ABR - Arbor Realty Trust: Short Attacks And Multifamily Distress?

2023-12-23 04:41:23 ET

Summary

- Arbor Realty Trust faces ongoing concerns and criticisms from investors following a short attack by Viceroy Research.

- Arbor's CEO and CFO made significant insider purchases of ABR shares after the short attack, showing confidence in the company.

- Arbor has released collaborative research reports and responded with "soft replies" to the allegations made by Viceroy Research.

I recently wrote about Arbor Realty Trust (ABR) at the start of the month. I gave a more long-term view of the company, valuing the shares at $24 and arguing the company is a buy. This was written and published on the heels of a short attack by Viceroy Research on November 16th . While I did mention some of these criticisms against Arbor, it's been a continuing point of concern that I've observed among other investors.

While I wanted to wait for the full-year results before covering ABR again, clearly this is something on people's minds now , as some wonder what kind of losses or gains they want to realize before the year's end. Similarly, my article was unfortunately timed, as it was prepared and published while this attack was still ongoing. I still think ABR is a BUY, but there is certainly more to discuss about the multifamily sector.

Scott Trench, writing for BiggerPockets , explained his concerns about multifamily real estate and laid them out pretty succinctly. It's worth a read to give you an idea of the mindset at the start of 2023. He also notes that real estate investment is local, and his article was talking about multifamily more broadly. Let this be a chance to delve into this story as it pertains to Arbor more specifically then.

Events Since Viceroy Report

Viceroy ended up publishing two follow-up pieces to their initial report. The first came out o n November 29th , while the second came out on December 5th . I'll discuss them more in a moment, but what about Arbor's response to the first report? They gave a very direct response to Ningi in the spring, but so far there has been no formal reply to Viceroy. Instead, there have only been what I consider "soft replies."

Why is this? I'll quote Ivan Kaufman (founder and CEO) from the Q1 earnings call:

While we will not go through a back and forth on every false and misleading allegation by the so-called research company, it should be obvious to everyone at this point that the report's an attempt to capitalize on fear instead of rational thought, and what is so ironic is that they took one of the most successfully restructured transaction our history that was highly lucrative our shareholders and to try to turn into a negative. Most importantly, we have reaffirmed with our auditors that all our accounting for the periods in question are, is correct, as evidenced by the filing of this morning of our first quarter 10-Q with no material changes. I urge our shareholders and the investment public to pay no attention to this noise that is clearly coming from a biased source lacking in credibility.

Given this, it's not surprising that Arbor has chosen not to go the mat again. Some might view this as avoiding fair criticism, and I won't tell anyone to view it otherwise, but let's at least look at the soft replies that we have.

Insider Purchases

We'll start with a look at Forms 4 filed for ABR since 11/16, which I aggregated into this table:

Author's display of Form 4 data

Here we see that Kaufman along with Paul Elenio ((CFO)) have made significant investment into ABR in the two weeks that followed the short attack and share price decline. They are almost certainly aware of the claims made against Arbor, but this is them speaking more with action than with words. Between the two of them, over a $1 million was spent buying shares. It's not their life savings, but I think it's a lot for them to stake in a small span of time.

More Buybacks Approved

As part of their reaction to the Ningi report, Arbor's board approved a $50m share repurchase plan, later confirming in Q1 that they repurchased $37m worth of shares. After Viceroy's attack, Arbor's board again approved repurchases for upward of $150m . We will have to see how many shares, if any, are actually purchased, when FY 2023 results are released.

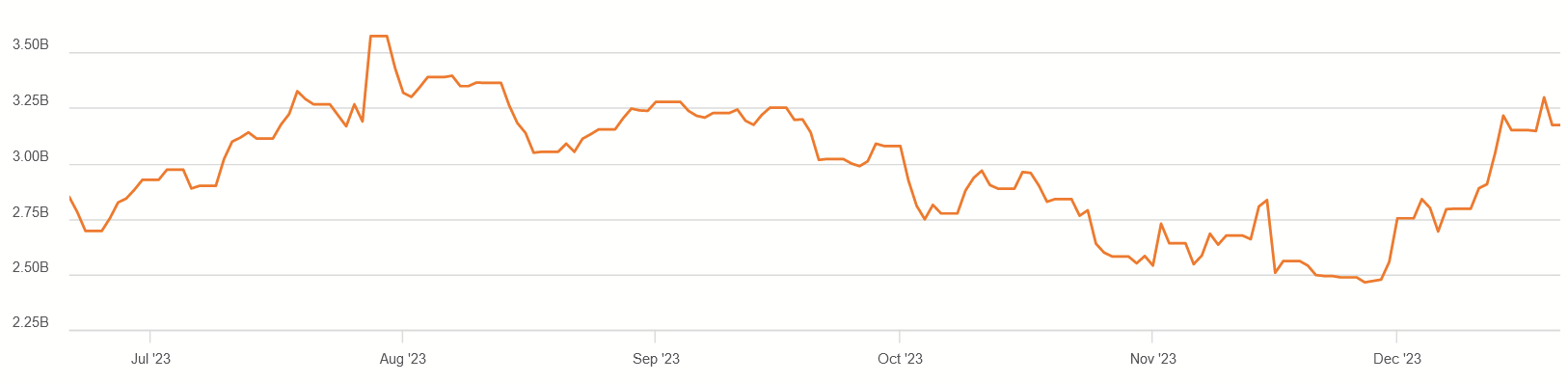

Market cap last 6 months (Seeking Alpha)

{kind=link}

As a thought experiment, if the full buyback program had been done during the recent bottom at about $2.5b, then that would have accounted for about 6% of the outstanding shares at a dividend yield over 14%.

Arbor-Chandan Reports

Similarly, Arbor has just put out a slew of collaborative research reports about rental properties with Chandanomics. It may not be fair to characterize these as responses to the short attack, as Arbor has put out such reports before, but we're still going to review them.

On November 28th, they put out a Fall 2023 Special Report. In it, they observed:

Historically, the multifamily sector has shown stability in times of adversity. Now, with default distress remaining limited so far, rent collections holding up, and Fannie Mae and Freddie Mac backstopping liquidity, the apartment sector is seemingly in a structurally sound position. It is expected that some properties across the country will experience an increase in delinquencies as a result of this point in the cycle. However, well-positioned operators and investors are likely to manage effectively.

In their conclusion, they noted, however:

A narrow avoidance of a recession is quickly becoming the baseline expectation and the outlook for interest rates appears to be more favorable than it was six to nine months ago. However, if 2023 has taught us anything, it's that a soft landing may not be the most apt description for what we are experiencing. Instead, this year has been more like flying through turbulence and the next two quarters are expected to be the worst of this cycle.

Even as the economy has sustained its growth, recent successes are not guaranteed to continue.

In their report on the small multifamily sector , they concluded:

Despite the unsettling market impacts of high interest rates, the small multifamily sector has maintained operational stability, and there is momentum toward price stabilization. On balance, the small multifamily sector, which is bolstered by underlying tenant demand and healthy property-level cash flows, remains well-equipped to navigate through macroeconomic headwinds.

Speaking about large multifamily :

In 2023, multifamily investors are in uncharted waters. Cap rates have risen and transaction volumes have slumped, a reflection of a challenging interest rate environment. But at the same time, property-level operations have held up remarkably well, and high mortgage costs have strengthened demand for multifamily properties. All else being equal, the U.S. multifamily market is balanced by a favorable combination of headwinds and tailwinds that are likely to remain into 2024.

They also released a report about affordable housing and single-family rentals . These, along with the three I linked, are thorough without being excruciatingly long and have graphs and charts to illustrate key trends. Read them in full if you like.

The general takeaway is that the sectors in which Arbor deals are faring better than many of the doomsayers have alleged and that there is good reason to think they will continue to do so, while clarifying that there have been some challenges and why they occur. If people are worried about general trends, this is their answer.

Addressing Viceroy

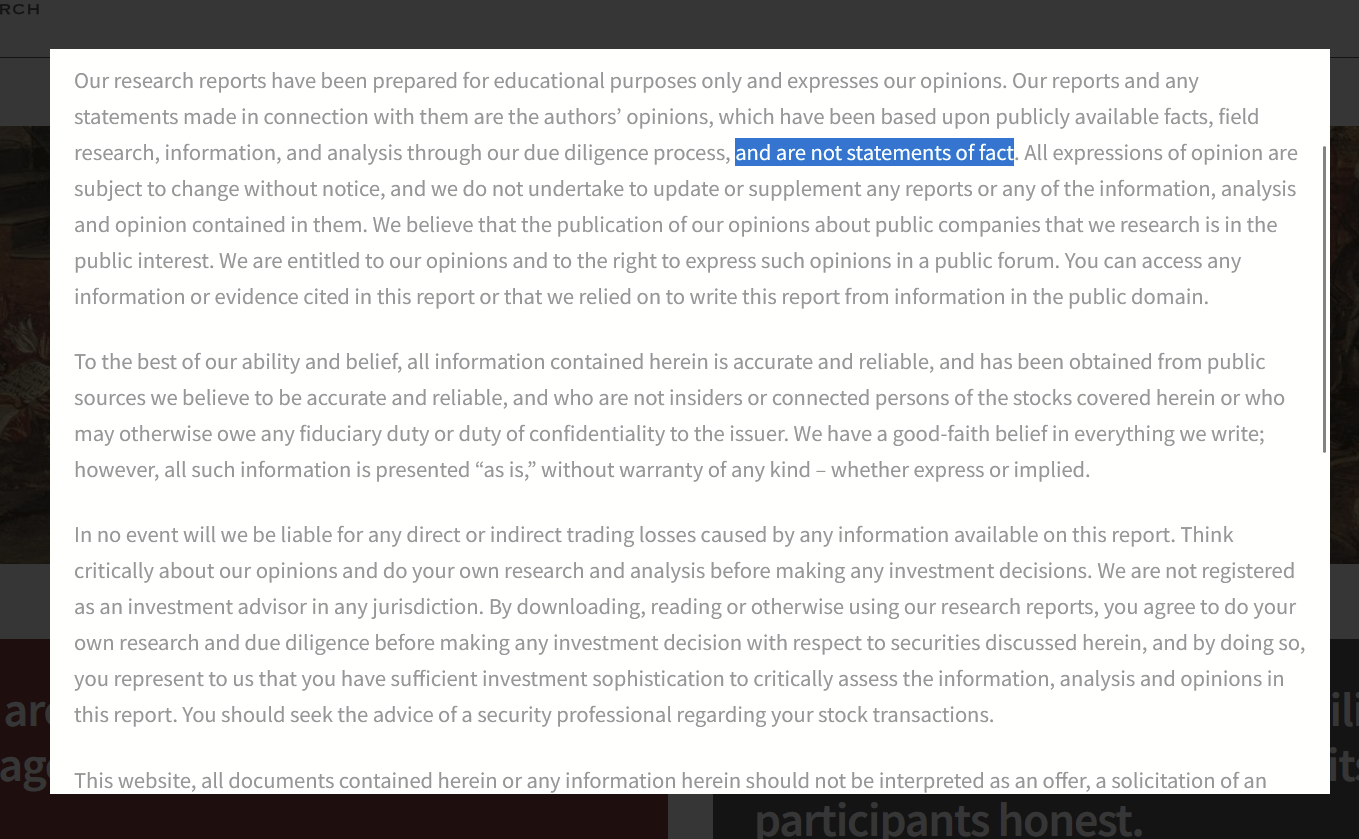

So let's talk about Viceroy and if its claims can be trusted. First, let's start with what automatically pulls up when you load their website:

{kind=link}

It's a verbose disclaimer, and I highlighted the part where they state their reports shouldn't be considered statements of fact. The disclaimer also goes on to say that we should assume the author of any report has a short or bearish position on that investment. This group actually has a Wikipedia page about them, and it gives a history of previous short attacks, some of which resulted in fines and defeats in court. I address these things because they are the first thing a lot of ABR holders noticed and where their curiosity ended.

If we're being fair, we should try to evaluate the claims they have made about Arbor. It is possible that they could have stumbled onto something, and it's an exercise to discern a fair critique of this company from embellishment. The full PDF of the initial report can be read here .

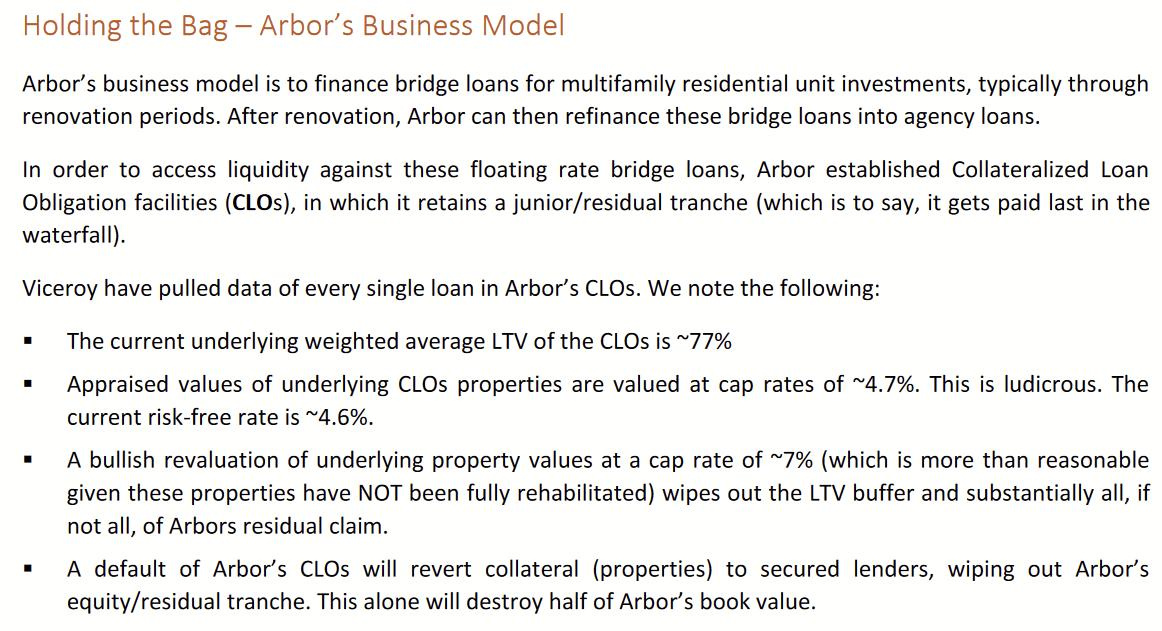

The crux of their claims comes down to Arbor's use of CLOs as part of their capital structure. Viceroy lays out the problem as such:

{kind=link}

This is a big deal, of course, if it pans out. Arbor itself describes this risk in its Form 10K :

If we fail these covenants in any of our CLOs, all cash flows from the applicable CLO would be diverted to repay principal and interest on the outstanding CLO bonds and we would not receive any residual payments until that CLO regained compliance with such tests....In the event of a breach of the CLO covenants that could not be cured in the near-term, we would be required to fund our non-CLO expenses, including employee costs, distributions required to maintain our REIT status, debt costs, and other expenses with (1) cash on hand, (2) income from any CLO not in breach of a covenant test, (3) income from real property and loan assets, (4) sale of assets, or (5) accessing the equity or debt capital markets, if available. We have the right to cure covenant breaches which would resume normal residual payments to us by purchasing non-performing loans out of the CLOs . However, we may not have sufficient liquidity available to do so at such time.

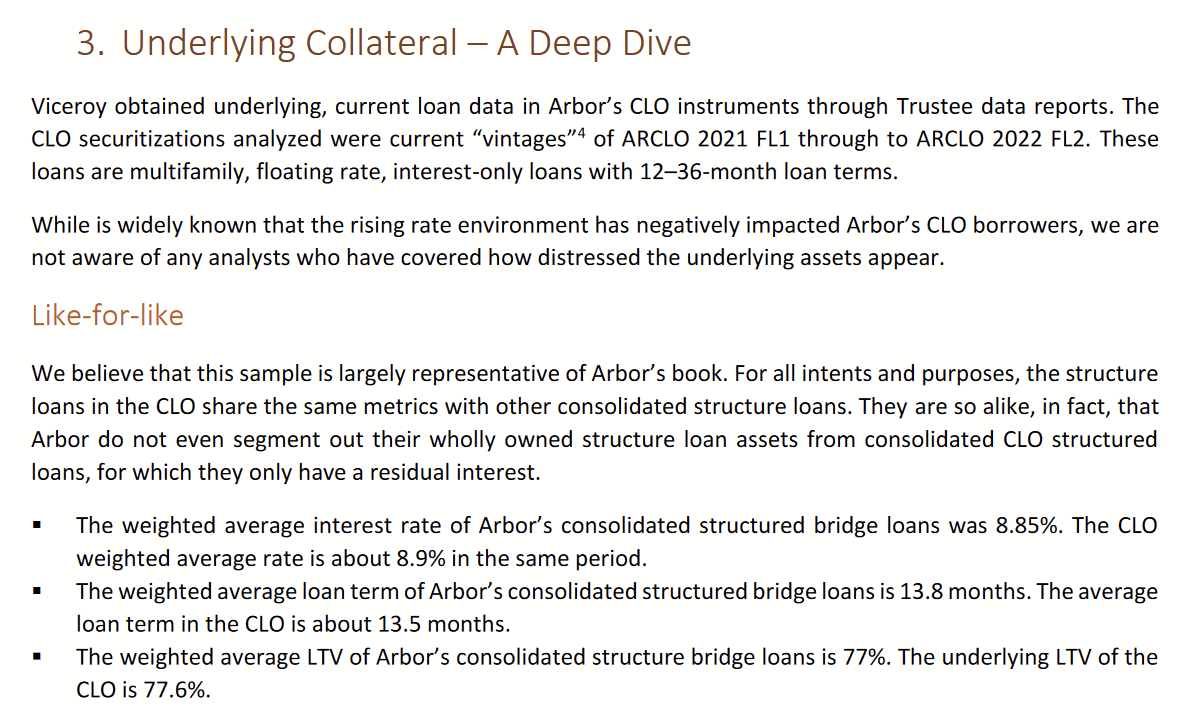

One concern is that, by having to purchase bad loans out of a CLO, Arbor could incur heavy losses. The problem is the "data of every single loan," which Viceroy claims to have in the screenshot above. Farther down the document, we see this:

{kind=link}

Here, they mention that they got loan data through Trustee reports that aren't cited. They then go on to say these data are a sample (not every loan) that represents the other loans. They also note in that screenshot that Arbor does not segment loans financed by the CLOs from those that Arbor finances itself. Later on they state:

{kind=link}

Here they have beliefs about the CLO portfolio but lack facts, such that they can't distinguish them from loans financed by Arbor itself. Then there's the limited information about the underlying properties. Starting on Page 16 of that PDF, you can see them cover four properties. This information just seems to be Google and Yelp reviews with claims that aren't relevant to repayment of the loans themselves.

That's all I am going to say on the initial report. Another report was published on November 29th . It mentions the delinquencies for the CLO loans, which they claim ballooned in the two weeks since the first report. Two weeks prior, they didn't know which loans were financed by CLOs or by Arbor itself, and now they know enough to spot the sudden uptick in CLO delinquencies and can even break it down on a monthly basis, all based on un-sourced data from "trustees."

I think it's clear why Arbor didn't respond. Viceroy isn't actually claiming anything. It headlines that it will make bold claims, but it's ultimately just guessing without verifying. What's there to refute? If you'd like another breakdown of Viceroy's report that is friendlier to the human attention span, Armchair Income made a video about it on YouTube a few weeks back.

Addressing the Near-Term Risks

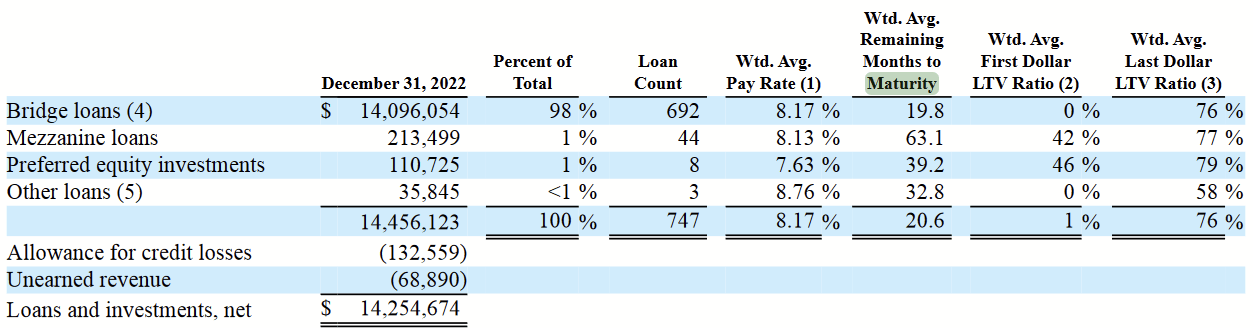

There's a reason Viceroy's report touched a nerve, though. There are concerns about the ability of multifamily borrowers to repay bridge loans that were originated between 2021 and 2022. That basic piece of information (which Viceroy also mentioned) is true. Of course, that was already publicly available in Arbor's 10K:

{kind=link}

There we see that their average bridge loan is maturing starting in 2024, so this bubble could burst very soon. Property values in general have decreased, to account for the fact that interest on any mortgage to purchase them now would be higher. Ultimately, it comes down to whether or not Arbor's individual loans have been or will be affected in that way, as that could hinder refinancing through Arbor's Agency platform.

Even if this occurs, there are a number of ways this can all play out, so let's the address that.

Simple Default

The first, of course, is that defaults can and will occur which would lead to losses for loans that Arbor financed itself, with CLOs, through their credit facility, or however. I think quibbling over which loans default isn't a huge deal here. Any defaults at a significant scale can lead to realized losses, margin calls, and dividend cuts. Arbor could very well just be stuck holding a lot of bags with no recourse. Is that all that can happen?

Extension or Restructuring

Arbor will allow some loans a right to extend repayment. Others might need to be restructured entirely. This is always a case-by-case basis, but an example of Arbor's adaptability was seen earlier this year, as I'll quote from their latest 10-Q :

In April 2023, we exercised our right to foreclose on a group of properties in Houston, Texas that are the underlying collateral for four bridge loans with a total UPB of $217.4 million. We simultaneously sold these properties to a significant equity investor in the original bridge loans and provided new bridge loan financing as part of the sale. We did not record a loss on the original bridge loans and recovered all the outstanding interest owed to us as part of this restructuring.

So they were quickly able to find a buyer for a bundle of loans without experiencing any losses. Of course, it doesn't always work out, and Arbor has reported losses:

{kind=link}

Complete and total losses aren't to be found, however. Some capital, usually most, is recovered and then reinvested.

Taking Hold of the Property

Even an uptick in situations that result in losses aren't completely doomed. Arbor can still seize the properties on defaulted loans, run them for a while, and collect rents until they can find a buyer. It's not ideal, and it would tie up their capital for longer than we might like, but it's still something that long-term owners should consider.

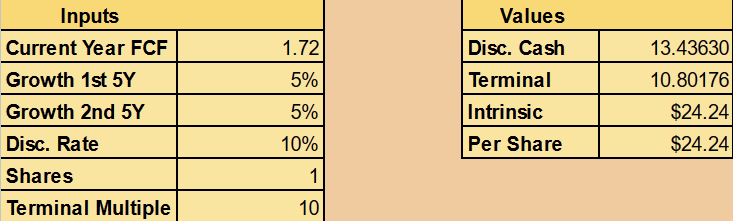

Revisiting My Valuation

In my last article, I valued ABR at just over $24.

{kind=link}

Having discussed the criticisms of Arbor, do I feel differently about this valuation? No. My belief is that we can't truly know what happens to Arbor's book of loans before they mature. Until then, it's really a matter of who you believe. You can believe the anonymous author of the Viceroy report. You can believe the investors who are generally skeptical of multifamily bridge loans. You can believe Ivan Kaufman and his team.

That said, I believe ABR is a buy, but I recognize that it's not a huge difference if someone buys right after my first article or if they buy sometime next year. If the risk of these defaults is too worrisome, I will say that it's okay to wait. Peter Lynch himself has often said this. If I think it's worth $24, I don't think it's bad to let the next three-to-six months pass, even if that means you buy it at $18. If it spares you the anxiety, then do that.

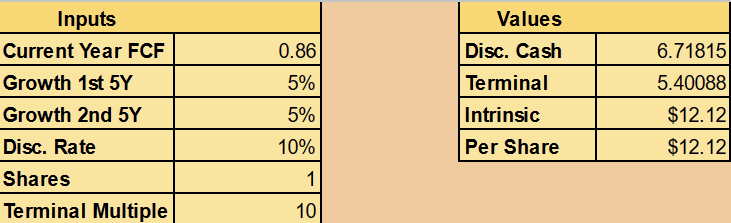

I'll still be a sport and present an alternate valuation, though. Everything is the same, except we don't use the current dividend of $1.72. We instead assume the risks materialize, Arbor has to take some unexpected losses, maybe even dilute a bit, and thus the dividend is cut in half. That would lower it to $0.86 per year, and then Arbor would have to start over with steadily growing it again.

{kind=link}

Naturally, halving the dividend halves the valuation, but this is roughly how low ABR fell after the short attack. Essentially, the shares have been priced for disappointment for quite a while now. I don't think these issues could ever be as bad as 2008, so unless there is a bigger monster around the corner that not even the critics have spotted, I think pricing in more pessimism is misplaced.

Conclusion

I dubbed Arbor Realty Trust the "High-King of mREITs." Even so, it isn't perfect, and this has brought the attention of both spurious short attackers and seasoned investors. The potential weakness lies in the upcoming maturity of its bridge loans that were issued from 2021 to 2022, many of which may not be completely refinanced through Arbor's Agency platform. This is a potential consequence of the rapid interest rate hikes that occurred after these loans were originated, which could have hurt the property values.

Yet, some of the research produced by Arbor indicates that demand for multifamily housing remains strong and that rent payments to borrowers remains steady, indicating ability to repay loans in this sector.

Lacking a comprehensive breakdown of every loan, every property value, and every property's NOI, we just can't know if Arbor exposed itself to the general risks or not until they materialize. The CEO and CFO spent the last two weeks of November investing $1 million of their own money into ABR, so either they see a tremendous profit ahead, or they are blind to their own failures.

If their skin in the game isn't good enough for you, you still don't have to buy the next time the market opens. Wait a bit, follow the story, and even if it means you'll get a higher price, there's nothing wrong with patience if it means crossing out some risks.

For further details see:

Arbor Realty Trust: Short Attacks And Multifamily Distress?