TFII - ArcBest: A Sell Due To Underperformance And Challenges

2023-09-26 11:34:01 ET

Summary

- ArcBest Corporation is a logistics company facing challenges such as a new labor union contract, increasing costs, and a potential recession.

- The company operates in a highly competitive industry with numerous competitors in both the asset-based and asset-light segments.

- ArcBest has underperformed its competitors in terms of financial performance and does not have a clear competitive advantage, making it a sell recommendation for long-term investors.

Introduction

ArcBest Corp ( ARCB ) is a logistics company that operates in a highly competitive industry. The company has underperformed its peers in recent years and is facing a number of challenges, such as a new labor union contract, increasing costs, and a potential recession. Given that it doesn't seem to have a competitive advantage over its peers now, I recommend selling ArcBest stock if the investor has a long-term approach.

Competitive Landscape

ArcBest Corporation operates in a highly competitive logistics industry; for instance, there are around 1.2 million trucking companies in the US and over 17,000 active brokerage authorities . Competition in the logistics industry is based on various factors, such as pricing, service, availability of flexible shipping options, quality of service, technological capabilities, and industry expertise. The Asset-Based segment competes primarily with other Less Than Truckload ((LTL)) carriers. In contrast, the ArcBest segment competes with a broader range of logistics providers, including asset-based truckload carriers, logistics companies, freight forwarders, etc. ArcBest's key competitors include:

-

Asset-Based segment: FedEx Freight Corporation ( FDX ), the LTL reporting segment of FedEx Corporation; the LTL segment of Knight-Swift Transportation Holdings Inc. ( KNX ); Old Dominion Freight Line, Inc.( ODFL ); Saia, Inc. ( SAIA ); the LTL reporting segment of TFI International Inc. ( TFII ); and XPO Logistics Inc. ( XPO ).

-

Asset-Light segment: C.H. Robinson Worldwide, Inc. ( CHRW ); Covenant Logistics Group ( CVLG ), Inc.; Hub Group ( HUBG ), Inc.; the Integrated Capacity Solutions segment of J.B. Hunt Transport Services ( JBHT ), Inc.; the Logistics segment of Knight-Swift Transportation Holdings Inc.; Landstar System ( LSTR ), Inc.; RXO ( RXO ), Inc.; and the Freight segment of Uber Technologies ( UBER ), Inc.

Seeing the last ten years' financial performance (measured by ROIC, EBIT, and FCF), it's clear that ArcBest has underperformed many of its competitors in the last ten years:

Author's Elaboration with data from QuickFS

As we can see, ArcBest's ten-year ROIC is a fraction of Old Dominion's ROIC; moreover, its EBIT margin is thin, which I believe makes it vulnerable to pricing competition and changes in labor and fuel costs that cannot be moved to customers. Likewise, qualitative information tends to align with quantitative information, as according to Comparably , Old Dominion is best ranked in Product Quality, Customer Service, and Pricing. In contrast, JB Hunt is best rated in Net Promoter Score (followed by Old Dominion) and second in Pricing and Customer Service. Thus, I think Old Dominion and JB Hunt are (and have been) capable of offering a higher value to customers than any other company in the industry. For that reason, they have achieved such a sound financial performance. However, ArcBest is the best in all the metrics related to all labor metrics, such as CEO Approval, Culture, and Employee Net Promoter Score, which signals that ArcBest may have a competitive advantage in hiring new talent over any other in the industry and have the happiest workers. So, even if the labor expense is high (over 50% of the sales before the pandemic).

Nevertheless, ArcBest is trying to improve its efficiency and financial performance by investing heavily in technology and its assets-light segment and expanding logistic services. However, the relative success of this strategy is yet to be seen, as it's difficult to predict if these initiatives will improve its competitive position because the market is highly competitive. Other competitors may develop better technology or adapt faster to customers' needs.

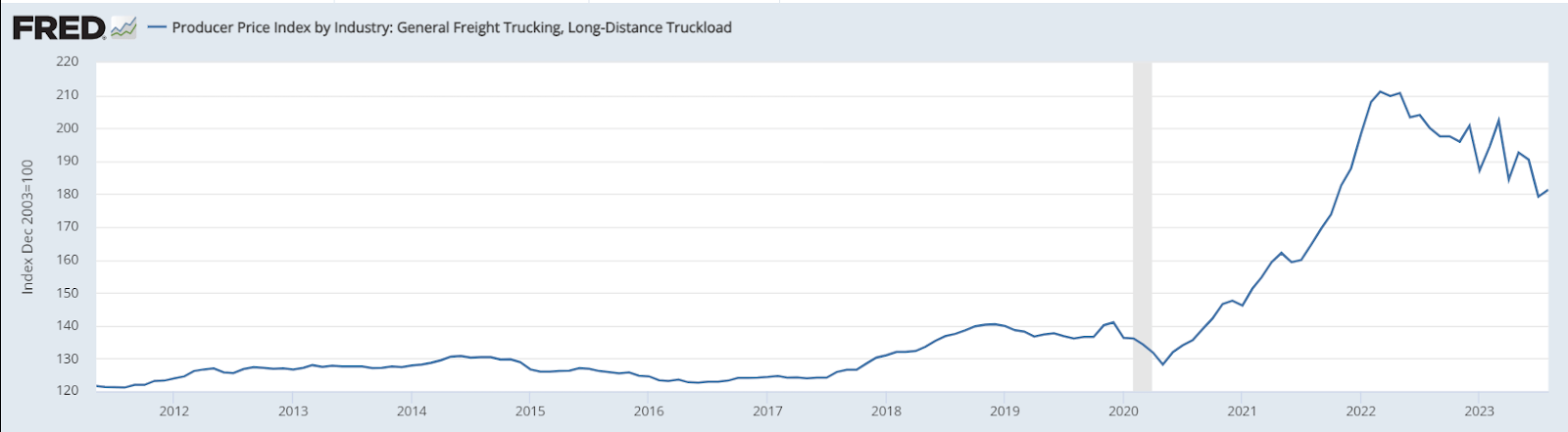

Knowing the competitive position of ArcBest is crucial, as the boom in the logistics industry has ended, and the future looks less promising than the two previous years when the supply chains experienced significant stress, as the demand was relatively higher than the installed capacity. However, economic data indicates that the boom has ended as the PPI Trucking has fallen since March 2022, and the Global Supply Chain Pressure Index remains lower than pre-pandemic levels. The former is confirmed by trucking companies experiencing decreasing revenue relative to 2022.

{kind=link}

It's impossible to know if the downward trend will continue or if the industry is close to a turnaround point. However, in the long term, the US LTL industry is expected to grow at 3.72% annually until 2028, according to Mordor Intelligence . Moreover, according to Technavio , the global road logistics market will grow at a CAGR of 3.59%. I believe the low expected growth of the LTL and the road industries will increase competitive pressure in the market, vanishing the outstanding financial results during the pandemic. Nevertheless, some markets in the vast logistics industry are expected to grow faster, and ArcBest may be able to capitalize on their growth. First, the On-demand logistics market is expected to grow at a CAGR of 20.8% globally and 16.7% in the US . Second, according to Precedence Research , the retail logistics industry is expected to grow 13% annually; I think ArcBest may capitalize on this growth by improving its inbound logistics solutions. Third, the Global Logistics market will grow at a CAGR of 11.8% .

Risks

Labor Union New Contract

Teamsters have overwhelmingly ratified a new five-year national contract at ABF Freight. The agreement provides members with improvements to wages, benefits, and working conditions, including:

-

A $3.50 per hour raise effective July 1, 2023, with a total of $6.50 in raises over the life of the agreement. The first-year salary increment surpassed all the increments of the precious contract.

-

Two additional annual paid sick days are added, increasing the minimum number of paid sick days from five to seven.

-

The company must increase its health, welfare, and pension plan contributions.

Consequently, it will be more difficult for ArcBest to keep its labor expenses down than 50% of the sales, as the company has to pay higher salaries and make greater contributions to health, welfare, and pension plans. I think the new contract, alongside the higher competitive pressure after the boom, will decrease margins in the following years.

Competition

ArcBest has underperformed competitors who seemed to have done better for their shareholders and clients. Even if past performance may be a poor predictor of future results, I don't see any factor that indicates a turnaround or an improvement in ArcBest's competitive position. Of course, the company keeps investing heavily in technology and the asset-light segment, but we still have to judge the outcomes of those investments after the boom.

Thin Operating Margin

As ArcBest competes with several companies, it's challenging to pass increasing costs to customers; hence, with the new labor union agreement and skyrocketing crude oil prices, the margin could suffer.

Economic Conditions

A recessionary economic climate could lead to declining freight transportation and logistics demand, impacting the company's pricing and profitability. Additionally, economic conditions could adversely affect customers' business levels and ability to pay for the company's services, impacting its working capital and financial obligations.

Valuation

In my opinion, it isn't worth buying or holding ArcBest's shares in the long run as the company has underperformed its peers; it's in a highly competitive market without a clear competitive advantage over other competitors, such as Old Dominion or JB Hunt; has failed to give attractive returns to shareholders since 2006 to 2019 (before the boom); and it has narrow profitability vulnerable to new labor benefits increases and higher crude oil prices. Short-term opportunities can arise, but if technological investment does not improve ArcBest's competitive position, it will hardly generate better returns for shareholders than its peers. Hence, my recommendation is a 'Sell.'

Conclusion

The company is in a highly competitive industry and has underperformed its peers recently. It also faces challenges, including a new labor union contract, increasing costs, and a potential recession. Based on this, I recommend selling ArcBest stock if the investor has a long-term approach.

For further details see:

ArcBest: A Sell Due To Underperformance And Challenges