MRTN - ArcBest Corporation: The Ride Has Room To Run From Here

2023-04-03 08:28:28 ET

Summary

- ArcBest Corporation has done well, for the most part, from a fundamental perspective over the past several months.

- The company has seen some weakness on its bottom line, but shares still look cheap enough to warrant upside.

- Management is also looking to buy back additional stock following an asset sale, which makes sense with how cheap shares currently are.

The perfect investor does not exist. We all make mistakes from time to time. It's because of mistakes that we can get most excited about the opportunities that do work out. Turning bullish on a company, then to see that company's stock price rise over an extended period of time, is a thrilling experience. You can imagine my elation, then, when revisiting ArcBest Corporation ( ARCB ), an enterprise that offers freight transportation services and other logistics solutions throughout North America. Even at a time when the broader market has declined, shares of the company have performed quite well, rising by double digits. And based on the data currently available, the picture for the business still looks to be rather positive.

A fantastic ride so far

In the middle of May of 2021, I ended up writing a bullish article on ArcBest. In that article, I talked about how performance leading up to that point had taken a hit. On top of that, shares of the company looked pricey relative to similar firms. But on an absolute basis, the stock looked cheap and a recovery of the firm looked to be underway. These positives more than offset the negative in my view at the time, causing me to rate the company a 'buy' to reflect my opinion that shares should outperform the broader market for the foreseeable future. And that is exactly what the company has gone on to do. While the S&P 500 is down 1.5% since the publication of that article, shares have generated upside for investors of 10.9%.

{kind=link}

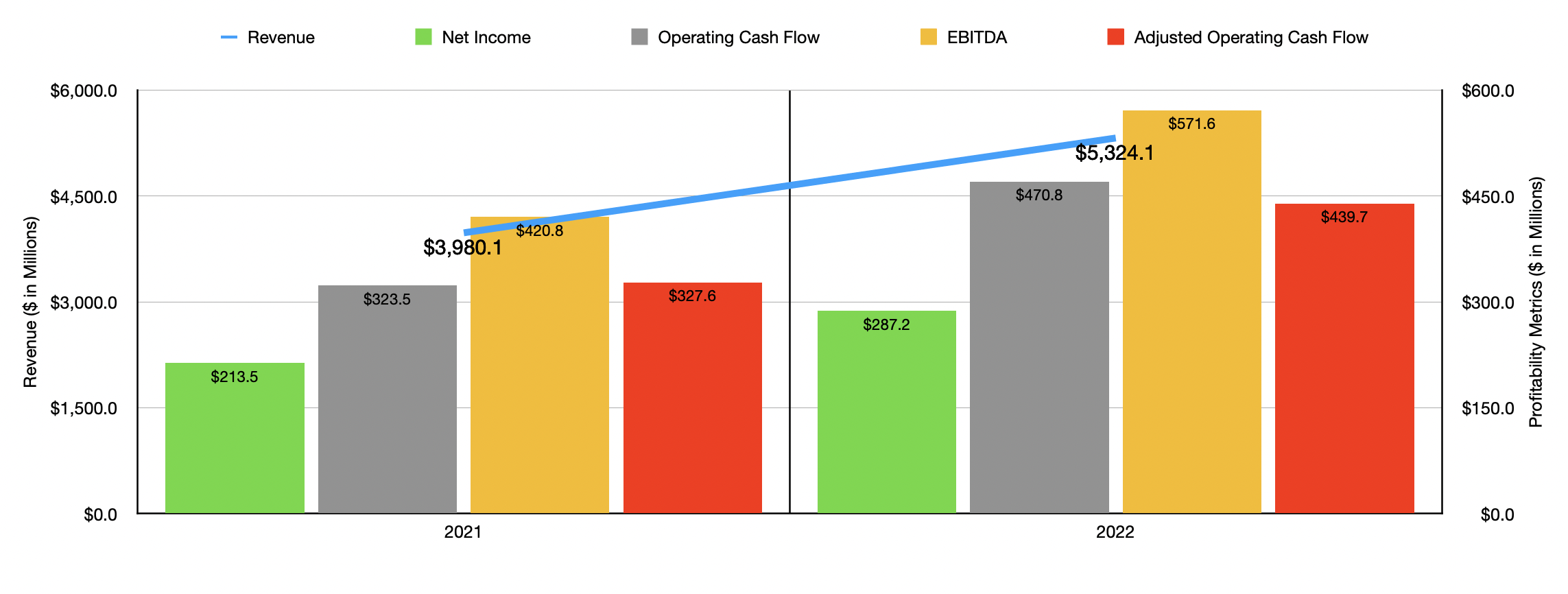

This return disparity has been made possible by robust financial performance achieved by management. Take the 2022 fiscal year as an example. During that year, revenue came in at $5.32 billion. That's 33.8% higher than the $3.98 billion the company reported one year earlier. The greatest chunk of this upside was driven by the firm's hallmark ArcBest operations, with revenue spiking 64.5% from $1.30 billion to $2.14 billion. Even though this portion of the company experienced some weakness in the second half of the year, overall performance was robust, largely thanks to a 58.3% surge in the number of shipments per day. This, management said, was driven by the firm's acquisition of MoLo in November of 2021. The company also benefited from a 3.8% rise in revenue per shipment. The company also benefited from a surge in revenue from its Asset-Based activities, with revenue climbing from $2.6 billion to $3 billion. Build revenue per hundredweight, inclusive of surcharges, grew by 14.5% year over year. But the company also benefited from higher shipments per day and higher pounds per day.

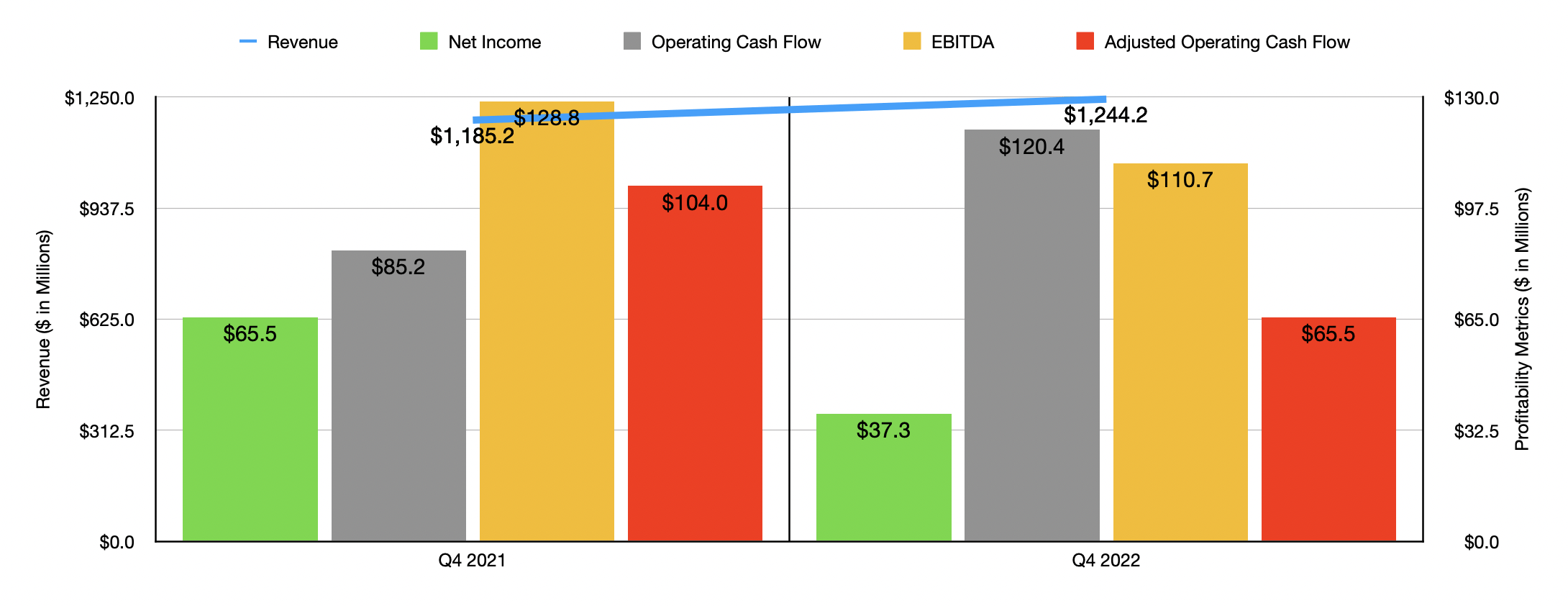

On the bottom line, the picture also benefited. Net income rose from $213.5 million to $298.2 million. Operating cash flow managed to climb as well, growing from $323.5 million to $470.8 million. Even if we adjust for changes in working capital, it would have risen nicely from $327.6 million to $439.7 million. And finally, EBITDA popped up from $420.8 million to $571.6 million. As you can see in the chart below, results were strong, for the most part, even throughout the final quarter of 2022. There were a couple of exceptions here. Adjusted operating cash flow, EBITDA, and net income were all lower year over year. There were certain one-time events that impacted profitability, such as a change in value associated with an earnout involving its aforementioned acquisition. But even without this, profits dropped slightly year over year.

{kind=link}

Shares look cheap

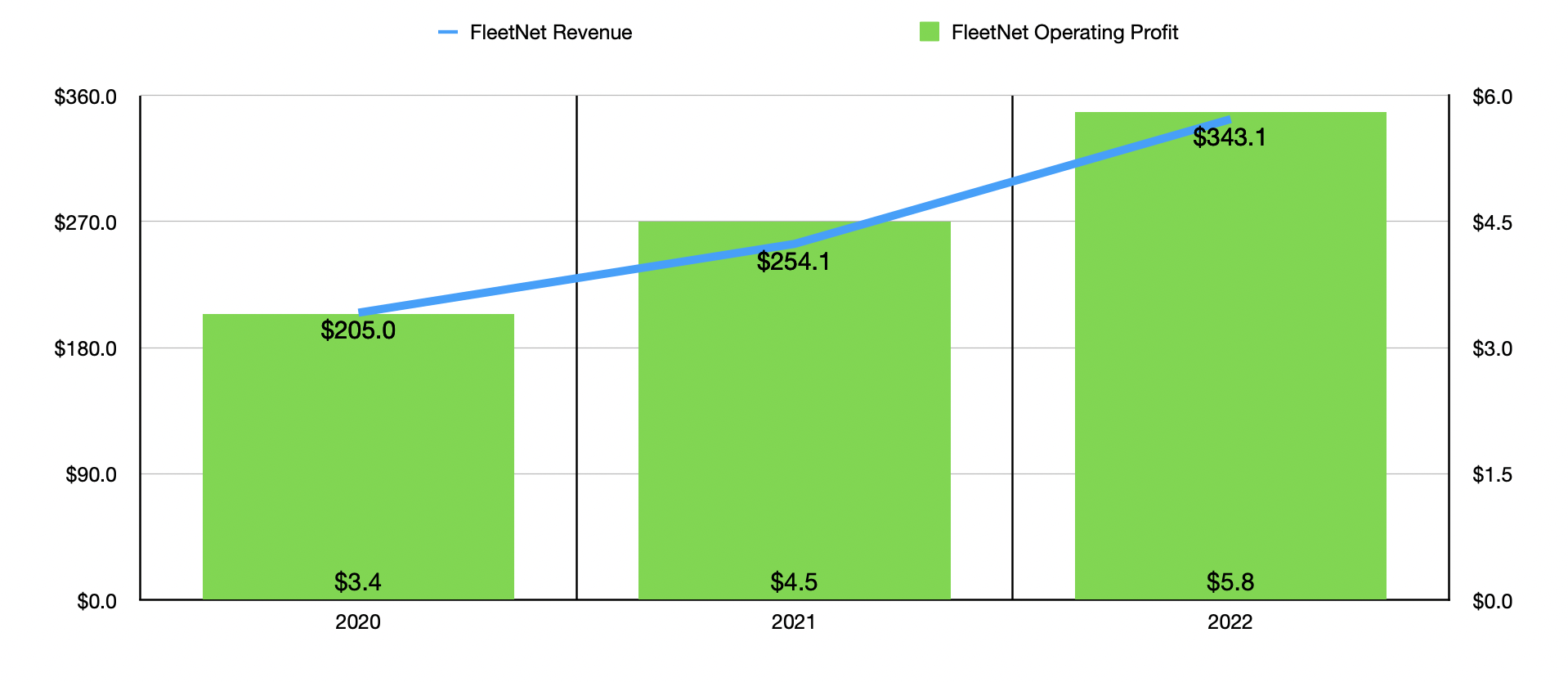

After the end of the 2022 fiscal year, the management team at ArcBest made an interesting announcement . They had agreed to sell off their FleetNet segment in a deal valued at $100 million. This is the smallest of the company's segments, with revenue of only $343.1 million accounting for just 6.2% of the firm's overall revenue and profits of $5.8 million accounting for 1.3% of overall profits. For those who might not remember or who are new to the company, FleetNet includes the company's operations that are dedicated to providing fleet maintenance and repair services, including roadside work.

{kind=link}

This has been a portion of the business that has grown nicely over the past few years, with revenue in 2020 totaling only $205 million. After factoring in taxes and other fees, the company expects to get net proceeds of $75 million from this transaction, booking a $50 million after-tax profit on the business. These proceeds will almost certainly be used to buy back additional stock. I say this because, as of the end of the final quarter last year, the company had only $26.5 million left under its share buyback program. They have since raised that to $125 million. I typically don't care for share buyback programs. But given how cheap shares are, this is a logical move to make.

{kind=link}

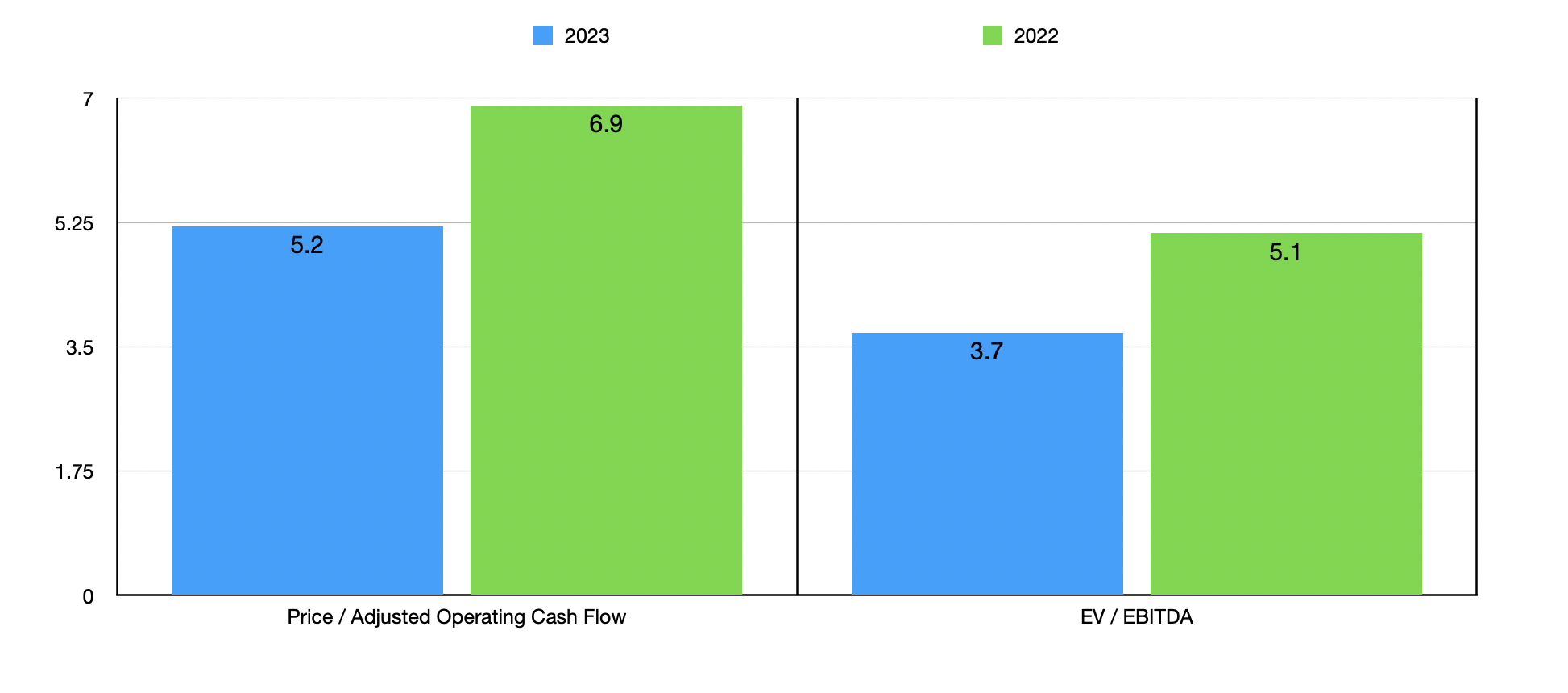

The terms of the deal also make sense when you consider how cheap ArcBest is as a whole. After factoring in the impact that this transaction should have on net debt and profitability, I was able to create the chart above that shows how shares are priced on an adjusted price to operating cash flow basis and on an adjusted EV / EBITDA basis. Though not shown in that chart, the price to total segment operating profit margin of the company is about 5.2 as of this writing. By comparison, FleetNet is being sold off at a multiple of 12.9 when comparing the profits it's responsible for to the net proceeds that management said the company will enjoy.

As part of my analysis, I decided to take the numbers from 2022, and compare the company to five similar firms. On a price to operating cash flow basis, these companies ranged from a low of 3.6 to a high of 7.8. Two of the five firms in this case were cheaper than ArcBest. Meanwhile, using the EV to EBITDA approach, we get a range of between 3.3 and 7.2. In this scenario, only one of the five companies was cheaper than our prospect.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| ArcBest Corporation |

| 5.2 |

| 3.7 |

| Marten Transport ( MRTN ) |

| 7.8 |

| 6.5 |

| Werner Enterprises ( WERN ) |

| 6.5 |

| 5.5 |

| Heartland Express ( HTLD ) |

| 6.5 |

| 5.0 |

| XPO Inc. ( XPO ) |

| 4.4 |

| 7.2 |

| Universal Logistics Holdings ( ULH ) |

| 3.6 |

| 3.3 |

Takeaway

Fundamentally speaking, ArcBest is on solid footing and shares look cheap, especially on an absolute basis. There has been some weakness on the bottom line, but not every quarter can be perfect. The sale of FleetNet is fascinating, since it will allow the company to buy back stock on the cheap. Add all of these factors together and I do believe that further upside for the company and its shareholders is warranted from here. As such, I've decided to keep it rated a 'buy' for now.

For further details see:

ArcBest Corporation: The Ride Has Room To Run From Here