AMBP - AptarGroup: A Solid Business That's Just A Bit Too Pricey

Summary

- AptarGroup has had a solid track record in recent years, especially when it comes to revenue and cash flows.

- The firm continues along that path and will likely generate value for its shareholders in the long run.

- But the stock does look lofty, especially compared to similar enterprises.

In my opinion, some of the most interesting companies are those that touch our everyday lives often without our own knowing. For instance, practically everybody has, at one point or another, used some sort of drug to treat an illness. While some attention may be paid to the drug itself, practically none of the attention is given to the company that produced the drug delivery system or packaging. But behind the scenes are multiple companies, some of them worth billions of dollars, that make the delivery of the drugs possible. One such firm that warrants the attention of investors is AptarGroup ( ATR ).

From a sales and cash flow perspective, the general trajectory of the company has been positive in recent years. Long term, I have no doubt that the enterprise will continue to do quite well for itself. But this does not necessarily mean that the company makes for a great prospect at this time. While I wouldn't exactly call shares of the enterprise expensive, I would say that they aren't undervalued at this moment. For those with a very long investment horizon, buying the stock may even make sense. But for value-oriented investors, I would say that shares are more or less fairly valued at this time and, as such, I have assigned it a ‘hold’ rating to reflect my view that the stock should move up or down more or less in line with what the broader market should for the foreseeable future.

A niche business with a global reach

As I mentioned already, AptarGroup serves as a designer and producer of drug delivery solutions and services, but that's not all the company does. It also is engaged in producing and selling consumer product dispensing and active material science solutions and services for its customers as well. In total, the company services various end markets, such as the pharmaceutical space, beauty and personal care space, home care, food and beverage, and more. And since its founding in the 1940s, when it focused initially on producing aerosol valves in the US alone, the company has grown to have employees in 20 different countries. And in terms of overall product sales, its reach extends throughout North America, Europe, Asia, and South Africa.

To better understand the company though, we should dig into each of its individual operating segments. The first of these is the Pharma segment, which accounts for about 40% of the company's revenue and 65% of its profits. Through this segment, the business supplies nasal drug delivery spray pumps and metered dose inhaler valves to the pharmaceutical and healthcare markets. About 42% of sales under this segment in total involve the prescription drug niche, with its offerings capable of delivering medications nasally, orally, or topically. One of the most popular uses of its products under the segment involves nasal allergy treatments. A further 23% of sales under the segment go to the consumer healthcare category. And 22% is attributable to injectables that management describes as elastomeric primary packaging components that include stoppers for vials and prefilled syringe components like plungers, tip caps, and more. The company also provides a platform product that is integrated into at-home COVID-19 test kits in order to protect against moisture and protect the integrity of the test kits. And on top of this, the company also serves the digital health market to aid in the remote monitoring of the health of patients when needed.

The next segment is called Beauty + Home, and it is responsible for roughly 44% of the company's revenue and 23% of its profits. About 49% of the sales of this segment include beauty products such as spray and lotion pumps, flow control components, sampling dispensing systems, and more. It also is responsible for personal care products such as lotion pumps, fine mist spray pumps, continuous spray aerosol valves, and more. Plus it's involved in the home care space through its portfolio of continuous and metered dose spray aerosol valves, lotion pumps, and more. The third and final segment the company has is the Food + Beverage segment. According to management, this unit is responsible for roughly 16% of the company's sales and 12% of its profits. This portion of the company focuses on dispensing closures, absorbent and non-absorbent food trays, and other related offerings for the food space, as well as similar products for the beverage market.

{kind=link}

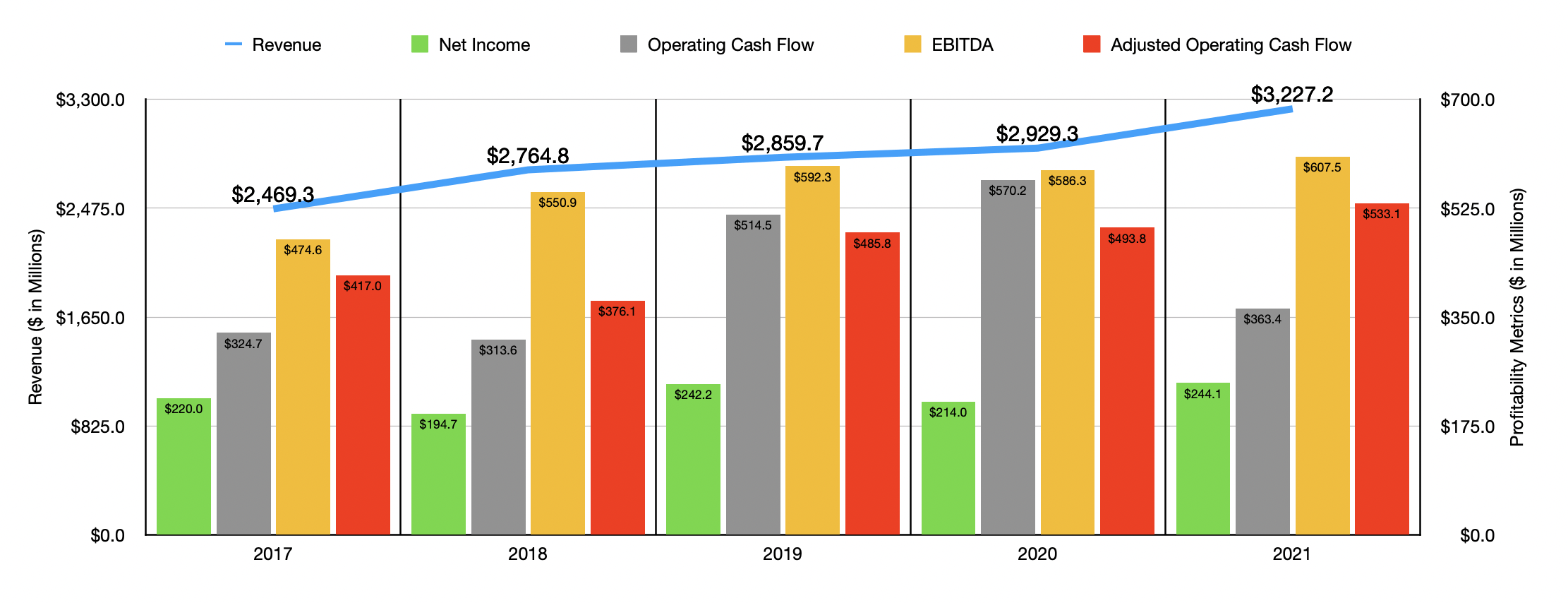

Over the past five years, the management team at AptarGroup has done a good job growing the enterprise. Sales have increased over each of the past five years, climbing from $2.47 billion in 2017 to $3.23 billion in 2021. The roughly 10% rise in revenue from 2020 to 2021 was driven largely by a significant contribution from its core activities. Core sales growth was a robust 7%, with 4% due to price adjustments aimed at passing through higher resin and other input costs to its customers. Most of that growth came from the Food + Beverage segment. Acquisitions added another 1% to the company's revenue, while foreign currency fluctuations contributed 2%.

Although sales have risen rather consistently, profits have been a bit less consistent. Between 2017 and 2021, net income for the company bounced around between a low point of $194.7 million and a high point of $244.1 million. Operating cash flow generally increased between 2017 and 2020, rising from $324.7 million to $570.2 million. But then, in 2021, it plunged to $363.4 million. If we were to adjust for changes in working capital, however, we would have seen that the metric would have continued rising in 2021, totaling $533.1 million compared to the $493.8 million reported one year earlier. A similar trend can be seen when looking at EBITDA, with the metric ultimately peaking at $607.5 million in 2021 compared to the $474.6 million that it experienced back in 2017.

{kind=link}

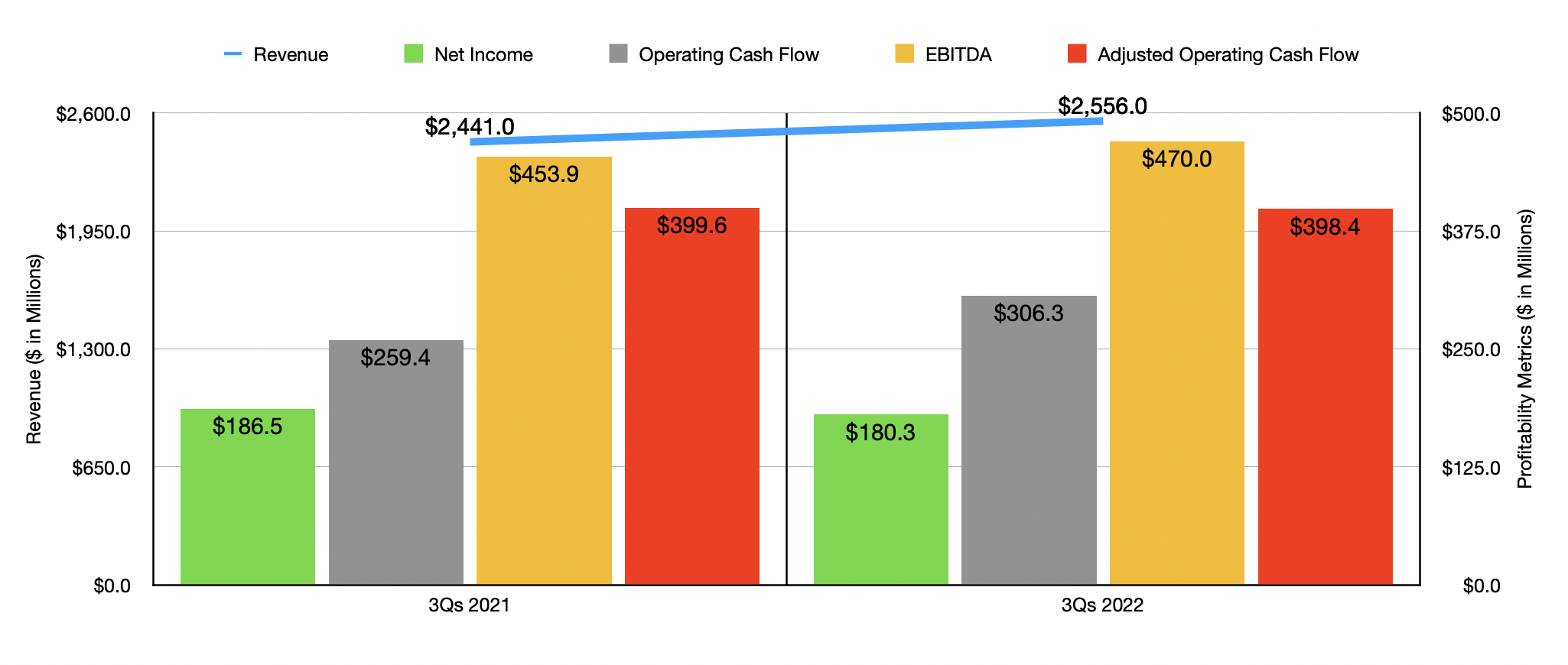

When it comes to the 2022 fiscal year, management has only so far provided data for the first nine months . But for the most part, that data has not been bad. Revenue of $2.56 billion beat out the $2.44 billion reported the same time one year earlier. Net income dropped year over year, falling from $186.5 million to $180.3 million. This was offset to some degree by operating cash flow rising from $259.4 million to $306.3 million. On the other hand, on an adjusted basis, that figure also dropped year over year, declining from $399.6 million to $398.4 million. Meanwhile, EBITDA hit $470 million in the first nine months of 2022. That's up from the $453.9 million reported one year earlier.

{kind=link}

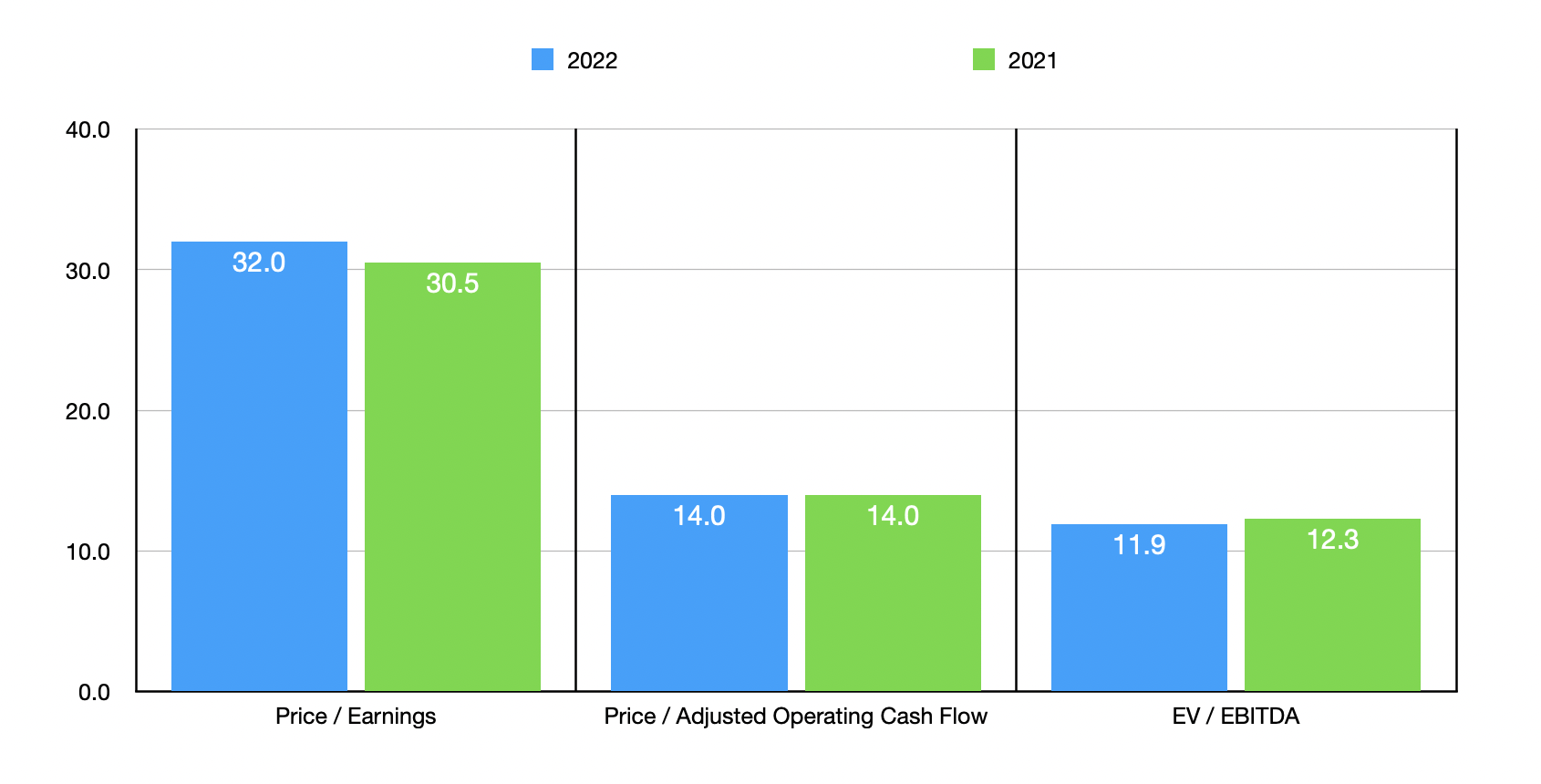

When it comes to guidance, the only thing management said is that earnings per share, on an adjusted basis, should be between $0.73 and $0.83 for the final quarter of 2022. At the midpoint, that would mean net income for 2022 in its entirety of $232.2 million. If we then annualize the other profitability metrics, we would get adjusted operating cash flow of $531.5 million and EBITDA of $629 million. Based on these numbers, the company is trading at a price-to-earnings multiple of 32, a price to adjusted operating cash flow multiple of 14, and an EV to EBITDA multiple of 11.9. In the chart above, you can see how this looks if we were to value the company using data from 2021 instead. As part of my analysis, I also compared the company to five similar enterprises. On a price-to-earnings basis, these companies ranged from a low of 10.6 to a high of 14.7. In this scenario, AptarGroup was the most expensive of the group. Using the price to operating cash flow approach, the range was from 5.2 to 17.5, while the range using the EV to EBITDA approach would be from 7.4 to 53.5. In each of these scenarios, four of the five companies were cheaper than our prospect.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| AptarGroup |

| 32.0 |

| 14.0 |

| 11.9 |

| Berry Global Group ( BERY ) |

| 10.6 |

| 5.2 |

| 7.6 |

| Silgan Holdings ( SLGN ) |

| 14.7 |

| 13.2 |

| 10.3 |

| Crown Holdings ( CCK ) |

| N/A |

| 13.6 |

| 53.5 |

| Greif ( GEF ) |

| 11.2 |

| 6.4 |

| 7.4 |

| Ardagh Metal Packaging SA ( AMBP ) |

| 13.5 |

| 17.5 |

| 8.4 |

Takeaway

Operationally and financially, I have taken quite a liking to AptarGroup. Its business model is interesting to me and it's diverse enough that it has the potential to do well in most environments. When it comes to the EV to EBITDA approach, shares do look quite affordable on an absolute basis, even though they are pricey relative to similar businesses. But because of how the stock is priced using the other two metrics and because of some of the lumpiness we have seen in profitability, I believe that a more appropriate rating for the enterprise at this time is a ‘hold’.

For further details see:

AptarGroup: A Solid Business That's Just A Bit Too Pricey