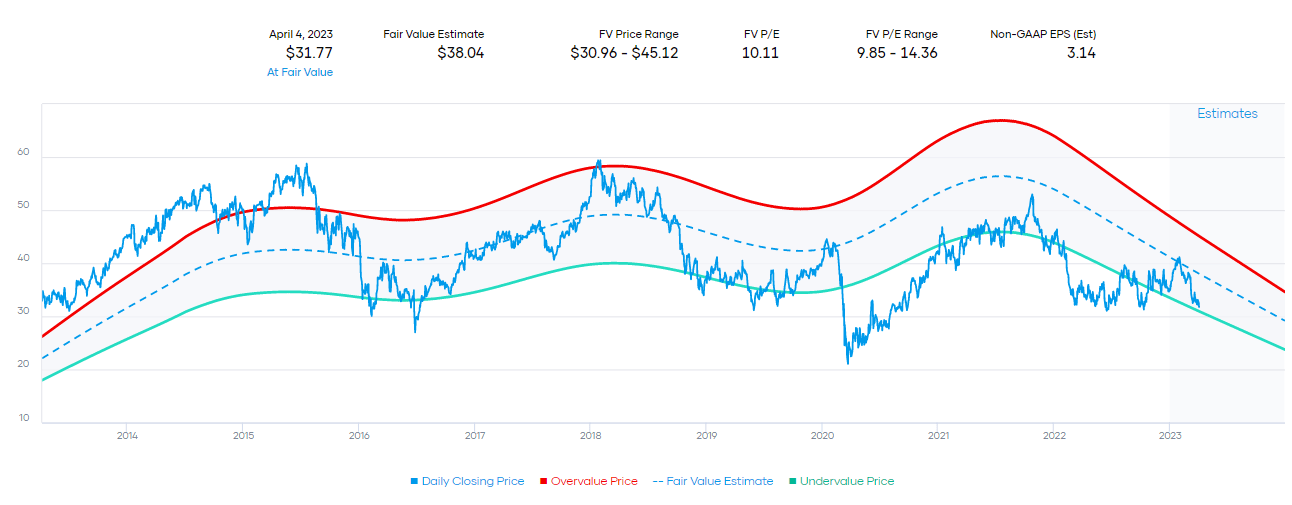

Based on the fair value estimate for LAZ, we are looking at shares trading near the lower end.

{kind=link}

Of course, that is with the assumption that things don't continue to deteriorate perpetually from here in terms of their earnings. However, much like the other companies that are linked to the market in this month's dividend screening article, a recession would likely send shares even lower. Being more patient or utilizing a dollar-cost averaging approach could be more appropriate. That seems to be one of the key and general themes during this uncertain period.

For further details see:

April's 5 Dividend Growth Stocks With 6.30%+ Yields