MT - ArcelorMittal: Executing Properly On Market Profile Normalization

2023-06-16 11:59:26 ET

Summary

- ArcelorMittal benefited from the improved steel market conditions to deliver strong results in Q1 2023.

- With the CSP acquisition and two furnaces coming online in Europe, the company is strongly positioned for profitability improvement in the challenging second quarter.

- The valuation discount compared to U.S. peers expanded, which opens a 2x fundamental potential for MT stock.

The destocking cycle has come to an end, which could give a positive tailwind to the steel industry. Against this backdrop, I believe it’s worth considering an investment in ArcelorMittal S.A. ( MT ). My previous piece suggested that MT could rebound after passing this point, and indeed, the improved market and demand profile is reflected accordingly in the first quarter financial performance. Going forward, the macro headwinds are still in place to restrict the demand from steel-using sectors, but MT is well positioned to deliver above cyclical growth. In particular, the company is reinforcing its business model with CSP acquisition and strategic investment projects, which gives a reasonable assurance that MT could go through the challenging second quarter with a profitability gain and explore the gradually improving market conditions to deliver resilient financial performance going forward.

Financial overview

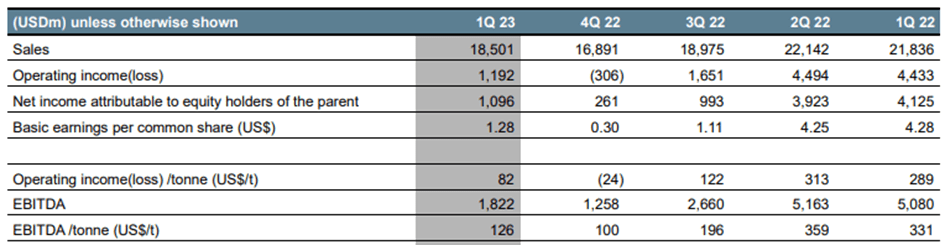

The first quarter of 2023 was marked by the end of the destocking cycle peak, which supported apparent steel consumption growth and steel spreads rebound. The improved market conditions were reflected accordingly in the company’s financial results, where total sales reached $18.5 billion , making a 9.5% sequential increase, thanks to the 10.1% increase in steel shipments.

Q1 financial results (company earnings release)

{kind=link}

Segment-wise, it’s worth noting the NAFTA segment, which registered a solid performance of 14.6% QoQ growth in revenue to $3.35 billion. Shipments were 21.6% higher compared to Q4’22 and benefited from overall consumption improvement in the US, strong flat operations in Mexico and Canada as well as increased slab volumes sourced for Calvert. The Brazil segment contributed $3.07 billion (+6.0% QoQ) to the consolidated revenue on a strong shipment growth of 11.3%, partially benefiting from the acquisition of CSP. Despite the Europe segment being hindered by the operating challenges during the quarter, the revenue advanced by resilient 8.2% from the previous quarter on 14% higher shipments following the improved activity of steel using sectors. The revenue from ACIS and Mining segments both reported double-digit growth on improved production in Ukraine and recovery of South Africa’s shipments.

The positive top-line performance of the main segments and JVs didn’t bypass operating efficiency. EBITDA for the quarter reached $1.82 billion, where the $26 EBITDA/tone gain compared to the last quarter resulted in a profitability improvement by 240bps up to 9.8%. Bottom-line, net profit for the period amounted to $1.1 billion, or EPS of $1.27 compared to $0.30 in the previous quarter, which included $1 billion impairment charges.

Outlook and forecasts

It only costed for MT to enter into the post-destocking cycle to showcase strong financial results. The first quarter exhibited some positive trends indeed, but the market environment is still not the most favorable one. The company’s financials are still in the red zone when compared to the respective period of last year, which is fair enough due to the elevated steel prices in 2022. However, the market conditions are improving, and in order to get some vision on whether the company could maintain such positive trends seen in the recent quarter going through the year, we can turn to steel using sectors dynamic.

Despite the war-related disruptions and macro headwinds, the blend of favorable development in engineering, construction and transportation through 2022 led to a positive output dynamic in the EU. The trend of weak demand conditions so far is expected to be present in 2023 as well, bringing uncertainty to the global industrial prospects. Real steel consumption is projected to increase marginally (+0.3%) this year, where only the second quarter is about to see a decrease. In the meantime, the apparent steel consumption is expected to decrease (-1.0%) in 2023 overall mainly on weak first half of the year. However, the mentioned developments (increase in the real and decrease in apparent steel consumption) are actually supportive for the steel industry and could accelerate the withdrawal of accumulated inventories. And although this could provide for a positive momentum in the steel sector, the ongoing macro uncertainty is set to continue restricting the growth prospects over the next few quarters.

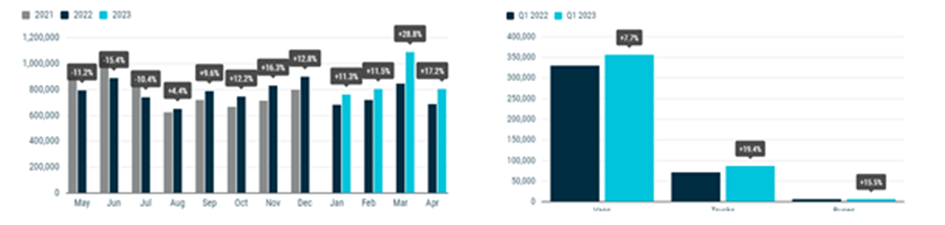

In particular, the construction industry is currently experiencing bearish developments and is forecasted to stagnate in 2023 by 1.6% due to the construction materials bottleneck and overall economic slowdown in the EU. On the opposite side, the automotive sector’s output is expected to increase by 1.2% and become the main contributor amid the steel-using sectors. The reasoning behind this could be a strong double-digit growth in new car registrations since the beginning of the year, because of the improvement of semiconductor availability.

EU new passenger car and commercial vehicles registration (ACEA)

{kind=link}

The alleviation of the supply-related disruptions, which used to force heavy vehicles output in the dense red zone, resulted in a strong performance of the commercial vehicles market in the first quarter as well.

Although the second quarter of 2023 is expected to be challenging in the steel-using sector, I believe ArcelorMittal could deliver an above cyclical performance. In particular, the acquisition of CSP could bring the EBITDA run rate in the Brazil segment up to $600 million. Although, we may not see this happening in the second quarter due to the time needed to fully unlock the synergy benefits, and potential integration-related costs. Still, the CSP is coming online to the company’s business model at the right time to strengthen MT’s offering with the additional 3 mt capacity and support its financial performance. Add to that the improvement in steel spread since the beginning of the year, which will be reflected in the coming quarters due to the lags. Going forward, the Europe segment's performance could be underpinned by Gijon and Dunkirk furnaces, which were set to be restarted in June. Overall, the following table delineates my forecasts regarding MT’s revenue and EBITDA for the second quarter and FY2023.

Forecasts for Q2 and full 2023 year (company reports; author’s estimates)

The company expects to deliver resilient shipments in the second quarter in the NAFTA segment, hence the estimates incorporate an 11.2% QoQ (+2% YoY) revenue increase. The Brazil segment is estimated to follow with a 6.5% sequential growth (-18% YoY) and $500 million contribution to the quarterly EBITDA line, as the CSP could emerge with full synergies in the next few quarters, in my view. Next, the Europe segment could be strengthened with the restart of both Spain and France furnaces to deliver a 4.8% QoQ growth (-8.6% YoY).

With the above assumptions, I estimate the company’s Q2’23 revenue to grow by 13.7% QoQ (-5.0% YoY) and reach $21 billion, with EBITDA of $2.4 billion on a margin of 11.6% (-11.4 pp YoY). For the 2023 full-year, the estimations led to revenue growth of 6.4% YoY ($84.9 billion) with EBITDA of $9.4 billion, down 33.8% on a margin of 11% (-6.7 pp).

Risk factors

Although the inflation and energy prices pressure abates, operational challenges at major production facilities could significantly drag down the company’s financial performance. In addition, a slowdown in the automotive, engineering and construction industries due to ongoing macro headings could restrain the prospects for steel manufacturers.

Investment takeaways

I will uphold to my valuation model, selecting Steel Dynamics ( STLD ), Cleveland-Cliffs ( CLF ), United States Steel Corporation ( X ) and Nucor ( NUE ) as a peer group in order to derive the sector EV/EBITDA forward trading multiple.

Comparable valuation (Seeking Alpha; author’s estimates)

MT is currently trading at EV/EBITDA forward multiple of 4.0x, which represents a discount of around 77% to the sector’s median of 5.2x, derived from the above selection. It’s worth noting that the MT’s discount expanded notably from 60% estimated in my previous valuation, and applying the above EBITDA forecast, the calculations should yield an enterprise value of $48.4 billion. Subtracting interest-bearing and pension-related liabilities, we should arrive at an equity value of 45.7 billion, which corresponds to $56.7 per share and implies 101.5% upside potential.

I am raising my outlook on MT shares to Strong Buy, as the company is trading at a significant fundamental discount to its main US peers. I am inclined to believe that ArcelorMittal could become 2x the current market price, since there are emerging signs of steel market normalization and demand profile recovery following the post-destocking cycle. I believe MT could gain up to 200bps of profitability improvement on the EBITDA line in the second quarter due to the positive price lag and acquisition of CSP. The latter could provide for a decent improvement of the Brazil segment and came at the right point to support the company’s performance ahead of the expected tough Q2. Moreover, ArcelorMittal’s strategic capital investment projects for high quality assets with a strong potential for synergies could place up to $1.3bn profit on the EBITDA line in the next few years to come. In addition, the management launched a new $85 million buyback program for a two years period, committing to the strong prospects for the company going forward. And looking at the company’s prospects in 2023, the market conditions are expected to see a slight improvement, where the automotive sector is subject to ensuring a resilient steel demand. This provides for a decent potential, since MT has a leading position in the market for AHSS and prevailing exposure to the flat rolled products demand.

For further details see:

ArcelorMittal: Executing Properly On Market Profile Normalization