ABR - Arbor Realty Trust: An Eventful 2023 But Still A Buy

2024-01-03 14:35:46 ET

Summary

- Arbor Realty Trust has seen significant fluctuations in its share price in 2023, but the impact of short reports on the company has been limited.

- The company is expected to report an increase in net income and distributable earnings compared to 2022, indicating a strong performance.

- Arbor Realty Trust has a commendable track record of consistently increasing its dividends and has a low dividend payout ratio, making it an attractive investment.

Introduction

To say 2023 has been an eventful year for Arbor Realty Trust ( ABR ) would be an understatement. The company saw significant fluctuations in its share price over the year, from a low of just over $10/share to a high of close to $18/share. This was in no small part due to the short reports on the company issued in March and November 2023. These reports have been discussed on Seeking Alpha ad nauseum, both by authors and readers alike, hence I will not delve into them. Suffice to say, the impact of these reports have been fairly limited, with the company’s share price rebounding swiftly in the days following the reports, and ultimately returning to and even surpassing pre-report levels.

I have written about Arbor Realty Trust several times previously, most recently in July 2023 following the release of its Q2 2023 results . Each time, I have had a “Buy” rating on the company. While the company’s Q4 2023 results will not be announced for another month at least (the company has typically announced its results in the middle of February), now is as good a time as any to look at the company’s performance over the past year and determine if it remains a good investment heading into 2024.

2023 Performance

In the company’s latest earnings release , for Q3 2023, the company reported a net income of $0.41/share and distributable earnings of $0.55/share. When considering the cumulative figures for the year, this translates to a net income of $1.28/share and distributable earnings of $1.74/share.

On its own, these figures mean nothing. However, they gain significance when placed in context. Notably, they represent an 8.5% increase in net income and a 6.75% increase in distributable earnings compared to the same period in the previous year. With a net income of $1.67/share and distributable earnings of $2.23/share for the whole of 2022, the company only needs $0.39/share in net income and $0.49/share in distributable earnings for Q4 2023 to match 2022’s performance. Given that the company has surpassed this in the past couple of years, it would not be a stretch to say the company will likely exceed its 2022 results.

Dividend

Arbor Realty Trust has a commendable track record of consistently increasing its dividends, and 2023 was no exception. There were 2 dividend hikes during the year - the first hike was a notable 5%, which increased its dividends from $0.40/share to $0.42/share in the initial half of the year, while the second hike was an increase of slightly over 2%, bringing the company’s quarterly dividends to $0.43/share.

Examining the broader timeline, in the 16 quarters since 2020, the company has increased its dividends by an impressive 43%, from $0.30/share in Q1 2020 to the current dividend of $0.43/share. This includes an impressive streak of 10 consecutive quarters of dividend increases, during a period where many REITs either reduced or halted their dividends.

The current share price of $15.01 gives the company a very attractive forward dividend yield of 11.44%. What makes this yield even more attractive is that the company has consistently maintained a conservative dividend payout ratio, which is one of the lowest, if not the lowest, in the industry. This low dividend payout ratio is reflective of the company’s ability to sustain its dividends.

The company had a dividend payout ratio of 78% for Q3 2023. Looking at the year as a whole, the distributable earnings for the first 3 quarters alone, totaling $1.74/share, is sufficient to fully cover the projected dividends of $1.68/share for the entire year, with a surplus left over. Assuming the company only barely meets its 2022 performance, this would give it a dividend payout ratio of approximately 75%, further underscoring the company’s capacity to sustain and potentially increase its dividends.

Nevertheless, it is essential for potential investors to recognize the conservative approach of the management. Despite the frequent dividend increases, management has actually been prudent with its dividend increases, and it was stated as such during the most recent earnings call :

And we certainly could have raised our dividend again this quarter based on a substantial cushion and continue to show earnings, the Board decided to keep it flat since we believe we are not getting credit for raising it in this environment and will be more prudent to preserve a large cushion as we head into the most challenging part of the cycle.

While management could have certainly opted for another increase to the dividends for the fourth quarter, the decision to keep its dividends flat was motivated by a strategic assessment of the current market environment, with management opting to build up a buffer in these uncertain times.

Risks

Despite the company’s commendable performance in recent quarters, management has adopted a cautionary tone regarding potential challenges ahead. During the quarter, the company increased its CECL (Current Expected Credit Losses) reserves by an additional $15 million during the quarter, making it a total of approximately $70 million in CECL reserves added over the first 3 quarters of the year. Additionally, the company saw the emergence of $98 million in new delinquent loans during Q3 2023, though it also saw the successful resolution of a $70 million delinquent loan from the previous quarter.

During the Q&A session of the earnings call, management acknowledged the possibility of more delinquencies in the coming quarters, stating:

“We've been pleasantly surprised the last few quarters, as Ivan said, we're expecting continued stress. And we think over the next 2 quarters, we'll continue to have those conversations with borrowers, but during the quarter, we only had one material modification, which we disclosed, which was that $70 million loan I mentioned in my commentary. That was a defaulted loan last quarter that we were able to restructure and get to a performing loan. That was the only material modification we had in the quarter. So as a percentage, that's a pretty low percentage. And we've been fairly fortunate that those numbers have been quite low over the last few quarters.”

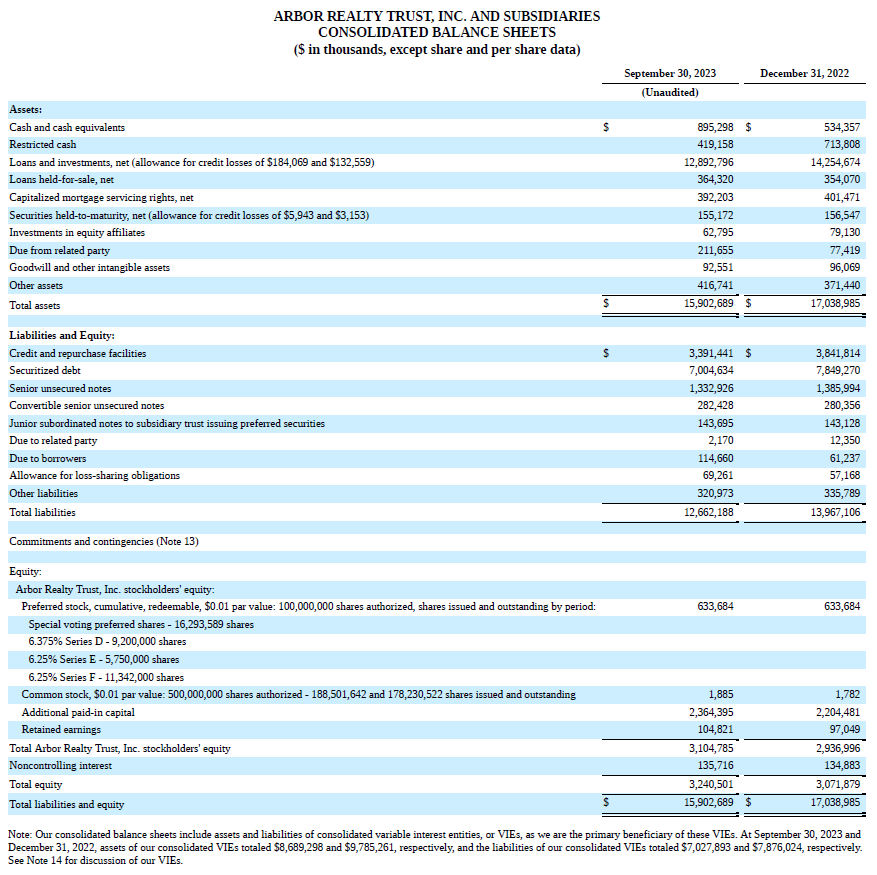

Nevertheless, the company is well-prepared to meet these challenges. Notably, the company has significantly bolstered its cash position, increasing from approximately $534 million at the close of 2022 to nearly $900 million as at Q3 2023. This substantial increase of close to 70% provides a considerable buffer for the company to safeguard its financial stability and navigate potential challenges and uncertainties in the market.

{kind=link}

Conclusion

Since I last covered the company, Arbor Realty Trust has seen a 12.41% decline in its share price. Even after factoring in dividends, this translates to a loss of 7.20%. In contrast, the S&P 500 has shown an increase of 3.45% over the same period. Despite these market movements, my belief in the company’s robust fundamentals remains, and I maintain my “Buy” rating.

There are a couple of other indicators to support this. Firstly, the company recently announced an increase in its share repurchase program, allowing for the potential buyback of up to $150 million worth of shares . This move signals management’s belief that the company’s shares are undervalued in the current market context. Next, and perhaps most importantly, is the actions of the company’s leadership. Both CEO Ivan Kaufman and CFO Paul Elenio have been purchasing additional shares of the company, a move which speaks to their conviction in the company in my view. In particular, they purchased these shares after the short reports on the company, a sign that they saw the dip in share price as a buying opportunity.

Seeking Alpha

The above, coupled with the company’s resilient financial performance throughout the years, leads me to maintain my “Buy” rating on the company heading into 2024. Of course, the high dividend yield doesn't hurt either.

For further details see:

Arbor Realty Trust: An Eventful 2023, But Still A Buy