MT - ArcelorMittal: A Global Steel Leader At A Good Price

2023-04-02 01:13:37 ET

Summary

- I have not yet reviewed ArcelorMittal, despite having owned a small stake in the company for a few years at this point. This changes today.

- ArcelorMittal is a global leader in Steel - and I believe at the right price, you should consider the business a definite "BUY" for your portfolio.

- Let me explain to you why when it comes to basic materials, mining, and steel, ArcelorMittal is at the top of my list of interesting businesses I might want.

Dear readers/subscribers,

So, ArcelorMittal ( MT ). I've actually talked about this company in a number of my articles previously. However, I've never reviewed the company in its entirety or constructed a clear, actionable thesis for my followers and readers.

That changes today.

In this article, I will take you through what makes ArcelorMittal a solid investment and why you should consider it at the right price. If you follow my work you know well that I'm not a big fan of plays that are "out there". I like hard things that you can touch - metals, chemicals, and physical products. I do have some growth, software, and IT stocks, but usually, they operate in extremely high-moat businesses that service exactly the companies I write about here, like ArcelorMittal. So for instance, I own several IT businesses that actually do business with MT in various ways. I don't go a whole lot of "left field" in my investments.

MT is a solid business - and I understand it. Here is how I understand the business and its appeal.

ArcelorMittal S.A. - Presenting the company

Understanding ArcelorMittal takes some time. The company is a Luxembourgish-Spanish-French (and Brazilian) steel company, and its headquarters are in Luxembourg.

The company can trace its history back to the mid-70s, and some of its assets can trace their histories back to the 19th century. What the company does, is research, development, and mining of steel. The company is one of the largest on earth in this, and produces over 90M tons of steel per year, including 200 unique grades of steel for automotive purposes alone, many of which did not even exist prior to 2007.

The company has come a long way in a short time. Its research and products have driven entire industries forward, improving the quality of metals produced.

The company was formed by combining/taking over West European steel maker Arcelor with Indian steelmaker Mittal. At the time, there was actually a planned merger between Arcelor and Severstal out of Russia (thankfully, that one didn't go through), but Mittal decided to launch a hostile takeover bid, with headquarters in Luxembourg.

ArcelorMittal produces around 10% of all the steel in the entire world. The company generates revenues of between $50-$75B usually, from which it manages to generate a mid-single digit EBITDA. Or, as in the year of 2021, that EBITDA came to just over $19B. It usually manages around $1-2B in FCF. Its current production numbers are around 60-70MT of steel shipments per year, with another 50M tonnes of iron ore.

ArcelorMittal is a steel industry leader . Its profitability numbers when put into context in the larger industry are consistently in the 60-80th percentile in mining/steel, especially when it comes to company RoIC, which is above the 80th percentile. The company furthermore has industry-leading, or among the top ratings in debt/asset, debt/equity, and interest coverage ratios. In layman's terms, ArcelorMittal has very few issues with debt.

This combination of record/high profitability, excellent fundamentals, and superb growth numbers , is what forms the foundational bedrock for the positive overall thesis on ArcelorMittal. The only even somewhat significant risk that I could perceive when going through the company's books and numbers is a building number of days of inventory - but that's pretty much it.

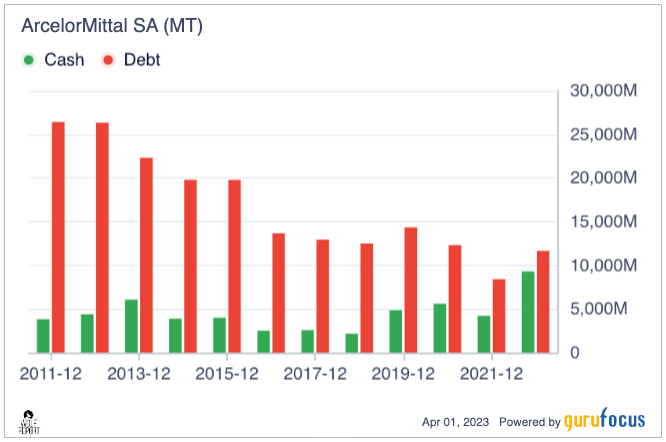

Take a look at the debt development, which is more or less exactly what you'd hope to see going into this interest rate environment.

{kind=link}

MT works with a geographical operating structure, as well as a separate "Mining" segment. Most of the company's business, and by most, I mean over 58%, is done in Europe. Aside from that, we have 17.2% in NA/FTA, 15% in Brazil, and 7.3% in Africa. The company manages GM of 15.7%, OM of around 13%, and a net of 11.7%.

Most of the money, as you'd expect from this sort of company, is COGS.

The company is in the midst of a strategic review and transformation - but its 2022 numbers were absolutely solid. EBITDA wasn't as high as 2021, but that was a record year - and MT still managed to generate $6.4B of FCF, recording a book value per share of $62 at an RoE of 20%, with a record low net debt of less than $2.3B.

This makes the company one of the least indebted companies in the entire metals sector.

{kind=link}

One of the company's primary risks has always been the ups and downs of the metals industry overall. This has led to relatively poor downcycle returns, that have impacted long-term RoR. ArcelorMittal, like most companies afflicted by the same, is trying to up their resilience to the cycles. Me, I say that these sorts of companies will always be cyclical, and you should adjust accordingly. There are times to buy them, and times not to.

The high-level market trends for MT are showing early signs of slight improvement. Inflationary pressures are serious, and negative economic sentiment has led to a slowing in real demand, along with a decline in steel prices for the end of 2022 years - but these unsustainably low spreads are starting to recover. Energy prices have also recovered, making certain underutilized assets more attractive again.

In short, we're seeing structural improvements to the entire industry, and this means that MT is also enjoying some of those trends.

MT is one of the leaders in low-carbon steel in the world.

{kind=link}

The company is refocusing its asset base, with cost improvements, and strategic aims to add another $.13B to the company's EBITDA in higher growth markets and categories. Along with the more important steps, cutting China capacity to respond to this nation's secular decline in demand and addressing some of the unfair trading going on there. New capacity is instead being planned in legacy areas.

{kind=link}

And strategic CapEx is being put to work in both renewables and mining - not just in legacy or Asia, but in Africa as well. One of the advantages that I see with investing in French or originally french companies is that their cultural heritage and the history of globalization/colonization gives the nation's companies an edge in competitiveness in Africa, where many other companies fail. This does not just mean in Basic Materials - I invest in Telecommunications where emerging growth markets in Africa constitute significant income. MT is another good example of a company that makes Africa "work", albeit slowly.

I believe it's fair to characterize the company's balance sheet as somewhat of a fortress given the development we've seen over the past 15 years. Take a look.

{kind=link}

While the dividend paid by the company is somewhat volatile, especially since it did not have one in 2020 due to COVID-19, MT is targeting a progressive and positive shareholder policy, and for the current year, despite lower EBITDA, it has raised this dividend to $0.44/share, which for the MT ticker represents a yield of nearly 1.5% (the information on the SA summary page is not yet correctly updated). This is not a high dividend, but you're investing in world-leading profitability steel, so maybe that is enough as an argument.

{kind=link}

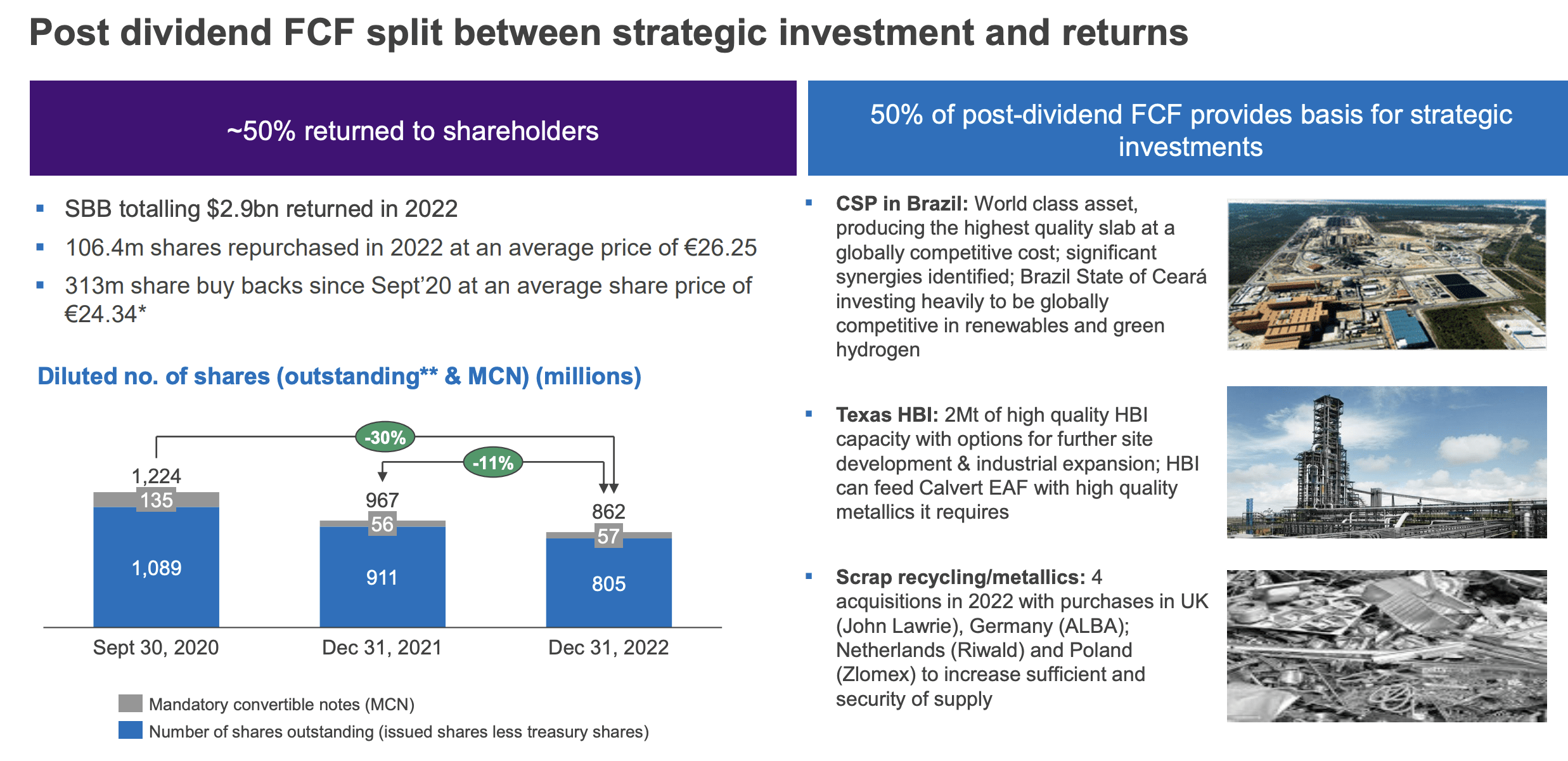

The company's outlook for 2023 is mainly positive. The company expects the world, minus China, to mostly recover as compared to 2022, which is resulting in shipment growth by around 5%, with positive FCF generation in the $4-$5B range. China is expected to slow down, but that's the only geography where this is expected. The company is also in the midst of a buyback program.

The main recent impacts for the company were late 2022 destocking due to the significant macro events. These are slowly unwinding. There's also the Ukraine war, and while we can't forecast when this will end, I believe it fair to say that it will eventually end, with corresponding effects for companies such as this one.

Let's move to valuation and see what we have going for us at this time.

ArcelorMittal Valuation - It's attractive, but there are alternative investments

ArcelorMittal is a strong company at a good valuation. It's one of the best companies in the mining and steel industry. Frankly, from any conservative perspective, a sub-$35/share valuation really is what I would consider an "insult" to the company's long-term capacity and capabilities.

Due to its significant conservative, financial strength, and solid operations which I view as quite resistant to macro from a perspective of basic materials, I assign the company a higher premium than I might otherwise to this sort of business.

MT "plays" in a sector that includes other big fish companies. These are Mitsubishi, which are larger in terms of market cap, and Nucor ( NUE ), which is also larger. They also include companies like Nippon Steel, JSW Steel, Tata, and others.

However, MT has one advantage. All of the ones mentioned are companies that I would view as either being fairly valued or overvalued at this time. ArcelorMittal, meanwhile, is attractively valued despite a recent spike in the share price.

Am I being too positive? I do not believe so. The company is trading at 0.34x to sales, 0.39x to revenue, and less than 7x normalized P/E on an NTM basis. The share price targets from 12 S&P Global analysts that follow the company at this time come to a range between $27 to $52, with an average of $38 - remember, below $35 is what I view as "insulting" to the company. The Book value per share alone as of 4Q is over $60/share. The least I'd want for that is a 0.45x or a 40% discount to that value. On that basis alone, we're over $35/share, which gives the company an upside of over 20% at this time.

Based on current macro trends and where things seem to be going, I forecast a slow growth year-over-year - around 3% to 2024, and another 1-2% to 2025E. Even if you just forecast the MT ticker at say, 5-6x P/E, that's still a 16% upside annually or more, or 50% total until 2025E, on one of the largest steel businesses on earth.

And that, dear readers, is a conservative upside, as I see it. I've owned MT since about the last downcycle, and I haven't sold my meager holding (less than 0.15%). I'm slowly looking to add here. What I want out of my investments is underappreciated/undervalued, above-average quality companies , typically sector leaders (or at least better than average), with a yield.

And one of my primary requirements is that I can see my way to a 60-100% RoR in 2-5 years and that this must be based on a conservative estimate, or stable 40-60% RoR if I'm looking at a sort of "Income investment".

I forecast MT at a higher P/E than the 5x - I believe the company may, on the basis of its quality and earnings, go to 5.5x or 7x normalized, and this pushes the RoR potentially above 18.5% annually, or 60% until 2025E, meeting my overall stated investment goals.

There are definitely other attractive potential investments out there - there's no doubt about that. However. MT is a solid one worth noting - and here is my current thesis for the company.

Thesis

- My thesis for ArcelorMittal is currently a positive one for one of the leaders in global steel. I view the company as investable on the basis of its sector-leading low debt and coverage and decent upside. There are "better" investments out there, meaning higher upside with decent safety, but if you want exposure in this sector, there aren't many companies that can measure up to ArcelorMittal.

- Based on this, I go into the company with a "BUY" rating, and I'm planning to add to my current position in the business.

- My PT for MT is $37/share conservatively, with the company currently trading at less than $31/share.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

I won't call the company "cheap" here, but it does fulfill all of my other criteria for investing, making it a "BUY".

For further details see:

ArcelorMittal: A Global Steel Leader At A Good Price