ARMK - Aramark - The Investment Finally Pays Off But Future Is More Difficult (Rating Downgrade)

2023-07-26 11:12:16 ET

Summary

- Aramark has delivered solid results for Q2, including 19% revenue growth, a 28% YoY increase in operating income, and a 50% rise in EPS.

- The company is preparing its uniform services segment for a spin-off, strengthening its balance sheet, and monetizing non-core assets to improve its financial position.

- Despite improved results, Aramark's high debt and low credit rating make it a risky investment in my view, but it may still offer an upside based on its valuation and growth rate.

Dear readers/followers,

I've been covering Aramark ( ARMK ) for some time now, almost 2 years. In that time I've been mostly neutral, though I changed my rating to a speculative "BUY" rating in my last article. Because it was speculative, I did not add tens of thousands of shares - but I did add a small position to my account just to have some skin in the game, a few hundred dollars. Now, I wish I'd added more than that.

Seeking Alpha Aramark RoR (Seeking Alpha)

It's impossible to know when a speculative company will see the reversal or upside - or even how long that upside may last. But I of course wish I'd gone deeper when I see more than 2x S&P500 outperformance on the part of this particular investment.

Remember, Aramark is not a bad company. It does things, business, that are very important on several levels. It's most definitely an investable business if things line up "correctly".

So let's see if things still do line up to where we can buy more and expect good returns, or if it might be time to consider rotating already.

Aramark - Plenty to like about undervalued food service - but not fully valued.

Due to significant company issues, I've been hesitant to invest before, at least until my last article, when I saw a bit of a turnaround in company potential and some clarification of the upside.

This is, more or less what we still have at this time. Aramark is a bit of a "special" investment. There's a reason it's speculative, after all. We have a BB rating in credit - so it's junk. We have only a 1% yield, and that one is very unlikely to grow massively based both on company policy and communication.

So what we have is a combination of two unattractive investment traits - low credit with a low yield - where typically junk credit can be expected to have a higher yield. That's also why I'm not especially "sorry" I didn't invest more - it's part of my core strategy to not go overboard in companies like these.

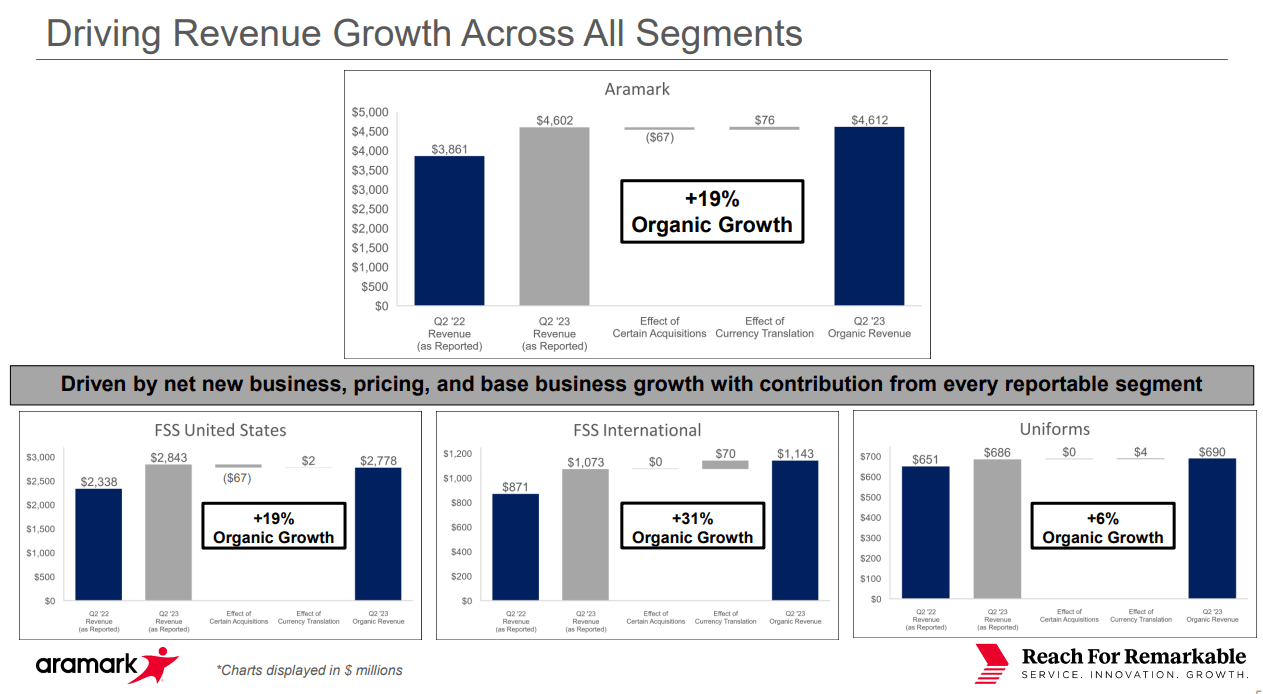

But now to look at current company results. Aramark actually delivered very solid results for the second quarter reported in May - this includes 19% revenue growth, all of which is organic in nature. It also went a long way to contribute to a very impressive 28% YoY increase in Operating income and a margin increase of 40% on the AOI level.

EPS was up by 50%, 38% on the adjusted EPS level, with impressive growth across all segments.

{kind=link}

Things we have been waiting for the company to do are finally materializing. And it's encouraging, the mix of new business and base business growth that's responsible for this increase. This also means that the valuation increase is "logical", and that means that I'm not eager to sell off my position here.

If you recall my last article, the company is preparing its uniform services segment for a spin-off. This new segment will handle workwear, and supply services for restrooms, first aid, floor care, and towels. This means that the new UniCo will compete with an entirely new set of peers, but it also means focusing the core business on what Aramark actually does.

This has come with the impressive strengthening of the company's balance sheet, the downpayment of over half a billion dollars worth of debt since quarter-end, and the April 2023A divestment of 50% of non-controlling interest in AIM services.

The company is busily monetizing assets that are non-core - including a portion of its ownership stake in the San Antonio Spurs NBA franchise. This is done to increase debt downpayment, improve outlooks for strategic refinancing, and really put the company in a better position overall.

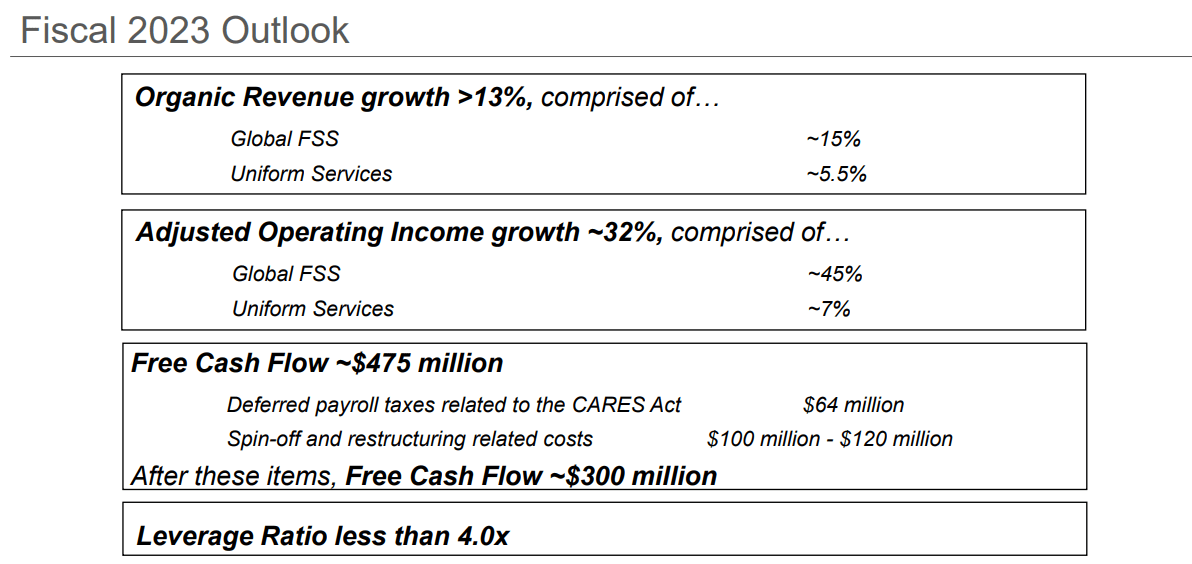

I would argue that things, as they stand, are going very well and that the company, and management, are showing responsibility and acumen. Operating income is growing, and this is in turn confirming the company's current 2023E outlook. Remember, 2023E is the expected "turnaround" year for the company - the first in a long line of hopefully growing results that are set to drive Aramark higher. At least, that is the thesis I currently am looking to work with.

{kind=link}

Also, remember that 2Q and 3Q tend to be lower quarters in terms of AOI cadence. The 4Q quarter tends to be profitable, together with 1Q, due to seasonal activity in both education as well as sports, entertainment, and destination. So I expect the next few quarters to come in stronger, and I now fully expect the company to deliver on a very strong year.

The question I often get to field with Aramark is what it would take for me to allow Aramark, given its degree of market penetration in core services, a higher or any sort of premium in its valuation. Because if this is allowed, the implied fair value for this company shoots through the roof.

And, to be completely honest with you, part of those requirements, are things that Aramark is currently in the process of starting to fulfill and meet. The company is seeing increased margins, profitability, and earnings overall. But for me to allow this, I want it to be a trend, not just a beginning which I would argue is what we're seeing today. COVID-19 was of high impact/influence on this company, and current results are not yet recovered from the pre-COVID-19 results - even though this is currently ongoing.

Aramark was a simple recovery play the last time I wrote about it. It's still that, to some extent, but it's much more of a growth play this time around. Because there's such a high degree of historical uncertainty with that, I think the risk factor is actually increased compared to my last article despite improved results this quarter.

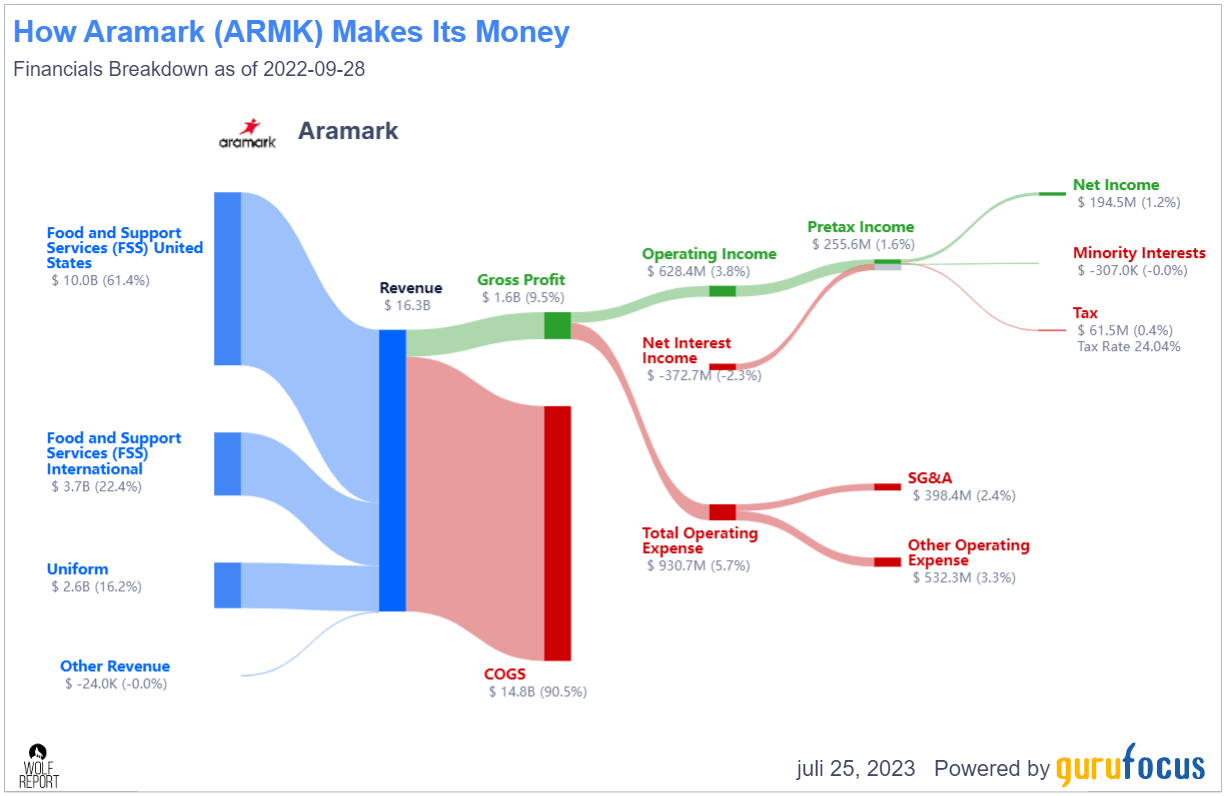

At its foundation, Aramark is not a bad business - it's just that it has margin problems. A sub-10% gross margin is not good, no matter how you slice that. And as of 2022, the company was still highly leveraged. That's going down here, but it's down from a level of debt/equity of 6.6x, and an interest coverage of less than 1.8x.

The company also has one of the highest COGS I've ever seen in a company - really, ever.

{kind=link}

Despite improving its debt situation, the company's debt is still high - and its ROIC net of WACC is still at a negative level - so you might see why I'm somewhat careful with going anywhere "deep" into this investment. The simple fact is that there are many, many safer, higher-yielding, and better-rated investments out there.

This does not make Aramark an objectively bad investment - it just requires a bit of context, and for you to be clear about what to expect.

For instance, I recently wrote about Societe Generale ( OTCPK:SCGLY ) and gave the company a "BUY", detailing almost a 150% total RoR in 3 years with a near-7% yield.

If you ask me which of these two investments I would choose to allocate $1,000 capital to, then my answer without a doubt would be SocGen.

Still, the company's upside and thesis are worth considering based on its valuation, and the fact that it has recently beaten the market - so let's see where the upside currently puts us.

Aramark Valuation

First off, S&P Global analysts do not consider the company all that likely to outperform here. Aramark has risen to a share price of $42.67. Analysts are at a range from $36 to $50, with an average of $44/share. That's 15 analysts, only 4 of which are at a "BUY", with the absolute majority at either a "HOLD" or "Underperform". So the sentiment is that for the time being, Aramark has risen as high as it can.

I would not agree with this necessarily. Depending on where you estimate the company to be on a forward basis, there is still an upside to the company based on the growth rate.

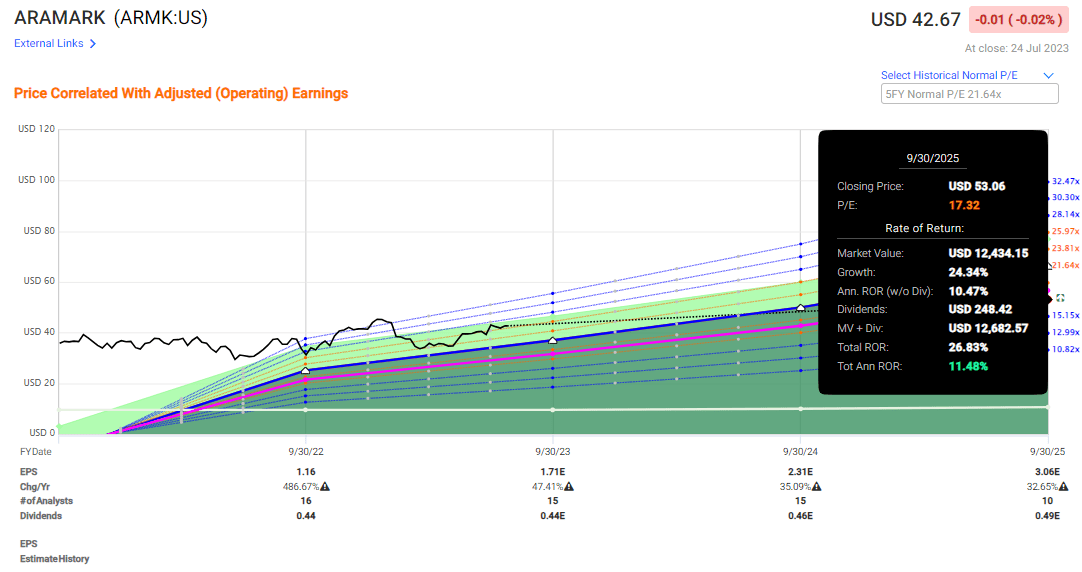

ARMK is slated to grow at around 30-40% per year in the next few years on average. That is a massive growth rate - and if it materializes, and even if you just estimate the company at say, a 17-19x P/E, which would be conservative for that sort of growth rate, you're still able to get double-digit RoR based on very conservative estimates - 17.3x here below.

{kind=link}

I hesitate to call any company with BB-rating "safe", but this is a relatively safe-considered upside. And at 21x P/E, it's an upside of almost 23.23% annually, or over 57% RoR until 2025E, which is a great RoR. But this is where I started to see some of the problems when seeing things contextually, or compared to other investments. As I said, alternative investments I look at have triple-digit upsides that are both reversal and dividend. Aramark has neither reversal nor dividend - at least not much. It's mostly growth here.

In my last article, I made a case for why the "base" assumption of a 15x P/E was still the right way to go. I now believe we can forecast at 17-19x P/E, which does allow for 10-20% RoR annually.

The problem is that rate of return is no longer as appealing as it once was when we have quality companies still trading "down" significantly, showing us upsides that are based on the holy trifecta of valuation that I am looking for - namely:

- Significant undervaluation.

- Significant projected growth

- Significant dividend yield.

If you can find all three of these , and can comfortably and with high conviction go into such an investment, then you're "golden".

And it's my firm stance that despite the difficult market we're in, there are companies that offer exactly this, to one degree or another.

Aramark is not uninvestable. The management's tone in recent earnings calls and communication is very positive. I also won't argue that the future is positive, and while I may argue that some of the specifics of the numbers may be calculated on the high side, I do think that Aramark is bound for even more EPS and margin improvements, which will go a long way towards improving what you may expect here.

However, the thesis still isn't simple - and because of that, I give you my current thesis on Aramark - and it's actually a thesis change based on the high valuation and my PT relative to the risk here.

Thesis

My thesis for Aramark is as follows:

- The company is a theoretically attractive business with an eye for food service, uniforms, and various sorts of services for organizations that are attractive to customers (education, sports, corrections, etc.). However, the company is hampered by poor fundamentals and a surprisingly deep reputation for food quality negligence and labor law violations that need to be seriously considered prior to investing.

- At the right valuation, this company can deliver you an upside of no less than 15-20% annually, and even more attractive ones. I believe that this is currently not an impossibility.

- Updated for 2023 and July/August, I now consider Aramark to be a "HOLD" at this time, and I go no higher than $35/share in my price target. I have once again bumped this target though, to reflect the somewhat higher upside. However, this is as high as I'll currently go.

Remember, I'm all about:

-

Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them.

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

For further details see:

Aramark - The Investment Finally Pays Off, But Future Is More Difficult (Rating Downgrade)