BXMT - Arbor Realty Trust: An Underappreciated Dividend Contender That's Great For Long-Term Investors

2024-01-06 07:00:00 ET

Summary

- Arbor Realty Trust has faced short attacks and headwinds, but insiders have continued to buy the stock, signaling upside potential.

- The company has a well-covered dividend and a track record of dividend raises, making it an attractive option for income investors.

- Arbor Realty Trust is preparing for turbulence ahead and has built up liquidity, positioning itself for future growth and strong financial performance.

- Both revenue and earnings are expected to drop by the end of this year, but grow by the end of 2025.

Introduction

It seems like every time I turn around, Arbor Realty Trust (ABR) is facing some sort of headwinds. The biggest headwind always seems to be short attacks, which affects the stock price. I last covered ABR back in August. In that article, I discussed the strong financial growth over time and the significant insider buying the mREIT had experienced, which you can read here .

Since that article, ABR's share price has retracted nearly 8% to $14.71 at the time of writing. But despite the short attacks and challenging environment, the REIT has continued to show its financial resilience, posting a strong Q3 back in late October. In this article, I discuss why Arbor Realty Trust remains a buy for dividend investors.

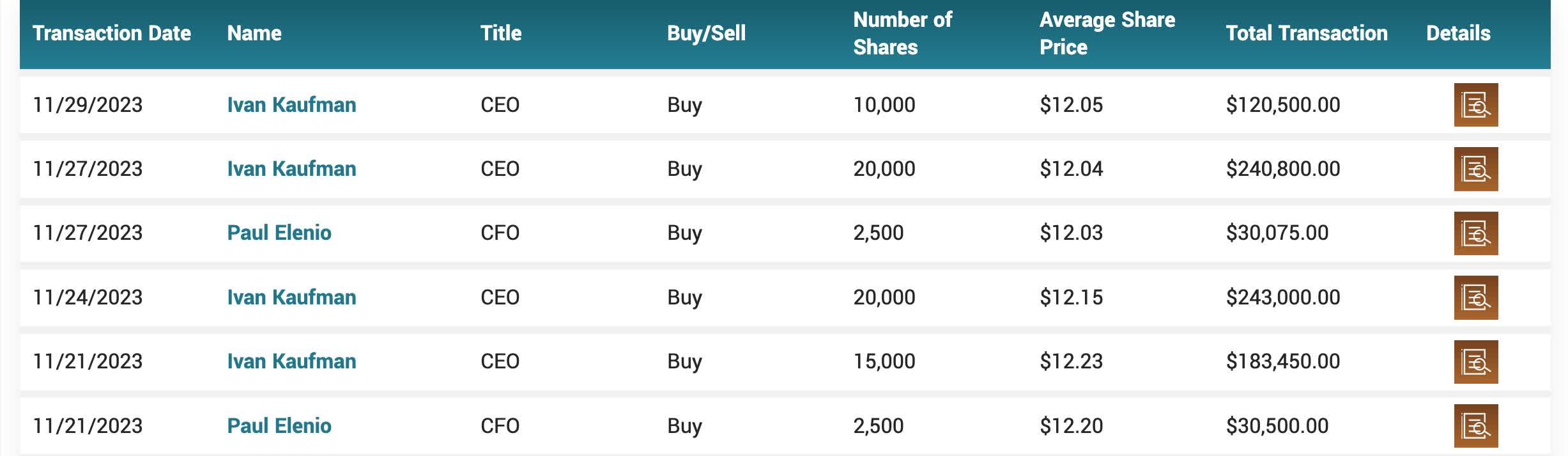

Further Insider Buying Signals Upside Potential

Despite the attacks upon Arbor Realty Trust, insiders have continued to pile into the stock over the last few months. In the words of Peter Lynch:

Insiders might sell their shares for any number of reasons, but they buy them for only one: they think the price will rise.

In my opinion, ABR is the best mREIT in the sector. And this is likely one reason why the stock has experienced a lot of insider buying lately. Cambridge Investment Research Advisors also purchased more than 14,000 shares. BlackRock ( BLK ) also increased its holdings by 55.6% back in the second quarter.

{kind=link}

In the past 12 months , ABR has experienced more than $544 million of institutional inflows, compared to just $77.7 million outflows over the same period. So, in lieu of the attacks and headwinds, investors are buying this stock. This speaks volumes to not only ABR's quality, but that they are a great long-term investment.

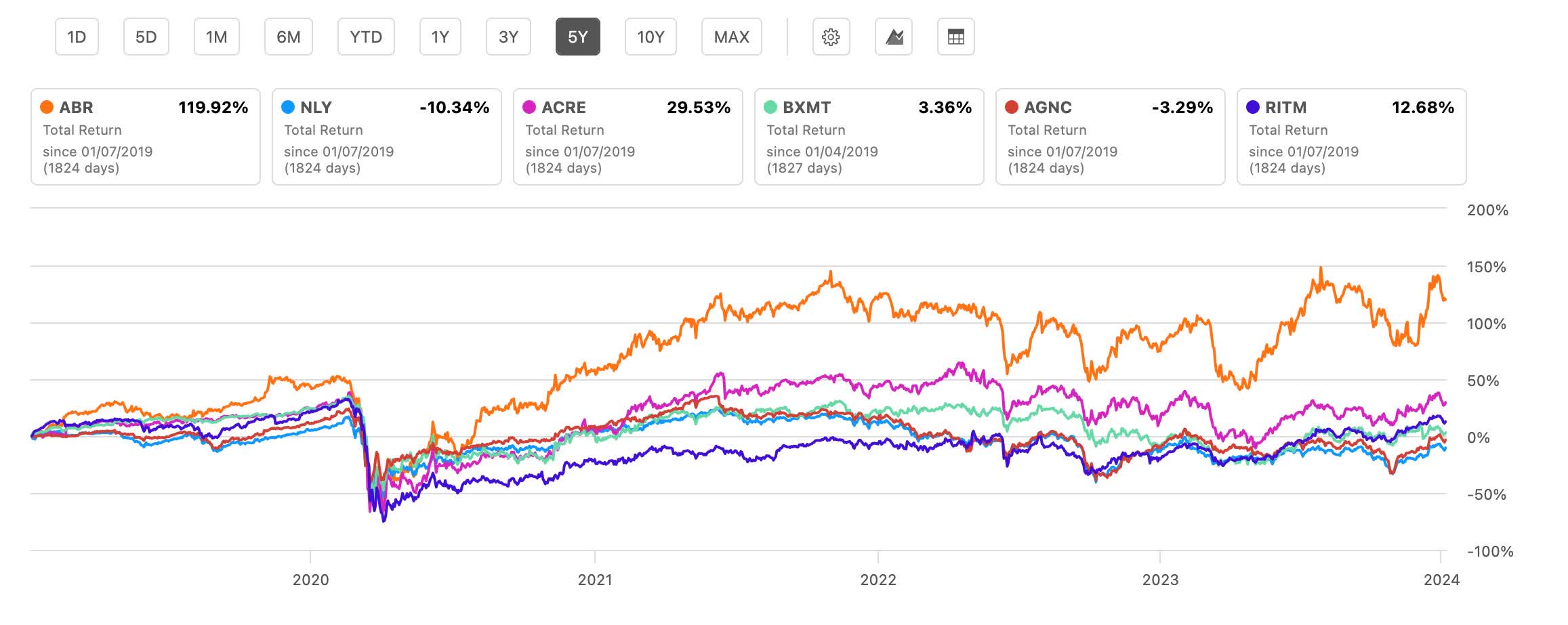

Furthermore, Arbor has superior total & price returns against some of their popular, and larger peers over a stretched period of time. In the chart below, you can see ABR significantly outperforms its peers when it comes to total returns. All have negative total returns over the past 5 years, with the exception of Blackstone Mortgage Trust ( BXMT ) and Rithm Capital Corp. ( RITM ).

{kind=link}

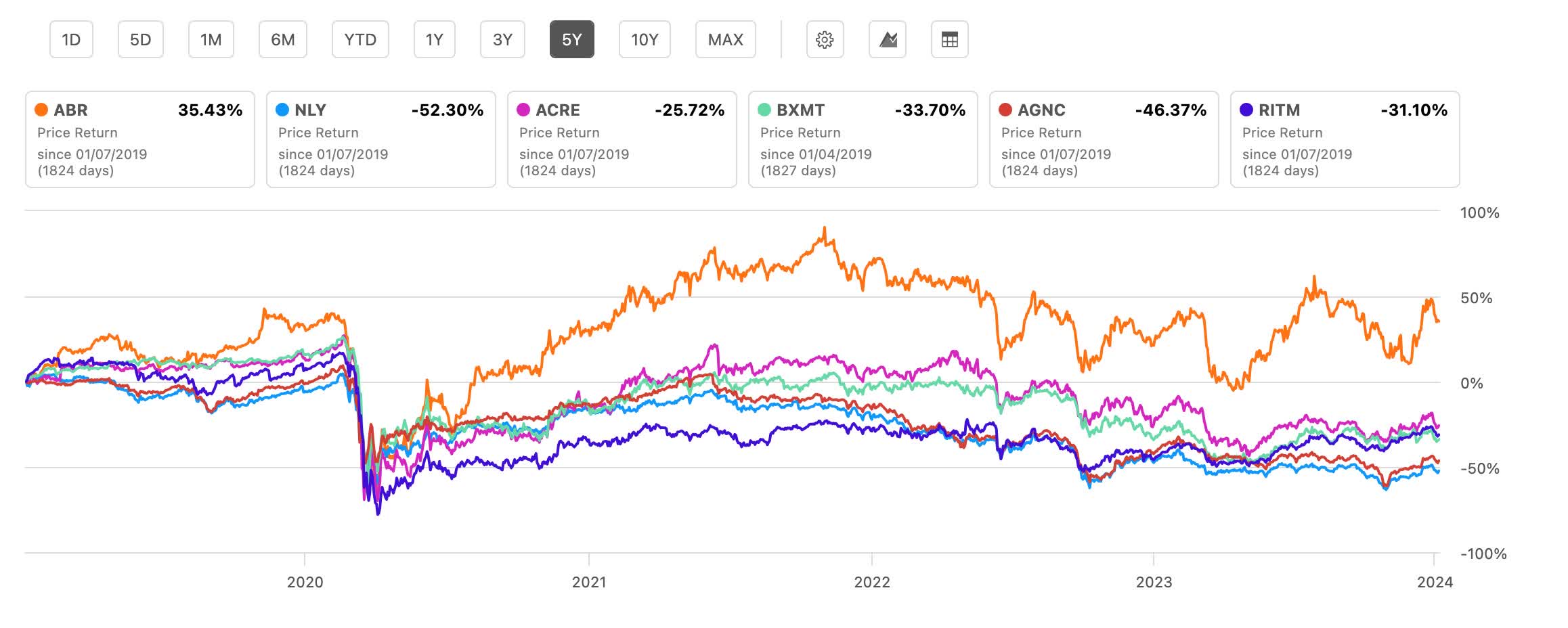

Here you can see they also outperform in price return as well over the past 5 years, being the only mREIT in the green.

{kind=link}

Unappreciated Dividend Contender

With a current dividend of $0.43 and a safe payout ratio of 78%, ABR has one best covered dividends in the sector. And with more than 10 years of dividend raises, their track record is impressive. Peer Blackstone Mortgage Trust ((BXMT)) is close with 9 years of dividend increases.

During the Q3 earnings, ABR's distributable earnings per share of $0.55 beat the consensus by $0.10, so you can see they comfortably out-earned their dividend by a sizable margin. In the last 3 years, the company has raised the dividend more than 40%, growing from $0.30 to the current $0.43.

During their earnings call, their CEO stated the following:

The dividend policy that we implemented with our Board of keeping such a wide disparity between our earnings and dividend has provided us with a large cushion and was very strategic knowing full well we're entering into a market dislocation. And we certainly could have raised our dividend again this quarter based on the substantial cushion and continue to show earnings. But the Board decided to keep it flat since we believe we are not getting credit for raising it in this environment.

Management also stated other reasons for not raising the dividend, which I'll discuss later in the article.

Something else ABR has been doing is decreasing its share count, which will drive earnings growth over time. The company recently announced an increase to $150 million in buybacks, and if the share price continues to decline whether it be from short attacks or the challenging environment, I expect management to repurchase a substantial amount of shares over the coming months. According to their 10-K , ABR had 183.3 million shares outstanding, and I expect this to decline over the coming months.

Growth Outlook

One reason for the management not raising the dividend and preferring to have extra income was that they expect additional stress ahead the next 2 or 3 quarters, mainly because of the high interest rate environment. To prepare for this, the mREIT has been building up liquidity and preserving cash, and ended the quarter with nearly $1 billion (in cash). This is up from roughly $500 million at the end of 2022.

This allows them the financial flexibility to navigate what lies ahead for the business. Furthermore, they recently launched their first construction lending business. This is expected to generate 10% to 12% unlevered returns on capital, and that they project to eventually leverage the business and produce mid-to-high teen returns.

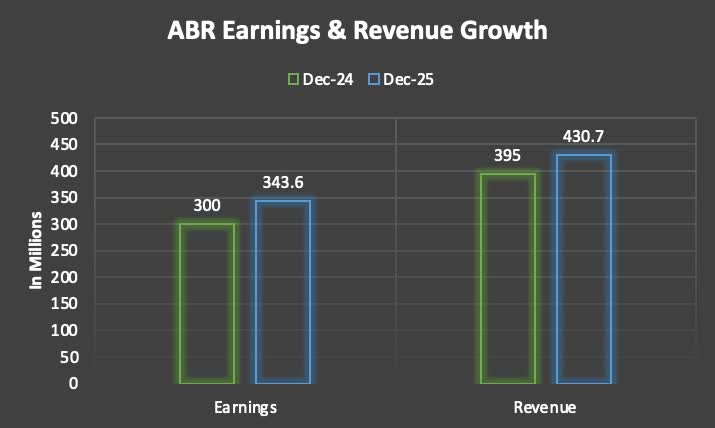

Both revenue & earnings are expected to drop by the end of this year, but are expected to pick up by end of year 2025. Revenue is expected to drop to roughly $395 million and earnings is expected to drop to roughly $300 million. But looking out until the end of 2024, both are expected to post growth of 14.5% and 9% respectively. In my opinion, I think interest rate tailwinds will provide some share price appreciation sometime in the second half of the year.

{kind=link}

Risk Factors

Despite the strong quarters significantly out-earning the dividend and the recent share repurchase program, ABR has faced challenges and these are expected to continue. During Q3 , they recorded an additional $15 million in CECL reserves on their balance sheet loan book which management touched on briefly. They also saw a slight net increase in delinquencies of roughly $28 million, and $98 million of new delinquent loans.

And although the macro environment should ease sometime in the coming months, management is preparing for a rough couple of quarters by boosting its liquidity. Judging by the latest earnings call, there's a high likelihood there could more defaults over the next few quarters. But seeing how rates are expected to decline significantly this year, the company looks poised for a strong 2025. Furthermore, I think they are well-prepared to navigate the rough seas by boosting their liquidity and electing to keep the dividend flat at $0.43 instead of paying out extra income with a raise.

Valuation

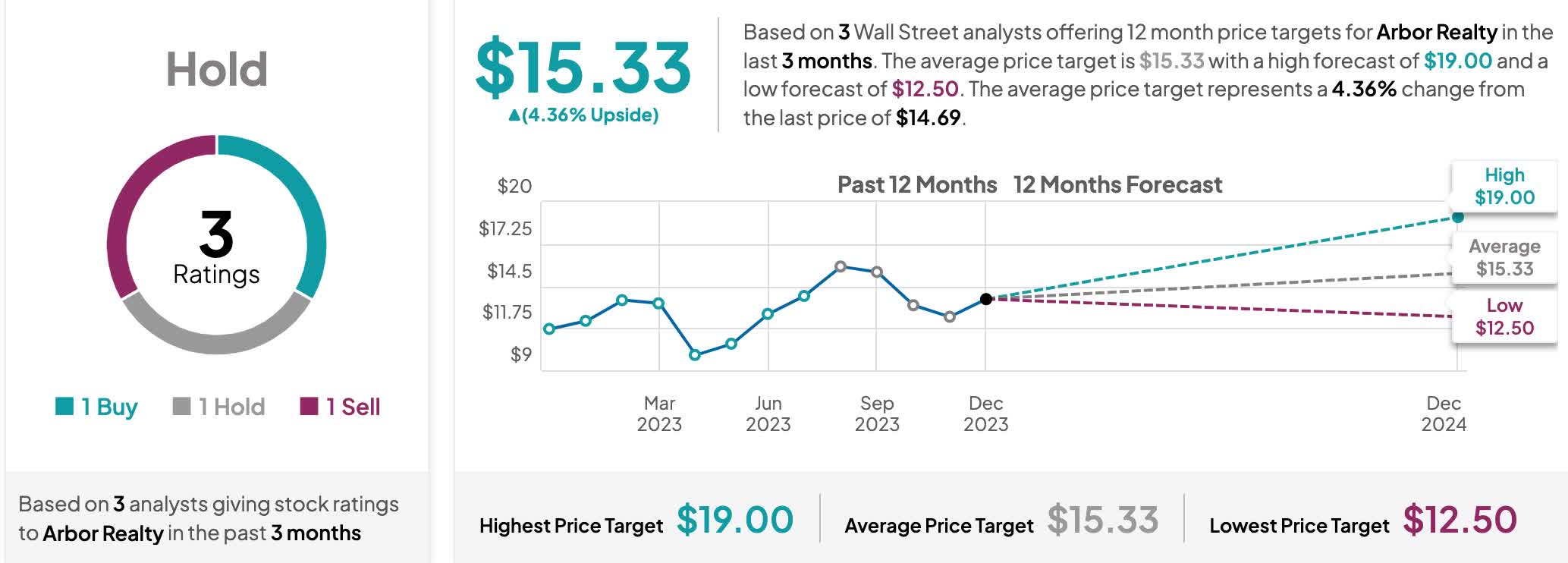

Currently, the stock trades at 1.15x above their book value of $12.73. Since my last article, the share price has dropped roughly $1 dollar and down nearly $3 from July '23. And seeing by the amount of insider buys in the past few months, I think Arbor Realty Trust still offers some upside, especially for long-term investors to their high price target of $19. If you can stomach the short-term pain the stock may experience, then ABR is a buy. If you want a better margin of safety, I suggest waiting for a pullback in price. And if the turbulence management expects comes to fruition, investors may get a chance of a better price entry.

{kind=link}

Bottom Line

As a buy-and-hold investor, ABR has everything you can ask for as an income investor. Well-covered dividend, commendable streak of dividend raises, and strong financials. Their management teams also seems experienced and proactive instead of reactive to unexpected or expected turbulence. This is something as a shareholder you want to see from a management team.

Additionally, the stock has experienced a large number of institutional inflows in the last 12 months and insider buying, signaling the stock has the potential for some upside. Furthermore, because of their strong liquidity position, multi-family centric portfolio, and experienced management team, I think the mREIT will navigate any rough waters ahead. Despite the perceived challenges the company faced and could face in the coming quarters, I think Arbor Realty Trust is the best amongst its peers and remains a buy.

For further details see:

Arbor Realty Trust: An Underappreciated Dividend Contender That's Great For Long-Term Investors