ABR - Arbor Realty Trust: Asset Quality Controls Persist At This 14% Yielder

2023-11-29 22:34:17 ET

Summary

- Arbor Realty Trust has continued to grow its book value per share while its peers have seen declines.

- Concerns have been raised about the rise in non-performing loans at ABR, which has offset gains from increased interest rates.

- The stock is currently trading at a discount to book value, reflecting concerns over defaults and increased volatility.

- In my view, the stock is trading around fair value given the heightened risks.

Arbor Realty Trust ( ABR ) is quite a unique stock in the mortgage real estate investment trust (mREIT) space. While its peers have witnessed substantial declines in book value per share amidst rising rates and increased mark-to-market losses, Arbor Realty Trust has continued to grow its book value per share. Nevertheless, management has repeatedly indicated that the mREIT is facing an increasingly challenging operating environment and considers that the most challenging times within the current credit cycle are up ahead in the next few quarters.

The portfolio and non-performing loans

In recent months several analysts and market participants have raised serious concerns about defaults at ABR. Indeed, the rise in non-performing loans has been mentioned multiple times in the most recent earnings call with management noting that while there has been a rise in earnings from increased yields on interest-bearing assets the gains from these higher rates have largely been offset by a rise in non-performing loans.

In an article published in The Real Deal , Isabella Farr notes that Arbor specializes in short-term, variable-interest loans, commonly referred to as "bridge" loans, which serve as a temporary financing solution before transitioning to more permanent options. The company's strategy involves bundling these loans into collateralized loan obligations (CLOs), which are then sold to investors. This has traditionally been a very profitable business for ABR.

However, she correctly observes that with the recent increase in interest rates, Arbor has found itself exposed to challenges as some borrowers struggle to repay these loans. A case in point is Gajavelli's firm, which defaulted on a $229 million loan provided by Arbor for Applesway earlier this year. Consequently, Arbor had to foreclose on four apartment complexes in April.

In August this year, Seeking Alpha analyst ADS Analytics also cautioned that investors would need to pay close attention to the rise in non-performing loans at the mREIT. At the time non-performing loans had risen from $3 million to $124 million over the course of just two quarters. Since then the mREIT has added some further non-performing loans with management noting that:

So we added actually six new nonperforming loans during the quarter for a total of about $98 million in total UPB. So they range anywhere from $10 million to $30 million of the assets, and then we resolved the $70 million asset that I took Rick through on the change in the terms. So the net change was $28 million during the quarter. The assets are not particularly different than the type of assets we've done. They're all multifamily, all bridge, they're throughout the country and the LTVs on these assets range anywhere from high 60s to 90s and then one we have 100, because we took a reserve against it of $1.5 million. But really nothing different than the type of assets we've had in the past."

The continued increase in non-performing loans certainly merits close attention. However, the total non-performing loans of just over $157 million is still a relatively small percentage of the mREITs overall portfolio representing just over 1% of its overall portfolio. Nevertheless, more concerning is the nearly $468 million worth of multifamily loans currently rated as substandard in terms of the mREITs internal risk rating. Management assigns a substandard rating to a loan where it anticipates that the loan may require some modification. While this does not suggest that the loan would necessarily become a non-performing loan, it certainly indicates a heightened risk in the investment.

Investors in ABR should closely monitor migration between different risk categories in addition to monitoring the non-performing loans. In my view, management has been signaling the rise in non-performing loans well in advance and has taken active measures to address the risks. Nevertheless, the rise in loan losses is likely to contribute to increased volatility in the stock even if the underlying business remains strong.

The dividend and its safety

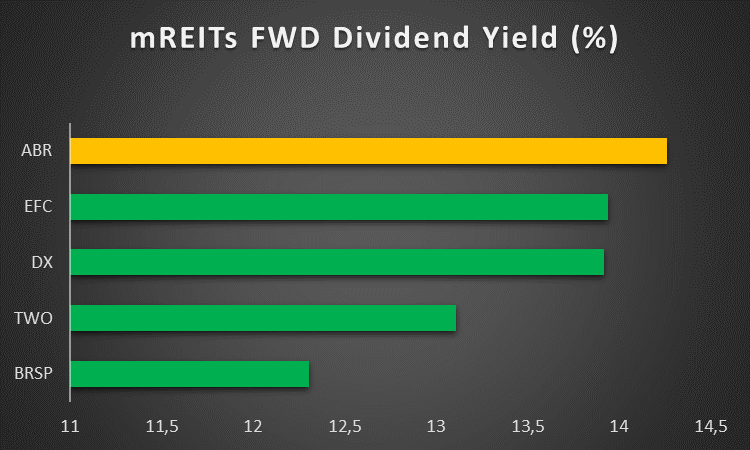

ABR is currently trading at a forward dividend yield of 14.26% which is the highest of the mREITs considered in the peer comp charts below. This dividend is also well-covered by distributable earnings with the mREIT reporting distributable earnings of $0.55 per share which is well above its $0.43 per share quarterly dividend. This presents a distributable earnings dividend coverage ratio of 127.9%.

{kind=link}

ABR also has a solid history of increasing the dividend per share. Nevertheless, further dividend increases have likely been placed on hold as management continues to position the mREIT more defensively amidst a challenging credit environment. This was reflected in the earnings call with management noting that:

The dividend policy that we have implemented with our Board of keeping such a wide disparity between our earnings and dividend has provided us with a large cushion and was very strategic knowing full well that we're entering to a market dislocation. And we certainly could have raised our dividend again this quarter based on a substantial cushion and continue to show earnings, the Board decided to keep it flat since we believe we are not getting credit for raising it in this environment and will be more prudent to preserve a large cushion as we head into the most challenging part of the cycle."

Importantly, despite the increase in non-performing loans and loan loss provisioning the mREIT's distributable earnings have continued to grow albeit at a slower pace. Nevertheless, the increased loan loss provisioning in quarters ahead could potentially have a negative impact on distributable earnings per share. In my view, this is a material risk but is not likely to result in a dividend cut given the substantial buffer between distributable earnings and the dividend that ABR has maintained.

Valuation

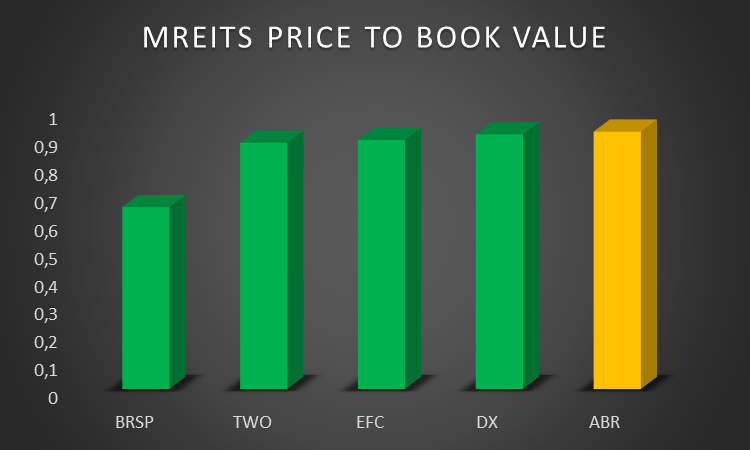

ABR is currently trading at a price to book value of around 0.92 representing a discount to book value of around 8%. Traditionally ABR rarely trades at a discount to book value given that it is one of the few mREITs with a consistent track record of growing its book value per share.

{kind=link}

As seen in the chart below, ABR is the only mREIT in the peer comp chart that has seen its book value per share grow over the past three years. Nevertheless, the recent discount is likely to be driven in part by concerns over increased defaults. This is not unreasonable given that management has continuously warned about the more challenging times ahead which could also see greater volatility in the share price. In my view, the stock is trading around fair value given these heightened risks.

Conclusion

Arbor Realty Trust stands out as a distinctive stock in the mREIT sector. While many of its counterparts have experienced significant declines in book value per share amid rising interest rates and increased mark-to-market losses, ABR has consistently grown its book value per share. However, management acknowledges the increasingly challenging operating environment and anticipates the most difficult times within the current credit cycle in the upcoming quarters.

The concerns about defaults at ABR have been echoed by analysts and market participants. The rise in non-performing loans, highlighted in recent earnings calls, has offset gains from increased yields on interest-bearing assets, particularly as interest rates have risen. While the total of non-performing loans represents just over 1% of the overall portfolio, the nearly $468 million worth of multifamily loans rated as substandard raises concerns about potential modifications, signaling heightened investment risk.

Investors in ABR are advised to closely monitor changes in risk categories, alongside non-performing loans. Management's proactive measures to address these risks have been evident, but the anticipated rise in loan losses may contribute to increased stock volatility, even if the core business remains robust.

ABR's valuation at a price-to-book value of around 0.92 represents a discount of approximately 8%. Traditionally trading at a premium due to a consistent track record of growing book value per share, the current discount reflects concerns over increased defaults and heightened market volatility. In my view, these concerns justify a discount and led me to conclude that the stock is trading around fair value with a very attractive yield for patient investors willing to wait out the heightened volatility that could arise at this stage of the credit cycle.

For further details see:

Arbor Realty Trust: Asset Quality Controls Persist At This 14% Yielder