ABR - Arbor Realty Trust: High Yield But Not That Appealing

2024-01-02 15:29:06 ET

Summary

- Arbor Realty Trust operates in two segments: a lending business that focuses on short-term loans on multifamily properties and an agency business that offloads loans to investors.

- The company faces risks of default due to the short-term nature of its loans and the cooling housing market, but management remains optimistic about its ability to navigate these challenges.

- A recent short attack on Arbor has resulted in high short interest, but the CEO and CFO have increased their stake in the company, indicating confidence in its prospects.

Dear readers,

I've published a number of articles on mortgage REITs (mREITs) last year and haven't been very bullish on the sector. It is true that prior to the November-December rally, prices seemed appealing from a price-to-book value perspective, but there were two things preventing me from investing in most mREITs.

Firstly, the sector has a very poor overall track record as most mREITs have proven to be value traps over time and have returned just 2% per year over the past 20 years. Secondly, I viewed the risk of defaults as quite high, especially for highly leveraged mREITs with a high exposure to distressed office properties. A good summary of my bearish stance can be found in my article here .

Today I start coverage on Arbor Realty Trust, Inc. ( ABR ) which is very different from other well-known mREITs such as Blackstone Mortgage Trust, Inc. ( BXMT ). My goal is to touch on some of these differences to give you a better idea of what kind of business ABR is actually in.

What makes Arbor different?

Arbor operates in two key segments.

First, the mREIT operates a lending business which it calls Structured Business . Contrary to most mREITs which hold a portfolio of long-term loans on commercial real estate, Arbor holds a portfolio of mostly short-term loans on multifamily properties. The loan portfolio makes money by earning a spread between their cost of capital (mostly fixed rate) and the interest rate on outstanding loans (mostly floating rate), and accounts for about two-thirds of all revenues.

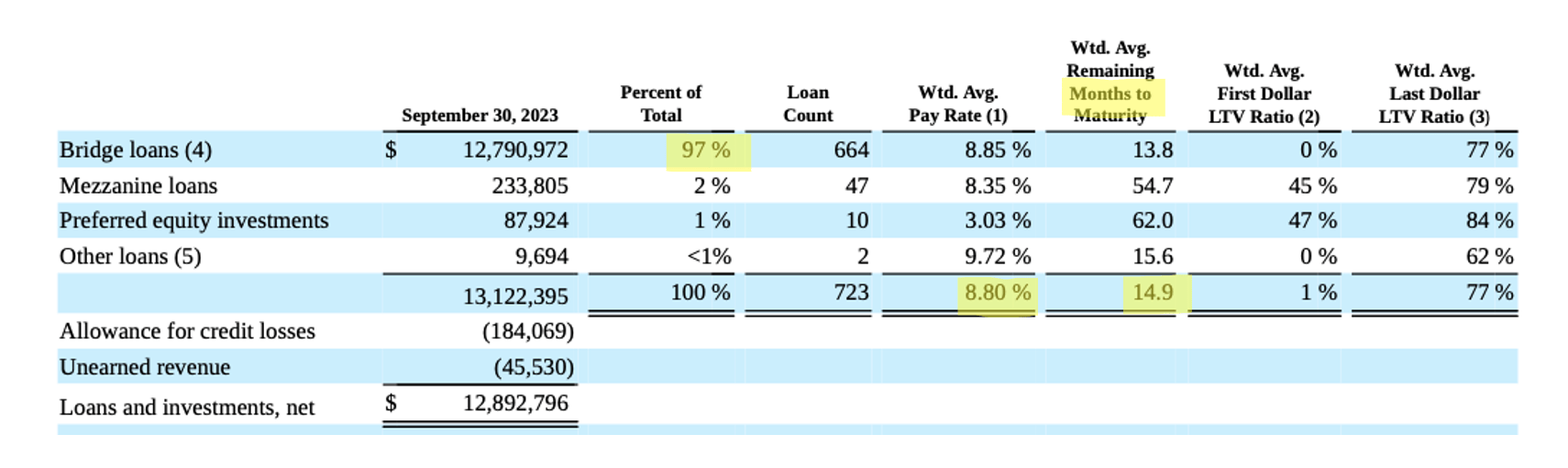

The overwhelming majority (97%) of the loan book is in bridge loans that are generally granted to borrowers looking to renovate/rehab multifamily properties and therefore have short maturities with an average remaining term of just 15 months. Because these loans are generally riskier than traditional mortgages, Arbor gets to charge a high average interest rate of 8.8%.

{kind=link}

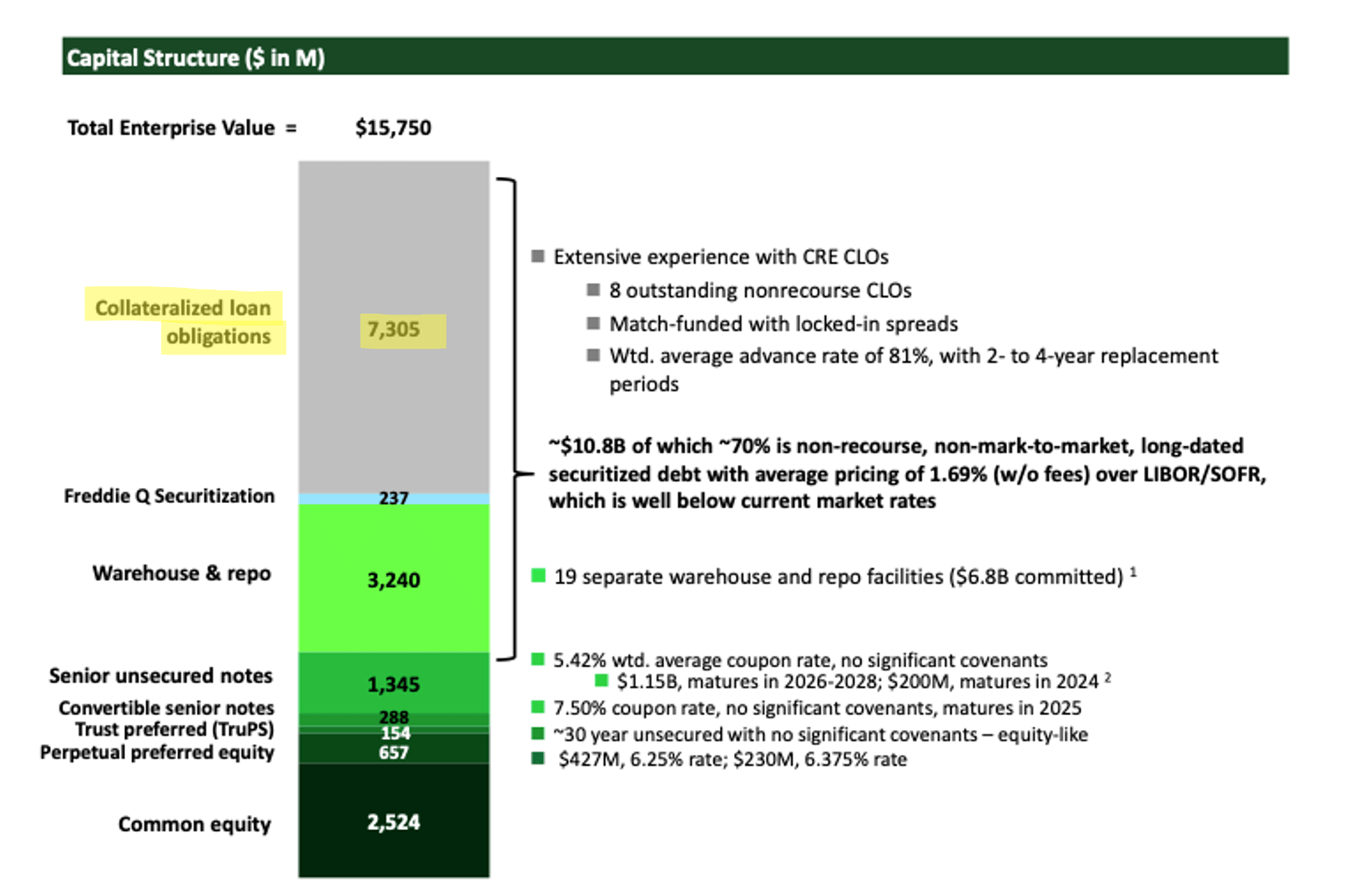

In order to get liquidity against these bridge loans, Arbor established collateralized loan obligations (CLOs) in which it retains a minority (junior) interest. Simply put, this makes ABR heavily leveraged with leverage of about 5.2x. Consequently, any change to book value has a disproportionately large effect on equity (and stock price).

{kind=link}

In addition to the lending business, the company runs an Agency Business , which takes the issued bridge loans and offloads them to investors, mainly Fannie Mae or Freddie Mac. Needless to say, this allows the mREIT to recapture a large amount of initially invested capital. In turn, ABR earns service fees that are longer-term in nature with an average term of 9 years and make up about 20% of all revenues.

ABR Q3 2023 Fact Sheet

Risks

Because Arbor's loans are short-term in nature and the housing market has cooled off significantly over the past two years, I believe there is a real risk that borrowers that took out loans at the peak of the bull market in 2021, might (choose to) default on their loans in 2024.

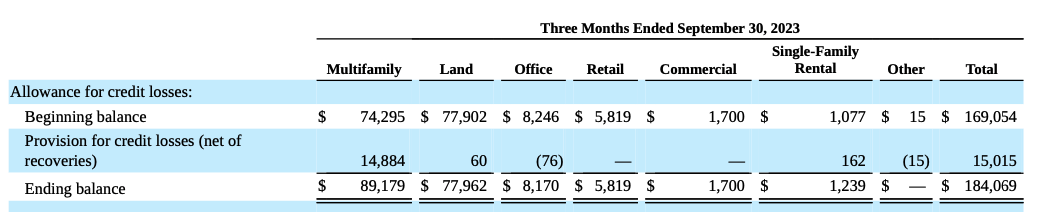

During the third quarter, Arbor increased its CECL reserve by $15 Million to about $90 Million and saw a modest increase in delinquencies of about $28 Million. Compared to a $13 Billion loan portfolio, these represent only about 0.2% which isn't a real threat to the company's bottom line. At least not yet.

{kind=link}

Management expects that the next two to three quarters will be the most challenging part of the cycle. With that said, I think Arbor is well-positioned here. It has been able to grow its book value per share by 2% over the third quarter, despite the increase in CECL reserves and remains one of only a handful mREITs that have been able to grow their book value per share over the past three years. Moreover, the company has nearly a $1 Billion in cash which allows for plenty of flexibility over the next couple of challenging quarters even if delinquencies and defaults pick up.

There has recently been a notable short attack on Arbor, well summarized in an article here , which has resulted in a high short interest of 33%. I don't give the report too much credit and although ABR's response has been quite vague, simply stating that the allegations are unfounded, I do like that both the CEO and CFO have increased their own stake in the company following the release of the report.

{kind=link}

Still, I want to emphasize that ABR's business is more complex (and potentially riskier) than most traditional mREITs and is highly leveraged. While a higher level of risk doesn't automatically disqualify an investment, it needs to be counterbalanced by an adequate reward opportunity.

Valuation

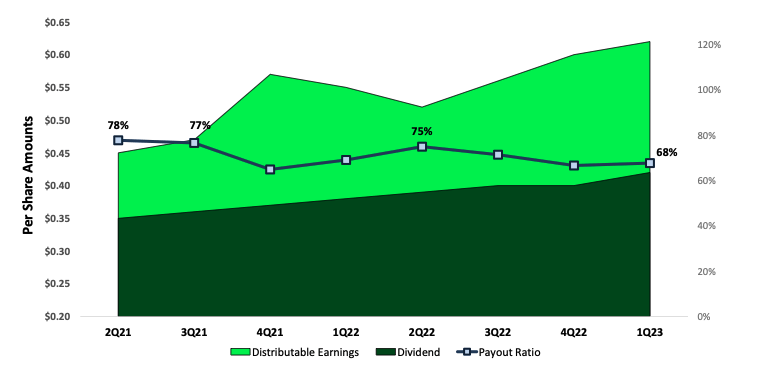

Arbor pays an 11% dividend yield which is very well covered with a payout ratio of 78% in Q3 2023. As such, the company maintains one of the lowest payout ratios in the sector, despite having grown the dividend by 40% over the last three years. And I fully expect the dividend to (at least) remain at this level.

{kind=link}

I have previously shown why a traditional mREIT should never trade materially above book value. ABR trades at 1.16x book value.

But Arbor is able to generate money "on the side" in fees by servicing loans in their Agency Business. As a result, a certain premium is justified here.

Using rough numbers and conservative assumptions, I assume:

- Bridge loan defaults of up to 5% which, given ABR's leverage of 5.2x, would result in a drop in book value from $3.2 Billion to $2.37 Billion.

- A price to sales multiple of 2x for the agency business which puts the fair value of the business around $400 Million

Under these assumptions and with 187 Million shares outstanding, I see ABR as fairly valued here at around $15 a share.

With that said, I do believe that the dividend is sustainable even if defaults pick up and a substantial part of the risk (defaults of up to 5%) is already priced in.

This leads to me rate ABR a HOLD here at $15.80 per share.

For further details see:

Arbor Realty Trust: High Yield, But Not That Appealing