FPI - Arbor Realty Trust: The Power Of Information Asymmetry

2023-04-05 05:30:54 ET

Summary

- The short attack on ABR had a major impact on the stock.

- It also took down the preferreds.

- We analyze the situation and believe there is an opportunity here.

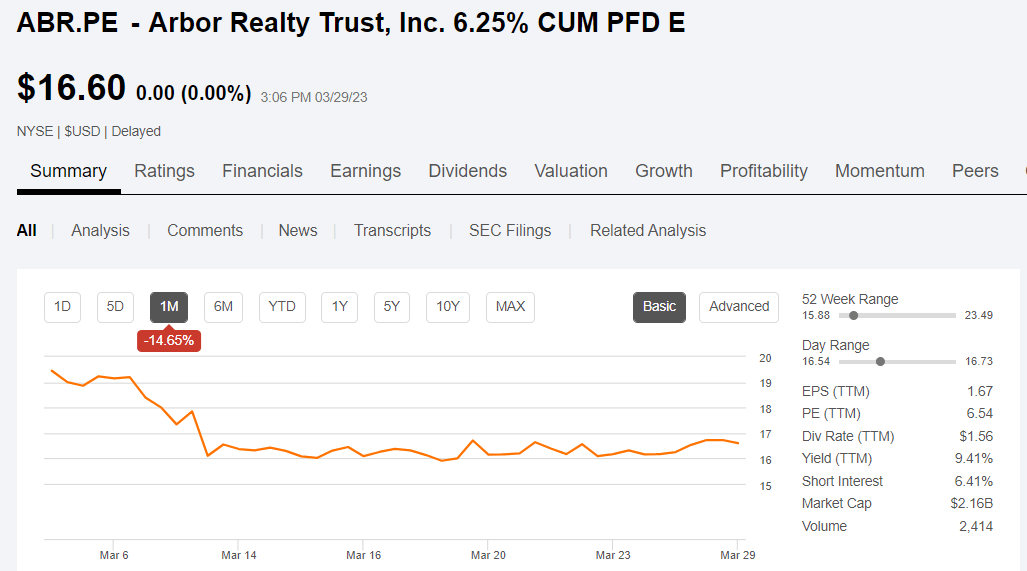

Arbor Realty Trust ( ABR ) has been the subject of a short attack resulting in a greater than 20% drop since the report came out.

{kind=link}

Such attacks are becoming quite commonplace these days and they usually represent opportunity one way or the other. Either the short attacker is right and the stock has significantly further to fall or the attack is misleading which means the stock should bounce back to its pre-attack level.

This article will examine the claims of the short attack and attempt to determine which way this will shake out. Let me open with why these attacks are becoming increasingly prevalent and why they are so effective at moving market prices.

The power of information asymmetry

The Ningi report attacking ABR made claims of fraud without explicitly using the word fraud. My hunch is that by avoiding the use of the word it makes a countersuit more difficult as their attacks are more nebulous in nature.

Here is Ningi's opening statement that I consider an accusation of fraud.

Arbor's financial statements for the last twelve years cannot be trusted, and auditors, as well as the board, turned a blind eye on misstatements and misconduct"

Such allegations are incredibly powerful because of the information asymmetry. Ningi, much like other similar short attacks, claims to have done thousands of hours of boots on the ground type research. This involves stuff like digging through hard to access property records, physically visiting locations to see if lights are on, asking questions of anonymous former employees, etcetera.

This is asymmetric information as investors in Arbor have absolutely no way of vetting these claims. It is information based on stuff that is not publicly accessible which makes it very potent at raising doubt.

When such allegations come out shareholders are left with 3 options:

- Sell the stock

- Continue holding and take the risk that perhaps there actually is fraud

- Do countless hours of proprietary research to debunk the allegations

Well, for heavily retail owned names such as Arbor, it isn't really plausible for each individual shareholder to do the massive counter-research. If someone has just a $10,000 position in ABR, it just isn't worth that much time and effort to dig that deep.

Thus, it is not at all surprising that stocks sell off when these sorts of reports come out. It seems to be a loophole in the system which allows for market manipulation.

Loophole in the system

Shorting is a healthy part of the financial system. Critical research reports are an essential part of protecting investors from bad actors in the business world. A short seller producing good research about why a stock is a bad investment is arguably a public service. Thus, we as a society must allow short reports as a category to be published.

The challenge is deciphering which short reports are honest, good faith research and which are intentional distortions and illegal market manipulation. Determining the difference is even harder based on the future being unknowable. Someone could write a short report with good honest intent and simply be wrong. As someone who has personally written a few dozen short reports over the years, I was wrong on at least a portion of them, yet I can say with certainty that my intent was honest in every case.

Thus, a report that ends up being wrong is not necessarily a misleading report. Predicting the future is hard. Usually the only way to prove that a report was written with ill intent is to find a money trail and communications demonstrating the report was written with intent to manipulate the market which is how the short and distort attacker of Farmland Partners ( FPI ) got caught. Farmland Partners went through the painstaking process of proving in a court of law that its attacker had ill intent. FPI won on all counts and yet the penalties to the short and distort attacker were so incredibly minor that it doesn't really deter such acts in the future.

Unfortunately, the incentivization is such that producing false research is wildly profitable.

Shorting a stock and then manipulating it down via such reports nets 10s of millions of gains while getting caught seems to just be a slap on the wrist. That is the reality in which we invest today and a reason to stay diversified. Any stock can be attacked at any time and it can take years for even a good company to clear its reputation.

Back to Arbor Realty Trust

Is Ningi's report honest research or a short and distort manipulation?

Like any other analyst I only have access to public information such as SEC filings, conference recordings, and fundamental data. In fact, this is enforced by the SEC's Regulation FD in which companies are not allowed to provide material information to anyone without providing it publicly to everyone.

Therefore, I have no means of determining whether the Ningi research which is based on non-public proprietary information which they supposedly collected is real or fake.

That said, I am of the opinion Ningi's report is a short and distort attack with ill intent and I'll provide my reasoning below.

Persuasive language rather than research report tone

The tone of the research report strikes me as something that is intended to manipulate market price.

For example, observe the ample use of words like "secret" and "missing" in the Ningi passage below.

In our opinion, Arbor is hiding a mobile home portfolio and the related $600 million debt; the company secretly invested in maintenance, most of its $170 million in net profits from that real estate portfolio is missing, Arbor's management is secretly selling the properties, sales profits are missing, Arbor's shareholders will have to fund any arising costs and take the losses."

It reminds me of internet clickbait headlines like "10 secret health facts doctors don't want you to know about"

What strikes me as particularly odd about this language is that the Ningi report cites the source of their information about the maintenance capex as SEC filings.

If information is in an SEC filing, it's really not much of a secret.

Straw manning

In argumentation, straw man is a logical fallacy but also a powerful persuasive tactic. Straw manning is basically the process of defeating a very weak argument and acting as if that weak argument were the crux of the opponent's thesis.

Much of the Ningi bear thesis is based around Lexford which is a portfolio of manufactured housing assets in which Arbor invested over a decade ago. Ningi spends a substantial portion of their 43 page report proving that Arbor does in fact own Lexford with the idea that ABR is somehow saying that they don't own Lexford.

Ningi even tweets a sort of taunt toward ABR about this idea.

Twitter

The idea Ningi is putting forth is that since ABR owns Lexford they are on the hook for the $582 million of debt tied to Lexford.

This is a straw man argument, however, because ABR does not claim immunity from this debt due to not owning Lexford. As far as I can tell, ABR has never made any attempt to suggest they don't own Lexford. In fact, ABR discusses Lexford in every 10-K from the most recent one all the way back to the 2011 filing.

Instead, the reason ABR is not on the hook for that debt is because it is in a subsidiary.

Such subsidiaries are very common among REITs. A REIT can put assets and debt into a wholly owned or JV owned subsidiary which can be structured so that it is non-recourse to the REIT. Let us consider an example in which a subsidiary initially had $1B of assets and $600 million of debt. If something catastrophic happened taking the asset value below $600 million the subsidiary would then have a negative equity value. However, since the debt is non-recourse to the REIT, it would not be a negative value to the REIT. It would simply be written down to zero on the REIT's balance sheet entry (there are a few different elective methods for how this is done in GAAP accounting).

I believe this is largely what happened with Lexford as ABR did in fact write it down to $0. It would seem that Lexford has since recovered fundamentally as ABR is continually receiving income from this joint venture.

This makes some sense as these are manufactured housing assets which is a sector we know to have performed very well over the past 7 years.

The value of the assets within Lexford as of today is unknown. GAAP accounting does not have a way for impaired assets to get marked back up unless they are sold or there is some other sort of exit event. Thus, even if the assets were today worth $1B against the roughly $600 million of debt, it would still be on the balance sheet at $0 if that is where they were previously marked down to.

Ningi goes on to suggest that the assets are worth $0 and that ABR is on the hook for the entirety of the $582 million due to bad boy guarantees. I see 2 problems with this assessment:

- The asset value is unknown and this subsidiary might actually be positive value net of the debt

- The debt appears to be non-recourse to ABR. Bad boy guarantees only trigger in certain events which I do not see evidence of having occurred.

Here is the explanation of the bad boy guarantees from ABR's 10-K

"we provide limited ("bad boy") guarantees for certain other debt controlled by Lexford. The bad boy guarantees may become a liability for us upon standard "bad" acts such as fraud or a material misrepresentation by Lexford or us. At December 31, 2022, this debt had an aggregate outstanding balance of $582.8 million and is scheduled to mature through 2029."

Having off balance sheet subsidiaries absolutely makes financial accounting murkier and harder to track, but it is legal and very common.

For examples I would suggest looking at Blackstone. Go through their records and you will find countless subsidiaries that went bankrupt and yet Blackstone is extremely successful. This is because subsidiaries can be structured such that any debt they take on is non-recourse to the parent company.

It affords compartmentalization of risk.

As an investor I am not a huge fan of subsidiaries, off balance sheet assets, or joint ventures. Each of these structures makes financial reporting significantly murkier, but it does have a purpose and it is legal.

As the subsidiary debt was the bulk of Ningi's bear thesis and I don't think it is going to end up hurting ABR, I think their short report is largely wrong.

Investment opportunities

Usually when a company's stock price is knocked down 20%+ without a change in fundamentals it is a great buying opportunity.

Yet I don't actually see much opportunity in ABR common. Frankly, the stock was quite overvalued prior to getting knocked down so this merely took it from overvalued to fair value or slightly undervalued. Arbor has been one of the best performing mREITs with stock returns trouncing those of its peer mREITs. Arbor is at 245% of 2017 values compared to 81.5% for mREITs.

{kind=link}

Some of that outperformance was fundamental in nature, but the price action did overdo it resulting in ABR trading at a substantial premium to book.

The collapse in March has pulled it down to 88% of book and I think that is roughly where mREITs should trade. Mortgage REITs operate risky businesses and as a sector generate fairly weak returns for investors. As such I don't like to invest in the sector until companies trade at very large discounts to book value.

If you agree with me that the Ningi short thesis is wrong, ABR is fairly valued or maybe slightly cheap, but if Ningi is right, ABR could still fall significantly more. I don't see the common as a great opportunity.

The Preferreds look excellent

In addition to common equity, Arbor has 3 series of preferreds which traded down in the days following the short report.

{kind=link}

At current pricing, the D series and E series have yields over 9% and substantial discounts to par. If these get redeemed at their call dates the capital appreciation takes total return on D and E to 74% and 79%, which would be an annualized return of 23.3% and 23.5%, respectively.

{kind=link}

However, given the relatively low coupons of 6.375% and 6.25%, I don't see redemption as likely unless interest rates broadly go back down close to zero. As such, a holder of these preferreds would just collect their 8.8% yield on cost in perpetuity or until something goes horribly wrong.

I think either one of those would be a reasonably good investment, but the bigger opportunity is in the F series. While the Series F has a similar current yield, it has a floating feature that kicks in on 10/30/26 which takes the coupon to 3 month SOFR +544.2 basis points. With where interest rates are today, that would be a roughly 14% yield.

Since the floating rate adder of 544 basis points over SOFR is so aggressively high, ABR is highly incented to redeem this issue when it hits the call date of 10/30/26. If it is called, shareholders get $25 per share plus the dividends they got along the way. That would be a total gain of 73.27% or an annualized gain of 20.45%.

Preferred safety

Mortgage REITs, Arbor Realty included, depend heavily on loan origination volume to fuel their earnings. With the banking crisis and a general freeze in real estate transactions, the outlook for originations is uncertain.

ABR does most of its business in the form of bridge loans.

{kind=link}

These are short term in nature and highly lucrative for ABR, but if transaction volume falls off, there will be fewer bridge loans to go after.

This poses a risk to earnings which I think makes the common a bit risky. If earnings decline sufficiently, the common dividend might need to be cut.

I can also see it going the other way. With banks having less liquidity to loan out, more of the loans could go to non-bank lenders like Arbor. If that is how this shakes out, ABR could have growing earnings and would indeed be quite undervalued.

As there haven't been all that many crises of this nature (significantly different than GFC), I think it would be foolish to be too certain on directionality.

Thus, I look at ABR's earnings as high but fairly risky. Its assets look significantly stronger. During the period in which ABR was trading at a premium they took advantage by issuing a metric ton of equity.

{kind=link}

Since most was issued when the stock price was high, it was accretive to shareholders, but even better for the preferreds. All of this equity is a cushion underneath the preferreds.

Even in the event that the bad boy guarantees somehow get triggered and ABR does become liable for the debt of the subsidiary, the preferreds still look strong. With over $2B of equity beneath them, a $582 million hit would be absorbed by ABR common and would not dent the liquidation value of the preferreds.

ABR preferreds offer an unusually strong reward relative to risk and we particularly like the F series.

For further details see:

Arbor Realty Trust: The Power Of Information Asymmetry