ARMK - Aramark: Margins Need To Improve Significantly

2023-05-04 16:00:49 ET

Summary

- Margins need to show much better improvement for the company to be considered a good investment.

- The company's financials are also not the best, with very high interest expenses that are barely covered by EBIT.

- I would avoid it for now until the company proves it can sustain higher margins and profitability in the upcoming quarters.

Investment Thesis

With Q2 earnings just around the corner, I wanted to look at Aramark (ARMK) deeper to see if, after the subsequent sell-off, the company is a good investment right now. After investigating deeper into the financials of the company, it doesn't seem to be a good buy at this point and if the company's improvement in efficiency by '25 doesn't succeed, it may not be a good buy for a while.

The Company and Latest Results

Aramark is a food service, facilities, and uniform service provider for many different institutions and events worldwide, including healthcare, leisure, prisons, and education. The company provides managed services like catering, dining, beverages, and plant operations.

For Q2, analysts expect revenues to slow down and bring in $4.39B compared to Q1 of $4.60B

The management announced a sale of non-controlling interest in AIM services to Mitsui & Co., which provides food services in Japan and was established as a joint venture by Aramark and Mitsui, for $535m that should be finalized by H2 of '23. These proceeds will be used to pay down the debt. I would expect to hear more about this situation in the earnings call.

I would also like to see much more margin improvements even if the company is going to bring in less revenue. This would suggest to me that the management is focusing on its efficiency plan that it set out in FY22.

Overall, I like how the company is progressing since the pandemic panic, and if it manages on improving these razor-thin margins that we have seen from them for a while now, that will play a big role in determining the company's fair value in the long run. So, let's see what the company is doing to achieve better efficiency and profitability.

Margin Improvements

The company intends to bring back much better margins by '25, in a range of around 7%-7.5% . Now that sounds good in theory but how likely is it that this is going to be achieved? When the management made these remarks, that was back in November of '22 when inflation was slightly higher than it is right now. One must wonder if their models take into account higher, persistent inflation and interest rates.

So far, from what I saw in the latest quarter, the company is doing something right because operating margins have seen 79bps to 104bps improvements from the same quarter the year before. When I built the financial model of ARMK, I was not very impressed with how it's been operating, with such thin margins, which sometimes brought in negative results due to the company's high debt, which I will talk about in a later section a bit more. I usually don't like companies that operate in such a demanding industry because it is very difficult to model what kind of outcome we can expect in the future, as even the slightest improvements in efficiency and profitability change the company's intrinsic value significantly.

I do believe the company will manage to improve the margins as the world is continuing to return to normal life after the pandemic, especially the international market which has seen very consistent growth already. I would expect the company to return to similar levels of margins it saw in 2018.

Industry Outlook

In terms of the industry outlook, I found a few different estimates which vary quite a bit in CAGR. The global catering services and food contractors market is estimated to grow by 6.28% CAGR . Doesn't look to be particularly high, but it is decent enough. Another article suggests a 4.4% CAGR over the next 10 years, while another suggests a 3.6% CAGR from '22 to '28. We could just take the average of the three to get some sort of an estimate which gives us around a 4.7% average growth rate. The company is guiding a range of 11%-13% in '23, which is quite a bit above the estimates, but the company is one of the bigger players in the industry and I would expect over time the revenue growth to come down to the industry's average.

Financials

I will be focusing on full-year results when showing graphs and other metrics as I believe this represents the company's financial health better than one quarter that might have performed well or not. I will mention some numbers from the latest quarter if I think these are needed for color.

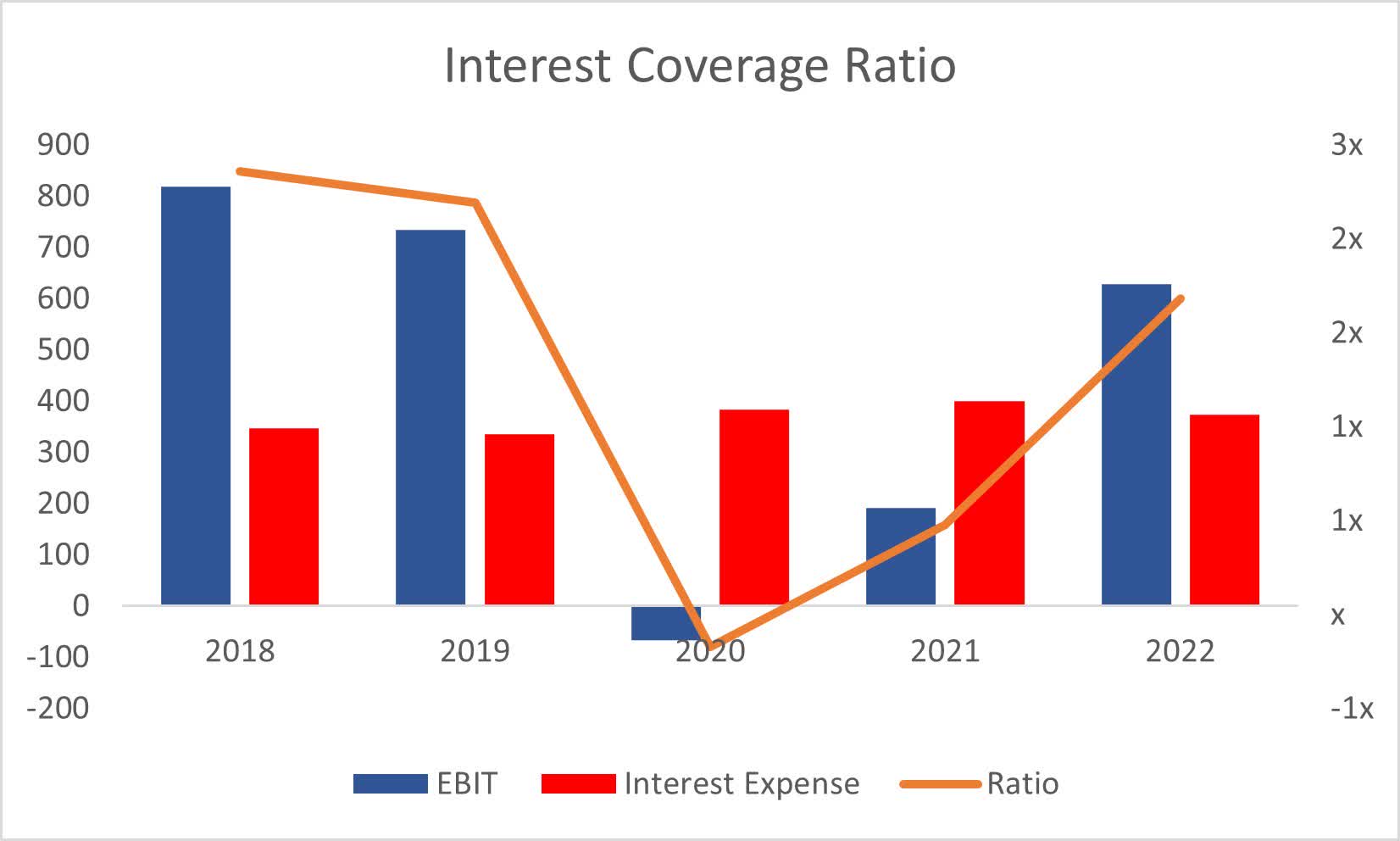

The company had around $300m in cash in FY22 and around the same in the latest Q1 that ended in December '22. The latest long-term debt figure is around $8B, which is very high in my opinion. This number has been elevated for quite a while now and has affected the company's financial performance significantly y-o-y, which saw negative results in '20 and '21 due to very high-interest expenses and low EBIT numbers that resulted in negative earnings. I usually don't mind debt at all; however, the company is overleveraged here in my opinion. The interest coverage ratio is less than 2, which means that any larger fluctuations in EBIT going forward will mean that it will be very hard for the company to cover its annual interest expenses. A good bulk of the debt is due in '25, which will relieve the company of around $4B of debt but they may just get more debt to pay for this debt as their cash reserves are nowhere near to paying off this debt. Cash flow from operations is also nowhere near.

Interest Coverage Ratio (Own Calculations)

{kind=link}

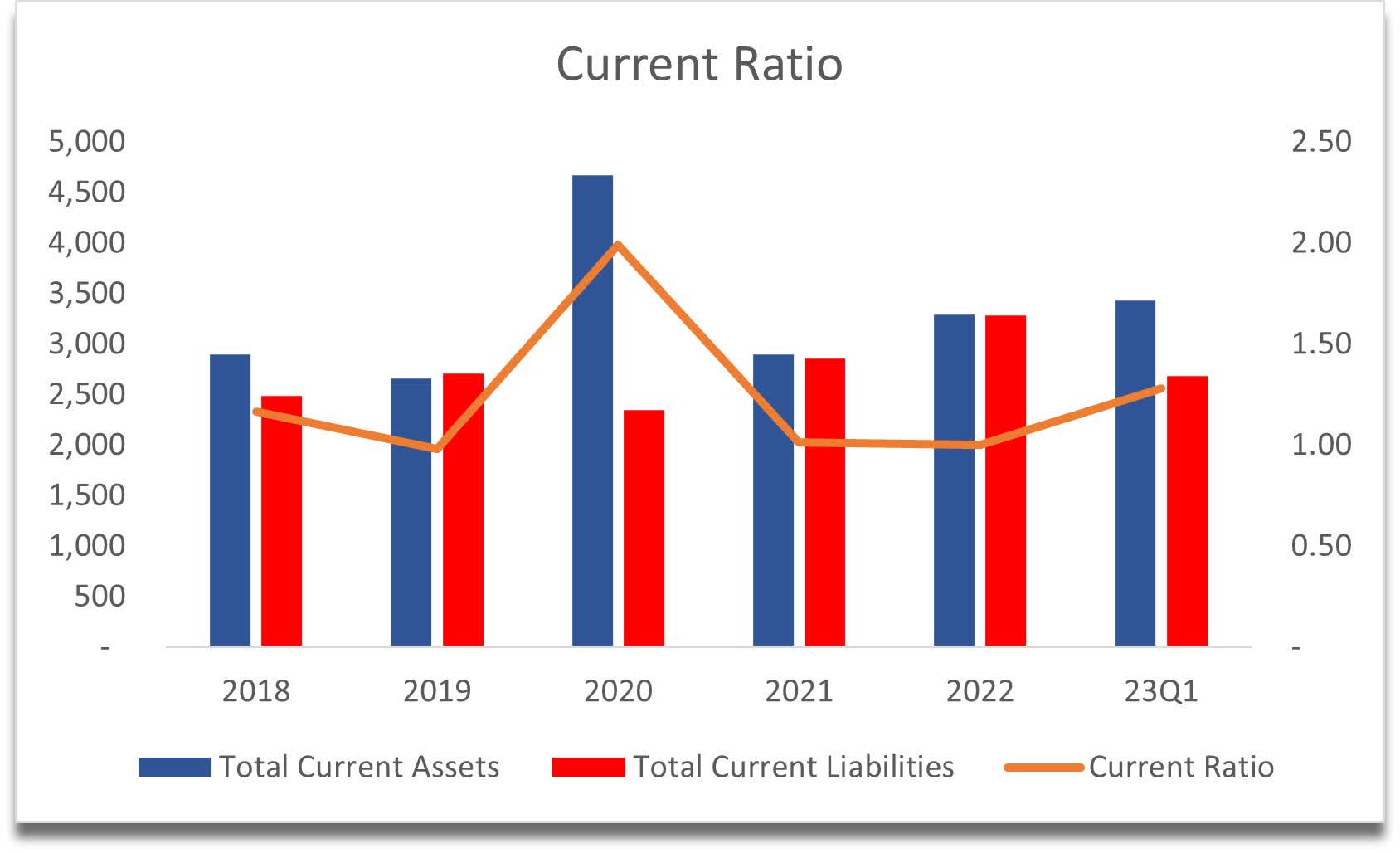

Continuing with liquidity, ARMK's current ratio was just about covering short-term obligations as of FY22 ended in September, but by Dec '22, the ratio improved to around 1.28, which is much better than 3 months before.

Current Ratio (Own Calculations)

{kind=link}

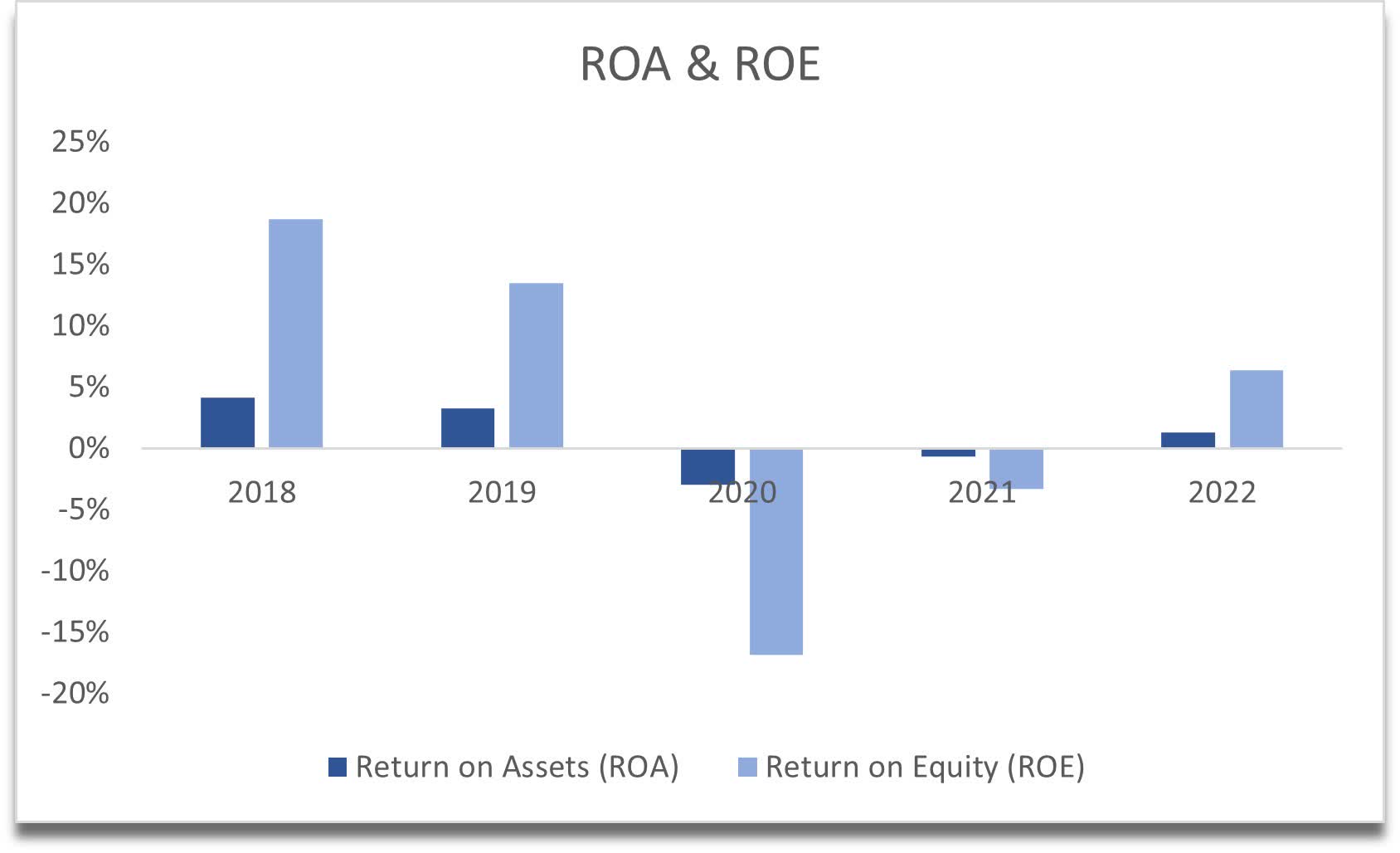

The next metrics that measure profitability and efficiency have left me with much to be desired. ROA and ROE have been very erratic and still very low compared to what the company managed to achieve pre-pandemic. I would like to see much more improvement in these going forward to make the company much more attractive in the long term.

ROA and ROE (Own Calculations)

{kind=link}

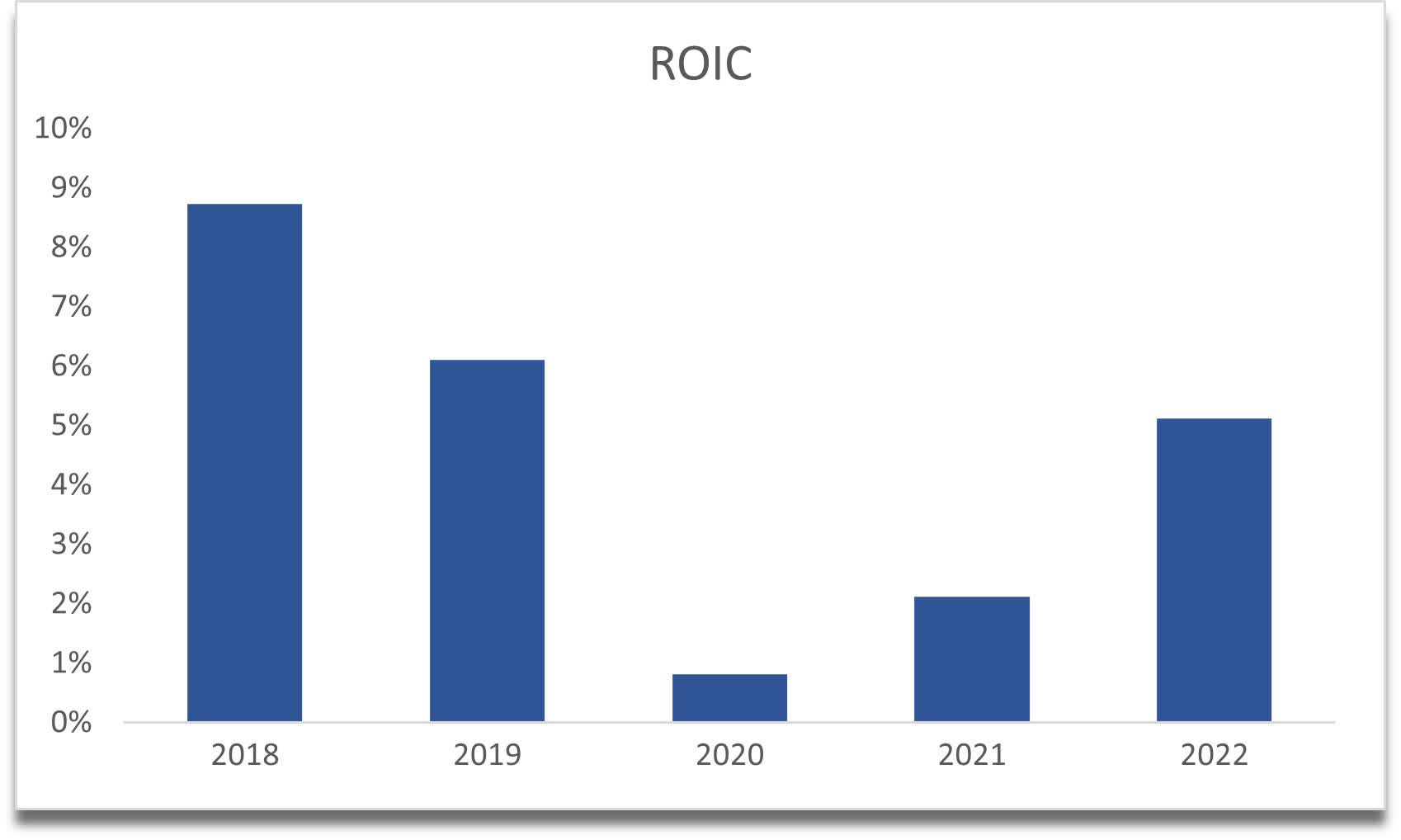

The same applies to ROIC. There are better companies that manage to achieve much higher returns on capital invested. The management is trying to improve this since the pandemic panic; however, I would need to see more improvements before I would consider investing my money. Seems like the company's moat and competitive advantage was erased in '20, but it is slowly coming back.

{kind=link}

To be honest, not a big fan of this sort of balance sheet. It's very erratic and hard to predict with much confidence where it is going to go next, due to the company's industry and very high interest payments on debt. It could keep the trend upward in terms of the above metrics, but if the looming recession will affect the company, then these metrics could go back down again.

Valuation

For the valuation model, I decided to go with a slightly more optimistic outlook in terms of revenues and margins.

For the base case, revenues will not see any declines and will linearly grow down to around 5% by '32 from 15% in '23. This will give me around 10% average annual growth for the model. For the optimistic and conservative cases, I went with 200bps higher and 200bps lower revenue growth respectively which ends up being 12% average for optimistic and 8% for conservative.

In terms of margins, I will improve them by around 400bps linearly by '32. This way EBIT margins improve by around 200bps by '25, slightly below the company's estimates but I would like to be more conservative here.

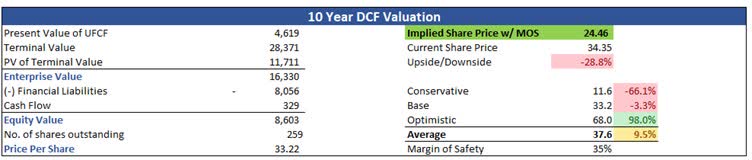

I usually add a 25% margin of safety to companies that have a very healthy balance sheet, but in this case, I will add 35% because I'm just not liking the company's balance sheet all that much in its current state.

With that said, the intrinsic value I assign to the company at this moment is $24.46, which implies a 28.8% downside from the current valuation.

DCF Valuation (Own Calculations)

{kind=link}

Closing Comments

The high-interest expense is going to distort the company's bottom line a lot if we are going to see a meaningful downturn in the economy. The maximum I would pay for the company is what is calculated above; however, I would like it to come back down even further, in case the efficiency and profitability measures aren't achieved as quickly as the management intends. I will set a price alert at around $25 a share and by that time I would expect we will see a couple of more earnings reports out which will give a better look at how the margins have developed and how the company is paying off the debt. I would like to see this prioritized for now.

There are better investments right now in my opinion and I am very patient when it comes to waiting around, especially when there isn't much capital available to throw around and when there's certainly more volatility in the markets ahead.

For further details see:

Aramark: Margins Need To Improve Significantly