ABR - Arbor Realty Trust: High-King Of mREITs

2023-12-02 01:06:33 ET

Summary

- Arbor Realty Trust is a well-run mREIT that offers a reliable stream of income and potential for growth.

- The company faced challenges during the 2008 Financial Crisis but rebounded and increased its dividend each year in the past decade.

- Despite negative research reports and short attacks, Arbor has continued to pay and increase its dividend while leading its industry.

Arbor Realty Trust (ABR), as an mREIT, primarily does its business by giving loans in the real estate space. As a sector, mREITs have been among the most hated of investments by the market, and it's not a surprise. Most mREITs are not well-run, with shoddy processes of origination that lead to defaults and, of course, dividend cuts. A REIT without a dividend is like a burger with no patty. Even those who manage to maintain a dividend do not grow it.

Arbor is different. Despite seeing its share price tumble with the rest of the mREIT sector in recent years and being the target of not one but two short attacks by "research reports," I will make the case that Arbor Realty Trust is a BUY for investors who want not only a reliable stream of income but even potential for growth on top of it.

History

Origins

Arbor was founded in 1983, initially as a lender for the sale of single-family homes, by Ivan Kaufman, who still leads the company to this day. Over the years it evolved. In 2003, they began their entry into the multifamily rental market and became a public company in 2004.

2008 Financial Crisis (2008 - 2012)

The company was severely impacted by the 2008 Financial Crisis. While their loans were not bad enough that they went out of business like many other lenders in that time, the devastation in financial markets hurt their earnings from a mixture of defaults and lack of available capital for new originations. They went from paying an annual dividend per share of $2.10 in 2008 to paying none at all until 2012.

{kind=link}

From there, it was a slow rise, and while Kaufman did not lose his business, he would implement the lessons he learned as he improved Arbor's business model.

Rebound (2013 - 2019)

In the years that followed the crisis, Arbor built its business back up. It focused more squarely on bridge loans for multifamily rentals and shifted into a portfolio that mainly utilizes floating-rate loans, with their own debt typically being fixed-rate.

Arbor's agency origination platform (Arbor.com)

{kind=link}

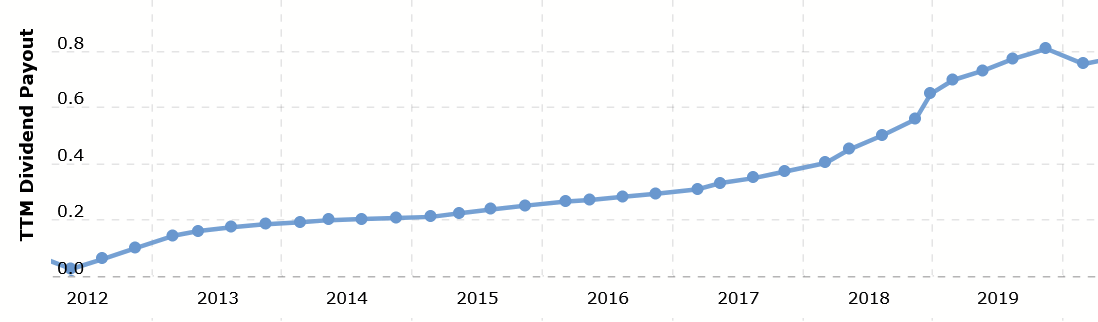

Crucial in its reforms, as holders of ABR should be concerned, is the acquisition it made of its manager and, with it, its Agency Origination platform. This occurred in 2016 and paved the way for stabler cash flows from the servicing fees this segment generates. By the end of the decade, ABR's dividend had returned and been increased each year.

{kind=link}

Recent Years (2020 - Present)

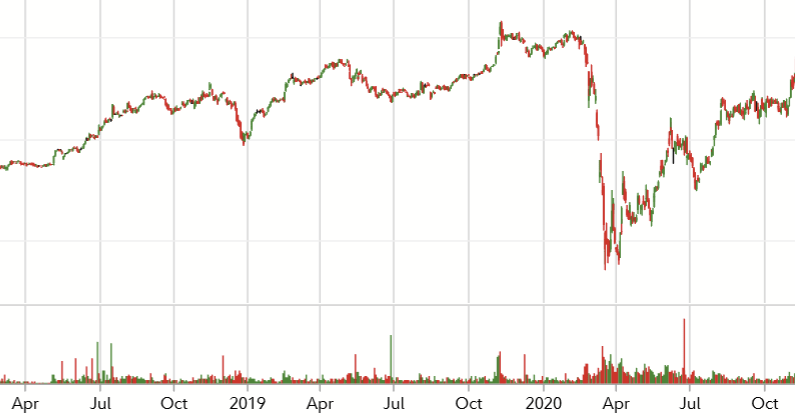

After a decade of reforms (both within Arbor and financial markets), the company would finally face stress tests, starting in 2020 with the arrival of the COVID-19 pandemic and the associated lockdown and recession. Shares of ABR plunged below $5 per share that March.

{kind=link}

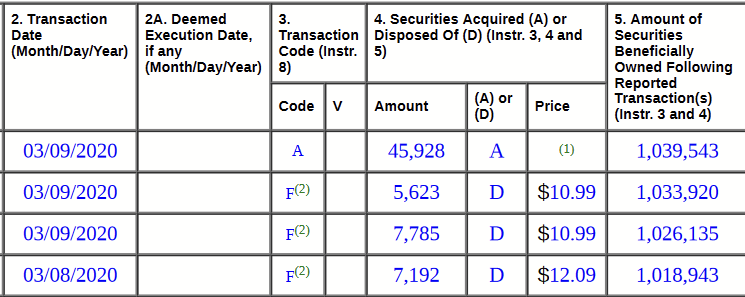

Yet, the company continued to pay its dividend and increased it in Q3 that year. Where many other mREITs and lenders faced massive defaults and dividend cuts, Arbor delivered the opposite. In spite of the uncertainty, this page of their SEC filings showed that management gobbled up the declining shares through individual purchases, well before they even hit the bottom. Kaufman himself put hundreds of thousands of his own dollars into ABR, despite uncertainty at that time if the government would intervene.

Kaufman's Form 4 (Arbor.com, SEC Filings)

{kind=link}

Of course, the government intervened, COVID restrictions gradually lessened, and 2021 was an easier year for businesses. More stress tests came in 2022, amid the Russian invasion of Ukraine and significant hiking of interest rates by for the first time since the Great Recession.

Arbor continued to enjoy strong earnings for that year, along with dividend increases. As Paul Elenio, the CFO, explained in the Q4 2022 earnings call :

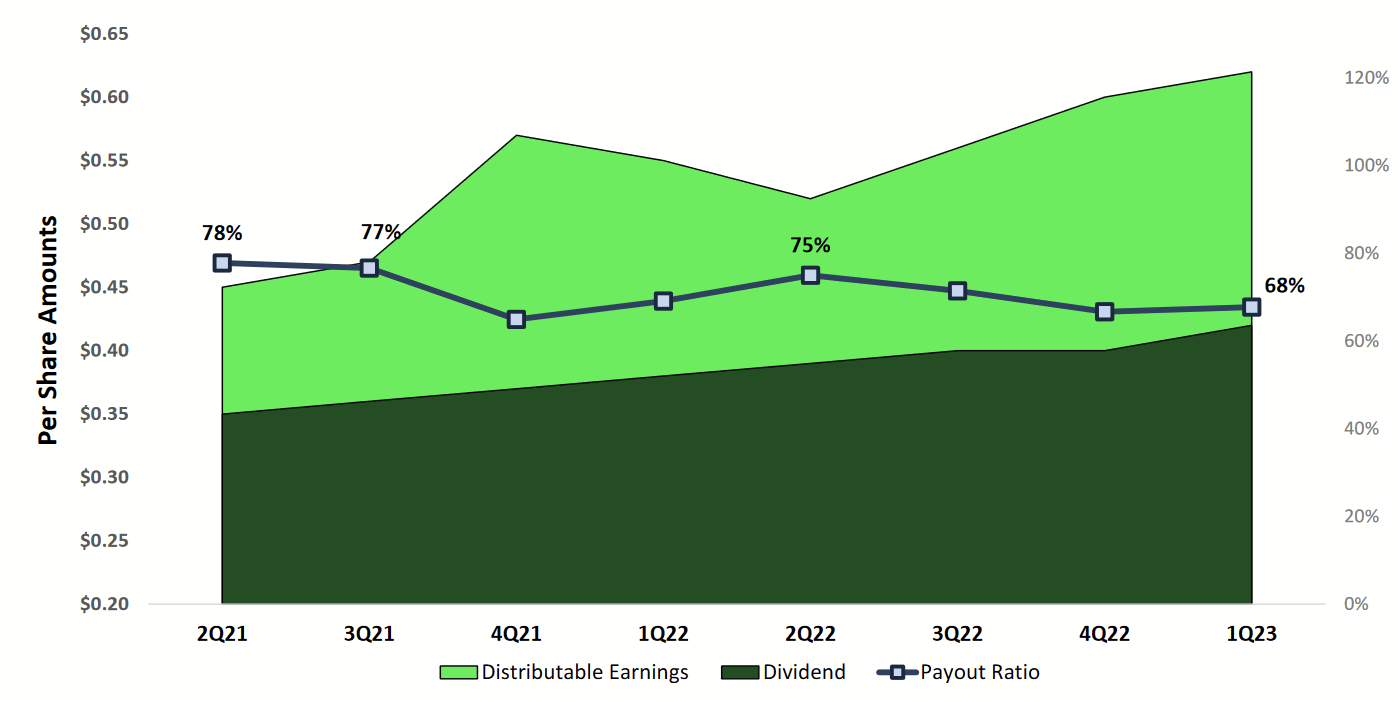

We also had a record year with distributable earnings of $2.23 per share in 2022, an 11% increase overall 2021 results. These results translated into industry high ROEs of approximately 18% in 2022, allowing us to increase our dividend 3 times to an annual run rate of $1.60 a share, reflecting a dividend to earnings ratio of around 67% for the fourth quarter and 70% for the full year 2022. Our fourth quarter results beat our third quarter numbers and our internal projections, largely due to substantially more net interest income on our floating rate loan book and higher earnings on our escrow balances , due to the increase in interest rates.

2023 would see Arbor become the target of negative research reports. The first one, by Ningi (which was timed with the ongoing Silicon Valley Bank crisis that had already deterred the stock market), came out in March, arguing:

We are short Arbor Realty Trust, Inc. (ABR), because, in our opinion, Arbor hid its toxic mobile homes portfolio to manipulate its stock price and avoid insolvency, $599 million of Arbor's escrows evaporated overnight, the company's escrow balances and revenue are fake, in an Archegos-like situation $2.5 billion of repo facilities are subject to margin call provisions, Arbor's funding through repo desks is drying up, the CECL allowances and provisions have been severely understated to boost earnings, Arbor's financial statements for the last twelve years cannot be trusted, and auditors, as well as the board, turned a blind eye on misstatements and misconduct.

Share prices shot down again, this time under $11. The company quickly disputed the claims and backed their own with a $50m share repurchase program three days later, with which it bought $37m worth (share buybacks being uncommon for an mREIT).

Another short attack, this time by Viceroy, came out in November. They claimed:

In this industry plagued with delusion and bad decisions, Arbor stands out as the worst of the worst. Viceroy's dive into Arbor's CLOs suggest its entire loan book is distressed and underlying collateral is vastly overstated. These loans do not qualify for refinancing anywhere, and substantially all mature within the next 18 months.

Arbor declined to respond. The share price fell again below $13, but another Form 4 filed days after the attack show, once again, that Kaufman was more than happy to take advantage of the lower price, personally purchasing over $400K worth of shares.

Operations

While mREITs are primarily defined by their real estate loan portfolio, Arbor's has more subtlety to it than that, and we need to understand this to see why it stands out and has a healthy dividend, even if other mREITs don't.

{kind=link}

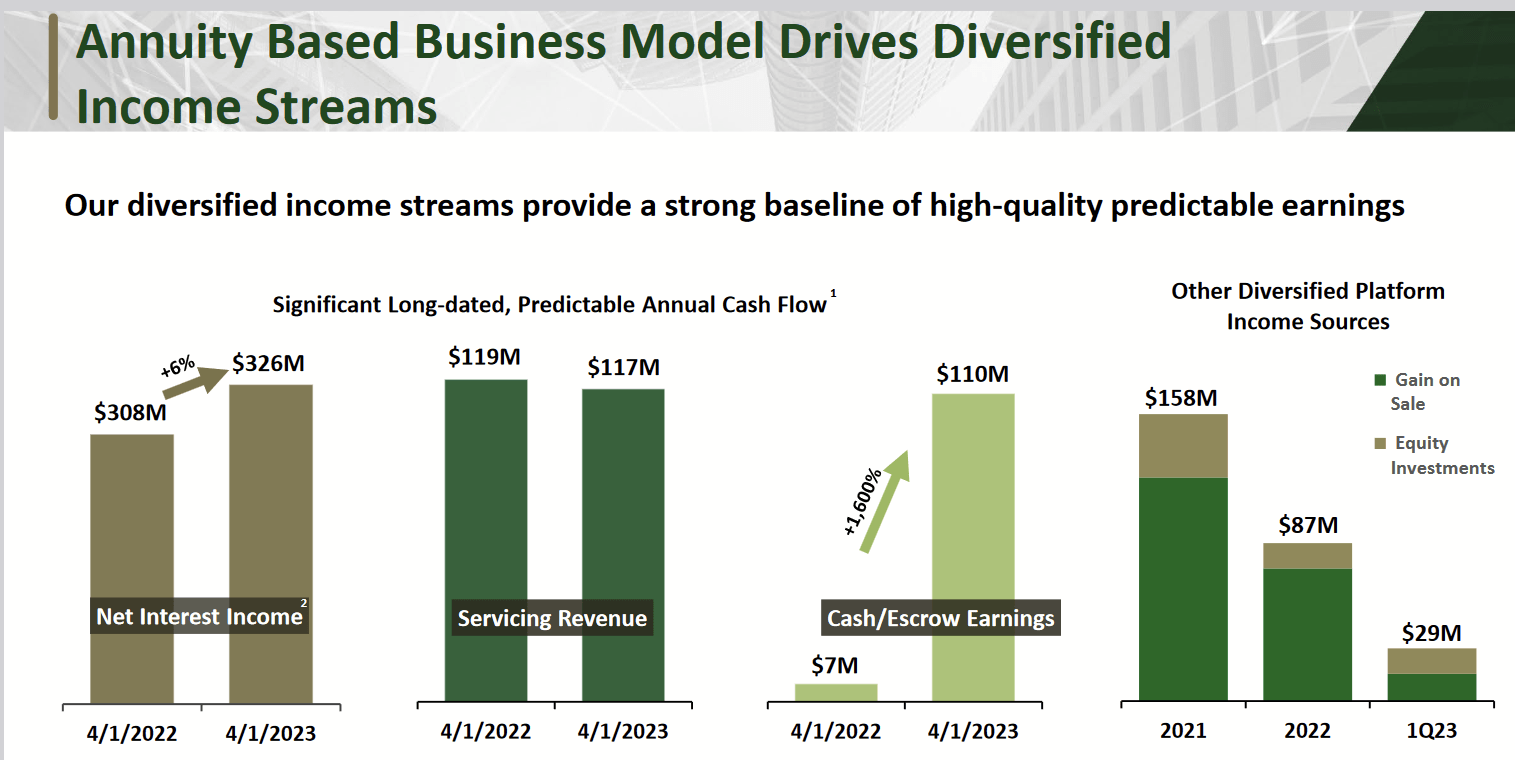

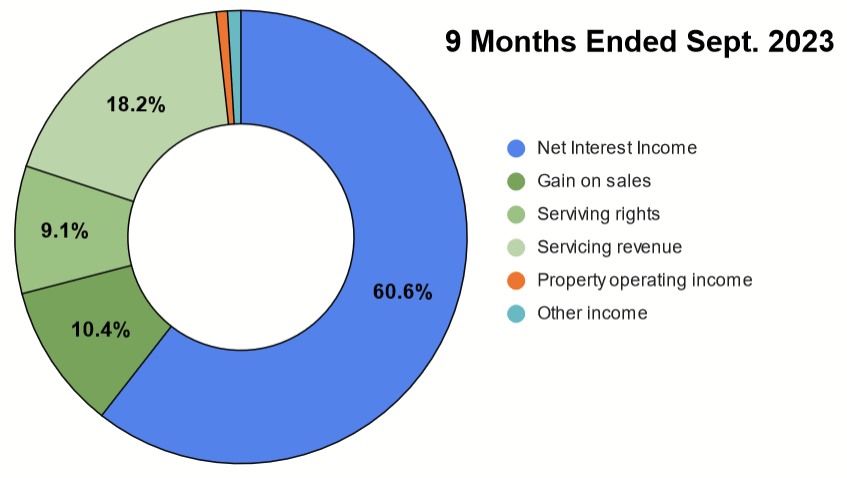

Arbor's dividend is supported by the net interest income on its loanbook, the servicing fees for its Agency Business, interest from its escrow account, gains on sales of some of its portfolio, and a little bit from its own equity positions.

Author's display of revenues (ABR's Q3 2023 10Q)

{kind=link}

Since only the real estate loan business is subject to the law requiring 90% of earnings to be distributed, there is more room for ABR's earnings to be reinvested or held in cash as a liquid cushion during times of distress. This flexibility is what allows Arbor to have a very low payout ratio in its industry, while still growing their dividend over time.

{kind=link}

Let's take a look at their segments more directly.

Structured Business

{kind=link}

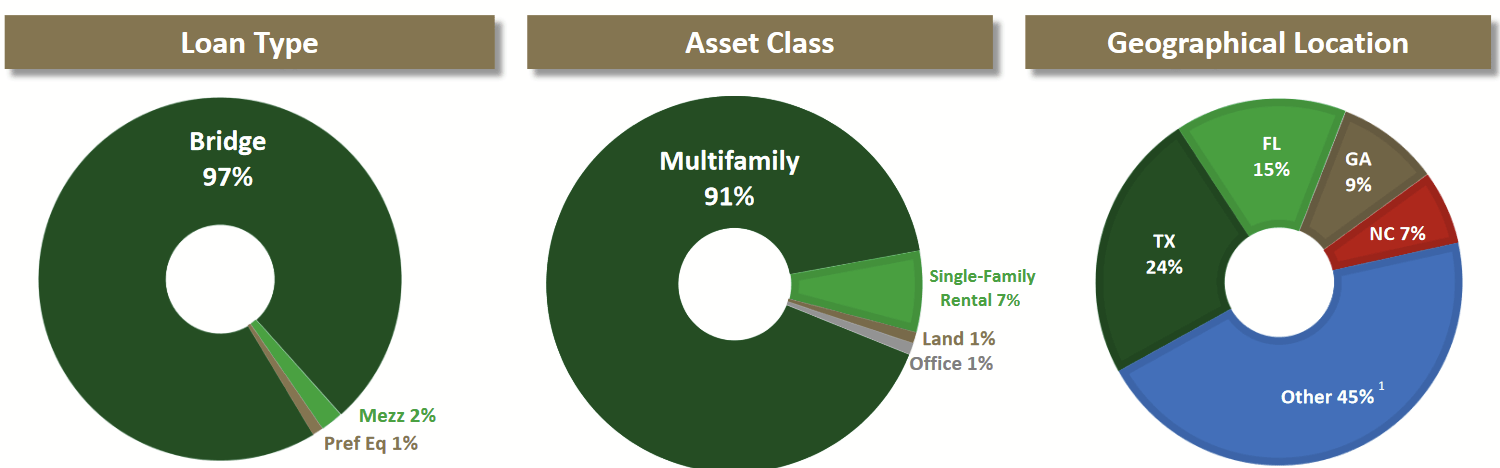

The Structured Business segment is where Arbor originates loans that it holds, where it profits from the net interest income between their debt capital (which is primarily fixed-rate) and the loan they originate with them (which is primarily floating-rate).

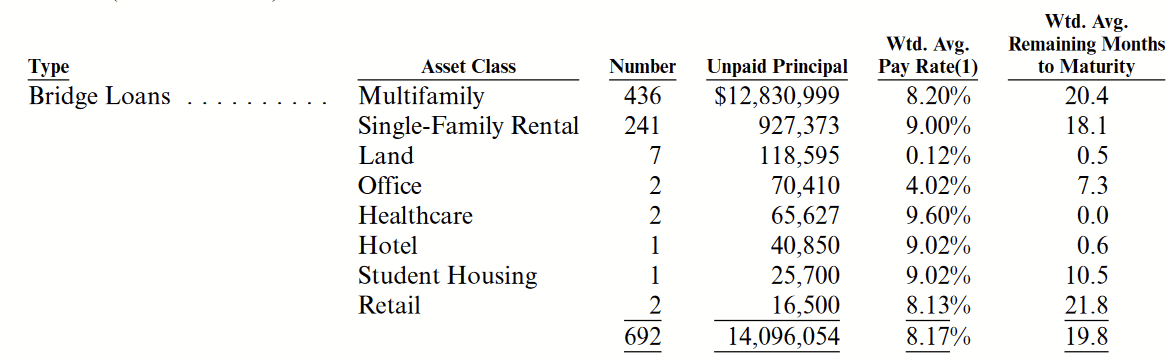

As the charts above show, most of these are bridge loans, given to borrowers in the multifamily rental space, and their nationwide presence means that their originations are concentrated in states experiencing growth and migration, (which for right now is Texas, Florida, Georgia, and North Carolina). As described in their 2022 Annual Report :

The borrower has usually identified an undervalued asset that has been under managed and/or is in a recovering market. From the borrower's perspective, shorter term bridge financing is advantageous because it allows for time to improve the property value without encumbering it with restrictive, long-term debt that may not reflect optimal leverage for a non-stabilized property.

These loans help a borrower secure a property at an attractive price, relative to its income potential. Bridge loans are therefore shorter-term in nature than other mortgages but enjoy high interest rates. This table shows their typical maturity.

{kind=link}

Agency Business

The other major source of income is the Agency Business. This is primarily derived from servicing fees they collect on loans that they originate on their platform and mainly sell to Fannie Mae or Freddie Mac. They are longer-term in nature and therefore provide more durable cash flow in case originations in their Structured Business need to be tightened.

Chart showing agency loans (Arbor.com)

The Structured Business naturally feeds into this, as many of the bridge loans are refinanced by longer-term mortgages through this process, once the borrower is at that phase in the development and management of the property they would have procured with the bridge loan.

A Look to the Future

Single-Family Rentals (SFRs)

While the company feels that it has maximized the potential of low-risk multifamily loans for now, it sees much more potential in SFRs as more renters want a home-like experience. Kaufman explained in the Q2 2023 earnings call :

We continue to expand our single-family rental business as we are one of the only remaining lenders in this space, allowing us to aggressively grow this platform. We remain committed to this business as it offers us three turns on our capital through construction bridge and permanent lending opportunities and generate strong level of returns in the short term while providing significant long-term benefits by further diversifying our income streams and allowing us to continue to build our franchise.

The near term will therefore show a plateauing of the multifamily business and market capture in SFRs, as Arbor's strong financial condition has left it in a unique position to seize on these opportunities.

Multifamily

One of the advantages of multifamily is the steady cash flows they provide to borrowers by having multiple tenants as income sources. In the same earnings call, Kaufman elaborated:

I think on the multifamily side, I do believe that business will return. We have talked about it. We put together programs. And I do believe the second half of 2024 will be a very, very good year for the multifamily bridge loan business, and we will get aggressive and we will start to get aggressive at the end of the fourth quarter, maybe first quarter.

Farther out into the future, it's just a matter of imagining that Arbor is well-positioned to make it through the tough lending market at the present moment and continue to grow its business once originations can pick back up.

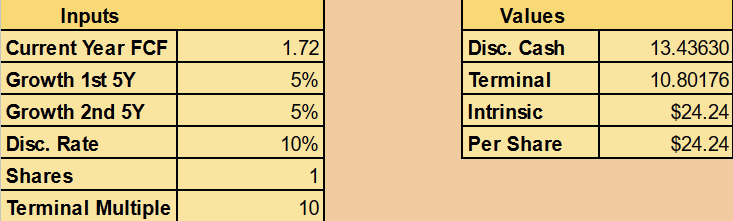

Valuation

As a REIT, the value of ABR is in its ability to grow its dividend per share. Therefore, I will do a Discounted Cash Flow of ABR on a per-share basis. Here are my assumptions:

- Using the most current dividend rate of $1.72

- 5% annual growth over a decade, reflecting the growth opportunities

- Terminal multiple of 10, as mREITs often trade at a high yield, around 10%

Author's calculation based on historical data

{kind=link}

That gets us an intrinsic value of $24.24 per share. Let's look at possible risks for investors.

Risks

Dilution

While Arbor's business model allows them to retain more earnings for reinvestment than other REITs, their payout ratio is still relatively high compared to other dividend investments, and they will often still need to raise capital by selling shares to grow or, possibly, to preserve liquidity.

For example, in 2022, the company raised $408.7m in capital by selling 26.3m shares, representing an average share price of $15.54. While they have stated that they believe they can deliver returns in the upper teens on their investments, they do indicate what they think a fair value of the shares are. Elenio elaborated during Q1 earnings :

It's a $21 price...if you just did a price to book at a seven, at an 8% dividend, yield direct 21 bucks, we've probably traded between seven and eight, like you said, Ivan. So, clearly, just to price us the way others get priced in the space, which we think is unfair. It's a $21 price.

It's more conservative than my own. I did mention before that the company repurchased $37m worth of shares earlier this year, but that's only a fraction of what they raise when feel that they need the capital. It doesn't mean that the returns will be awful, and Arbor has attested to their opportunities, but if at-the-market dilution at mediocre prices becomes a long-term thing, then I believe long-term holders will feel it through a weaker-than-possible dividend.

It will depend too on how opportunistically they respond to things like short attacks in the future. I think great buybacks, while nice, will be rare.

Departure of Ivan Kaufman

As the founder and largest individual shareholder, I think much of ABR's success is connected to Kaufman's shared incentives with other holders, to produce durable dividends that thrive even under times of stress. In earnings calls, he gives straight answers to analysts (at least to my ears), often going beyond the letter of their question to provide deeper insight and to educate them.

{kind=link}

Aged 62, he is not at the end of his career and could easily work another decade if he wants . That said, his retirement or an unfortunate event would mean the loss of an experienced leader. He has a large team of folks who have grown under his tutelage, so attention must be given to who his successor will be.

Recession or Financial Crisis

A recession or major financial crisis could have the effect of limiting Arbor's access to necessary capital or dry up their well of good borrowers. Even a loanbook that is structured for capital preservation may see a halt of interest income in this context for lack of originations and thus limited returns.

Furthermore, their Agency Business is set up so that they must cover up to four months' worth of defaulting loans. While Fannie and Freddie are ultimately obliged to reimburse Arbor, a sudden surge in Agency delinquencies that they must cover could put Arbor in a liquidity pinch that hurts the company and, if nothing else, compromises the dividend. While this is a "perfect storm," shareholders should be attentive to warning signs.

Conclusion

I think Arbor Realty Trust is the High-King of mREITs. With an experienced leader in Kaufman, who has learned from the past by having plenty of skin in the game, he has made a better company, one that stands out among mREITs for its low payout ratio, dividend growth, and resilience during the tests of the last three years.

As long as investors pay attention to the business-specific risks, ABR offers a high yield that is well covered by cash flows and should return significant value to shareholders for years to come.

For further details see:

Arbor Realty Trust: High-King Of mREITs