ARMK - Aramark: The Upside Is Finally Here Though Speculative

2023-05-04 04:57:27 ET

Summary

- Aramark is a play I have looked at a few times in the past, only to come to the conclusion of "Hold" for the company due to an unfavorable risk profile.

- As of this article, I am changing my stance on the company. I'm now calling it a "speculative BUY". The company doesn't have great fundamentals, but it has potential.

- Let's review what Aramark might give you if you were to invest here.

Dear readers/followers,

Aramark ( ARMK ) is a qualitative food service/restaurant business if your definition of "qualitative" includes a number of serious scandals in recent memory. I've actually been through some of these in my past articles on the company when I established my basic thesis for the business.

In fact, my previous stances have all turned out to be remarkably correct and profitable. I rated the company a "HOLD", and told prospective investors to consider staying away. My latest article easily shows how correct, at least until today, such a stance was.

Seeking Alpha Aramark RoR (Seeking Alpha)

What I've wanted for Aramark since started to cover it is a better price. My target the last time I covered it was $34. That's pretty much where we are now.

Of course, we've also seen marked market deterioration since then, which has in part made the company contextually less appealing - but I also set my initial price target pretty low - so I'm going to shift it a bit here.

Let's review recent results and see where we are as we end up giving the company a "BUY".

Aramark - An update and a review

I've looked at Aramark plenty of times before, always calling the company a "HOLD" owing to its issues and somewhat lacking fundamentals. However, any qualitative, profitable business has an upside and a price where that upside becomes appealing or realistic enough. So does Aramark.

We've finally reached that point.

Aramark has some of the worst gross margins in the entire business service field. On a gross basis, the company doesn't even manage double digit, for 2022 coming in at 9.55%, with an OM of 4.05% and a net of 1.03%. That's worse than every conservative FMCG/consumer defensive stock I invest in, and this is the primary challenge for this particular business that we need to overcome through a cheap entry.

Other than that, it's not actually that bad. Sure, debt is high - 2.71x to equity is some of the worst in the field, and 6.94x to EBITDA is also not good. But the company does have a solid Piotroski-F score, measuring things like RoA, CFROA, Leverage, current ratios, asset turnover, and so forth - indicating at least some level of safety.

However, you can't take away that a quick glance at the company's revenue to net income flow, it has every sign of being an ineffective, if still profitable business.

Aramark Revenue - Net (GuruFocus)

{kind=link}

Illustrations such as these are valuable to determine where the bottlenecks and company issues might be.

The company isn't bad in much of what it does, or in the latest results. Revenue is up 18% organically for 1Q23, and operating income is up 42%, with margins increasing over 70 bps on an OM level - which means we're up over 4% compared to what you see above. EPS is, consequently, also up, by around 65%. The company also disclosed a sale of its non-controlling interest in AIM services in order to address what can only be called the elephant in the room - the company's elevated level of debt. The company's portfolio is, as I've mentioned in my initial articles, quite attractive. Aramark covers the spectrum of food services.

{kind=link}

If you "only" view what the company does and what exposures it has, it should technically be a very attractive business. However, the company is dragged down by its high debt and volatility. Fundamentals give us a credit rating of BB-. That's deep in junk territory, with an LT debt/cap of 71.6%. The dividend, while well-covered even from conservative levels of earnings, is only 1.29%, which is well below the norm in this segment.

What we want to see from Aramark to allow for a higher premium is very easy - we want margin and earnings expansion. For 1Q23 and 2Q23, that's what we've started to see, and that's also what the forecasts are calling for. COVID-19 was of high impact/influence on this company, and current results are not yet recovered from the pre-COVID-19 results. Remember that Aramark is a very seasonal business- most of its cash flow tends to come towards the 4Q period, while 2Q and 3Q tend to be relatively weak, and 1Q tends to be the weakest of all.

The exciting part about investing in Aramark is that you're coming in on the ground floor in the coming spin-off/transaction which is splitting Aramark into Aramark, and Uniform services - and this is on track to occur in 2H23.

{kind=link}

When accounting for the sale of AIM services, which was announced in February of this year, the cash proceeds should somewhat improve the company's debt situation, while being accretive to EPS on an annual basis. The 50% JV stake in the AIM services contributed no more than $30M on a pre-COVID-19 basis to the company, with a similar weighting as the company's other segments, meaning towards the end of the year.

Aramark is a simple recovery play. The fundamentals, meaning its contracts and services, are sound - its performance of turning the top line into profit is not, unfortunately. That's what we're waiting to improve, and when it does, Aramark will be worth substantially more than it is today.

The current company forecast calls for organic top-line growth of up to 13%, with around half a billion in FCF before deferred payroll related to CARES, net of which we should be at around $350M for the full year. Accounting for the AIM transaction, the company expects Operating income growth of up to 37% for the year, with leverage down to around 4x by the end of fiscal 2023.

This is a solid improvement compared to what we've seen previously, and this combined with the double-digit decline we've seen since my last article, is what forms the basis of a positive thesis from here on out for Aramark.

Aramark has historically been a company that, over the past 10 years, has had a really hard time making profitable ROIC. Its investments have been poor compared to its cost of capital, and this is part of why the stock has been punished. Its revenue/net hasn't been all that appealing, and the bullish thesis is that this coming set of transactions should optimize the company for growth and finally reward shareholders with not only earnings but an incentive for the share price to move up.

I believe that at this price, we're starting to see the potential for that to occur. After accounting for all the transactions planned this year, I do believe the possibility is there for increasing the share price and seeing growth.

So, moving onto Aramark valuation.

Aramark Valuation - It's starting to look attractive here, even if speculative

Aramark has been punished quite a bit. While we're not at a multi-decade trough price, we're at an attractive price relative to the expected earnings growth as we move forward.

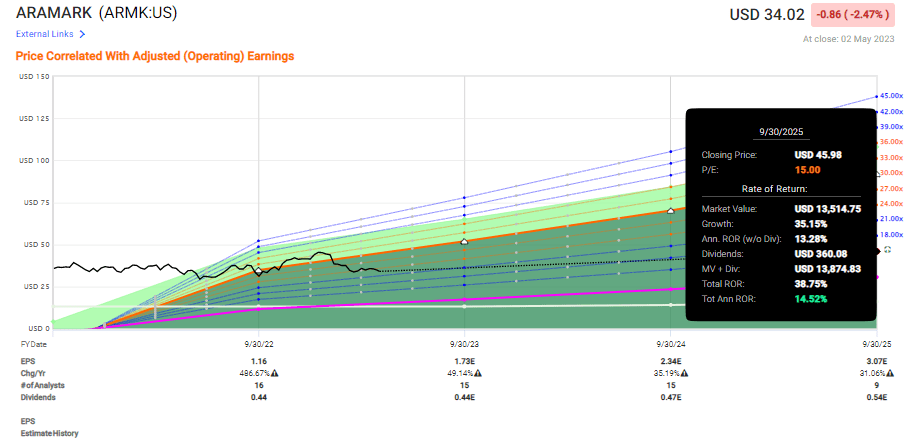

At this point, Aramark is expected to see EPS recovery rates of 30% per year until 2025E. The company has a 10-year premium of around 20x P/E, which means that forecasting it at 15-20x P/E is somewhat realistic here.

Well, even on a 15x P/E on a forward basis, the RoR here is now almost 15% per year.

Aramark Upside (F.A.S.T graphs)

{kind=link}

And if you assume that 20-21x P/E premium holds, that's double that upside, at 31.4% per year. That's how it works when you catch a company on the upswing of an earnings improvement. I personally wouldn't count on that 30% or that 20x P/E - it's a bit high - but I would say that fairly speaking, the downside in this investment is starting to look less and less likely to be significant or worrying to any significant degree.

I've previously had difficulties reconciling the company's reputation and flows with a premium, which is why I've been hesitant to allow for a premium in the forward-looking share price - and that's also why I continue to forecast at a "base" case of 15x P/E. That is why, by extension, the rating I've had for Aramark in the past has always been a "HOLD". That 15x P/E really requires that $34/share or slightly above to make the numbers work.

And as a value investor, the numbers have to work out.

There is already so much the math that when we look at Aramark, looks worse than we might want to. The company really is below average in profitability and fundamentals, at least for the time being. Generally speaking, and for many of you reading this, that might be a dealbreaker. Me, I just discount it at a higher and higher level the worse things get, until I finally call a business "uninvestable" in the current circumstances.

Aramark is not uninvestable. The management's tone in recent earnings calls and communication is very positive. I also won't argue that the future is positive, and while I may argue that some of the specifics of the numbers may be calculated on the high side, I do think that Aramark is bound for some improvement in EPS. We've already seen this begin, and I believe we're bound to see it continue going forward.

That doesn't make this current thesis simple. Remember, we're in a market situation where many things are actually quite cheap. Many quality companies are on sale, and with the recent crash we saw yesterday in the finance sector, my money is actually flowing into finance at this time, not Aramark or similar companies.

In my recent article, I raised my target to $34/share from $28. I'm now giving it a final bump for the time being, and moving it to $35/share, allowing for some of this outperformance at a somewhat higher multiple. That means that for the time being, Aramark is actually a "BUY" at the time I'm writing and submitting this piece.

Thesis

My thesis for Aramark is as follows:

- The company is a theoretically attractive business with an eye for food service, uniforms, and various sorts of services for organizations that are attractive to customers (education, sports, corrections, etc.). However, the company is hampered by poor fundamentals and a surprisingly deep reputation for food quality negligence and labor law violations that need to be seriously considered prior to investing.

- At the right valuation, this company can deliver you an upside of no less than 15-20% annually, and even more attractive ones. But this requires you to take a substantial risk at this time, which is not present in more qualitative investments.

- Updated for 2023 and April/May, I now consider Aramark to be a "BUY" at this time, and I go no higher than $35/share in my price target. I have once again bumped this target though, to reflect the somewhat higher upside. However, this is as high as I'll currently go.

Remember, I'm all about :

-

Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them.

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Aramark is neither cheap nor the best - but it's a speculative "BUY" with a potential of making 15-30% RoR per year, which comes close to double digits. I'm not invested in the company yet, but I may buy a small position, because I don't believe we're going much lower than this.

For further details see:

Aramark: The Upside Is Finally Here, Though Speculative