ARMK - Aramark: Bullish As Cheap Share Price Mixes Well In Soup Of Earnings Growth

2023-12-12 21:41:57 ET

Summary

- Aramark rated Strong Buy, more bullish than the consensus today on Seeking Alpha.

- Tailwinds from the cheap share price, earnings and revenue growth, strong client retention, declining debt, and growing equity.

- Headwinds from the modest risk of recently losing two major university contracts in 2023.

- Dividend yield below 2%, however, 10-year dividend growth positive.

Stock Snapshot

Often, I will come across an under-covered stock here for a company that provides a lot of the behind-the-scenes services that make everyday things function, one of them being food services.

My first time learning about Aramark ( ARMK ) was in the early 2000s as a college student living on campus and using the campus dining hall 3x daily. Aramark was the vendor that managed the dining hall, for example, and made it possible for hundreds of students to be fed daily.

Some more quick facts about this company include the fact that they operate across a spectrum of solutions including food services, facilities management, supply chain services, and more. Recently, their uniform services segment spun off to become Vestis , an independent company.

Another fun fact is that their food services division "serves over 275 colleges and universities."

Scoring Matrix

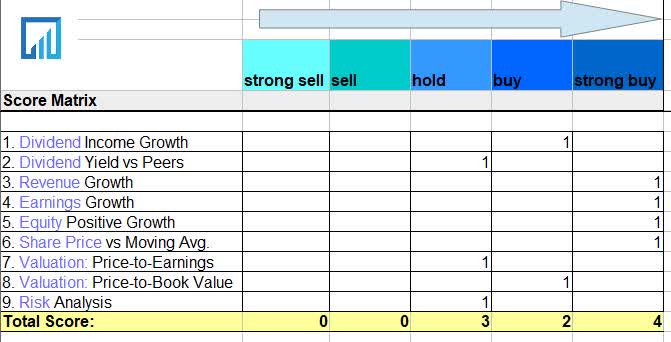

This article uses a 9-point scoring matrix that holistically considers multiple angles of the stock, with an emphasis on cash flow potential for investors and fundamental trends from the key accounting statements publicly available such as the balance sheet and income statements, as well as a future-looking outlook on this stock.

Today's Rating

{kind=link}

Based on the score total in the score matrix above, this stock is getting a rating of strong buy , although a potential hold rating would have come in a close 2nd place.

Compared to the consensus rating on Seeking Alpha, I am actually going to be contrarian this time and be more bullish than the consensus, which today has shown a mixed sentiment on this stock:

Aramark - rating consensus (Seeking Alpha)

Dividend Income Growth

This section uses dividend growth data to explore the 10-year dividend income growth for a hypothetical investor owning 100 shares, to determine whether this stock is a great dividend income opportunity.

{kind=link}

Using the above dividend growth chart, we can start with 2014 when the company paid an annual dividend of $0.23/share. As a hypothetical example, if my portfolio had bought 100 shares then, it would have seen $23 in dividend income that year.

Fast forward to 2022 and the annual dividend went up to $0.32/share ($32 in income), a 39% growth in a decade.

Should the company continue with this dividend growth rate, which is just an assumption, by 2032 we could see $0.44/share and $44 dividend income annually, a 91% growth from 2014 to 2032, an 18-year period.

In this category, I will call it a buy , on the basis of a modestly growing dividend income potential, while not being anything extraordinary, along with a history of steady quarterly payouts in the last several years.

Dividend Yield vs Peers

This section uses dividend yield data to compare the trailing dividend yield vs 3 similar peers in the same sector, to determine if this stock presents the most competitive dividend yield on capital invested.

{kind=link}

In the above chart, I am comparing my focus stock Aramark with a peer in the food-service solutions space, Sysco ( SYY ), as well as related food service stocks like ONE Group Hospitality ( STKS ) and Yum! Brands ( YUM ).

Of this peer group, Aramark came in third place with a trailing dividend yield of just 1.24% (1.40% forward yield), while Sysco led the pack with a yield of 2.68%.

If I was looking to pick one in terms of best dividend return on capital invested, in this case, I would go with Sysco.

In this category, I will call Sysco a hold , on the basis of having a subpar dividend yield vs a key peer, with a quarterly dividend of only $0.10/share.

Revenue Growth

This section explores this company's revenue growth trends over the last year, using data from the income statement.

What this data point tells us is that in the quarter ending September, the company saw $4.9B in total revenue, vs $4.39B in Sept 2022, a +11.6% YoY growth. Also worth mentioning is that since Sept 2022 the top-line revenue has generally been on an uptrend, and this last quarter compared to April 2022 it was a +27% growth.

The nature of this business is that it has to keep existing contracts while also growing new accounts. What the company said in its quarterly comments indicates that both existing and new business did well:

Annualized gross new business totaled $1.2 billion, representing 8.8% of prior year revenue ? Retention at 95.5%, maintained significant improvement vs. historical levels.

Further, the company provided a positive top-line outlook for FY24:

Entering fiscal 2024, Aramark is already off to a strong start and remains confident in the robust sales pipeline for the remainder of the year to achieve its target Net New Business at 4% to 5% of prior year revenue.

Notably, also, its core business of food service saw really strong organic growth, as per their quarterly results presentation :

{kind=link}

I am calling it a strong buy in this category, on the basis of proven YoY positive growth as well as longer-term revenue growth trends, new business growth, and strong retention of existing clients, as well as positive forward outlook.

Earnings Growth

This section explores this company's earnings (net income) growth trends over the last year, using data from the income statement.

What we can gather from this section is that the company achieved $205MM in net income (earnings) in the quarter ending September, vs $75.8MM in Sept 2022, a 170% YoY improvement . Also, after March 2023 the earnings have improved in the subsequent two quarters that followed.

One notable item to mention is the decline in interest expense since it can impact the bottom line result. The company saw interest of $85.4MM this last quarter vs $89.7MM in Sept 2022, a +4.8% decline. It also declined significantly from its high in March 2023.

Besides mentioning the benefit the company saw from the spinoff of the uniform solutions business into Vestis , the company's quarterly presentation indicated an outlook of double-digit YoY growth in FY24 when it comes to earnings per share:

{kind=link}

I will call this a strong buy in this category, on the basis of proven double-digit earnings growth so far coupled with double-digit positive earnings projections going forward, indicating sustainability in achieving profits.

Equity Positive Growth

This section explores this company's equity (book value) growth trends over the last year, using data from the balance sheet.

From this data point, we can see more good news about this company. It achieved $3.7B in positive equity in the last quarter, vs $3.03B in Sept 2022, a YoY growth of +22%.

Further, the longer trend between Sept 2022 and Sept 2023 shows an upward trend in equity growth in this entire period, rather than just a one-time event. This metric is one I follow as I believe a fundamental business concept is the importance of a company having positive equity.

One obvious factor that could impact this is debt, and for this company, it saw long-term debt drop to $6.53B vs $7.22B in Sept 2022, a +9.5% YoY decline. In addition, debt has gone down in each quarter since Dec 2022. This is a positive achievement, considering that this is a very capital-intensive industry with high overhead costs to manage such a large logistical operation and understandably the need to make use of debt financing.

At my former campus I mentioned earlier, I recall that Aramark had a few dozen employees working multiple shifts, plus the food and supplies needed to feed hundreds of students each day, and the trucks to bring the supply to the cafeteria. Now, multiply that by a few hundred campuses across America. That is certainly a major supply-chain management challenge, not to mention the effects of inflation on the cost of goods.

In this category, another strong buy rating, on the basis of double-digit growth in book value/equity, declining debt, and what I think is sustainability in this regard going forward.

Share Price vs Moving Average

This section explores the current share price compared to the 200-day simple moving average , to decide if it currently presents a buy, hold, or sell opportunity.

From the YCharts, we can see the share price is hovering around $27.09 as of this article writing, nearly 23% below the 200-day simple moving average (orange trend line shown). Further, it has been trending far below the moving average since its price dip this autumn, and significantly below its July highs.

This is a simplistic way to say that I believe this shows a strong buy opportunity right now, not because of a great dividend yield but rather a cheap share price for an otherwise profitable company with growth in earnings, revenue, and equity, as well as a positive future outlook provided.

Valuation: Price-to-Earnings

This section uses valuation data to explore the forward P/E ratio and whether it presents an undervalued opportunity.

I will be using the GAAP-based forward P/E ratio. It shows a P/E of 22.19, which is +31% above the sector average.

Tying this multiple of 22x earnings back to the financials and share price already mentioned, I think this elevated valuation is not justified because the data shows the share price in bearish territory trading below average while earnings have grown quite a bit, so this valuation ought to be lower in my opinion.

In this category, I will call it a hold for now as it is modestly overvalued.

Valuation: Price-to-Book Value

This section uses valuation data to explore the forward P/B ratio and whether it presents an undervalued opportunity.

This metric shows a GAAP-based forward P/B ratio of 1.55, which is +38% below the sector average.

Tying this back to the financials and share price, I think it is justified because the share price has been cheap while equity/book value has only improved. This is a great combination in my opinion.

I would call it a modest buy at this valuation of 1.5x book value, on the basis of lower-trending share price combined with improving book value. You are getting improved book value at a cheaper share price.

Risk Analysis

This section identifies a key risk to consider about this company and what its probability and impact could be on the business.

A key risk I found was the risk of Aramark's clients ending contracts with them, since there are other vendors that can provide similar services and in an era of high inflation it is understandable that cost-effectiveness is monitored.

For example, a Dec. 8th article in the Waco Tribune-Herald of Texas mentioned that Baylor University is ending its food-services contract with Aramark, instead picking another company:

Baylor University announced Friday it selected Chartwells Higher Education as the university’s new dining services vendor, ending a 68-year partnership with Aramark Dining Services.

In addition to dining, Aramark provides facilities services, including energy and project management, as well as custodial and engineering services for Baylor. According to a message sent last month to university faculty and staff, Baylor is also seeking new vendors for those contracts.

This was not the only case like this in 2023. The Miami University's student news reported in September that their school was also severing the Aramark contract there as well.

While I think these are considerable risks to consider, at the same time think about the fact that this company serves several hundred campuses and is well diversified in terms of contracts. In addition, it serves other types of institutions besides campuses. For example, Shelby County (Tennessee) recently approved a contract for Aramark to provide food service to the county correctional facility, according to a recent article .

Obtaining public-sector contracts for anything is not an instant overnight process but takes a while and goes through multiple channels, so either gaining or losing a major contract can be a huge win or loss to a company and its employees who depend on it.

I would call this stock a "hold" in this category because I think the evidence shows a moderate risk probability and impact on this very large company if a few contracts get lost, however, I think the bigger risk could be from bad PR it could generate and hurt the brand as it continues to try and acquire new accounts.

Quick Summary

To summarize, contrary to the mixed consensus I am going very bullish on this stock today and this is driven by strength in revenue, earnings, and equity growth, combined with a share price trending far below its long-term moving average.

For a dividend-income investor, the yield is nothing exceptional but there has been proven growth over the last decade along with steady payouts. The price-to-book is reasonably undervalued, its forward-looking earnings outlook calls for double-digit growth, and it is a large and well-diversified company with many stable and existing contracts in force that provide regular revenue.

Further, this company helps feed America in more ways than one, whether it is our college students, those incarcerated in institutions, or those in our hospitals, Aramark remains a key factor in ensuring the behind-the-scenes magic takes place to get that plate of food in front of hungry people each day.

For further details see:

Aramark: Bullish As Cheap Share Price Mixes Well In Soup Of Earnings Growth